Article Link: Text “simple” to 314-665-1767 to download the Hui Google Drive files and the 2018 Rental Property Analyzer

For a free electronic version of my bestselling book in 12+ categories text the word “ebook” to 587-317-6099.

Please help the show by leaving a review: http://getpodcast.reviews/id/1118795347

Join the Hui Deal Pipeline Club! SimplePassiveCashflow.com/club

Pardon the grammar – I’m an Engeneer, Enginere, Engenere… I’m good with math!

________Here are the Show Notes________

Is dealing in Cryptocurrency dangerous?

Bitcoin grew in value by 1,000% in 2017.

Ripple was the best performing crypto, which had gains of 36,018% last year due to its ease of use. Each coin of Ripple is worth a small fraction of a Bitcoin. The technology makes it easier for banks, payment providers and businesses to send payments globally. They promise to deliver an experience that is instant, traceable, and inexpensive.

NEM is an enterprise blockchain with “smart assets.” It can also be used to manage things like currencies, financial instruments, supply chains, and notarizations. Think how eBay or Amazon takes data from UPS or USPS to track your packages, but a lot bigger.

Other Cryptos:

Ardor

Stellar

Dash

Ethereum (2nd biggest Cypto)

Golem

Litecoin (getting in mainstream vernacular)

BitcoinLearningCenters.com by Andy LaPointe

Mr. LaPointe created this complete bitcoin learning system from the ground up!

You will learn practical insights into this global phenomenon. By the end

of the interview, you will also have a practical understanding of

cryptocurrencies, blockchain technology and Bitcoin.

The information that Andy LaPointe will share is entertaining, insightful and easy-

to-understand. No matter who you are or your background, the information he’ll

share will help anyone to get started with cryptocurrencies today.

You listeners will learn:

– What is a Blockchain?

– What is Bitcoin?

– What is cryptocurrency?

– How blockchain and Bitcoin are related.

– How to determine if investing into cryptocurrencies is right for you.

– What are some of the misconceptions about Bitcoin, cryptocurrency

and blockchain.

– How to create the right cryptocurrency portfolio for you and your

financial future.

– And much more!

ABOUT THE AUTHOR:

Prior to getting involved with blockchain technology in 2013, Mr. LaPointe spent 15 years in the corporate world as a Registered Investment Advisor (RIA), Series 7 Stockbroker and Mutual Fund Wholesaler. He offers deep knowledge of the financial markets, blockchain technology, asset allocation, risk tolerance and cryptocurrency.

Andy LaPointe lives in Northern Michigan and is available for interview by calling 1-231-676-0643 (Eastern Standard Time) or email: lapointeandy@yahoo.com

– Instant Availability

Or visit: www.BitcoinLearningSystems.com

SPC followers are typically younger than 30 or older than 35. My observation is that when people have kids, that takes all precedence.

Launch 2019 with a 50-minute goals brainstorming session.

(we will not be talking real estate investing – the second half of the presentation will be our 2018 Quarterly recap – this will likely take us another hour… please stay if you can or listen on slient)

Here is the editable worksheet to follow along link

Topic: https://simplepassivecashflow.com/2019-launch/

Time: Jan 5, 2019 9:00 AM Pacific Time (US and Canada)

On the last day of 2019… I will be immensely satisfied when I…

[Get down to 155 lbs and raised $3M in fund]

If it does not scare you bit… Its not high enough.

If you accomplish it what will it give you?

[A level that I can maintain and focus on quality.]

In TEN YEARS… I will be immensely satisfied when I…

[$25k passive a month with still being able to interact with a person a day.]

“We over estimate what we can do in one year and underestimate what we can do in ten years” -Tony Robbins

5 things you did NOT accomplished in 2018?

[Weight goals

Find a new hobby outlet

Operate in a less frantic mode]

Why not?

1) Disconnect

2) surrogate to accomplish the same why

3) used the wrong strategy

4) lacked knowledge/resources/people

5) you took the easy way

6) crabs in a bucket (peer group)

Creating the plan…

Break down the goal in four chunks:

1) Complete routine of activity 3 days a week

2) Evaluate progress in March 1

3) Possible add 4/5th day of activity

4) Evaluate progress in June 1 and at that point address diet

3 People hack: 1 person above you, at your level, and below you that you mentor

Setup environment

Four tendencies: upholder, rebel, questioner, obliger

Rewards

Taking action

Scheduling in the calendar (not recurring cause it won’t be special)

Every two weeks review big goals

Would you like an accountability partner?

Most of you folks are hard-charging achieving types who listen to my podcast at 2X speed. For once you need to stop that just for this exercise.

Set the timer for 20-40 minutes and get into the right State.

Getting into this State is critical. Music, a little wine, whatever floats your boat…

Get a pen, paper, (or your computer/mobile device) and a quiet space and here we go…

The group coaching is something that I have been trying to put together a couple years now after I accumulated a lot of content and got a feel for coaching students these past few years in a one-on-one setting – see SimplePassiveCashflow.com/coaching

I’m code naming this project, “The Journey to Simple Passive Cashflow” and it will consist of:

1) 27 weeks of curated content with concepts building on top of each other

2) Participants go through those modules together and are able to interact on the Bi-Weekly Call and the Private Facebook group in a “group study” environment

3) Bi-Weekly hour power calls switch between the topics of a) Acquiring you direct investment and b) more high-level wealth building concepts and syndication education

It’s going to be a really cool format where people take the journey together. Think like a Fraternity/Sorority without the weird stuff. When I was going through programs it was most beneficial to connect and climb the ladder with quality people. Who knows someone of your Cohorts might do a deal together or become lifelong friends or accountability partners.

