I currently have a verbal agreement to put together a long-term joint venture.

I’m engaged and in the due-diligence period with multiple extensions.

Traditionally a down payment for such a transaction is a ring. Hopefully, if you have not gone through this experience before, you will learn about procuring this rare commodity. If not, I hope you find it entertaining.

For those who haven’t caught on yet – I’m talking about diamonds.

I think everyone knows that you get ripped off at a retail brick and mortar jeweler… even Fred Meyer Jewelers because you have to pay for all the overhead and compete with unsophisticated buyers. Plus I don’t like all the sleazy sales tactics and it is a huge time-sucking experience.

In the back of my head, I know the diamond market has to be rigged sort of like the sunglasses world where all the brands are owned by Luxottica and there is price rigging involved.

Now some people say they can haggle for a better price in person, but that takes time. Also, I am in the “first stage” of learning: I don’t know what I don’t know.

I turned my attention to the top 3 sites using Google and Reddit forums.

1) Blue Nile

2) James Allen

3) Rare Caret

I was happy with getting approximate “market value” on the website. I trusted the overall grading system in an online store.

What I really like about these websites is that they allow you to sort hundreds of diamonds in online spreadsheet form with a sort feature based on different attributes.

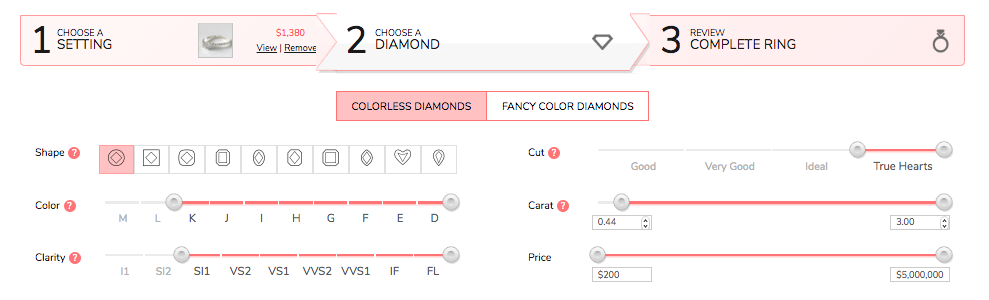

This might be review but the big four C’s are Carat-weight, Colour, Clarity, and Cut. Unfortunately, you cannot buy the 5th C – Confidence.

(Not to be confused with the three C’s of evaluating people into your network: Character, Competence, Commitment.)

If you would like to know more than the 80% of people, take 10 minutes to read this article to determine the quality & value of diamonds, via the famous 5cs of diamond grading.

Now, in my humble opinion … real talk here… the most important factor is size. So Carat Weight is numerouno. Most people cannot tell you the difference between the other three attributes; they only see how big the freaking thing is.

For those who know a thing or two about diamonds, Cut is the second most important thing. Cut is the sparkle-factor, how much the diamond shines based on the angles of the Cut. I went and got the top grade Cut because that is a big wow-factor (second to of course how big it is).

The other two attributes, Colour and Clarity, I frankly don’t really care. Some people could actually like a little color or whatever that clarity thing is. So I set my search criteria to have all the levels in those two categories. One exception is that I just did not put the worst-grade Colour and Clarity in my selection. This for no good reason other than not wanting to have the worst one (as vain as it sounds). Call me dumb, but I feel embarrassed when I order the cheapest wine on the menu…I always go for the second cheapest.

Rare Caret seemed to have the best selection of diamonds, but their ring selection seemed to be lacking. So after a side by side comparison of Blue Nile and James Allen, I found James Allen to be ~5K cheaper for the same diamond.

At the end of the day, I knew what my budget was so I was just trying to get the best bang for my buck. In other words, the money was allocated and this is how I mentally process non-income producing assets.

Unfortunately, I was not able to use Mr. Rebates – a go to for getting a few percent points of cashflow by going through a simple shopping portal. Nor was I able to find many coupon codes using RetailMeNot.com or navigating their email digital marketing campaign. Most sophisticated marking emails are laced with smart links to kick out a discount coupon based on what links you click in the email and if you do not buy right away to get you off the fence as a buyer.

You can spend a fortune on Carat-weight, Colour, Clarity, and Cut…but the most important 5th “C” of all, Confidence.

A lot of my high net worth single friends (who by the way get a lot of dates) don’t see the value of getting married in this modern era (other than if you would like to have kids). I definitely understand that perspective to some extent. This makes buying an archaic stone that may or may not have been a blood diamond just another thought to complicate things.

But as a recovering cheapo – simplepassivecashflow.com/cheapo – I understand that money is not evil and can buy a variety of things including freedom, time, and happiness. This purchase is a perfect example of that.

The way I see it, marriage is a lot like playing with leverage. It is a little more risk than going it alone, but the reward (if done right) is disproportionately greater (per the Shape Ratio’s risk-adjusted return).

My first plan was to make the big reveal in a new Honda CRV. Note – at this moment I’m over the whole Mercedes, Tesla, wealth-based off of the car I drive. Instead, I am striving to achieve the financial freedom level I am looking for.

I even had my VA scrape a lot of Honda contacts to do my normal email blasts to put multiple dealers against each other. By the way, I lease cars because I did the math and it makes more sense for sophisticated investors who get higher than average returns.

I got the car but scrapped the idea because my buddy mentioned… “dude – you don’t want to propose at a car dealership.”

Takeaway here is that everyone has a blindspot and its good to have people around you to bring up counterpoints.

Thanks for following Simple Passive Cashflow. Onward and upward.

“A lot of the funds are shots in the dark with the only certainty that you get tax savings on the front end. Don’t let taxes be the cause to going into bad deals”

I did some research on this new Opportunity Fund Zone tax benefits. Below are some notes and ideas. Generally speaking I stay away from OZs because they are typically in crap areas which is why congress needs to offer incentives for investors to go there and infuse capital/life there. I’m all for tax savings but I don’t want the “tax tail to wag the dog”, the primary focus of my investment philosophy today is investing in solid locations. This recent article proved my point.

In 2019, I sold my last Turnkey rentals and did so without a 1031 exchange (which we don’t really do in our syndication accredited investor ecosystem. Nor do we mess around Opportunity Zones because we don’t really need exotic tax mitigation strategies once you get on the “golden hamster wheel” of good deals that get great passive losses from bonus depreciation. For more info on taxes go here.

Note: I’m not a CPA or attorney just putting it out there to help inspire some ideas.

An Opportunity zone (OZ) is a tax-favored investment for people with capital gains.

6-pages in the tax document in the new 2017 Tax Cuts and Jobs Act Goal to encourage long-term investments in low-income communities across the US. Every major city has some OZ. Most of Detroit is an OZ plus large portions of Baltimore. Allows investors to sell their appreciated assets and invest their realized capital gains into one or more designated OZ. EVEN STOCKS! Non-like kind assets are OK! After your selling your appreciated asset you have 180-days. The longer you hold the more benefit you get (up to 10 years). 1) Defer your original capital gain tax obligations until 2026 or until you sell your OZ investment.2) Discount of 10% or 15% on the taxable amount of your original gains. If you hold more than 5 years your original cap gains decrease 10%3) If you hold 10 years or more. You will pay NO capital gains tax on any appreciation. You can self-certify so you do not need an intermediary like in 1031 exchanges. No investment minimum. There are some items that get a little unclear… where you should really consult your CPA. Check out the IRS opportunity comes frequently asked questions page and additional resources below. Resources to Google: community development financial institutions fund, CDFI Fund map. Note: Spending $100 dollars to save $20 dollars is not a wise idea. Just like buying a rental next to Grandma’s house because of your travel there. A lot of specifics are still being played out but something intriguing to augment an already good investment. Other ideas: Look at the OZ map and try to find the smaller slivers of OZ. This is called “buying on the line” whereas areas improve on the edge of development you greatly benefit. I would ask your CPA if they know about these opportunity fund zones. If they don’t you might need a new CPA. If you are a current Hui Deal Pipeline Club member I would be more than happy to refer you to some people and then you can see if you work well together.

There is a lot of rumors floating around how this tax will be implemented later this year. One of these rumors suggests that we might not qualify for the Opportunity Zone Fund. See second to the last page of the attached where they state that we have to do improvements that is the same as the basis in order to qualify. Here are some other notes that a buddy of mine took:

Temporary tax deferral on reinvested capital gain until 12/31/2026 (from stocks/sale of a business/real estate partnerships/direct real estate sale)

Elimination of a portion of the reinvested capital gain over the term of the investment.

10% if invested for 5 years

15% if invested for 7 years

Permanent exclusion (100%) of gain on appreciation in excess of initial capital gain investment if held for 10 years.

This means if you have sold an asset whether it be real estate, stocks/bonds, partnership interest, cryptocurrency or a business, you can reinvest that capital gain within 180 days and defer taxes, reduce those taxes by 15% after 7 years of holding and eliminate any capital gains created on the new asset after 10 years.

Post-tax Internal Rate of Return (IRR) increases by a staggering 50% when you invest in a Qualified Opportunity Zone Fund!

This is different from a 1031 exchange which only allows you to exchange like-kind investments and also requires an intermediary (this program does not need an intermediary).

It’s worth noting that the intent of this tax incentive is to help spur development and economic activity in “distressed communities”. So this really is an opportunity to do good and do well.

I have a boatload of income this year, is a OZ project something I should look into?

