https://youtu.be/5_Slm_guB8EBRRRR is an acronym for buy, rehab, rent, refinance, repeat.

If you have done one of these deals before good job you probably made a bunch of equity and likely got into a deal for no money. For my outsiders’ prospective its successful most times (~70%) but it always takes Time. As higher net worth investors, for some of us at least time is more important than getting the best deal. When you add in an element of risk it makes the decision closer. Most Accredited investors would not bother with a Turnkey rental and a BRRR because of scalability. The sub-$200,000 bro might get really excited about getting into a cool $60,000 property with no equity after a successful BRRRR however $20,000 of manufactured equity means very little for an Accredited investor.

Other Considerations

Have you done a partnership deal with this GC before? Is this a small-time GC or a medium/larger sized builder? Either way, I’d be very skeptical of the deal unless he is incentivized to do you a favor in return for future referrals or some type of reciprocation down the road. I would be super careful before getting into bed with a GC on a project..especially if this is the first partnership type deal you are doing right now.

Maybe I’m just cynical but I feel the business proposition puts all the risk on you and he is free-rolling and possibly incentivized to screw you over.

Assuming as-is value is $160k, $40k construction price, ARV of $250k.

Off the bat, the renovation could easily go over (as larger renovations typically do) which may translate to 25% overage on the $40k estimate. That’ll put the reno at $50k.

Let’s say the builder has other higher-paying renovation jobs/priorities or that he concentrates on other items and the home reno goes until ~March.

You are looking at best-case scenario may be a ~$20k profit if everything goes perfectly for shouldering all the risk.

There is no backup plan if the house doesn’t sell. The ownership of the property is convoluted and you won’t be able to execute a cashout refinance (unless you pay him off for the renovation costs in full, but then how do you calculate his profit margins since the GC is not going to work for free). Say the appraisal comes back at ~$250k, but the best offer you get is ~$210k? At a sales price of ~84% of appraisal, I’d rather just refinance at ultra-low interest rates, turn the house into a rental (long-term or corporate rental, etc.), ride out the COVID craziness and re-assess in a year or later down the road.

Now, if the builder/GC is shady…and I’ve had awesome GC’s and I’ve also personally had to fire at least 8-10 for a myriad of reasons. But for the sake of example:

GC takes there time and overcharges you for the renovation, he makes up a bunch of BS and charges you $80K for the renovation even though the actual cost of the renovation is $40K. The extra $40k he’s charging could be to pump up his overhead rates and fake billing hours, he could supply receipts for materials that he will (or has already used) on another project, mark up other jobs or artificially increase the scope, or have items “stolen” and need to be repurchased, send you pictures of problems that need to be fixed from another house, the GC could have friends/relatives in other trades that markup their rates via a kickback scheme, etc. These are extreme examples but they happen more than you’d think. The all-in break-even point is now over $240k. And if the house sells for only $220k…guess what – the GC is going to be screaming that it’s YOUR fault…yada yada and say he needs the $20k shortfall to pay his people or he’ll put a contractor lien your house, sue you, etc. etc.

What if the renovation goes sideways and you need to fire him midway through the job?

To be honest…I would strongly advise against this partnership deal and just go the simple and straight-forward time tested route of getting bids for the renovation from multiple licensed GCs (through a referral from other investors if possible).

Set up a standard draw schedule based on project completion milestones

A full scope of work and signed construction contract

All the other standard stuff that comes along with a renovation… we can help you this in the Incubator

This option you have multiple exit strategies and have the ability to fire the GC for subpar work. Plus you are taking all the risk anyways with the partnership route, so this option is a much better risk/reward proposition in my opinion. It is very easy to get into partnerships….but HARD to get out of them and this small sfh could become a huge pain in the ass if the project goes sideways…believe me from experience. I would 100% prefer to keep the lines very clear between the owner of the property and the contractor doing a fixed scope of work to be delivered by a specified date at a predetermined price.

My two cents anyway 🙂

For those who are able to save more than $30k a year or have substantial liquidity (over 200k), being a landlord and especially flipping is a lot of work. If you like it cool/good for you… but just remember why we got into this… To be free from a JOB. A lot of us (80%) who stumble upon simplepassivecashflow.com and start drinking Kool-Aide will be financially free in 4-7 years pending taking action. So I always urge people to start with the end in mind and take a more passive approach.

Focus on being an Investor not a Landlord.

Do the math here… with 300 dollars per property (2 months of work to buy a turnkey rental) you are going to need 20-40 of these to replace your income. I have 10 of these and have systems in place but have 1-2 evictions a year and 3-4 big things that happen. Image if I had 30, just 3 x those numbers.

Directly investing in a turnkey rental or small MFH is a good way to start to learn and build up the war chest to go into my scaleable investments such as private placement syndications.

If your net worth (income minus expenses) is under $300,000 or barely save $30,000, syndications are not for you. Stick with these Turnkey rentals despite what Gurus (who are trying to sell you their program) tell you for now. They have a little higher gains (a lot more volatility) but a syndicator who is willing to put you in a deal with more than 10-20% of your net worth is asking for trouble.

*PS never like the idea of wholeselling where you basically steal houses from people at 50 cents on the dollar and say you are “helping people solve problems”

My last BRRR ever 😁 No more direct ownership rentals

https://youtu.be/qzErI3chAZ4

This is process on my Last 2021 BRRR – its a complete PITA

In these challenging times, we’re here to answer your questions.

These days, your house is more than your home. It’s your home base, your safe spot, your office, your kids’ classroom, your entertainment space. Now more than ever, it’s the center of your life. If your situation has changed or if you’re out of work right now due to the Coronavirus Pandemic, the last thing you want to think about is not having enough money to pay for your home. Thankfully, you have options, but they can be confusing. That’s why we’re here: to help you understand your options right now-and figure out which option is best for you later, based upon your individual financial situation.

What help can I get now?

Under the CARES Act, you are eligible for a forbearance if you have a federally backed mortgage loan. It’s the first option if you are experiencing a hardship due to the Coronavirus and meant to help you before you fall behind. As a borrower, you may request a forbearance on your federally backed mortgage.

A forbearance is a temporary suspension of your monthly mortgage payments.

It does not mean your payments are forgiven.

It’s important for you to know that once the forbearance period has ended, the suspended portion is due—but you will not have to pay it back all at once. You have options.

The CARES ACT allows a borrower to have an initial forbearance period of 180 days regardless of their delinquency status. After that, if you’re still financially impacted by the Coronavirus Pandemic, you can extend up to an additional 180 days.

It’s not always easy to see whether your mortgage loan is federally backed. Or, in other words, who owns your mortgage loan. Many mortgage loans are sold and the servicer you pay every month may not own your mortgage.

There are some online tools you can use to look up who owns your mortgage:

Loans insured or guaranteed by FHA, VA, or the USDA are also federally backed loans.

When might deferral be an option for me?

A deferral program was just announced which will go into effect on July 1, 2020 for Fannie Mae and Freddie Mac federally backed loans. It is only available after your financial hardship has ended or the forbearance periods are exhausted. A deferral enables you to avoid having to pay your suspended mortgage payments all at once typically by adding a non-interest bearing loan at the end of your mortgage, but repayable if you sell your home. Depending on your individual financial situation, we will work with you on available options. Other options available also depending upon your financial situation and the type of loan you have include:

A reinstatement, which means paying what you owe on missed payments if you can afford it.

A repayment plan, which means spreading what you owe on missed payments over a short period of time.

A loan modification, which modifies the terms of your loan permanently in order to change your payment amount.

The website is your key resource for information, guidance, and tools. It’s also the place where you may request a forbearance if you have a hardship due to Coronavirus. To get started, just visit www.loanadministration.com, complete and submit the request form.