1) Currently open for investors – 101-Unit Class C in Gulfport MS

2) 30% – MFH Apartment

3) 90% – Finally a Non-MFH fund syndication (where I do the admin/accounting) to lower costs and get higher prefs and lower minimal investments. Q2 2019

Current investors in past deals let’s meet up when you are in Hawaii. Non-investors you can still kick it with Lane

The Hui Deal Pipeline Club is a free investor club where I filter investments and underwrite the numbers and partners myself. Unlike other investor lists and groups, my investors have personal access to me and know that I personally have skin in the game investing alongside with my investors.

We have acquired over $155 Million dollars of real estate acquired by syndicating over $13 Million Dollars of private equity since 2016.

Track Record of success:

15 Apartments Buildings Purchased, 2 Manufactured Home developments, and an Assisted-Living Facility

2,100+ total units

10 US Markets – AL, GA, IN, OK, LA, IA, TX, WA, PA, MO

Started investing in 2009 – 9 years of experience

Countless Mastermind and Mentorships in the Live & Virtual clubs through the education platform at SimplePassiveCashflow.com

2,600 investors and 100 new Kool-Aid drinkers every month!

Article Link: Text “simple” to 314-665-1767 to download the Hui Google Drive files and the 2018 Rental Property Analyzer

For a free electronic version of my bestselling book in 12+ categories text the word “ebook” to 587-317-6099.

Please help the show by leaving a review: http://getpodcast.reviews/id/1118795347

Join the Hui Deal Pipeline Club! SimplePassiveCashflow.com/club

Pardon the grammar – I’m an Engeneer, Enginere, Engenere… I’m good with math!

________Here are the Show Notes________

Graham Parham: New Awards:

#1 in units at Highlands Residential Mortgage for 2017

#11 in state of Texas and 92nd in the US according to The Scottsman Guide and

Mortgage Executive Magazine – 1% top originators in the US

Top Ranked – Ask A Lender

Discussion today is 1-4 unit income properties, not owner-occupied.

20% down on first ten financed properties? 25% for 2-4 units?

DTI considerations when using HELOC from primary residence to invest?

Credit scores down to 620. Max. credit score that helps?

Reserves?

New Fannie Mae Reserve Requirements for Investors with Multiple Properties Owned

The Old requirements were six months Principle, Interest, Taxes, and Insurance (PITI) on the subject property and two on all other properties up to 4 leveraged 1 – 4 family properties excluding the primary residence. Properties 5 – 10 would require six month PITI on all properties.

The New requirements are based on a percentage of the unpaid principal balance on each loan excluding the primary residence.

If a borrower has 2-4 financed properties, the reserves of 2% of the unpaid principal mortgage balances are required, excluding the principal residence and the subject property.

If a borrower has 5 – 6 financed properties, 4% of the unpaid principal mortgage balances are required, excluding the principal residence and the subject property.

If a borrower has 7 to 10 financed properties, 6% of the unpaid principal mortgage balances are required, excluding the principal residence and the subject property.

The aggregate UPB calculation does not include the mortgages and HELOCs that are on

the subject property,

the borrower’s principal residence,

properties that are sold or pending sale, and

accounts that will be paid by closing.

The subject property will still have monthly reserve requirements based on the total mortgage payment (PITI). Reserves are funds that you have access to liquid or non-liquid. Reserves are funds you need to have after the closing your transaction. Funds for reserves cannot be your funds for down payment or closing cost.

Fannie Mae now will allow for 100% of the Non-Liquid funds, not 60%

Non-Liquid funds can be used for reserve requirements.”

IRA’s

401K’s

SEP Funds

Gifts are NOT allowed on an investment property.

Investor interest rates how much higher than owner-occupied?

Mortgage sequencing. Example: if buyer wants to buy in Memphis today, Jacksonville next month, how should they plan?

Overall, lending climate more lose or tighter than 1 year ago? 5 years ago?

What should a prospective borrower do before contacting you?

1031 exchanges Cost and funding

What cost are covered in the exchange

What is UP with interest rates?

4 Factors that determine your mortgage interest rate:

Credit Score

Credit Scores Adjustments

740 +

740 – 720

720 – 700

700 – 680

680 – 640

640 – 620

% of down payment 20% or 25%

Loan Amount Adjustments

Property Type

What about the 15 Year fixed?

Does it make since to pay points?

What is the difference between Mortgage Brokers and Mortgage Bankers?

What are overlays?

Does Fannie Mae have a black list?

Are Appraisals regulated and by who?

Is there an appraisal black list?

What happens if the appraisal does not come in a contract price?

Closing cost differences between lenders

Should I pay cash for my investment properties or use leverage?

The next example will show the benefits of using 20% down leveraging for properties versus buying one property and paying CASH.

If you pay $150,000 in cash for one property, your net cash flow is $1245.00. By putting 20% down with an 80% loan to value and a 5% interest rate, your net cash flow is reduced to $600.81. Let’s not stop there. Keep in mind that 20% down payment on a $150,000 home is only $30,000. If you bought FIVE $150,000 homes and put 20% down on each with the same loan terms and monthly rents, you could increase your return on investment by $1759.05 a month to $3004.05. Invest your money wisely.

The net cash flows do not take into account the annual city, county and state property taxes and the annual hazard insurance. The numbers may vary considerately by the taxing authorities. You will have to include that information in your bottom line.

Graham W. Parham has been a Mortgage Loan Officer for over 18 years with 25 years

in sales and marketing. He is a leader of financial expertise in the North Texas

residential real estate market, developing a significant following among homebuyers

and investors. Known and respected industry-wide, Graham’s production consistently

ranks him as a top producer in this market place. According to Scottsman Guide

Graham ranked 92 nd in the US loan originators.