The OZ is a pretty sweet tax haven and works in theory but I just caution that in the end of the day you are putting money into a shitty area. If you take the tax hit today you will lose 50% but if you invest in a crap area that does little growth then you might lose all of it in a 10 year period. Here are a few options: 1) Go into an opportunity zone fund – these things will be a shot in the dark and my concern other than not knowing these people personally is that these types of fund are a ponzu scheme waiting to happen. We could go with a Vanguard one which I am sure is “reliable” but the yields will be super low like 2-6%. The other funds that I were looking at are 6-10% a year. Perhaps we can spread it all around :/ 2) Find a 2-12 unit in a cash flowing area and run it as a mom and pop yourself

Definitions:

Qualified Opportunity Zone Business – A trade or business. Substantially all of its tangible property (whether owned or leased) is Qualified Opportunity Zone Business Property AND At least 50 percent of its gross income must be from the active conduct of a trade or business in an Opportunity Zone, A substantial portion of its intangible property must be used in the active conduct of its business in an Opportunity Zone, No more than 5 percent of the average unadjusted basis of its assets may consist of “non-qualified financial property,” Cannot be a golf course, country club, massage parlor, hot tub facility, suntan facility, racetrack or other gambling facility, or any store the principal business of which is the sale of alcoholic beverages for consumption off-premises

Qualified Opportunity Zone Business Property – A tangible property used in a trade of business if: It is acquired by purchase (as defined in Section 179(d)(2) related party rules, but using a 20% related party test instead of 50%) after December 31, 2017; The original use in the Qualified Opportunity Zone commences with the Qualified Opportunity Zone Business OR The Qualified Opportunity Zone Business substantially improves the property; and During substantially all of the holding period for such property, substantially all of the use of such property is in an Opportunity Zone.

Substantial Improvement Test: Property is treated as “substantially improved” if, during any 30-month period beginning after the acquisition of the property, additions to basis of the property exceed an amount equal to the adjusted basis of the property at the beginning of such period. Land excluded

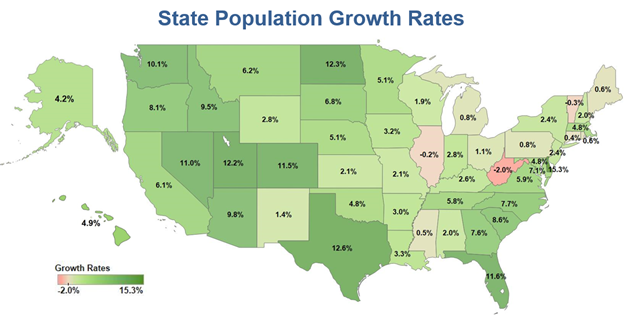

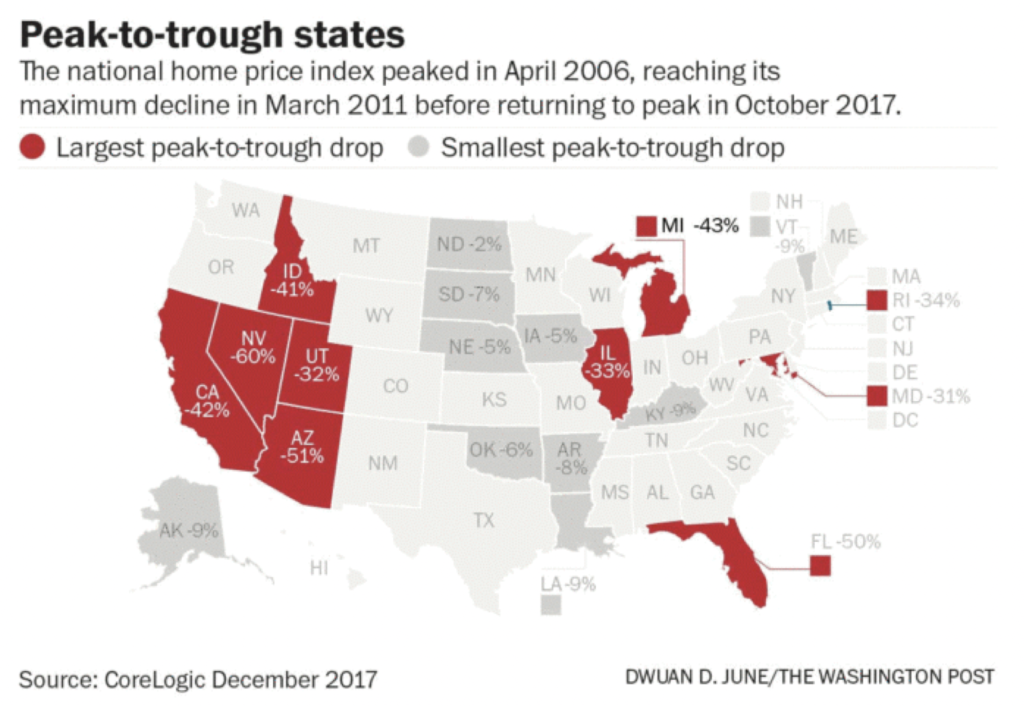

Between 2010 and 2017, population growth averaged 5.5% for the US as a whole. Delaware boasted the highest growth rate, 15.3%, over these years. A state with a relatively small population, however, needs fewer new residents to achieve such a high growth rate. The double-digit rates recorded by Texas (up 12.6%) and Florida (up 11.6%), both high-population states, are therefore that much more impressive. There were three states that posted population decline between 2010 and 2017: West Virginia (down 2.0%), Vermont (down 0.3%), and Illinois (down 0.2%). – ITR – 19.02.28