If you’re already on a forbearance plan, there is nothing more to do right now. We will be in touch with you to discuss your options before your forbearance ends.

In the meantime, please stay safe and stay well.

Confirmation of approval!

Thank you for reaching out to us about mortgage payment assistance options. This email confirms that your forbearance plan is in effect. A forbearance plan is a temporary suspension of your mortgage payments, in this case, due to the Coronavirus Pandemic. It is intended to allow you the time and flexibility to manage the challenges affecting your ability to pay your mortgage.

We are here to assist you now and when your hardship is over.

The federal CARES Act (the Coronavirus Aid, Relief, and Economic Security Act) offers mortgage assistance options for borrowers who have federally backed mortgages and who are experiencing financial hardship as a result of the Coronavirus. The mortgage assistance option available is forbearance.

Prior to the end of your forbearance period we will work with you to determine your best options based on your financial situation. These may include:

If you are still impacted by the Coronavirus Pandemic:

1. Extension of the Forbearance Plan: The ability to extend the forbearance period. There will be no additional fees, penalties or additional interest (beyond scheduled amounts) added to your account, if your hardship continues.

If your financial hardship has ended, there are additional options available to assist you with the suspended payments:

1. Loan Reinstatement: Bring your mortgage current by repaying your suspended payments in one lump sum. Please see the total amount due on your statement.

2. Repayment Plan: The total amount of suspended payments is spread out over future payments until the full amount is repaid. *

3. Loan Modification: Permanently change the terms of your mortgage to bring it current. *

4. Partial Claim (for FHA-insured loans only): A Partial Claim is a no interest junior loan secured by your property. No payments are due on the partial claim until the payoff, maturity or acceleration of your insured mortgage, including for the sale of your property or a refinancing, or the termination of FHA insurance on your mortgage. If you are not eligible for the COVID-19 Standalone Partial Claim, you will be evaluated for the FHA’s other loss mitigation tools to help you repay the balance owed over time.

*Available options may vary depending on investor guidelines. Additional eligibility requirements and documentation may be required for these options.

Important Information to Come

In the next several days, you will be receiving a letter that provides the details of your forbearance plan. Please carefully review all the information provided in the letter including the options that may be available to you after the forbearance plan period.

A Note About Automatic Payments

If your automatic monthly draft was set up with us, your payment will be stopped when your forbearance plan begins.

If you set up monthly drafting (bill pay) with your financial institution, you will need to contact them directly to stop automatic drafting.

Transcription:

In this short video, I’m going to show you guys how to put your loans into forbearance and I’ll walk you through some of the screenshots on it. This is the story but if you’re using the internet and one day he will try to rent them out. And then he became one, stop me. I got this email recently from my mortgage company. Actually, this is my servicer send lar, email saying that due to the Coronavirus and all the challenging times, the job brought this up to my attention that a forbearance in a temporary suspension of your monthly mortgage payment does not mean your payments are forgiven is important for you to know once that the forbearance period ended the suspension portion is due and you will not have to pay it back all at once you have some options. The Cures Act allows a borrower to have initial forbearance up to 180 days regardless of the liquid status. Scrolling down on this For Fannie Mae and Freddie Mac, every bank loans, see how we can do this to make you want to click on the link here and I’ll walk you guys through me trying to apply for this thing and see really how hard it is to put your loan in forbearance. So my lender on this particular property, it’s a turnkey rental in Birmingham, Alabama. But that doesn’t really matter. The only thing that matters is I’m using settler A lot of you guys are using some different servicers. On these servicers work with you know, folks like Wells Fargo Bank of America, servicers just is the person that interacts with you and collects the payments and that you basically these days, you just do everything through this internet portal. So I’ve logged in here and what you want to look for is something that says some kind of Coronavirus or forbearance option, usually have a flag in here it is for me, so I’m just going to click right here. Basically, they want you to certify that you’re telling the truth and everything. So acknowledging here I’m going to put in my low numbers of security number properties and press Next. Next screen, they’re asking if there was a financial hardship due to Corona virus. Yes, we were impacted. And remember this is they’re asking if you’ve been impacted, not necessarily infected. And that’s I think that’s what’s throwing a lot of people off. Of course, I’m not giving any tax legal or professional advice here, I’m just doing a holiday, how I would do it. Here’s kind of the forbearance option number forbearance is not really like you’re getting your payments, forgiven or anything like that. It’s more that you’re getting your payments delayed, which is nice, I mean time value of money. I’d rather kind of hoard cash a little bit, especially if you’ve got some other liabilities going on delay and basically they’re going to tack it on at the end and Right on the third or fourth month, your next payment is due anyway. Can you do the process, they kind of spell this out a couple ways just because there’s so much confusion over it again, they just pretty much tack it on at the end and you got to make sure you got this money. At month four or five or six, I think how long you’re going to do it. There’s a couple options here. Whether you want to take the three month forbearance options, and I think that’s they’re going to give that to everybody. But if there’s an option here, if you want to extend it out, you’re probably going to have to send in some a little bit more proof. You know, I want the longest term but the least least amount of headaches in interaction with you guys. So yes, and yes, Smith, see what happens. This confirms that you have been placed in the forbearance plan I think that’s it and there’s no other screen. So I think that’s about it. I usually set up auto payment on all my loans. So what I’m thinking is hopefully they just won’t fall. next few payments but I got the money in the bank anyway in case they do I just mainly did this to show you guys who are in some financial trouble out there that you know this is an option and it’s pretty simple to do you don’t have to talk to anybody. If you guys want more help with this, check out our newly started incubator group for new remote investors check out our podcasts will pass the cash flow.com and please share this with your friends and subscribe to the YouTube channel. I’ll see you guys later

this website offers very genuine information concerning real estate for investment purposes every investor situation is unique always seek the services of licensed third party appraisers inspectors to verify the value and condition of any property you intend to purchase. Use the services of professional title and escrow companies and licensed tax investment and or legal advisor before relying on any information contained here and information is not guarantee as in every investment there is risk. The content found here is just my opinion and things change And I reserve the right to change my mind. Above all else, do your own analysis and think for yourself because in the end, you’re the only person who is going to look out for your best interests.

This is a nice way to make 10 grand on the side, the way it works is authorized user goes on your account for a couple of months, and then you take them off. And most cards you can have two authorized user per card. So if you do the math, it’s like one every month one of these things every month on average, to add and take off an authorized user takes about five minutes. So let’s just say you had a car that was 15 grand credit limit, and it was got a back in the day, 10 years plus and the broker is telling you, we’re going to give you 200 bucks every time an authorized user signs up after the two billing cycles typically go around. So the broker will tell you, hey, add this person on this account. Here’s other social security birthdate address name, you add them on your account. A lot of times this can be done through your credit card portal. And then in a couple months, you get an email from the broker saying hey, everything’s all good. You can remove them now But yeah, I made 10 grand doing this in my 2019 year, go to SimplePassiveCashflow.com/tradelines and check out the E course which is on sale right now.

The Hui Deal Pipeline Club is a free investor club where I filter investments and underwrite the numbers and partners myself. Unlike other investor lists and groups, my investors have personal access to me and know that I personally have skin in the game investing alongside with my investors.

Taxes – In the beginning of the acquisition process you have to assume part the taxes as a certain percentage of the market price. However keep in mind that every county calculates this differently and re-assesses the tax basis for properties especially when the property transfers ownership. Best tip is to get around other passive investors in that area to ask them what the change as been or to assume that taxes will go up 10-80%.

Insurance – You can take a certain percentage outlined in the spreadsheet, ask the current owner (if you believe them), or what we suggest is to get one of our insurance referrals within the mastermind to give you an actual value.