Graham offers invaluable insight into a purchaser’s likely requirements, providing an

exceptional business ethic of customer service and respect, catering to their needs from

pre-qualification to closing. He is a truly dedicated person, who strives to ensure that

each transaction is handled in a timely and stress free manner. By employing these

standards, Graham has established a solid reputation for going the extra mile to put

together the absolute best financing available for his clients. Graham prides himself on

staying ahead of the curve, keeping up to date with the latest products and industry

trends.

As an active investor himself, Graham has a strong insight on what his investment

buyers are looking for to accomplish their short and long term goals. Knowing that

investment loans strongly scrutinized, it is up Graham his team of underwriters who

understands rental property loans versus that of an owner occupied residence. His

general knowledge of REO properties and Turnkey providers coupled with a strong

operational staff allow his loan closings to be seamless and “On Time Every Time”

Highlands Residential Mortgage, LTD. is completely submerged in the real estate

investing industry and has access to many lenders nationally. Our clients benefit from

up to date guidance on all conventional investor loan programs, and less known

creative financing strategies. Knowing that an investment loan will be far more

scrutinized, it is Graham Parham and his team of underwriters who understand a loan

processed for a rental property versus that of an owner occupied residence.

Just as you would not seek legal counsel from someone who does not have a law

degree, nor should you trust a loan originator for your investment property loan from

someone that is not an investor themselves. Highlands Residential Mortgage, LTD. is

an unparalleled mortgage lender whose delivery sets us apart!

Graham Parham’s team mission is to consult every investor based on those

individualized situations and goals. Whether you are buying your first home or

investment property, we carefully look at your options that will give you the best

opportunity for success. Because we know how important your investment financing

strategy is, our extensive research and knowledge of those programs will be brought

forward in educating you as an investor, throughout the lending process.

“My goal is to continue assisting my clients for life and help them meet the ever-

changing needs life throws our way!”

To get access to the lending guide please sign up below:

Erin Lowry (https://brokemillennial.com/) is the author of Broke Millenial, a book about how to stop scraping by and start getting your financial life in order.

She talks about how she learned about finances at a young age, how she gave up her dream school so she could live her dream life, and how living in New York inspired her to write her book, Broke Millenial.

“Invest your spare change,” may be a catchy line but you really can’t invest your spare change to wealth. It has to be more than spare change.

In the financial world, you are above nothing. Just because you have a college education doesn’t mean that is your way out of financial difficulty. You also need to be prepared to take non-professional jobs or jobs that might be below you.

Just like in any financial goal you have to figure out how to take a high-level idea and break it down into smaller parts. Think of whatever your long-term financial goals are and work backwards to break it down into something that is actually more achievable. A lot of people in their early twenties have beautiful, lofty dreams but no tangible steps on how to get themselves there.

Podcasts are great sources of information.

Saving is important but earning more is bigger. To earn more is a key part of building wealth.

The biggest thing when it comes to feeling in control of your money is that you have to identify what you truly value. Don’t allow other people to dictate where you should spend your money.

As a real estate investor, imagine using Cost Segregation as a real property investment strategy that will grant you tax free cash flow from fixed assets and allow you reinvest even more (and possible lower your ordinary income).

What is Cost Segregation?

This is one of the easiest and fastest ways to squeeze a little extra profit out of an investment. If you have ever played those racing video games where you modify your car (like Gran Turismo) it’s like paying for that cheap computer chip upgrade to get an extra horse-power boost, it’s a no-brainer.

For those of you who aren’t ex-gaming nerds like me, it’s “low-hanging fruit”.

A cost segregation study gives a tax benefit to the taxpayer to take advantage of current bonus depreciation laws (starting to phase out slowly in 2022) in order to depreciate their assets by taking a loss on paper.

The cost segregation specialist/engineer analyzes the components of a commercial real estate asset to create a cost segregation report to equip the tax accountant or CPA the needed breakdown of the asset in order to make the depreciation determinations.

To better understand the benefits of performing cost segregation, you must first understand depreciation.

Depreciation is where you reduce the value of your assets (in this case, your real estate properties) due to natural wear and tear over time. There is a type of depreciation wherein the value of your fixed asset (real estate properties) depreciates faster than it should be. This speedier depreciation or most commonly known as accelerated depreciation.

Let’s look at it in detail: If you own commercial or residential real estate investments, you can depreciate your real estate holdings. A commercial property establishes a 39-year depreciation schedule and a residential property establishes a 27.5-year depreciation schedule. These are the numbers we will use to calculate the rate of our depreciation deduction.

Above link is for smaller assets. Larger assets will likely require other vendors that we use on our assets. Join the club for access.