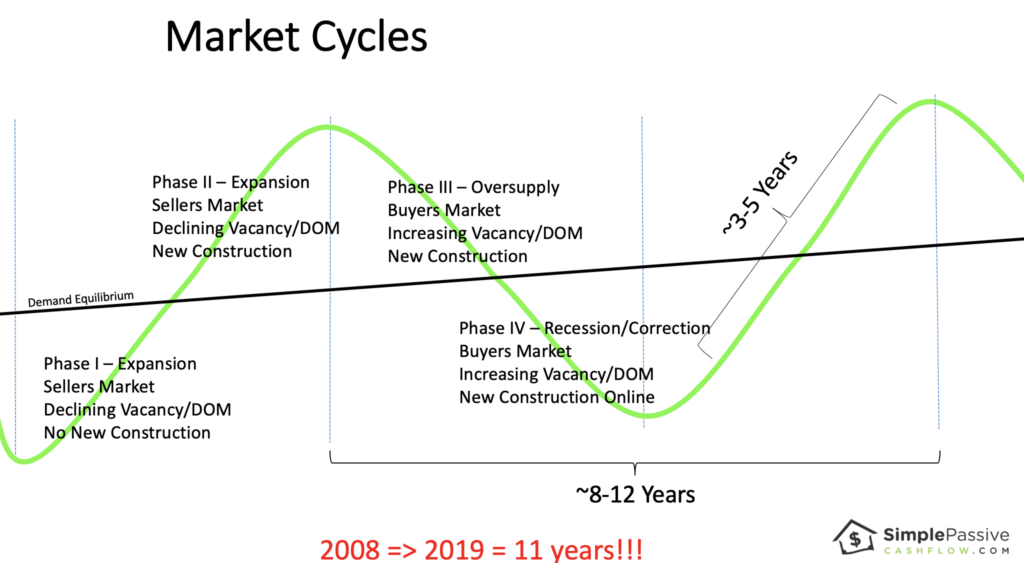

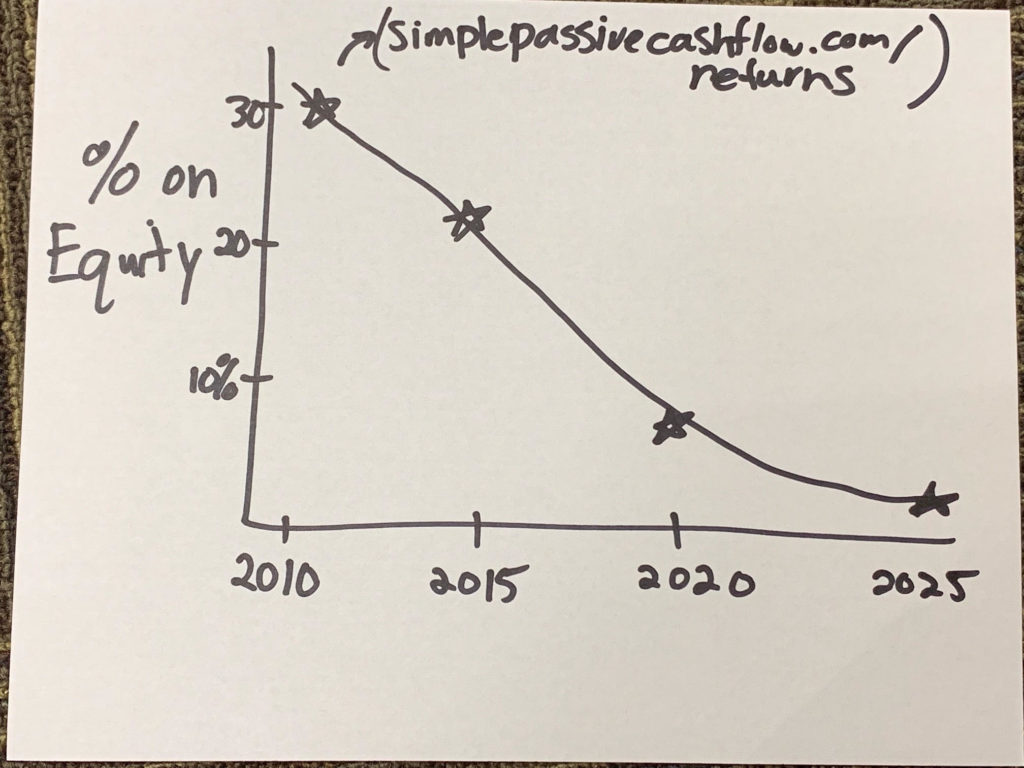

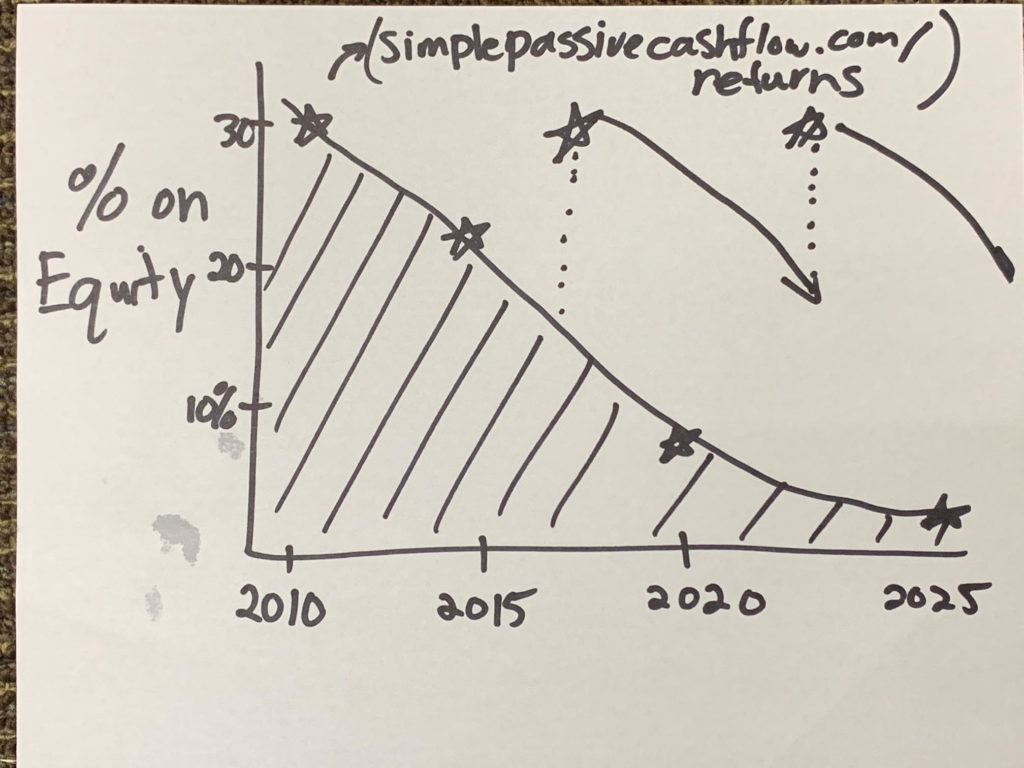

Since I feel we are in the 9th inning of an 11 inning ball game, I decided to pass on a recent Class-A apartment deal in a secondary market.

Here is my thought process…

First off, Robert Kiyosaki has a saying: “There are three sides to a coin.”

People like to argue that it is either a good time to buy or a bad time to buy. For example, they say that “MFH” is overheated or commercial is getting killed by Amazon and e-commerce. I think these are mental justifications by tire-kickers who are scared to act. I mean really how many of these people are under the accredited status (not sophisticated) or not obtained their “Simple Passive Cashflow number.”

Sophisticated investors still trying to grow live on the edge of the “coin.” They buy deals out of the reach of amateurs due to the amateurs’ lack of network/knowledge. These opportunities are undervalued, with undermarket rents, with value-add opportunity. Sophisticated investors are patient; they don’t stray from standards that force them to get crushed in a market correction. (Cashflow from other investments makes this possible.) They invest following the macro- and micro- trends and don’t gamble on gimmicks such as guessing where Amazon’s next HQ is going or where the hurricanes just drowned a market.

The trouble is that an unsophisticated investor or an outsider (in terms of having a poor network) is figuring out which of these deals transcends the two sides of coin and is on the edge. Stating the obvious (though often ignored by many)… starting out as an investor is going to be slim-pickin’s due to the lack of network. But you have to push through this rough part. You are not able to decode the noise until after a few deals or having someone mentor you.

With that out of the way let’s continue…

Real estate is one of the best risk-adjusted investments out there. In private placements or syndications, we are able to crowd-invest in larger & more stable assets while maintaining control with operators who are aligned in our best interests. By going into a project properly capitalized with adequate capital expenditure, budget, and cash reserves, you are able to remain steadfast through softness in the market where rents stagnate and vacancy decreases.

(If you are starting out you should start with turnkey rentals even though they are much more volatile)

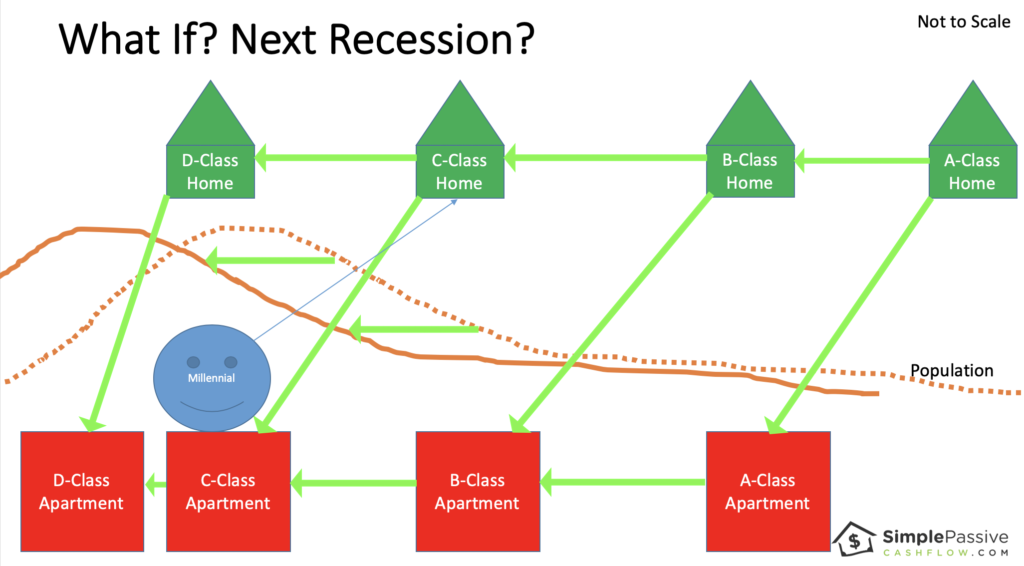

Pause there. In troubled times what happens?

People lose their jobs and there is a bit of shuffling.

Yea, people need housing, but there will be some vacancy as some people will lose their jobs and be displaced elsewhere.

Following this train of thought…

In a recession, the high end or class A will be hurt the most. It is Class A workers who fulfill much of he discretionary services. We are already seeing softness in rent by rent decreases in class A of the high-end markets such as Seattle and San Francisco.

For example a once $1,700 one bedroom is now $1,625.

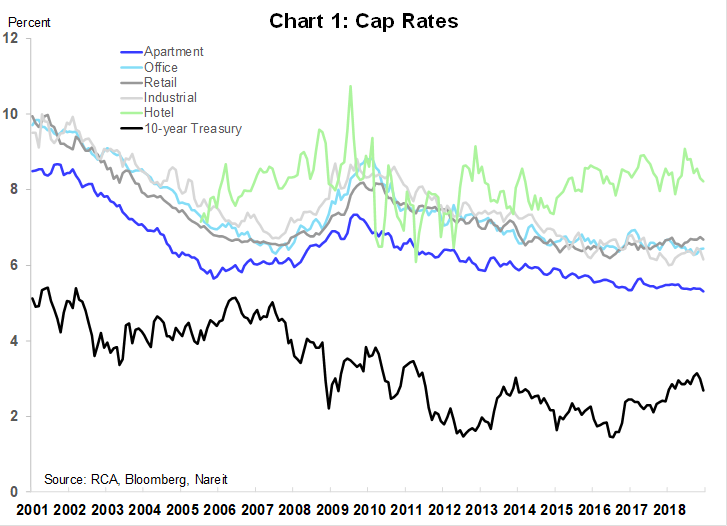

Most deals model for 1-5% in annual rent increases or escalators. Other than the Cap Rate to Reversion Cap Rate truck, this is the second most manipulated assumption in investment modeling.

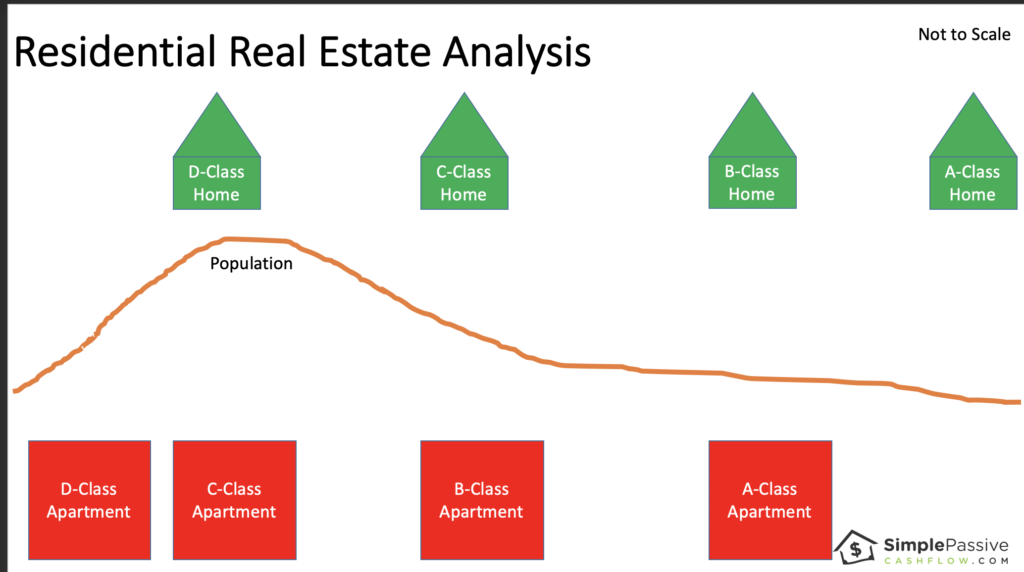

In this unfortunate but natural event, the A-Class renters will fall to class B housing. Some homeowners will even lose their jobs creating foreclosed investments for smaller investors in the single-family home scale.