Management – This is typically 8-10% of the rental revenue plus 50-100% of the first months rent. The property management can also collect additional fees by splitting late fees or charge for renewing previous tenant leases. This is where it is important to have peers or a mentor to save you hidden dollars here. Also make sure you pick a good one with this guide.

Vacancy/Turnover Expenses – Typically it takes 2-6 weeks to do some touch ups around the property after a tenant moves out to when the new tenant moves in. 4 week vacancy is 1/12th loss rents and needs to be accounted for as a “Vacancy” expense line item. This is where most novice investors fail to account for.

Maintenance – I have always been told to put aside 10% of the rents or 1 months rents as money set aside to fix random things in the property. Also remember that when you old tenant moves out you might have to fix a thing or two (or $20,000).

Also don’t forget about contract services such as lawn/yard service, snow removal, pest control, or pool maintenance.

Warning: Some nerve-racking property inspection. Don’t watch this if you’re having your meal!

Cap Ex – This is not in your net operating income for all you geeks (engineers) crunching numbers but this is another 10% or so going to a cash reserve account to pay for broken stuff down the 2-15 year road. This money is to pay for large ticket items. I say geeks because experienced landlords know that its very hard to predict this stuff and it is a waste of time to track and build models to predict this stuff. In reality the best thing you can do is spend your time not in Spreadsheet Land but find more deals to decrease your risk but making more cashflow! Easier said than done when you are limited with fund and getting started which is why you get a mentor to mitigate your risk and understand that these scary things is exactly why you should push forward because most people will back out and thin your competition.

Utilities – In most single family homes the tenant is in charge of the utilities (electric, gas, trash, sewer, water) which makes you life easier. However in 2-4+ unit arrangements the responsibility is all over the place.

HOA Fees – It worth mentioning but check if your property has this. Condo or townhouses typically have a HOA monthly fee and is why we don’t recommend them as investments in addition the face that it is a nightmare dealing with their governance system.

Other expenses not associated with rental property but more as a part of your investor business:

CPA to do your taxes

Lawyers to deal with lawsuits

Most times a professional property management company will handle evictions and pass through costs to you.

And are you tired of running after financial freedom, struggling to pay your student debt even as an established professional doctor?

Physicians are not the only ones who can issue an Rx (prescription). This will be my financial freedom Rx to them. Whether they are junior professionals or senior professionals it’s never too early or too late to lay down a financial goal. Besides, money is a tool to gain more freedom.

As a doctor, have you ever found yourself in this kind of scenario as well?

Let’s face it!

Doctors are misunderstood when it comes to money or finances. Most people think that you’re high income earners (sad to say it comes with high tax as well) in fact, it’s true but mainly depends on specialization and level of seniority.

https://www.youtube.com/watch?v=3CEqQ5oMCvc

It isn’t until after spending years in medical school to earn their degrees, the whole residency system, and finally taking the requisite board exams that many physicians will enter the full-time workforce and start making the “big money”.

At that point, there is so much delayed gratification and external expectation that “doctors are rich and has huge wealth” to buy a large house or fancy car.

!!! Attention Doctors !!! Pay 11% in overall tax rate as paid medical professional.

Here are my tax returns and in 2019, I paid ZERO in taxes.

Let me show you how!

“FYI, I just got my tax returns back. My effective federal tax rate went down from 29 to 15% in spite of the fact that my income doubled in 2020. All thanks to you and FOOM! It’s helped me adjust my mindset, learn more about the tax code, and implement effective strategies.”

Sure doctors make good money (more and more going to insurance companies- like dealing with disability insurance and admin), but most people don’t realize they work long hours. The burden of student loan debt, credit card debt, and payments on new houses and cars cut into their income, facing financial uncertainties, and make it hard for many to grow their wealth.

Additional downsides are malpractice suits. Stemming from negligence claims from misdiagnosis, superfluous patient claims, or untimely release. Side note (I am not a lawyer) I believe all doctors should have an international trust and not mess around with flimsy LLCs which I have seen getting blown up all the time or pressured into a bad settlement amount (average malpractice settlement amount was $350k per The National Practitioner Data Bank.)

With those in mind, here are five practical tips to help doctors and medical professionals achieve Financial Freedom.

5 Tips for Physicians to Achieve Financial Freedom

Set up a REALISTIC plan

You entered med school because you planned for it!

In reaching one’s goal whether it be in your career, relationship there must be a plan to set things up for success. The same goes with your finances, there has to be a financial plan (especially if you still have a student loan). Another TIP: Consult a financial advisor who can help you manage your personal finance if you have queries about life insurance, strategies to maximize your Roth IRA for your retirement plan, and all about financial literacy. You have an option to join our syndicate as well. We talk about real estate investing, rental property, asset protection, estate planning, and how high income individuals like you can gain more cash flow and passive income.

Remember, as Benjamin Franklin once said, “If you fail to plan, you are planning to fail.”

https://www.youtube.com/watch?v=I1eVpkOPWMI

Stick to your plan NOT on your colleague’s plan

It’s easy to be disheartened when you compare yourself with others’ financial life. For some, this is a struggle, especially with the booming social media.

I understand, you’ve been deprived for so long! You had a low salary as a trainee or resident, long hours of duty, always on call, no social life, and late-night work. Needless to say, you need to focus on your OWN PLAN towards a better financial future and be able to come up with suitable financial decisions.

It won’t be easy, but it’s achievable, with your determination and disciplined financial practices.

Take note, this won’t be forever!

Once you arranged your financial life, reached financial success, and (if possible) did your retirement planning, you’ll be grateful that you did it!

Invest on ASSETS & live WITHIN your means

Never live way beyond your means especially if you’ll be spending your money on liabilities rather than buying assets (real estate investment). Just because you’re earning more than you are used to, as a resident, doesn’t mean you’ll go all the way.

https://youtu.be/3zUvhJOzvkI

Think about having a comfortable retirement (perhaps an early retirement), what happens if there are scenarios that are beyond your control (disability, death, environmental disaster), being debt-free (or having good debt instead of bad debt), and reaching financial independence.

Save MORE than enough

This is connected to the previous tip that will benefit not only you (for retirement savings or you can become a business owner) but your family as well. If you still cannot afford a luxurious house, rent for the meantime then save and invest the others. If you’re planning to buy your dream Tesla car, afford a modest Honda/ Toyota and let your other money work for you.

Follow REAL experts advise

Beware of those who are pretending to be financial advisor claiming that they will help you obtain your financial independence, reap more money, and secure fiscal peace.

Don’t waste your money on them!

Check on their credibility, talk to some of their clients and ask them how they can help you.

Remember: Diagnose if you’re watching or talking to a real financial expert.

You see, this pandemic caused a lot of difficulties to so many including doctors and medical professional. They are not spared! Trends you should know

Physicians are seeing fewer patients. 41% of physicians saw patient volume decreases of 26% or more.

Physicians are making less money.

They are making major staff reductions.

New physicians entering practice may not be able to get their first or second choice of employment opportunities, which was not the case a year ago.

More physicians have reached out to physician recruiting firms over the past six months than they’ve had at any time in recent history.

All in all, financial freedom is attainable for Doctors and Medical Professionals. Same as everyone else, who grow older and face the reality of mortality, physicians that get further into their careers will soon start to face the reality of their preparedness for retirement.

But again as I said it’s never too late to manage your money well, saving and investing it well (real estate investment), and build your wealth that is beneficial to you.

Remember, your time and money are valuable.

Video: Doctor Using Short Term Rentals for FI – David Draghinas from DoctorUnbound

https://www.youtube.com/watch?v=hJhVAFN0Zw8

Private equity commercial real estate offers cash flow, capital growth, and capital preservation are prime examples of assets consistent with personal and investment objectives.