Real K1 from a past dealReal K1 from a past dealReal K1 from a past deal

Above: Example of a cost segregation estimate for a past deal

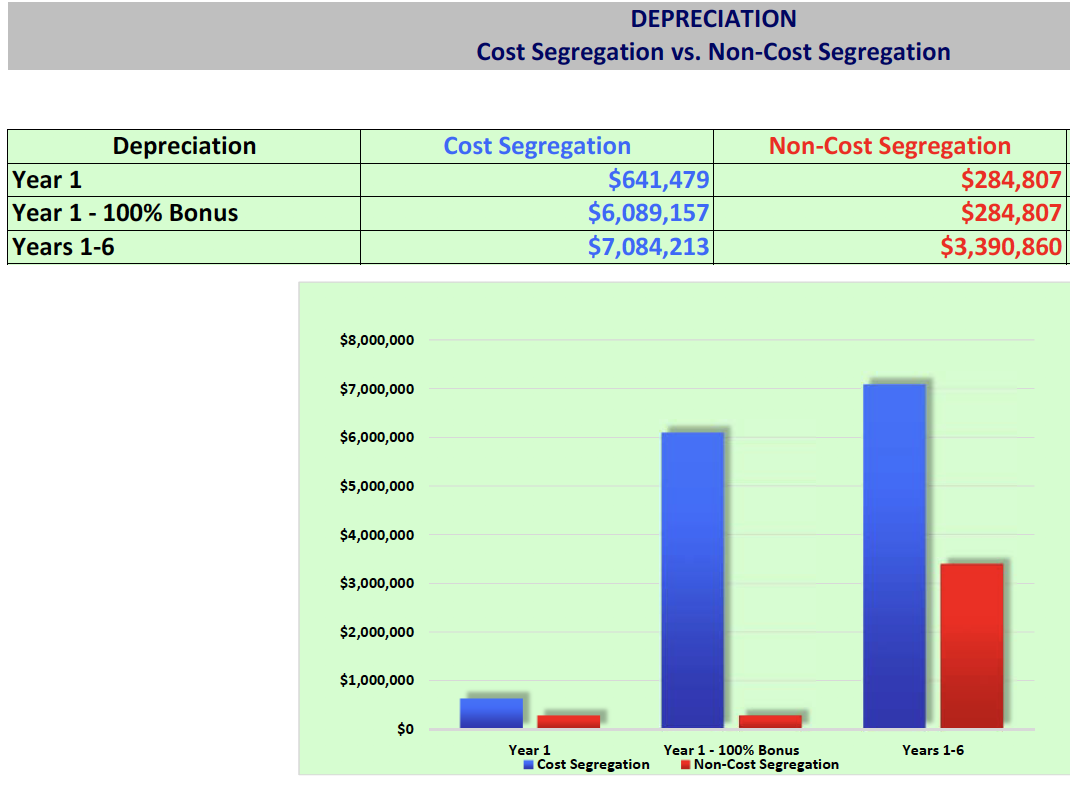

Below: Another estimation of regular depreciation vs the more aggressive deprecation timeline (what is coined as “bonus depreciation”)

Envision a 3 bedroom single-family home in Birmingham, Alabama that is worth $100,000. Of that, approximately $65,000 is determined to be the building value and $35,000 is determined to be the land value. Each year you can deduct 1/27.5th of the building value, which is about $2,363 a year that can offset income gains. $2,363 can be taken for the next 27.5 years until all the value on paper is depleted.

Is there a catch?

Unfortunately, you cannot deduct the value of the land unless you have made a land improvement, granting that the improvement you made has a “useful life” that is depreciable. Only the improvement will be depreciable, not the land itself.

https://youtu.be/tlI83umq-DE

When you sell the asset you will need to recapture the depreciation. This is the major disadvantage to a cost segregation.

We pay $8000-12,000 on our larger commercial assets to do a cost segregation and our advisors tell us that the general rule is to do a cost segregation if we intend to hold onto a property more than 3-5 years because if we sold quicker than the time benefit to the passive losses we got as investors you be less and might not be worth the price of the actually cost segregation study.

But, guess what?

There are some exciting new benefits to passive losses since Mr. Trump enacted a tax law where 100% Bonus Depreciation creates substantial benefits on your taxes for the acquisition year. In the future, us investors are crossing our fingers that this part of the tax code sticks around.

Paper losses from single family homes

Previous

Next

Think about this: My $3M, 52-unit apartment, is looking to get more than $266K in tax savings (at 37% tax rate) in the first year of ownership by doing a cost segregation.

If you are interested in learning more about how to best utilize your passive losses, you can learn more here.

Companies and investors who have constructed, purchased, expanded, or remodeled any kind of commercial real estate (including 1 to 4-unit residential rental properties) since 1987 can use cost segregation studies for maximize their tax savings.

The study allows the owner to take advantage of accelerated depreciation deductions and defer federal and state income taxes on the reclassified building components mentioned above.

A team of real estate investors evaluates several personal properties, residential rental property, and land improvements that can be upgraded to improve the value of the property. Those improvements are assessed with the assistance of a Cost Segregation specialist. After completing this cost segregation analysis, the property owner may deduct the depreciable life of the individual fractional interest (IFI) through a cost segregation study, with or without depreciation. If the taxpayer is eligible and has not failed to take advantage of the tax rebate, the taxpayer may claim the expense directly within the given year of the seller’s ownership.

To elaborate more on Accelerate Depreciation Deductions, it is a deduction of the cost you pay to a person if you own your personal property assets. The accelerated depreciation deduction provides significant tax savings but it is not another type of benefit. The exchange of property owners whose benefit is primarily from cost segregation is a limitation in tax savings. The depreciation expense is deducted at the source rate in another year.

What are the Benefits of Cost Segregation?

Lower Property Insurance Premiums

Since it generally costs less to insure personal property, versus real property, building components reallocated as personal property should reduce your insurance costs as well which will yield potential benefits in the end.

Capture Retroactive Savings

Since 1996, taxpayers could capture immediate retroactive savings on properties added since 1987. Previous rules, which provided a four-year catch-up period for retroactive savings, have been amended to allow taxpayers to take the entire amount of the adjustment in the year the Cost Segregation is completed.

This alone is huge!

This opportunity to recapture unrecognized depreciation in one year presents an opportunity to perform retroactive Cost Segregation analyses on older properties to increase cash flow in the current year.

What Components Can I Reclassify?

Components of a specific property or qualified leasehold improvement are identified and reclassified for depreciation over a shorter time (5, 7, or 15 years). For example, 30% to 90% of the total electrical costs in most buildings can qualify for 5 or 7-year depreciation.