What’s happens to the B and C class renters?

It is likely that they will also lose their jobs at higher or lower rates, but that is up to debate. In the same fashion as the A-Class renters, the Class B/C renters will downgrade to make ends meet.

I imagine this similar to a game of musical chairs (where the chairs are getting crappier and crappier). Or it looks a lot like the natural housing shuffle in the summer near colleges with people moving in and out. The landlord/investor is likely to see increased vacancy.

Multifamily occupancy varies from 85-95% in stabilized buildings. Some markets are hotter and some are colder. It is important to use the correct assumptions depending on the markets. For example, Dallas typically sees 92% occupancy while Oklahoma City sees 89%.

One of the reasons we love multifamily is because of the decline of the middle class and the need for more scalable workforce housing. [And those millennials can’t save] The population is increasing too.

[I like to use this image cause I make fun of millennials… this is the millennial version… cause they can’t seem to afford (or want) to own anything]

When I travel to Asia (which I see as a more mature society, for better or worse) there is a much larger wealth gap than in the USA. People are living in cramped apartments or very rare single-family homes. And they are driving a Mercedes on barely enough money to share a family moped. This is the trend that the USA is following.

As with many things, you need to look past the headlines and the general data. Instead of analyzing a whole asset class, as the media likes to do, let’s break down vacancy in terms of classes.

Here are some typical vacancy rates (notice the spread).

Class C 4.5%

Class B 5.0%

Class A 5.5%

Why? Because there is just more demand for the lower class properties cause there is more demand than supply.

Many times the business plan is the be the “best in class.” For example, businesses want to be the best mobile home park or best high end remodel because you attract the richest customers in that niche.

I like to monitor the number of new units coming online because that is your downward pressure. It is rare that new builds are for Class C or Class B.

The micro-unit trend is an attempt to build for Class C and B tenants due to the need. But often the numbers don’t make sense when you have purchased the same building materials and mobilized the same crews to build a Class B asset as opposed to a class A asset.

Let’s go through that Armageddon example again.

Class A will have to drop rents severely and see great vacancy.

Class B and C will see vacancy come up too as people are losing their jobs but should see some absorption from ex-A Class tenants.

Mom and dad will also see some absorption as deadbeat son or daughter move back home.

Shows like Friends and How I Met Your Mother will go on for another decade.

Note: one can argue that class A+ will not be affected at all which I believe is true. That’s why we are trying to invest right to enter that untouchable status.

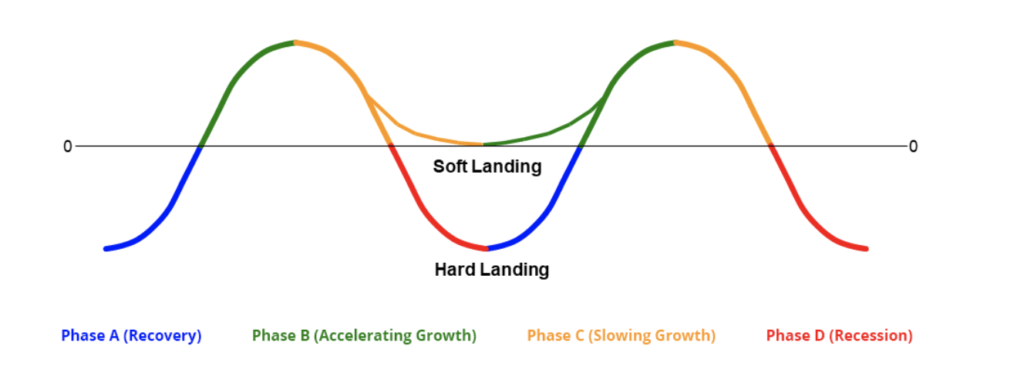

I remember when I sat through the same economic presentation at work from 2010-2014. The sentiment at the time was that it was going to be an extremely slow recovery. It makes sense that the length between the 2008 recession and now is very long which is why I mentioned an 11-inning ball game.

This is why I took a set back from some pretty Class A deals because I asked myself the following questions:

1) What will happen to the rents if IT should happen?

2) Is the modeled 90% vacancy rate going to get blown up?

Class B and C apartments in strong submarkets will perform best over the long term. If you ensure the loan term is long enough so you don’t get hurt then you should Outlast the bumpy ride ahead.

Beware of the self-destructive behavior of not investing. You know what I mean… are you someone who self-sabotages?

Understand the micro and proceed if the numbers make sense.

I have to admit Class C and B assets are boring but work especially in a seller’s market because 1) they cashflow and 2) have a forced appreciation value-add component to give you levers to pull in tough times.

Again going back to Mr. Kiyosaki’s three-sided coin quote, investors go through three stages.

Stage 1: Go into MFH… Duh (I did well at single-family rentals let me try apartments)

Stage 2: Be a contrarian investor so go into other asset classes most decent investors are afraid or don’t even know about

Stage 3: Do special projects such as Affordable house taking advantage of tax credits or specialized operators (ie take abandoned big-box space like movie theaters and convert to the latest consumer needs)

Experienced investors who were in the downturn in 2008 say its interesting that the sentiment in 2006 was exuberance that it was going to keep going up. Now in 2018 the sentiment is fear… This is a good thing.

Remember that in this market we still have:

Historically low-interest rates

Historically high rent increases (not 8% anymore but still 2-4%)

Historically low vacancies

Things to monitor if you really need to geek out on numbers:

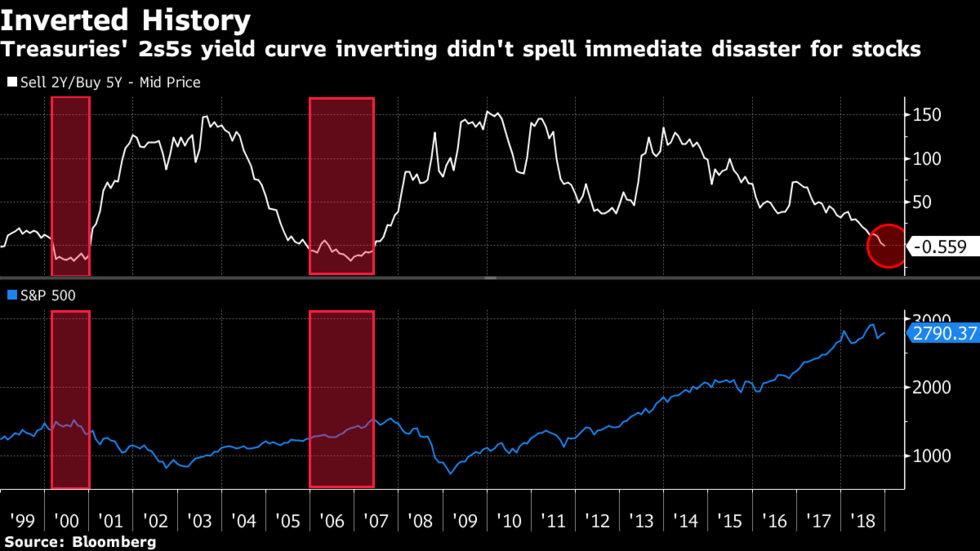

2 and 10 yield t curve. When that crosses you have just-a matter do time. Because its a measure of fear.

Automation and AI – huge shifts in jobs. People need to work but technology has been increasing since the beginning of time.

Wage growth

Bankers prospective: how deals are getting funded and by who (institutional or dumb capital)

There is a saying out there that real estate is location specific. However, when I invest in more stable asset classes its a National market based on the economy both USA and international. When you invest in a micro-economic fix and flips then its location specific. When you invest in commercial assets it’s with more stable tenants and based on the aforementioned larger economy.