These include:

Assuming responsibility for their timetables. By having the option to take additional downtime without agonizing over salary.

Opportunity from stress of how government and insurance agency strategies will influence their training and earnings.

Less stress over claims and other lawful consequences of rehearsing medication.

Needing to leave an inheritance and give generational riches that will last over different ages.

Having additional time and assets to serve others by adding to good cause and worthwhile motivations.

To discover fulfillment and satisfaction in building different organizations and associations outside of medication.

Besides immunity to economic downturns (COVID19) and inflation, private investments offer investors higher returns at lower risk than public options.

Tadah! Proof that it works!

Image (below): Hui member’s tax form for 2019. AGI of 429k and 47k taxes paid!

I am trying to find a way, and need your insights, in becoming a Qualified Real Estate Professional in 2021!Challenge #1: By law, I need to clock in more hours as an ACTIVE, RE Professional than an emergency physician i.e 51% vs. 49%. Right ?Solution #1: I will be cutting back to 144 hrs/month as an EM Doc, starting on Jan 1st, 2021. So, if I “work” an additional 145+ hours/month (4.83 hrs/day) as an active, RE professional, I would qualify that part. Right ? Lane (Not A CPA): You are partially right there you need to have 750 hours at least of active (a lot of exclusions there so I don’t want to just generally throw that word around) participation. Technically 49% or less of you time being a doctor is what you need but I would say as a best practice is for your spouse to be the person qualifying and not yourself if at all possible. Challenge #2: I need to clock in 750+ hours of active RE professional work per year and I know that being an LP in any Nap Cap syndications or and researching any other PASSIVE investment does NOT qualify me. Right ? Correct, you are not a managing member and do not have carried interest (not guaranteeing the loan or much skin on the line)Solution#2: Do I have to become a state licensed real estate agent, in Texas, and start listing SMF’s to qualify for that active work or can you think of any other activity that may qualify me instead ? This has nothing to do with Active Participation in your portfolio. This is a common misnomer. Solution #3: I have a friend who owns and manages his own, 40+ SFH’s, in 3 different states. If I help him manage these homes or help him look for future properties to purchase (and add to his portfolio), will that qualify me as an RE prof. ? This has nothing to do with Active Participation in your portfolio. Solution #4: Does becoming a GP in any future syndications qualify me as a RE Professional ? Will those future dividends/proceeds now become active income vs. passive ? This might be a possibility here. Consult your CPA and coach them through your logic. This is where the Family Office Ohana Mastermind comes in where many people are educating and sharing best practices to set up their family affairs and bring their CPA/Tax professionals on board.

In general, remind me again, why can’t my passive gains in my ER Hospital ownerships can NOT offset, dollar for dollar, the K1 losses from my passive MFH syndications ?

Passive losses (PALs) can offset Passive gains.Your time and money is valuable – often over $500-1k an hour!

Many of you folks have have some relationship with a financial planner, advisor, insurance agent, accountant, attorney, etc. When we take a holistic view of their planning, however, most are financially imbalanced. They are often exposed to unnecessary risks from embedded taxes, lawsuits, lifestyle factors, inefficient use of assets, etc. Failing to address all of these forces places downward pressure on their ability to build wealth.

Here, we bring together leading professionals in the fields of financial planning, taxation, law, practice management, succession planning, and client retention. This way, we can best assist our clients in addressing these issues and achieving optimal financial balance in their lives.

For a surgery to be successful, you need several team specialists available to address the various circumstances. Why would your unique planning situation be any different?

140-Character Bio: Father, Husband, Son. Industrial Engineering Consultant, part time options trader and real estate investor.

1) How much simple passive Cashflow are you making today and how are you doing it?

(You don’t need to give a number if you would like privacy. You can be vague such as halfway to quitting my job, cover my mortgage, Make 25% of my expenses, over $10k, although people like when people open up the kimono.)

About $1,700 per month PRO FORMA – accounting for a conservative amount of vacancy, maintenance, capex and management. 7 rental properties and counting. It is passive for the most part because they are all professionally managed. I spend very little time after the initial acquisition and rehab.

2) What is your Han Solo moment – Han Solo and his buddy Chewbacca from Star Wars were cruising around the galaxy as lowlife smugglers but then cross paths with Luke and Leia and his life took a pivot point. Describe the resistance that was the catalyst for change.

Did you “burn the boats” or did you let it happen naturally – was there an internal (you decided to make a change on own – what was thought process?) or external trigger (ie got fired from your job)?

I love Star Wars 🙂

I can talk about the moment when I realized I didn’t want to be a high powered consultant for the rest of my life. Then I realized that I had NO IDEA what I wanted to do with the rest of my life…

3) Worst life/business moment what did you do after? Lesson learned?

I could take this multiple directions…would like some examples of what others have answered…

4) Current 2-week experiment and 6-month project? (90-180 day goal) A mark of a high performer is to put your ego aside and accept the help of others and mastermind maybe folks can help you by you asking.

2 week experiment: I recently took on a “mentee” and asked him to help me find deals by driving for dollars.

6 month project: building a direct mail campaign to increase my deal flow.

5) What is your simple passive Cashflow number? Now imagine you had 2x that amount… Describe your ideal day, detailed routine, and what projects you are working on.

Assuming you mean how much cashflow I need to not work?

$6K per month and my wife and I could comfortably both not have to work, so that is the goal right now. That might increase depending on where we buy our next house (in a few years) and how many kids we have.

2x that amount…I’d wake up early, before the kids, and do my “Miracle Morning” routine, including meditation and a 1 hour workout. When the kids and my wife wake up, we would do something outside. One of our long term goals is to own a lake house, so I’d probably be working on improvement my lake house or future primary residence. I want my future primary residence and lake house to be value-add investments…

6) Something that you have recently or thought about “burning your cash” on for time savings or an improvement in quality of life.

I’ve made the decision to forgo making money on Fridays – Fridays are Daddy day for me to spend with my one and half year old son. I give up a lot of income but it is great for the soul to spend a whole day with just me and my son.

7) Something that you changed your mind on? Our ego often gets in the way of greatness.

I changed my mind about real estate – I used to treat it as a completely passive investment – I now think of it as a business and this mindset has opened up new possibilities and has opened up some fruitful relationships with property managers, contractors, etc.

8) In this sellers market… what are you investing in? What should a someone who does not have a substantial level of cashflow yet be investing in?

Value-add (also known as BRRRR’s) single family and multi-family properties. Less competition and opportunity to force appreciation and preserve capital.

Someone with little cash flow should buy a house hack – buy a multi family property, live in one of the units and rent the others out.

8) Tony Robbins identifies two large concepts that we are continually struggling to gain perfection at: #1-Art of Fulfillment and #2-Science of Achievement. If you died tomorrow and I were to email this to your kids a couple decades later… this is what they would hear.

What is your secret/hack for the “Science of Achievement?” Any secret habits to share? Morning or Nighttime ritual?

I talked about the morning routine that I try to do. I would say be strategic in everything you do and constantly be running if/then scenarios. Have backup plans for everything. Be constantly prepared to react to things beyond your control. For example what if rents drop 20%? What if we have another Great Recession? What if I have a health problem and can’t work?

What is your secret/hack for the “Art of Fulfillment?” How you do contribute back?

I would say just to act with integrity and honesty in everything you do. People like dealing with people they like…it’s pretty simple. Treat people with respect both in business and your personal life.

9) Anything we missed and contact info if you would like anyone to get a hold of you. URL?

My website iswww.realliferentals.com and I use it to track my monthly portfolio performance. I can be reached through the contact page on my website.