5- year tax-life components

Non-structural elements: carpet, decorative lighting and trim, HVAC systems, dedicated electrical and plumbing, and security systems.

7-year tax-life components

All telecommunication related systems: cabling, telephone, etc.

15-year tax-life components

Exterior land improvements: landscaping, curbs, sidewalks, fencing, and signage.

As a Passive LP investor the details of this is not needed as all you need to ensure is that your sponsor is aware of cost segregations to optimize tax benefits.

What is required to have a study done?

You need to provide as much of the original documentation pertaining to planning, construction, and current tax depreciation as you can.

This could include a complete set of:

Construction plans

Current tax depreciation records such as tax returns, building cost budget information, final AIA (American Institute of Architects) appreciation

Document of certification of payment or other cost information, change orders, direct or indirect costs paid by the owner that are not included in other documents

Other information depending on the project

How much does a Cost Segregation Study cost?

On average, the total fee will generally fall between 5% and 20% of the estimated net present value tax saving. You can often get a free preliminary analysis to help determine this. This can be impacted by how large or small the real estate project is.

In addition, the location, accessibility, and quality of the records and documents will impact the entire cost (costs typically range between $8,000-$12,000). Minimum fees can be as low as $2,000 for small projects, and some firms GUARANTEE a minimum of 500% ROI (fee vs. tax recovery) on projects over $500,000.

Cost segregation studies are typically cost-effective for larger syndication buildings purchased or remodeled at a cost greater than $100,000. Acost segregation study ismost efficient for new buildings under construction, but it can also uncover a retroactive tax deduction for much older buildings as well.

What are the steps involved in the process?

First off… if you are a Passive Investor (LP), your sponsor should be taking care of cost segregation for you so you will have one less thing to worry about.

If not, the cost segregation process can be broken down into the following steps from start to finish:

Step 1

Vet Cost Segregation Firm

Engage a reputable Cost Segregation firm that utilizes engineers and architects trained in Cost Segregation and it’s application to the proper allocation of assets. If you need a referral go here.

Step 2

Document Review

The engineer determines what documents are available (e.g. planning, construction, invoices, appraisal, and current tax depreciation) for reference and referral.

Step 3

Schedule Property Survey

The engineer then sets a schedule for surveying the subject property and gathering the available documents for review prior to arrival at the subject property.

Step 4

Document Recreation

For those documents that are unavailable, time is then scheduled into the Cost Segregation process for document recreation using known industry standard costing data (Marshall & Swift and/or RS Means costing publications). The process takes about 4 to 6 weeks after all necessary documents are acquired. The time that a Cost Segregation Study takes depends on the size of the project and the completeness of the documentation that you can supply.

Step 5

Conduct Site Survey

The site survey is executed and completed. Surveys can be completed within as little as an hour, but it varies between each survey. Measurements are taken and all areas are photographed for IRS verification and substantiation of asset values during the survey.

Step 6

Calculations

The engineer returns to the office and crunches the numbers. The number crunching process is when all documents are reviewed in detail, assets are verified, and measured against known costing data, and asset reallocation is applied.

Step 7

Review

A review committee then examines the results of the analysis completed by the engineer of record to verify its veracity and confirms it meets and exceeds IRS guidelines per the Cost Segregation Audit Techniques Guide.

Step 8

Compile Report

Once approved, the study results are compiled into a final report that includes: all IRS tax code to substantiate the reallocated assets, spreadsheets identifying all assets categorized according to their building codes, representative photographs of the reallocated assets, and the engineer’s credentials for IRS review.

Step 9

Issue Report

The final report is issued. The client and CPA of record receives digital copies via email, for application to the client’s tax return.

When Should Cost Segregation Be NOT Considered?

There’s an attempt to sell within within 5 years

Not being able to use the losses- planning 5 years ahead and looking back 5 years for taxes; income isn’t enough or PAL restricted.

No savings of at least 2X cost of study (not depreciation but the existing cash savings)

Be wary of 1031 exchanges- there are 2 ways to calculate the depreciation to carryover

5. Check that the federal 1031 doesn’t open you up to exuberant state taxation on the state 1031. Note: Many states do not follow federal guidelines for depreciation and personal property ineligibility.

6. Discern if 179 expensing method is a better option (due to presence of limitations)

7. Possess your real estate in S Corps due to many reasons: basis and step-up

Cost Segregation Example #1

Depreciation is distributed to investors on the K-1 Form in syndications.

Not making any promises as depreciation amount is primarily based off building specifics and the amount of leverage used in a deal, but here is a real-life example from a $50K LP investment in a Class C apartment syndication in the first year K-1 in 2018 which yielded a $36K paper loss by utilizing a cost segregation. Extract 10-20x what you normally able to deduct in the first year alone! Take these passive losses and employ the “Simple Passive Cashflow Gravy Train” strategy where you offset your ordinary/W2 income with real estate professional status. For more details on that check out our Master Tax Guide.

I paid 4% in taxes in 2018. All because of the passive losses that real estate gave me.

Previous

Next

If this is a new concept to you, you may be able to go back to previous years taxes and get back some benefits this year. Oftentimes, getting a quote is free and quick.

A recent quote I got back for a few properties:

Previous

Next

Cost Segregation Example #2

We purchased a $20M apartment and are about to write off $6M in the first year! The total capital raised from investors was $5.5M, that meant almost a dollar for dollar deduction in year one!

Cost segregations are not new. On the contrary, they have been in existence since 1954, when the IRS allowed for certain personal assets to be accelerated into a shorter life class. However, it wasn’t until Hospital Corporation of America sued the IRS in 1997, and won, that the IRS revisited the issue of accelerated depreciation. The IRS ruled that property qualifying as tangible personal property under the former Investment Tax Credit (ITC) rules, would also qualify for purposes of federal income tax depreciation under MACRS (Modified Accelerated Cost Recovery System).