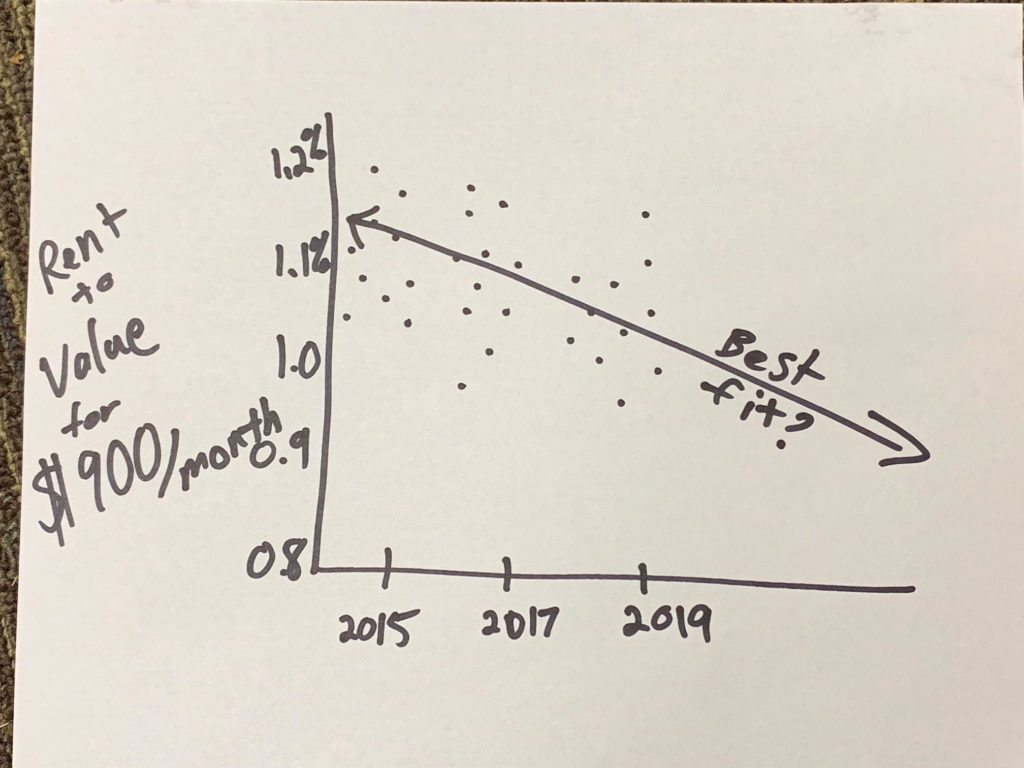

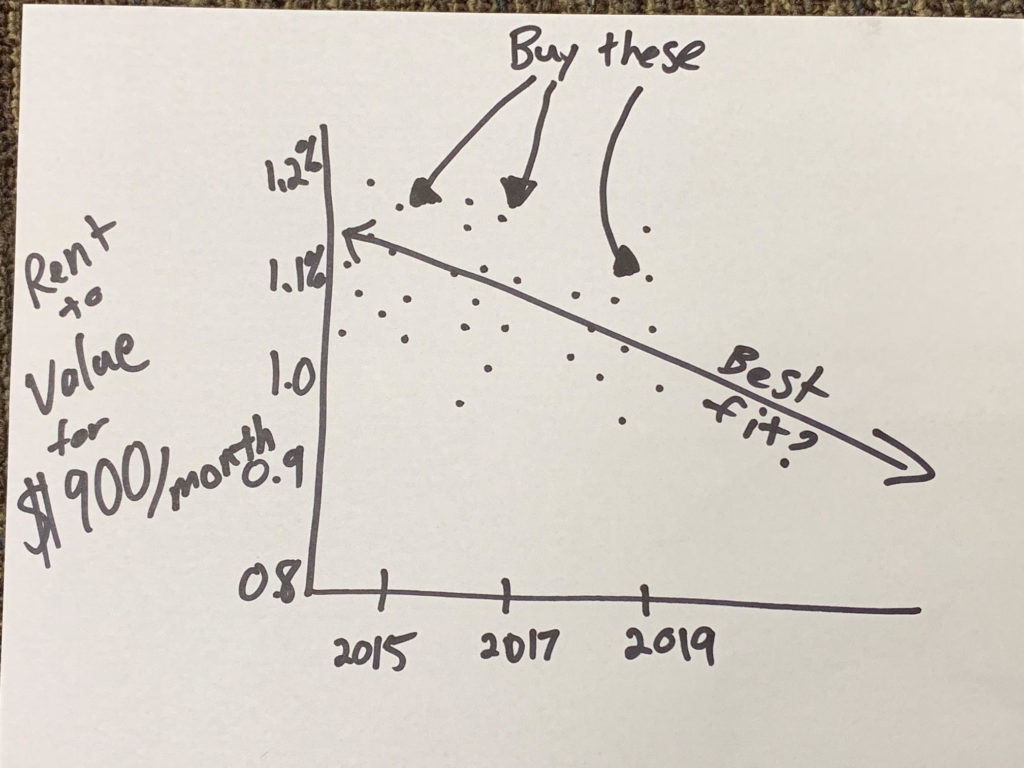

How affordable is rent really? – “During the same span, median effective rent nationally has risen by about 26%. That rent appreciation pushed the median monthly rent nationally to around $1,220 per unit to end 2018. With the US median household income being just over $62,000, this rent accounts for 24% of monthly income. Using the typical benchmark of monthly rent being 30% of monthly household income for affordability, a margin remains for renters.” – [If you stick to using 2% and under rent growths and stay away from Tier I or Primary markets you should be fine] – ALN 19.02.24

A lot of people point to the Yield-Curve as a big indicator. In the end, I do believe that real estate will go down because of consumer instability. But if you have stocks you should sell those before even thinking of lumping it into cashflow type rental real estate.

“The guy not investing right now and hoarding cash (with net worth of under $1M… because if you can live off your cashflow then cool you can do what you want) is just afraid and lacks deal flow. Its like the person who complains that there is nothing to do during the weekend in LA (insert city with a vibrant scene) when in actuality they don’t have any friends (lack dealflow)… and by the no one likes (has a bad attitude and that person who makes excuses”

Doomsday theory: Everyone talks about national debt but we are far far behind debt to GDP ratio that of Japan. When Japan hits the wall lookout. Her is my theory… watch out post-Japan Olympics when they have to let loose the belt (after a holiday period of excess calories). Leading up to a period where Japan has to save face while they are in the Olympic spotlight (and I’m not being racist cause I am Japanese and it is a thing). I don’t have the latest data but Japan is at around 250% where the USA is at 100%.

Household debt KPIs: student debt, car loans, housing debt. Which is why I like these assets that are used by the poor and middle class! #RenterForever

Lane’s theory: I’d rather be in deals that cashflow today that do better in a recession like Class C and B assets. Say it cashflows a 8%.

The guy who is stilling on the sidelines with the “hoarding cash” mindset will lose because they will make 0%.

I, on the other hand, might dip from 8% cashflow to 4% cashflow. On paper, I might be in a market with compressed cap rates but hopefully, I have forced appreciation potential if I really needed to sell – the counter move is to get 8-12 year debt to effectively bridge you to the next side of the market cycle. In the meantime you cashflow 4% which is 4% more than the “hoarding cash guy”.

In addition, remember back in the 2008 crash. 2009-2012 people did not know if that was the bottom and it was so hard to close deals in that Phase IV (see below). “Hoarding cash guy” in 2009-2012 and the few years after the next recession will likely be in the same clueless situations.

Wouldn’t you like to be in solid Class C and B assets that continued to cashflow?!? 4% x 4 years is still 16% ahead!

Now if you are “hoarding cash guy” with no deal flow then I get it. Saving cash is the best thing to do for the guy with no deal flow or does not know how to run the numbers. I guess everything does suck.

[Investors are chasing for decreasing yield these days] – REI.com – 19.03.4

[Sophisticated Investors know interest rates and caps go up and down together and their money is made in the delta between the two] – REI.com – 19.03.4

Of course, all the Pro-Apartment publications will say this: Get Ready: Recession-Proofing An Apartment Portfolio – National Apartment Association 19.03.7

But enough of this doom and gloom because most gurus out there call recession everyday just so they can have Tweetable content. And they make a living selling subcriptions to their $79/month newsletter. But we are better than the average investor! And understand that future softness could very well be slowdown before the next great bull market.

To join our Hui Deal Pipeline Club and stick with the group join below:

A pretty impressive event. Its where 2000 financial bloggers, you-tubers, and podcasts this year gathered around all this money.

In 2006, I started reading financial blogs. Sole of my favorite was getrichslowly, Wallet Hacks, and of course mr money mustache. FinCon started in 2011 with just a couple hundred people.

Real estate investing is a minority. 95% of people are debt adverse and about the 4% rule. Buying cash so so debt. Living small is selfish? Make 150k a year and retire when you are 35…

The Millionaire Next Door book is not the type of lifestyle I would like to live.

I am cool with how it is enough to be happy and content.

Other Findings:

New investment account that incorporates mobile interfaces and suto-AI. Mint app has click to invest and banking apps have click to refi. It’s a little dangerous.

A cool 5% instant liquidity online savings bank that invests in inventory loans. Let me know and I can connect you with that as I try to do more due diligence on my own.

Liberty health share – religious-based health insurance

Side gigs – consistent theme from high performing growth mindset W2 employees who are not getting fulfillment at their bureaucratic day jobs.

Interviews to follow in video…

Please share this with friends because if you don’t soon you won’t have any friends to have mid-day lunch with when you not doing anything

Article Link: Text “simple” to 314-665-1767 to download the Hui Google Drive files and the 2018 Rental Property Analyzer

For a free electronic version of my bestselling book in 12+ categories text the word “ebook” to 587-317-6099.

Please help the show by leaving a review: http://getpodcast.reviews/id/1118795347

Join the Hui Deal Pipeline Club! SimplePassiveCashflow.com/club

Pardon the grammar – I’m an Engeneer, Enginere, Engenere… I’m good with math!

________Here are the Show Notes________

I worked with Matt’s team way back when in 2014 buying turnkeys. Simplepassivecashflow.com/turnkey Since then it is interesting as times change how his strategy has changed.

We just completed the last deal for an Mobile home park. Which is a little different than apartments.

Please leave an iTunes review – Help fight negative one-star review

Earning $30,000/mo through single-family homes and seller-financed notes.

Epic Real Estate started selling turnkey properties in 2009.

Built successful portfolio, but returns lowering. However, real estate always a good purchase to buy and hold long-term.

Amortization, depreciation, appreciation, and leverage (wealth multiplier) all make real estate investing attractive.

Focusing more on lease options now for C- and D-class properties to rent properties and eventually sell them to tenant.

Went from 7-figure year as a musician to bankrupt at 34. Found real estate mentor at grocery store and life changed.