Notes from a lawyer learning to see beyond the maze

Imbued with the dream of becoming a lawyer — upholding the law, arguing in front of a judge and jury, defending the underserved or mastering the art of the deal — you head to law school and never look back. Three years and over $150,000 in student loans later, you graduate, eager to apply your newly minted legal mind. You pass the bar and proudly step into your new job at a law firm, corporate legal department, or government office. But unbeknownst to you, despite your juris doctorate degree and “Esq.” title, you’ve just entered the same rat race as the majority of the U.S. workforce.

I know all this because I’ve been there. After graduating from law school, I was lucky enough to find a job at a “biglaw” firm where I practiced corporate law in the mergers and acquisitions field. That meant many 80+ hour weeks representing companies and private equity firms in the fast-paced, high pressure world of buying and selling companies. My colleagues in litigation practices were subject to less ups and downs, but were still regularly cranking out 60+ hour weeks under intense deadlines and filings. We all got there by employing the same mentality we used all through our lives — work hard, perform well to achieve the goal at hand and collect applicable accolades. What I realized when I got to the “top” of the legal profession, however, was that the view wasn’t so pretty.

The Golden Ticket?

Landing a job at a top ranked biglaw firm, at first, appears to be a golden ticket to higher compensation, benefits, opportunities and ultimately, a better life. Biglaw firms were seen as the most “prestigious” in the legal world for handling the most complex work and servicing even more illustrious clients – big pharma, tech giants and oil companies. The associates and partners are paid top dollar in return for their expertise, ability and availability. For instance, right out of law school in 2018, a first year biglaw associate is paid $190,000 as base salary and is eligible for a $15,000 annual bonus. For the next eight years, the base salary and annual bonus at most biglaw firms increases in a lock-step fashion according to the market-setting Cravath pay scale. Beyond the compensation, top-ranked law firms boast taglines of “unparalleled legal training” and the opportunity to “work with like-minded intellectuals” and “sophisticated clients” on “diverse and challenging matters.” For these reasons, even after a long hard week where you may be subjected to extreme stress, no sleep and eighty billable hours (not counting the ten non-billable hours of face time at the office), you are supposed to put your head down, keep going and receive that big fat paycheck every other week. After all, it’s worth it, right?

Why We Do What We Do

A handful of lawyers enjoy the practice of biglaw and its intellectual rigor — the litigator’s ability to creatively craft a brief to sway the court’s decision (or checkmate the opposing side into settlement) or the dealmaker’s negotiating savvy that secures the client’s acquisition of a promising portfolio company. These select few are the ones willing to grind it out for years into a lucrative partnership with the firm.

But the vast majority of biglaw attorneys are young professionals who admit they are not particularly interested in partnership and are only looking to gain some experience and training to parlay into an in-house position in a company’s legal department or a smaller firm, where they will take a substantial paycut in return for a more balanced lifestyle.

Nearly all biglaw attorneys share one thing in common: a $150,000 plus student loan burden that makes a high-paying six figure job that much more appetizing. Lawyers are known for their risk aversion, and many think that this debt is a risk in the sense of impairing their ability to dump their earnings into savings and their 401k. As a result, it was common for colleagues to talk about surviving in the trenches of biglaw long enough to eliminate their student debt.

Finally, there is the phenomenon of the golden handcuffs. Law firm associates get used to the high income and adjust their lifestyles accordingly. As a result, they believe themselves to be stuck in their jobs. Of course, they don’t realize along the way how much money they are wasting to make themselves “happy” — buying the nice watches, a few bottles of wine each week to unwind at a fancy dinner, the new car — and that they are holding the keys to the handcuffs that keep them at their job and lavish lifestyles.

At What Cost?

Time = Money

Being a lawyer at a firm is the epitome of trading time for money. Your working life (and therefore the majority of your life) become ruled by the billable hour, and you start to see your life measured in .25 hour increments. Associates are expected to meet certain billable hours (i.e., hours actually billed on client matters) in order to be eligible to receive the annual bonus. With the billable hour as a metric, your value as an attorney is measured by how productive you are and how efficiently and precisely you can churn out work product per hour. These billable hours are the firm’s source of revenue, and it is not uncommon to have a billable hour requirement of 2,000 hours per year. 2,000 hours equates to a roughly 40 hour workweek. Not bad right? But that does not include lunch, bathroom and water breaks, and any minute away from your desk chatting with a friend or asking your secretary to file away old matters. It was not uncommon to work a 9 a.m. to 8 p.m. work day only to see my billable time for the day clocked in at a measly 7 hours. Sometimes, there was not even enough work to support that, and during these slow times, it was not uncommon to bill 4 hours or less even though I was in the office the entire day. Finally, not having steady work flow meant oftentimes getting reacquainted with matters that you had not seen for 3 weeks or so, and feeling pressured into writing off the first hour you spend getting your bearings so as to not look slow or inefficient. This “billing” pressure — having partners pressure you into billing more hours to pad their pockets, but also to be conscious about keeping the client’s bill down to create the image of efficiency — takes a toll on associates and even partners. Even at the most elite firms, the most senior partners who have worked 60-80 hour weeks for over 20 years earn at most in the low seven figures. Unless you are the plaintiff attorney taking down big tobacco or pharma, there is no such thing as “the sky is the limit” in the legal profession.

Serving Two Masters

Associates working at a law firm really have two clients: the partners they are working for and the clients who the firm is working for. Both partners and clients expect that associates be available at all hours of the day, 24/7. For instance, a client could email regarding an emergency before the break of dawn, but the associate is still expected to give a timely response (within the hour). Similarly, a partner could give an associate an assignment before he heads home for the day and expect to see the work product before the next morning. There are no boundaries on when partners and clients can expect an associate to work. It is even more frustrating when you realize that the client bossing you and your partner around is a 25 year-old who stepped into his current gig after working at an investment bank for two years after undergrad. He’s the one who dictates your weekend plans by needing an update on the deal memo and other docs “immediately” so he can let his own boss know that his trip to Vegas won’t be a disruption since the lawyers will still be turning drafts all weekend.

A Thankless Profession

Starting out as a young associate, one expects to be inundated with the trivial tasks, such as due diligence of companies’ customer contracts in a buy-side deal or doc review to find the smoking gun. One would think that the more senior an associate becomes in a law firm, the more control they would have over their schedule, perhaps by delegating work to younger associates. However, it’s the opposite. The more senior an associate, the more responsibilities he or she will have and oftentimes, it is too complex of a matter to delegate to younger associate. Partners’ responsibilities and commitments between doing the work for multiple important clients to business development (which does not count toward their own billable hour requirements) have it even worse and are often working earlier in the morning and late into the night.

One particular memory I have from my time working in biglaw was a conversation I had with a partner on the eve of a transaction’s closing. It was about 3 a.m. Friday morning at the end of a week of late nights, and we were leaving to get a couple hours of sleep before an 8 a.m. closing call. He said, “You know how we lawyers all think we are the smartest people in the room? How when a business guy says something way off, we roll our eyes and figure we’ll have to get it right in the contract and negotiation? Well, we’re actually the stupid ones. We’re in the wrong profession. That business guy went to bed early fully expecting that we’ll get this thing done. He’s getting paid big tomorrow morning and may not ever have to work again. And we’re here until 3 in the morning and all we’ll get is a thank you and a bottle of wine at best. But if we mess it up, we’re gonna have a lot to lose. And this is only one of the 3 deals I have closing tomorrow.” That conversation stuck with me. Granted, he’ll get a share of the legal bill for the deal, but here was this well-respected, well-paid partner in his late 40s admitting to me that he made a career and lifestyle mistake. He was out of shape and always looked stressed out. The worst part was that he was sticking to this career with no end in sight because his attitude was that he made his bed and he just has to lay in it. I knew definitively that I never wanted to be like him, at the peak of my career, telling a younger colleague that someone else out there was living the dream while I was toiling away, trading my time for money.