The IRS Chief Attorney wrote a memo saying, “. . . Cost Segregation, for it to be properly applied, had to involve those with competencies in architecture, engineering, or construction and/or construction techniques, in order for personal property assets to be accurately identified and segregated.” As a result of this memo, cost segregation became a viable tax-saving strategy allowed by the IRS.

CPAs are not qualified according to the IRS guidelines. However, most Cost Segregation firms will gladly work with them on a consulting basis to complete the work for you. Remember, the IRS Chief Counsel issued a memo that made it clear what constitutes proper “methodology” in applying Cost Segregation, and it must be done by people who are competent in architecture, engineering or construction and/or construction techniques. You will want to ensure you are working with a cost segregation specialist to follow correct protocols. See ” Is Cost Segregation something new? ” above.

As investors, we like paper depreciation to occur earlier because that offsets gains earlier and gets more money in our pocket earlier. Just like how you give a mouse a cookie…. Give an investor a dollar early and… they will turn em’ and burn em’.

In other words, you are not creating more depreciation, you are shifting it earlier to take advantage of the time value of money concept.

On the project-level in a single asset LLC arrangement, the more you can lower your tax liability, the more you can significantly increase your passive income and create more value for investors.

A cost segregation study, in effect, gives you an interest-free loan from the government for the first 15 years, which you will then repay interest-free over the remaining 25 years. Wouldn’t you rather have your money now? There are also advantages in doing a study if the building is going to be sold (via 1031 exchange) or if the owner of the building dies.

Most cost segregation firms will perform a free analysis if you provide your basic property information and tax rate. From the information you provide, they can calculate a conservative estimate of the accelerated benefits you can expect, as well as their fixed fee proposed for the final study.

Typically, tax savings from 5% to 10% of the building’s original tax-basis are generated, but there are instances where it can be substantially more. Each property and circumstance is unique, so it requires a case-by-case approach to give you a definitive answer.

Certain types of commercial properties can be grouped together to give us an idea of the percentage of those types of buildings eligible for accelerated depreciation. Your results may be greater, or less than those quoted here, but in general, property that falls into one of the following categories is most likely to result in accelerated depreciation within the specified ranges.

A study conducted by a reputable Cost Segregation firm should strictly adhere to the IRS Cost Segregation Audit Techniques Guide . The type of study most firms perform places you in Internal Revenue Code Tax Compliance, which actually decrease your chances of an audit. However, you should be aware there are six different Cost Segregation methods allowed by the IRS, and not all are of equal merit. There is currently no standard method, and there is still some ambiguity about which method is best. If you have heard conflicting information about what is, and is not possible regarding Cost Segregation, it really depends on which method is being used.

A reputable Cost Segregation firm can assist you in the event of an audit. They will focus on doing the Cost Segregation Study to create documentation and support for conclusions so that these are easily communicated and resolved with the IRS. In fact, you should expect a final report that is “all inclusive”. The report should quote specific Internal Revenue Codes related to the reallocated assets. Additionally, it should provide photographic evidence of these same assets for complete substantiation of the assessment. A properly documented Cost Segregation Study helps resolve IRS inquiries at the earliest stages.

A cost segregation study can still be performed even if you lack some of the necessary documentation. Construction, engineering, and other specialists will do an extensive site visit. They will measure and estimate using currently accepted costing techniques and pricing guides (such as the IRS-recommended costing publications Marshall & Swift and RS Means ) to determine the costs that qualify for shorter recovery life periods.

Paying ~2% fees per year on my Health Saving Account driving me crazy that I withdraw it and invest cash.

I’m going to start out by saying please do not take this as legal/tax advice!

One rule I follow is “pigs get fat but hogs get slaughtered.”

But if there is a tax code or loophole within reason/ethical good faith you should exploit it as much as possible.

In 2017, I purchased a half acre in a turnkey Coffee farm in Panama in my Health Savings Account (HSA) for about $15,000.

HSA’s are truly awesome! You add money to an account tax-free (like a pre-tax 401k), don’t get taxed on the gains (like any retirement account), and you don’t have to pay taxes when you use it on Eligible Health Expenses (like a RothIRA).

You need a High Deductible health plan to be eligible for an HST. I’m going to get a little political here… health costs are on the rise because it bails people out for not being accountable (good diet, sleeping habits, stress, and exercise program). The company famous for the yellow Twinky bars cited rising health cost as their reason for going bankrupt… go figure.

You WILL have health expenses, MAY have retirement expense… in other words, you will likely die and have health expenses before you retire. So it makes sense to fund an HSA account before any 401K, Roth IRA, IRA, etc.

Here is some information for your entertainment purposes to see what you can start to use your HSA for:

Getting a doctor to sign off on your medical purchase as necessary will need a template:

Sample Letter of Medical Necessity for Hyperhidrosis Treatment

[Date]

[Insurer name]

Attn: [Name of individual]

[Address]

re: [Patient name]

[Policy number]

Dear [Insurer name]:

I am writing on behalf of [Patient name] to document the medical necessity of [insert treatment option here] for the treatment of hyperhidrosis. This letter provides information about the patient’s medical history and diagnosis and a statement summarizing my treatment rationale.

Hyperhidrosis, or excessive sweating, is a medical condition that can have a devastating effect on a patient’s quality of life, causing physical discomfort, secondary skin problems, social/emotional sequelae such as anxiety and depression, and disruption of occupational and daily activities. This has certainly been true for [Patient name], who has been impacted by hyperhidrosis for [insert duration of symptoms here]. Specifically, [he or she] has had difficulties with [insert quality-of-life, social/emotional and/or career/daily living problems here].