Real estate is the final frontier for the average person to have a legitimate shot a creating wealth.

Paid $22,000 for mentorship in 2006. Everyone thought it was insane, but helped him get started.

People who made it were ready for it. “Move faster than your doubts.”

Find the deal first and then the money will find you.

Authored book “Do Over” that chronicled struggles and how he built his real estate empire.

Be intentional with who you surround yourself with. Peer pressure works.

Always be looking for a coach and outgrow them. Results accelerator.

Spends $100,000/year on masterminds – worth being around the right people of doers.

Goal was to increase passive income and decrease expenses. In 4 years became “retired,” but wants to be wealthy; not just financially independent.

Bookkeeper should be the first role you should outsource. Transaction coordinators and marketing person also helpful.

Hardest part of the business is to find the deal and get into contract.

Visit www.epicrealestateinvesting.com to check out the Epic Real Estate Investing Podcast.

MFH is the obvious choice when it comes to jumping into syndications because it is the shorted logical leap for a single family home investor.

Here are some other reasons:

We need more housing for class-C and class-B renters due to population increasing and rising interest rates

Inflation favor hard assets

We are no longer a buying nation we rent (think millennials)

[This is the millennial version… cause they can’t seem to afford (or want) to own anything]

The government is trying their best to incentive investors – Follow the money people!

2018 tax changes with bonus depreciation make it better for projects like large apartments to get better tax treatment than ever before via a cost segregation.

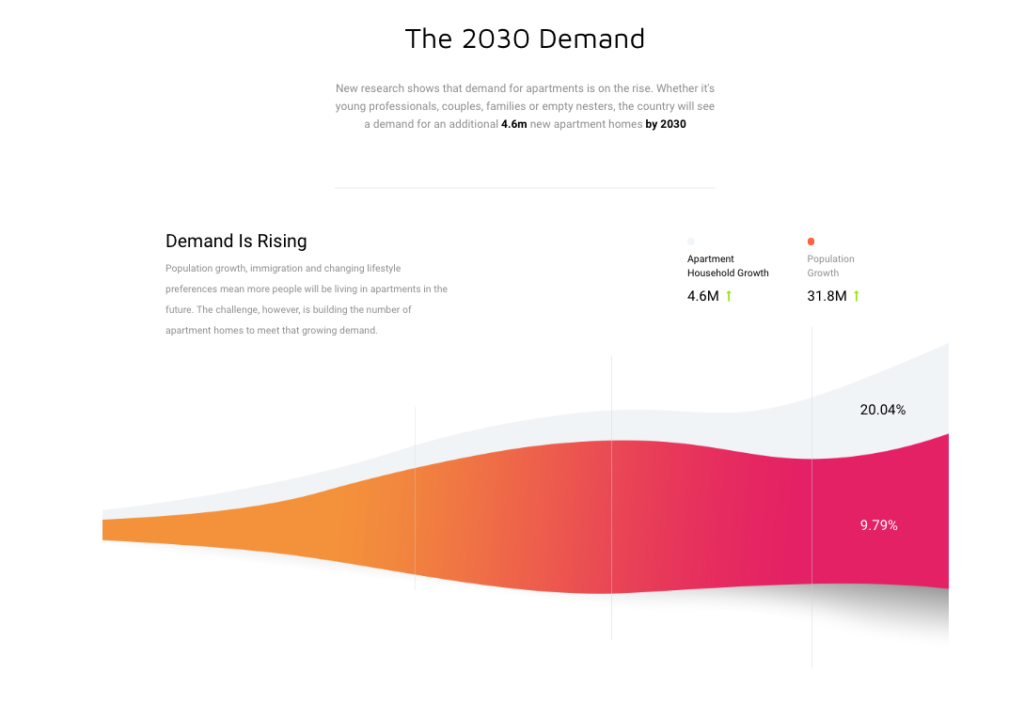

The country needs 4.6m new apartments by 2030 (Source). We need more class C and B housing. Our country is becoming more like Asian Countries where the is a bigger divide in the wealth gap and need for low-income communities.

60+ units or more to get economies of scale and to have dedicated staff on site

1970-1980s Class B or C buildings

Utilize Fannie Mae or Freddie Mac Non-Recourse debt with up to 12-year loan terms

Buy right – rehab units with $2,000-8,000 per unit – reposition by improving operations and stabilizing rents for exit

Property cashflows day one after purchase

Re-brand (new signage and online presence)

Value-add:

Poor existing property management

Old tired units or leasing center

Outdated amenities

Creative improvements using best practices and technology

Additional opportunity for extra income

Miscellaneous ideas for thought:

2010 to 2015 is the golden era of Multifamily. Many rents were going up 5-10% per year (average 2-3% in a good market).

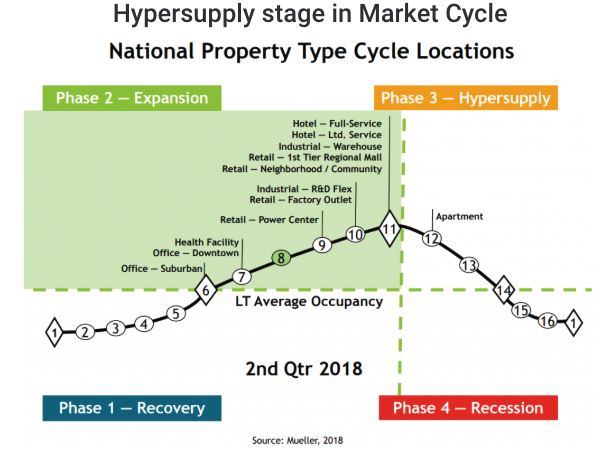

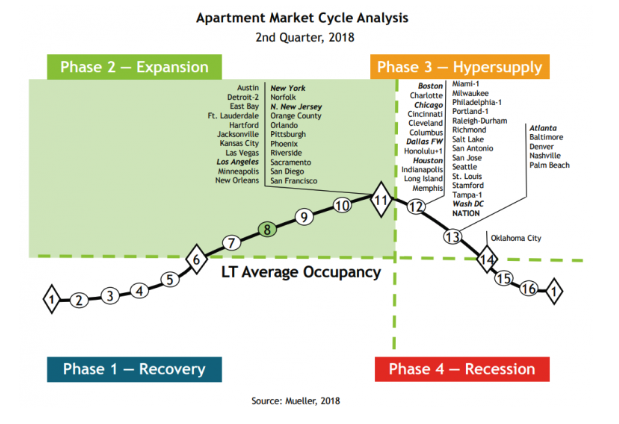

The (Global/National) markets go in cycles, the sub-markets (physical locations) go in cycles (see below)

Asset Classes go in cycles but hopefully, you are investing with the pros who transcend the high-level norm.

Lending

Unit Mix Discussion

When looking at the unit mix profile take notice of the mix of studio/efficiency units and 1,2,3 bedrooms. This can throw off your rent per square foot metric which is important when comparing comps. A sudio/1 bedrooms will have higher rent per square foot amounts however the tenants will be more transient.

The 2/3/4 bedroom units will yield lower revenue per square foot but will attract more of a family type renter and improve the intangible community aspect.

Headwinds

Millennials Leaving the Renter Pool?

Once they get married and have kids, they move out to the suburbs into a single-family house. 82% of couples between the ages of 25-39 married with 2 or more children live in a single-family home. The only difference today is that Millennials are getting married and having kids later in life so they stay in the renter pool longer. And the lack of affordable homes caused by the great recession of 2008 has delayed new builds to be created which creates more demand as population increases. New builds are really starting to come online.

The 73 million Americans aged 18 to 34 are beginning to cycle their way out of apartments and into homes. In fact, the net growth of 18-34-year-olds falls to zero by 2024.

Fun facts about new builds:

2009 and 2010, multifamily housing starts hit a low of about 100,000 per year.

The 40-year historical average (1970-2010) is 355,000 starts per year.

Multifamily housing starts gradually increased, peaking at 383,000 units in 2015. Production then declined modestly, to 381,000 in 2016 and 345,000 in 2017 but reverted to 354,000 in 2018.

Annualized multifamily housing starts stood at 289,000 units in January 2019, up from 278,000 units in December 2018, but down from the one-month annualized peak of 435,000 in January 2018.

Multifamily statistical models forecast about 401,000 average annualized starts in each of 2019 and 2020, 389,000 in 2021, and 390,000 in 2022, all of which are modestly above the 40-year historical average of 355,000 multifamily housing starts per year.

The cumulative 17-year shortfall of multifamily housing starts (benchmarked against historical norms) peaked at over one million units in 2013 but is on a choppy decline, standing at 905,000 as of February 2019.

Zelman & Associates are forecasting multifamily starts to increase 3% year-over-year in 2019 and another 1% in 2020, as opposed to a decline which many researchers previously forecasted.

MFH is great but you need to be aware of new Class A apartments being built to put downward pressure on pricing – Source MHN

MFE 2-6-19 – 2018’s Record Deal Volume Suggests Positive Trajectory for 2019 – “driven in large part by increased interest in the student housing sector, which accounted for 17% of all deal activity in the third quarter, compared with a consistent 4% over the past 13 years” – [I don’t like student housing as I am seeing an education bubble with all the lending. It’s crazy how dorms get renovated every few years]

MFE 2-6-19 -Freddie Mac Sets Multifamily Production Record – “$78 billion in total production bests the company’s prior record of $73.2 billion set in 2017. Overall, the company financed more than 860,000 rental units, more than 90% of which are considered affordable to low- and moderate-income families making 120% of area median income (AMI) and below.” – [More more more!!!]