Life on the Run

Because associates are expected to be available 24/7 and to meet the billable hour requirements as mentioned above, it is nearly impossible to find work/life balance. It was normal for associates to be working in their office late into the night everyday and on weekends and holidays. I used to joke with colleagues that “of course I’ll be in on Monday, it’s Labor Day after all!” Clients like to take their holidays, which meant that you would often be stuck with something as they head out the door.

Your exercise and eating habits also fall by the wayside. And even when I was able to drag myself to the gym on mornings with only 6 hours of sleep, there was always the stress. Some of my friends refused to wake up early for the gym because that meant another hour of consciousness where you could be subject to an email that would ruin your day. Biglaw is notorious for being able to take a normal working day from a 2 out of 10 stress level to a 10 out of 10 client emergency, and you never know when the next fire will need to be put out. I’ve counted more than five of my own personal biglaw acquaintances who fell prey to stress manifesting in the form of severe illness.

Countless birthdays, Thanksgivings and family get-togethers were either missed or spent in the other room cursing under my breath as I tried to turn a document before an artificial deadline. I would make weekend plans while at dinner on a Friday night, only to get an email or phone call later that evening letting me know I had to be in the office all weekend. Breaking plans with loved ones and friends was one of the most soul-crushing feelings about legal practice, as you knew that you were directly affecting their lives, not just your own. Ensuing stints of depression were not uncommon. And you know it doesn’t get better when the partners and more senior associates are in on weekends earlier than you and there well into the night. Sometimes my fellow associates and I joke that maybe these partners secretly hate their families, because they’re always at the office. But sadly, the truth is that they have convinced themselves that this is the only way to make a living, and therefore trapped themselves for good.

The lack of your ability to have a social life, take control of your health or maintain your relationships gives the biglaw attorney the sense of playing Russian roulette, but instead of a “bang,” you dread the “ding” of your email on a Friday night. There was always the sense of looking over your shoulder, because sooner or later, biglaw was going to get you.

Learning to Love the Law After Drinking the Kool-Aid

I knew pretty quickly that I could never sacrifice my family life to the needs of my clients to such an extreme, and so I began to look around for a way out of biglaw and the life of a lawyer in general. On my long commutes to work, I stumbled on investing podcasts, and then real estate specific podcasts (even this light hearted on with this dude and his ukulele), and although I did not have a way out mapped yet, the one catalyst on interviews that everyone mentioned was, of course, Rich Dad Poor Dad by Robert Kiyosaki. Once I read that and his Cash Flow Quadrant, I knew that the universe was telling me that there had to be another way to live a meaningful life, and that it was passive income and cash flow investing.

Of course, it was nearly impossible to take action, since biglaw was an all-encompassing job. So I tried to learn what I could about the world of passive real estate investing so that when the time came where I had enough control over my life to start investing, I could be ready to pounce.

After listening to hundreds of podcast episodes and reading dozens of books on the subject, it became clear that to escape the rat race, leverage was an important factor. Not just in the sense of using debt to acquire cash flowing properties, but leveraging your time and your talents. So that begged the question: how can a lawyer’s skills and resources be parlayed into real estate investing?

Lawyers generally have higher incomes due to their advanced degrees. As mentioned earlier, biglaw associates straight out of law school make nearly $200,000. Outside of biglaw, even government lawyers can make six figures. This means quick accumulation of investment capital through earned income (W-2 wages). With the right knowledge on controlling finances, a lawyer can save well into five-figure portions of their salary per year, which can allow for the rapid growth of a cash-flowing asset portfolio. In addition, a lawyer’s personal network will invariably include many similarly situated legal professionals with disposable income for investing, which may prove useful for raising capital and attracting other investors to deals.

The skillset of a lawyer is also applicable to passive real estate investing. Lawyers have very strong reading comprehension, writing, research and negotiating skills. Real estate property analysis can be learned, but the ability to spot issues and inconsistencies and to tackle complexities is what lawyers are trained for, and this will inevitably come in handy when dealing with agreements involving your real estate investing (including term sheets, purchase and sale agreements and private placement memorandums). Due diligence is a familiar term of art for transactional attorneys, and similar principles apply in the real estate purchase context. Furthermore, managing more junior attorneys or specialists (especially in an M&A deal) is useful experience when applied to overseeing your own investment team of property managers, agents and other advisors.

Finally, a lawyer’s title carries a sense of professionalism and respect that translates well in the investing world. When I was a biglaw associate, sophisticated clients with 20 years of experience in investing often called me to ask me to explain a complex vesting mechanism or to handle the entire due diligence process in their purchase of a hundred million dollar company. Being a lawyer may bring some negative associations due to popular culture and general experience, such as being conniving, risk averse or not business minded, but by branding yourself as a business savvy and commercially-minded attorney trusted with great responsibilities in your W-2 job, you can stand apart with your less common background and skill set.

Planning the Escape

As a lawyer at a biglaw firm, I had little control over my life and free time. Eventually, after years of going through the grind, I was fortunate enough to land an in-house position, where I am generally on a 9 a.m. to 6 p.m. schedule. This was a crucial step that allowed me to devote more time and resources to passive real estate investing.

In order to get started on escaping the maze of a W-2 legal job and the rat race, an action plan is needed. Most important is an investment in one’s financial education. Start with Rich Dad Poor Dad and Cash Flow Quadrant to drink the koolaid (or SPC Latte) and indoctrinate yourself into the paradigm of being financially free and having real wealth. Listen to podcasts such as the Simple Passive Cashflow podcast, and read books on real estate investing.

Then, after a few books and podcasts to get yourself comfortable, it is time to take action. Do not get caught up in looking for the next shiny object that will be the magic pill to get out of the matrix. Financial independence and escaping the rat race takes time, and you should not be distracted by what others have done to amass total wealth if their situation is much different from yours. When observing the stories of other W-2 income earners and how they have mapped out their escape, one thing became clear: the investing must be passive, and intentional efforts and actions have to be made towards pursuing even those passive investments. Not to say that quitting your legal job now and diving into real estate or other investments cannot be done, but just realize what it is you’re trying to achieve. If it is financial independence and escaping your rat race job, then focus on attaining passive income that will cover your expenses, and then replace your salary. If you’re looking to get out of the law by jumping into flipping or wholesaling real estate, just realize that you’re just doing a career switch into another active endeavor and that you are not achieving financial independence in that way until you have a passive income stream from your investments.

Like Plato in the Myth of the Cave or Neo in the Matrix, the paradigm shift is the most important first step in seeing the truth. Without it, we are just highly educated esquires blindly fumbling through the corporate ladder or firm hierarchy until we reach 59 ½ years to collect our 401(k) payments. I am lucky enough to have gotten through the first level of the maze of the legal profession that is biglaw, where time is traded for dollars. I am now on my way in the second level, where the only way out is the accumulation of passive income. Many tell me that once I free myself of the day job or the need to collect a paycheck I will begin to ponder what else to do with my time and find difficulty to find fulfillment after. Well, I welcome that first world problem 😉

If you’d like to learn more about how to escape, start here on the Journey to Simple Passive Cash Flow.