[Discuss patient’s diagnosis, treatment history, and degree of illness]

[Insert patient’s name] has tried the aforementioned therapies thus far without success and I, therefore, recommend [insert treatment option here] as the next logical choice for treating [his or her] hyperhidrosis.

In light of this clinical information, and this patient’s condition, [insert treatment option here] is medically necessary and warrants coverage. Please contact me at [(000) 000- 0000] if you require additional information.

Sincerely,

[Physician’s name]

Here is what I put together to get massages for stress from dealing with SPC listeners who don’t listen to the podcasts before booking a call or people who don’t take action:

I am writing on behalf of Lane Kawaoka to document the medical necessity of massage for the treatment of mental stress and muscular discomfort. This letter provides information about the patient’s medical history and diagnosis and a statement summarizing my treatment rationale.

“Mental stress and muscular discomfort”, is a medical condition that can have an effect on a patient’s quality of life, causing physical discomfort, secondary skin problems, social/ emotional sequelae such as anxiety and depression, and disruption of occupational and daily activities. Specifically, he has had difficulties with discomfort performing his duties at work and exercise routine [insert quality-of-life, social/emotional and/or career/daily living problems here].

[Discuss the patient’s diagnosis, treatment history, and degree of illness]

Lane Kawaoka came into the office in early 2018 where we ran a cardiovascular and blood assessment.

Lane Kawaoka has tried the aforementioned therapies thus far without success and I, therefore, recommend massage as the next logical choice for treating him.

In light of this clinical information, and this patient’s condition, massage is medically necessary and warrants coverage. Please contact me at [(000) 000-0000] if you require additional information.

I would say this is a bad report because it’s not Prescriptive. It is very important to have a chat with your inspector so they know it’s not going to be a warm and fuzzy home to live in but a rental property. They will need to avoid citing nitpicky things because the seller is likely another investor and more sophisticated than a regular homeowner and will call BS at your repair requests.

This is where an hour of coaching will go a long way to maximize what you get at the negotiation table.

I suggest bringing an accountability buddy or significant other. The worse thing is to come back to normal life without someone speaking the same “language” around you.

I see these motivational events as “baths” which you need to take from time to time. Even if you are someone who is internally motivated, this will take you to another level.

You will leave this event changed – as silly as it sounds “things will never be the same”

This event will be held in a smaller venue (12,000 people) which I was really excited about when I was planning this because it is a lot better environment than the normal sports arena setting where everyone is captive in their rows.

You get to walk on burning coals!

Learn more about the event here – note the LA event is not yet listed

Details are still being formed but we will likely get upgraded one or two levels if we come in as a large group.

I am also arranging for a Monday decompression meeting to connect with other investors who attended from the Hui.

This event is more for personal development than investing. But it is certainly investing in yourself! After all… getting the passive cashflow is Simple but what you do after is the hard part.

I don’t personally guarantee investments because of course there is always a risk but I WILL guarantee your ROI if you come to this event! Call me and I will share my experience.

After going in 2016, I made these goals in 2017. Some of which happened so of which I overshot.

2019 Takeaways:

Less urgency with more systems

Barriers- peers around to do the same things,

What needs to shift what actions… Deciding how to do this

Why will you live in a beautiful state everyday no matter why?

Life is too short It is a slippery slope backwards In the end a beautiful state is what we are after anyway not money, house, job or relationships. I have control over this… Potential => Actions => results => belief/concerns

Flavors of reaction:

Three things that cause suffering the fear of 1) loss 2) less 3) never have something

Suffering => appreciation => joy

You will make more money if you are in a better state.

Two things that I did to start investing to go bigger – 1) started something that could be better and connect with others and build a platform to have larger impact. I made small changes and found models and copied and got around the right people and slowly built 2) started paying to learn

So you are in!

Preparing for your first Unleashed the Power Within Seminar:

1) Come with an open mind.

2) Make a list of a few limiting beliefs. Everyone has these. Some common examples are I am not achieving what I want because… (I’m to young, too old, never went to college, a woman, I’m brown, I did not come from money). These are the things that subconsciously hold us back. What are limiting belief’s here are some softer examples and they range to not being a certain race, not having the right education, not being tall enough, to not being good at math.

3) Prepare to tackle your biggest, hairy, huge goals.

4) Tony will bring it. He drops the F-bomb a lot. Mostly for shock value as again it is entirely on purpose. Note: he gives free tickets to some troubled kids and he tries to speak to a lot of the kids in the first few minutes who likely have never have heard him before.

5) Prepare to dance your ass off. Even if you can’t dance/hate to dance/have no legs… You will still want to dance. Get in that “puppy pit”. For goodness sake… Live like you don’t give a fuck. Get comfortable with being uncomfortable. Dance because if only it is you trying to do something different.

6) Joseph McClellan will speak on day two and day four. He is a good speaker too. This is not a 5k seminar so you do not get four days of Tony… Its a fraction of that.

7) Be prepared to show up early and go long. Like 8 am to 2 am long. Stay as close to the convention as possible it will be crazy leaving when everyone else does. Don’t try to skip out. If you are getting tired you are letting circumstances control you instead of your leading your state! It is often in the moments when you are close to your limits that the biggest breakthroughs happen, so don’t sell yourself short.

8) Firewalking is real. I thought it was a party trick when I did it and did NOT get into state. You can do it and you will remember it for the rest of your life. This will be trumped by day 3 transformation evening showcase.