Past performance is no indicator of future success. Many operators in Dallas 2012-2014 were able to double investors money in just a year or two – come to find out they only implemented 20% of the rehab. It was mostly market appreciation which is out of our control and can bail out a bad operator.

Pretty simple if you understand the way to utilize them and how they play together in real estate transactions

Applies a lot in larger transactions (multifamily), but can be applied as well in smaller (single family) transactions

Income (types):

Different ways you can make money on a property

Rent – not what is on the contract, but what the market would yield for the space that you have

Other Income

Pet Fees

Laundry

Reserve Parking

Late Fees

Gross Market Rent:

Sum of all the different types of income you can earn from the property

Deductions that can be taken from the Income types (can also be called Efficiency deductions):

(Loss to) Lease:

Loss of income based on the market value of the property minus the amount you are renting the property for

Example: You have a property you are renting out at $750/month. The current market value of the property is actually $825/month (based on listings in Craigslist, etc.) You have a $75 Loss to Lease per month on that property

This is money that will never be gained, as the market changes so much

This has to be factored in when looking at properties, and you should constantly monitor the market you’re in to see what kind of Loss to Lease you’re taking on

(Loss to) Vacancy:

Especially on bigger properties – you will never have it leased all the time

Normally, there is a week or two of vacancy, sometimes more (up to a month or even longer) between tenants

A lot of people like to estimate 5% loss due to vacancy, but should be considered more scientifically than just stating a number. For example, if it’s a single family home, you’ll want to factor in at least one month’s rent, which would be equivalent to 8%. If it’s a duplex you’ll want to factor in one month’s rent for your most expensive unit. The more units you have, the more you can expect that vacancy rate to go down. But be conservative when you’re writing up a deal – the smaller the deal, the higher your vacancy rate. So start at 10 if it’s a one or two unit deal, and then drop accordingly.

(Loss to) Collections:

Isn’t just money you will be getting back from tenants who are late on payments

Includes loss of money from tenants who move out and are not able to pay their balance

You need to factor it on your own in the market you are in and what the economy you are dealing in is

Example: If you are dealing in C or D type neighborhood, you will have to factor in [Loss to] Collections. If you’re in a B or A type neighborhood, then you can lower Collections down to zero and assume the loss will just come out of Vacancy

Physical Occupancy vs. Economic Occupancy in Apartment Investing:

Note this is mostly used as an example of what LP’s should be aware of. In most cases LP’s either know too little for example they just look at the Pro-Forma returns and don’t look at the assumptions that the operator used to get there. Or they spend so much time evaluating things that have little impact to the numbers for example running away when they hear of minor foundation issues or rodents that can be remediated with a few thousand dollars of seller concessions. In the Passive Investor Accelerator & Mastermind we try to focus on what is really important but obviously that is not free (but going into a bad deal is costly too). Vacancy in apartments decreases top line income and getting occupancy as high as possible is the goal. There are two different types in apartment investing 1)

Physical Occupancy and 2) Economic Occupancy. Physical occupancy (number of units that have a tenant with a signed lease, occupying a unit) is what most people are familiar with in apartment investing and what is often overlooked when a passive investor reviews the underwriting assumptions of a syndicator. This is shown on the rent roll with the tenants name next to the unit number which also needs to by physically audited with boots on the ground verification. Physical occupancy is a percentage calculated by dividing the number of occupied units by the total number of units for example a 100 unit apartment with 8 units vacant has a physical occupancy is 92% (92 ÷ 100).

Pay attention here… if a rent roll shows a unit is occupied, doesn’t necessary mean it’s also generating income. A tenant might be a deadbeat or the nice way of putting it there might be “loss to lease.”

Economic occupancy is the amount of money of actual rents received as related to the occupancy. This also takes into account tenants who don’t pay the full rent and also things like concessions ($200 move in specials, discounts to motivate tenant prospects). This is the net rents received (not including other income). The net income will deduct for bad debts/loss to lease. The economic occupancy is calculated by dividing net rent received by the gross rents possible.

On the same 100 unit apartment, assume each unit rents for $1000/mo. There’s a gross potential of $1,200,000/year (100 units x $1000 = $100,000/mo x 12 = $1,200,000/year). Using the same physical example say there are an additional 10 deadbeats (that the previous seller stuffed in there right before the sale) and 10 people only able to pay half the rent… then you are looking at an economic occupancy of 75%.

This might be a little too much info for a LP but Economic occupancy can be a sign of the following:

Bad Management and bad collection practices

Bad tenant qualification practices

PM stealing money

Bad rent collection practices

Lack of maintenance, causing tenants to leave

Or a clear sign of opportunity!

Effective Gross Income (EGI):

Gross Market Rent minus whatever loss will come out during operations (Efficiency deductions)

Real money that comes in through the property

From your EGI, you will still need to deduct your expenses (listed below)

Expenses:

Insurance

Professional Services – Leasing commissions and/or other professional services you bring in (legal, accounting fees, etc.). If you’re an LLC, you will need to put in your budget the cost (tax) for the LLC every year ($400 – $500), IRS

Regular Maintenance (landscaping, snow removal, heater service, pest control, touch-ups and minor renovations on unit before tenant moves in, fixes like clogged-up toilets, etc.)

Rule of thumb for Regular Maintenance: Brokers will place it 3% of your EGI, but is more effective to think it as dollars per unit.

Example: If property is something you bought, did a full renovation on, put tenants in, and then got it refinanced (BRRRR – Buy Rehab Rent Refinance Repeat), your maintenance should be lower because you’ve done everything and should be able to call for a warranty call at the very beginning if it’s something the contractor who did the work on your property didn’t do. If you’re very good at turning these properties over, then you should have very little maintenance going in

If it’s a newer rental, could be anywhere from $300 – $400 every year

If it’s something you’re inheriting (inheriting maintenance issues as property already has current tenants and will need to deal with it as you go), you will want to go with higher maintenance numbers: $700 – $900 per unit per year

Will really depend on how much you project it to be (check out the property thoroughly, and/or if there are existing tenants, ask them what are the maintenance issues) as it can really kill or make you a lot of money on your deal.

Property Management Fee – 6%

Property Management means looking after the property and make sure operations is running smoothly

If you are managing the property, you will want to put that in your own pocket

Asset Management Fee – 2%

If you are hiring a Property Manager, you will also need to hire an Asset Manager, or you can be the Asset Manager and that money will also go into your own pocket

Fee of managing the Property Manager

Asset Manager will be the one to pay mortgage, ensure real estate taxes are being paid, monitor the markets and ensure that the right rents are being charged, will also have veto power to veto work orders that might come up that you don’t want to have done because they’re too expensive, etc.

Asset Manager is also there to look at the real value of return on the asset

Utilities

Everything from heat, water, sewer, even CCTV systems, phone lines

You will want to look at the prior owner’s expenses for utilities were (around 18 months’ worth), or look to see what the market or other people are paying

Make a good guesstimate on what your utility projections are going to be and go from there

Real Estate Taxes

(Above the) Line:

Term sometimes used by brokers when grouping Gross Market Rent, Efficiency deductions, EGI and Expenses (everything that gets deducted out to determine the profitability of the deal)

Note: I don’t really talk in terms of Cap rates because you can manipulate the “above the line” assumptions to get whatever you want

Net Operating Income (NOI):

EGI minus all the expenses that can be deducted from it

Does not include mortgage payments or Debt Service (money you have to borrow to buy the property)

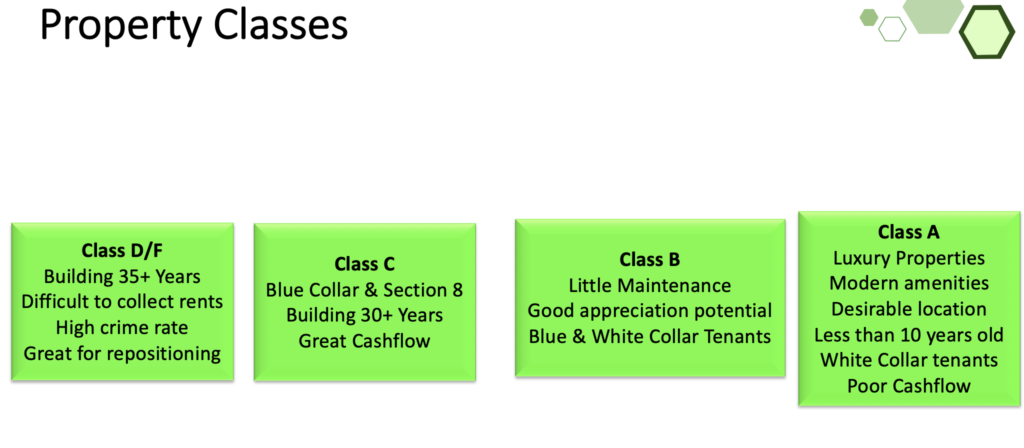

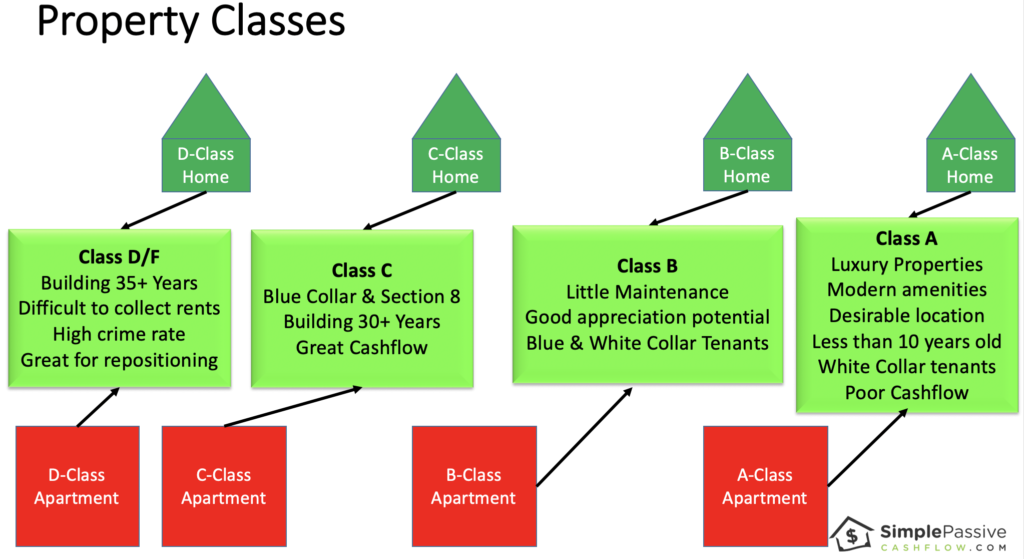

Classes:

Class A

Built in last decade and are more luxury

Struggle in recessions as white-collar workers drop back to Class B Assets

People are jogging around at night

Class B

Generally 10-25 years old

Younger white-collar and blue-collar residents

Cap rates are higher than Class A and lower than Class C

Females not advised to take that evening jog around the block

Class C

1970-1985 built

Mix of blue-collar to lower, single mothers etc

Good cashflow but comes with issues that property management must keep in check

In a recession, a lot of B and A class renters fall back to Class C

Its ok during the day but personally I would not want to be there at night

There is crime but you want to look for minimal violence/homicide

Class D

1960s and older

Generally Section 8, government-subsidized residents such as LURA, LURK with rent restrictions

You don’t even want to get out of the car to walk around during the day

High crime area, security needed

Can be amazing rewards for taking on this risk

Capital Expenditures (Cap Ex):

Also usually referred to as Below the Line expenditure but is also sometimes considered as Above the Line, depending on whether you are selling or buying a property

Long-term improvements to your building/ property

Major renovations to bring unit/ property up to market standard (replacing the roof, replacing the furnace, full renovation on a unit)

Any expense that will add long-term value to your building

You will need to set aside money for this (Cap Ex Reserve)

Not taxable as it is just money you are earning but will be setting aside in a savings account

CAP Rate:

NOI divided by the price you’re buying the property for

Determines the money that the property will give you

Example:

If NOI is $100k and the price of the property was $1 million, then CAP Rate would be 10%

Intended to be used when valuing buildings (especially commercial real estate)

Cash Flow (CF):

NOI minus Debt Service

Also determines your Return on Investment (ROI) on the property

Debt Services Covered Ratio (DSCR):

Looked at by the banks

How many times the deal can cover the Debt Service

Calculation: NOI divided by debt service

Most banks will want to see a DSCR above 1.25%, you will want to see a DSCR of above 1.5% to get a higher ROI

Green Credits:

Breaks in your interest rates for employing energy saving means

Many buildings have asbestos from the 1960-1970s. We have a binder in each office that shows how to handle different situations should the asbestos be exposed. All the managers go through training as well. As long as we don’t disturb the drywall than it’s safe. This is consistent with how many organizations do things outside of real estate… I know because I am a facilities Engineer as a day job.

How can you increase the value (increase income or decrease expenses)?

Application Fees

Late Fee

Pet Rent

Early Termination

Month to Month Fee

Lapse in Renters Insurance Fee

Redecoration Fees

Resident Discount Program (This seems counter-intuitive unless we’re at CostCo.)

Marketing Coordination Fee (to pay for social media at the property)

Eviction Holdoff Fee (You can’t pay, so we’re going to charge you not to kick you out)

“We also have community gardens which we charge for”

Offer a steam cleaner, power washer, or other useful tools for rent by residents.

Place native ads/sponsored posts from relevant local/lifestyle businesses on your community blog.

Offer furniture rental packages.

Sell ads on the digital signs in your leasing office/elevator lobby/parking garage.

Create moving kits with tape, boxes, packaging, etc. Sell them from your website, or build a set of items you can resell through Amazon. One-click buy and move!

Shared sponsored posts from local businesses on your property Instagram account.

Upsell garages, bike lockers and/or storage space.

Upsell smart home technology packages.

Offer RentPlus to help residents build long-term credit. They charge a small fee to the resident, you get a cut.

Offer interior design consulting through Havenly. Make affiliate income when your renters buy goods and services through the app.

Buy cable and Internet services in bulk at wholesale rates. Resell them to residents at a discount and make money off the markup.

Host resident events. Partner with brands who are willing to pay to get in front of your renters as a target audience. (There are lots of them out there.)

Publish a resident newsletter (print or digital). Sell ad/editorial space to local businesses.

Rent space to Amazon so they have a place to put their lockers.

Turn your move-in gift into a subscription box trial. Make money when new renters upgrade to an ongoing subscription.

Host “premium” resident events that get people excited. Charge a small admission fee. Open them to the public and charge more for non-residents.

Sell the furniture and items you showcase in your model. Partner with Wayfair, West Elm, or a local furniture store on this.

Sign up for Amazon Associates (or any other affiliate marketing network). Create timely gift/necessity guides (Mother’s Day, spring cleaning, back to school) that are relevant to your residents.

Article Link: Text “simple” to 314-665-1767 to download the Hui Google Drive files and the 2018 Rental Property Analyzer

For a free electronic version of my bestselling book in 12+ categories text the word “ebook” to 587-317-6099.

Please help the show by leaving a review: http://getpodcast.reviews/id/1118795347

Join the Hui Deal Pipeline Club! SimplePassiveCashflow.com/club

Pardon the grammar – I’m an Engeneer, Enginere, Engenere… I’m good with math!

________Here are the Show Notes________

Estate planning

Guests I have are giving insights but always hire your own person because these things require personalization

I try to bring guests on and ask the questions that I think you folks would ask.

I believe you need to have a basic level of knowledge before engaging with a professional

For those of you who are in the Mastermind and my current investors you will hear about my Fort Knox strategy which makes LLC enitites creation look like childs play

Email me any questions to feature on the next ask Lane podcast or monthly email newsletter

Andrew L. Howell is the Co-Founder of the law firm, York Howell, with a focus on asset protection.

Many useful tools out there, but where do you as an investor fall on the asset protection spectrum?

Two fundamental risks: 1) Asset-based risks 2) Direct-based risks

Real estate considered as “hot” assets because liability risks are greater – more than equity.

Liabilities both inside and outside the asset.

Typically form a holding company to hold limited liability companies to abate asset- and direct-based risks.

Holding properties in one LLC basket is good, but still risks if something happens in one property.

Concentrate on family protection first (trust, wills, etc.). Then move to next level of asset protection planning.

If own property out-of-state, advise on setting up a parent LLC in states with charging-order protection.

Tough LLC rules and taxes for poor California residents!

Need to do your due diligence on reviewing PPM’s – especially who you are doing business with.

Asset does not create liability risk for LP’s; only GP’s.

If you get personally sued, can go after your MFH syndications and other assets even as LP.

6% of current generation feels obligated to give back to kids. Instead of giving, create a bank.

Create purpose when setting up your trust.

Please reach out to teamandrew@yorkhowell.com and visit www.yorkhowell.com.

Article Link: Text “simple” to 314-665-1767 to download the Hui Google Drive files and the 2018 Rental Property Analyzer

For a free electronic version of my bestselling book in 12+ categories text the word “ebook” to 587-317-6099.

Please help the show by leaving a review: http://getpodcast.reviews/id/1118795347

Join the Hui Deal Pipeline Club! SimplePassiveCashflow.com/club

Pardon the grammar – I’m an Engeneer, Enginere, Engenere… I’m good with math!

________Here are the Show Notes________

Jake and Gino have a great podcast and definaetly fit in the category as guys who are growing and doing things right

Let’s work together to redirect money from the Wall-Street casinos and corrupt financial institutions…To help the endangered ‘Middle Class’ savers find safer, more profitable investments in Main Street opportunities benefiting local communities. Join Hui Deal Pipeline Club and check out the sSimplePassiveCashflow.co/mission

Gino Barbaro from Jackandgino.com who focuses on MFH real estate.

Group owns 848 units valued at >$50 million. Expecting to go up this year.

Took 5 years to get $25K-30K/month in passive cash flow.

Fumbling around in the beginning with smaller cash flow amounts, but snowballs over time.

Came from the corporate world to managing a family restaurant. 2008 transitioned to real estate to make better use of time outside of the kitchen.

Highly recommend reading “The E-Myth” by Michael Gerber. Need a visionary, manager, and technician for any business.

Believes you need a Connector, Executer, and the Backbone. Can’t do all 3 – pick 1 or 2 and hire out.

95% of blocks are internal. The rest are external. So, focusing on resolving limiting beliefs and get a life coach.

Google Tony Robbin’s 6 human needs. Have to continue to grow and contribute in a large way.

Relocated to Florida and aiming to obtain $40K/month by end of this year.

Have lifestyle work for his business; not his business work for his lifestyle.

Becoming more efficient by hiring a VA and Digital Marketer for jackandgino.com. Wants to spread content and message; not work on menial tasks.

Focus on 1 or 2 niches for real estate and become an expert at it.

MFH has more barrier-to-entry v. stocks, crytocurrencies, etc. The more people in it, the less profit margin there will be.

Share weekly successes. It’s not bragging, it inspires people and surround yourself with the right people.

Be present in the moment. When you’re at work, with family, etc. focus on dealing with that situation.

Visit www.jackandgino.com. Also on FB, LinkedIn, Twitter, and Instagram. E-mail works too: gino@jackandgino.com.