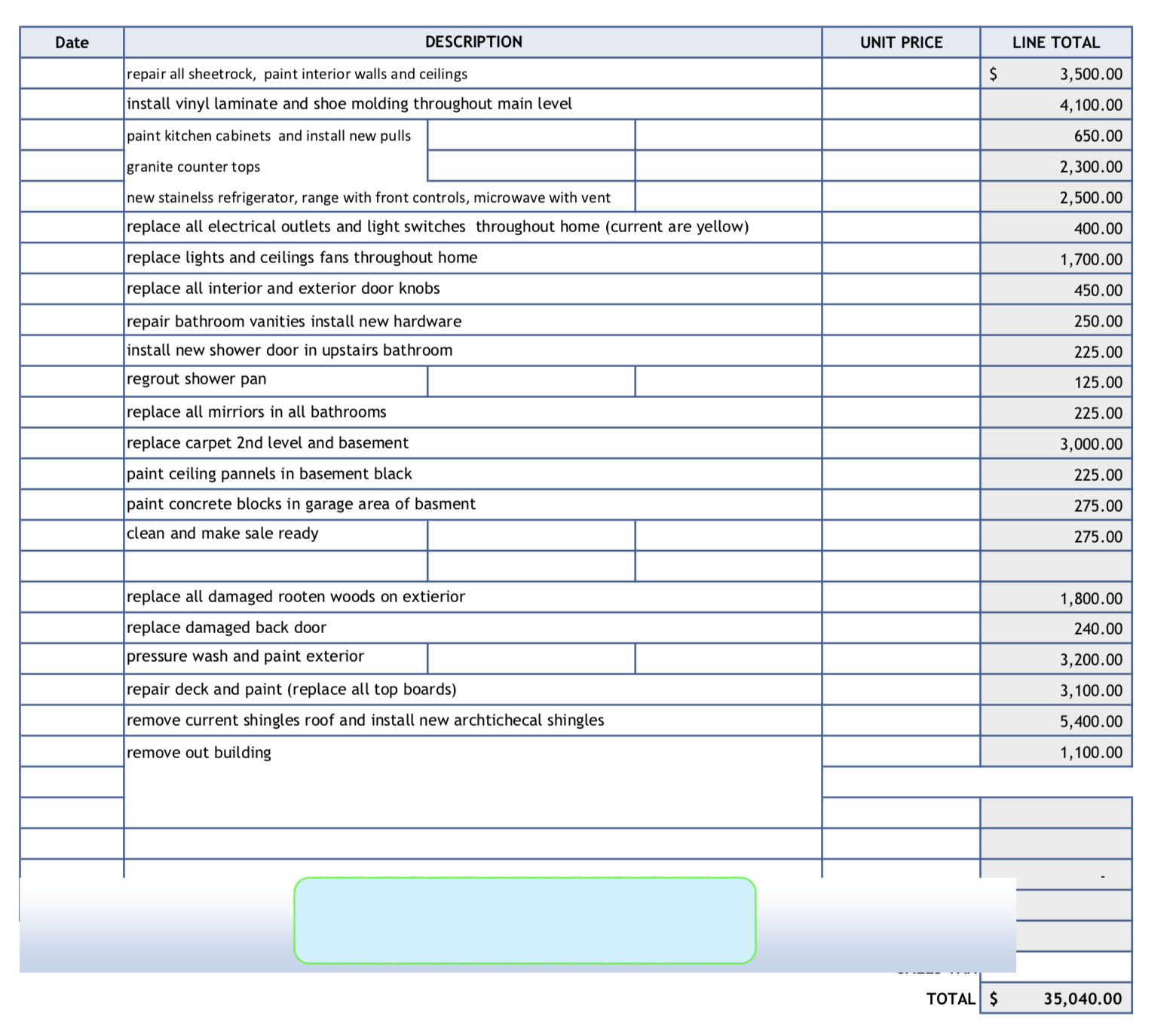

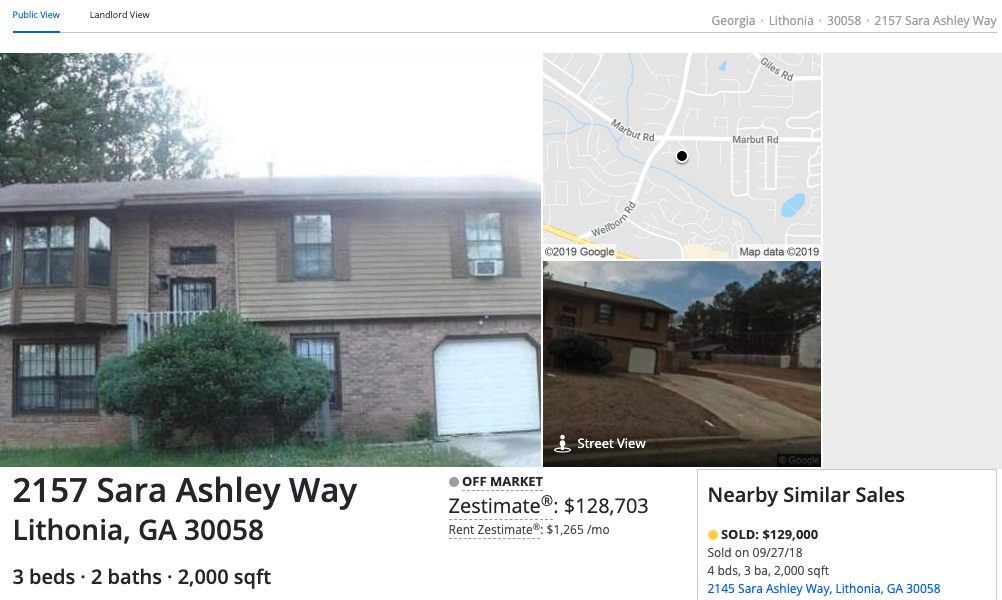

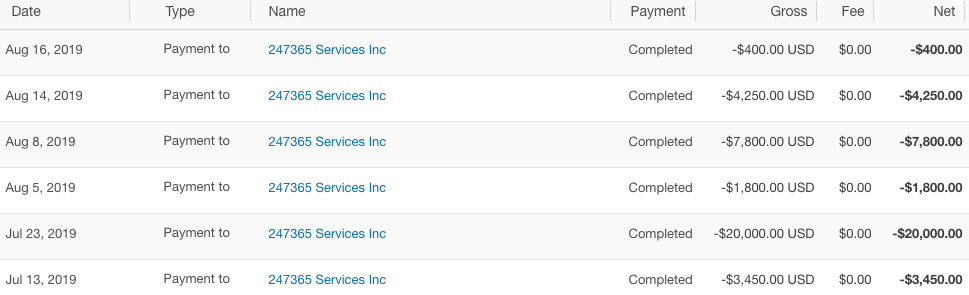

I purchased this property back in 2015 as turnkey rental.It was a B class rental in B- location and rented for about $850 a month.

It was a very stable property for a few years but in 2019 we had to evict the tenant who left this.