9) Taking your spouse or buddy? It’s good that you will be on the same page when you get back to real life but consider not sitting together for part or all of the seminar. There is a lot of value to connecting with others there and getting outside of your normal conventions. Don’t be afraid to talk to some people. Volunteers, there are a wealth of information about what’s coming next and what to do. You can be your true self when you don’t know the other person as they don’t know you or have any expectations of who you “should” be. Here is what the staff told me “It is highly suggested, but not mandatory, for family members, friends and colleagues to not sit with each other. We find it that you end up “playing full out” with strangers than with people you know.

10) I would take notes and more importantly brainstorm action items and implantation plans.

11) Drink the kool-aide. Be all in. Dance, scream, visualize. Show up on time and stay till the end. Get your money’s worth. Do it! It’s worth it.

12) Tony is on another level in terms of hypnosis that makes NLP obsolete. Go with it.

13) Try to sit in the aisle so you can mix and mingle. This makes it easier to run out for a quick bathroom break. You will have to be in there a little earlier like 30 minutes scheduled to start. Also, try and find the bathroom that no one uses for quicker usage. don’t wash your hands it’s faster… Jk.

14) Read/listen to any of his books or audio program

15) Check out what is on YouTube e.g. his TED Talk

15) Watch I Am Not Your Guru on Netflix

16) Six Human Needs and Triad are the core of his work you can learn more in his TED Talk or on his website

17) If you’re not in the right state, not getting it, not feeling right etc. ask any of the leaders and trainers for help, they are amazing resources and have been through it so many times before so have seen, heard and experienced it all before.

18) Subscribe to UPW Facebook group for the event

19) On day two make a list of things you will Stop doing

20) You may not want to commute to and from the event as the event starts early in the morning and end late night. The first night may end after 12 midnight.

What to bring to the Seminar

1) A heavy jacket or even blanker – Tony keeps the room extremely cold on purpose. It’s all part of his magic. Embrace it.

2) You will be jumping for hours. No heels or dress shoes. The only type of shoes you should be wearing are tennis/keds/flats/basketball shoes. Most people will wear causal or gym type attire.

3) Don’t just bring snacks. Bring meals. I’m talking fruit, nuts, hummus, veggies, crackers, granola bars, etc. If you don’t, prepare to race 10,000 other people to be in front of the food line. Post-mates/Uber eats can be a good healthy option. If you are so compelled fast for the four days – and start the literal cellular autophagy – as you will learn the pain is all in your mind!

4) Notebook

Post-event:

1) Give yourself a couple of extra days after the event to catch up on sleep, decompress, review your notes, absorb and process what you learned and make a plan for how you will integrate changes in your life. You will be tempted to plan to rush back into “life” straight afterward but to allow yourself to recover and to successfully integrate your learnings you need to give yourself a little time. There will be some discussion on this on the fourth day.

2) Stay tuned… I will plan an event Monday morning or Sunday evening.

Outside food and beverages are not permitted in the LACC Center with the exception of sealed bottled water and sealed light snacks. Light snacks include single-serving items that would be consumed by one person. For example, granola bars, protein bars, bags of chips, crackers, beef jerky or whole fruit, etc. Empty refillable water bottles are permitted and can be refilled on the main concourse at LACC Center’s drinking fountains. Coolers and grocery bags are not permitted in the LACC Center.

MHN 11-1-2018 – Student Housing Costs Compared – How affordable is purpose-built off-campus housing? – [All this data means nothing if there is a student bubble coming – think about it on a granular level… it makes no sense of a family that makes 90K a year to send their kid to a public college that costs $40K+ a year to get some random degree]

MFE 2-6-19 – 2018’s Record Deal Volume Suggests Positive Trajectory for 2019 – “driven in large part by increased interest in the student housing sector, which accounted for 17% of all deal activity in the third quarter, compared with a consistent 4% over the past 13 years” – [I don’t like student housing as I am seeing an education bubble with all the lending. It’s crazy how dorms get renovated every few years]

List of SDIRA Custodians in no particular order based off feedback from other Hui Deal Pipeline club members.

Accuplan

Advanta IRA

American Estate & Trust

American IRA

Asset Exchange Strategies

Broad Financial

CamaPlan

Capital IRA

Central Bank

Checkbook IRA

Community National Bank

Crowdfund IRA

The Entrust Group

Equity Trust Company

First Trust Company of Onaga

GoldStar Trust Company

Guidant Financial Group, LLC

Horizon Trust Company

iPlanGroup

IRAvest

IRA Advantage

IRA Club

IRA Express, Inc.

IRA Innovations

IRA Resources

IRA Services Trust Company

Kingdom Trust Company

Lincoln Trust Company

Madison Trust Company

Midland IRA

Millennium Trust Company

Mountain West IRA

Nevada Trust Company

New Direction IRA

New Standard IRA

Next Generation Trust Services

Nexus Direct IRA

NuView IRA

PENSCO Trust Company

PGI Agency

PolyComp Trust Company

Preferred Trust Company

Premier Trust

Provident Trust Group

Quest IRA

RealTrust IRA Alternatives

Safeguard Advisors

Self Directed

Self Directed IRA Services, Inc.

Sense Financial

Sovereign International Pension Services

Specialized IRA Services

Summit Trust Company

SunWest Trust Company

Trust Company of America

uDirect IRA

Vantage IRA

401kCheckbook

The Self-Directed IRA Graveyard

American Pension Services

I don’t personally like these accounts for my own investing even though the future gains and withdrawals are tax-free because you can’t use the best Fannie Mae or Freddie Mac loan products when investing in your IRA.

Unless you are using a QRP (Qualified Retirement Plan).

With syndications using leverage (as most good deals do) you will be likely opening yourself up to UDFI etc taxes.

In the end, I want the freedom to enjoy the money now and not have to wait till I am 60 something.