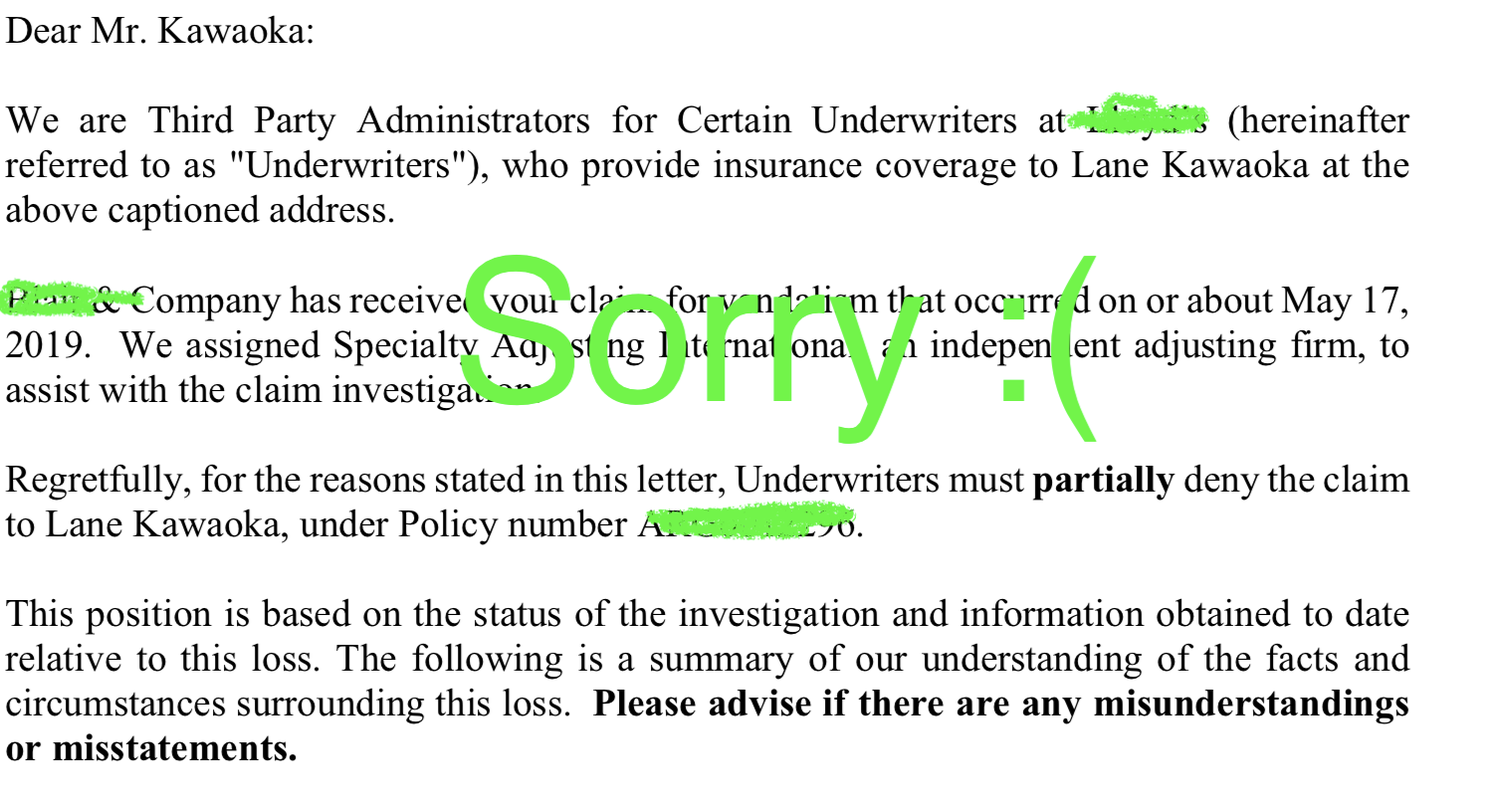

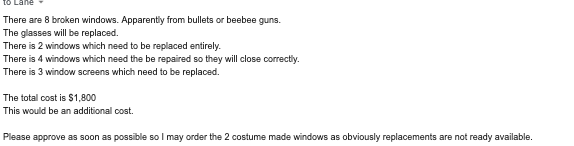

When I tried to put in a claim in the insurance company a couple months to get back to me with a really lame “sorry but we can’t help you” letter. Apparently vandalism is not covered. I even got the aid of our commercial insurance adjuster that I helped us with a $400,000 fire damage claim on our 114-Unit Apartment complex in Atlanta. His response is that SFH policies just are not as robust as commercial policies.

Another reason I am leaving the PITA behind and going to more scaleable syndications.

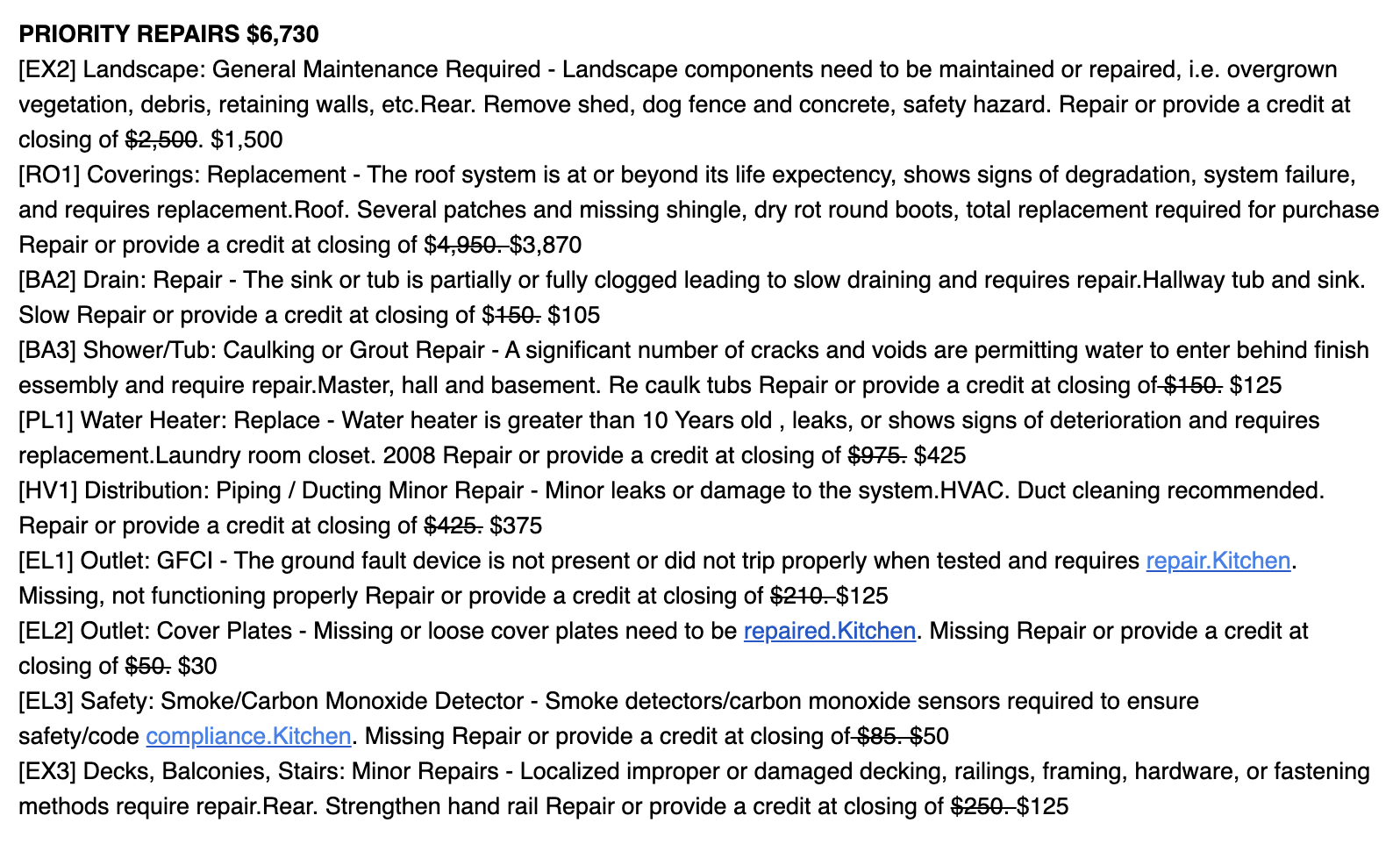

Scope of Work

$3,450 -Interior and exterior clean up. Overgrown lawn and bushes. Pressure wash exterior. Exclude 55 gallon oil drums- 19.07.13

The buyer sort of played me a bit as a tad-desperate seller. I wanted to get out of the deal and move to just better deals with less of the aforementioned BS. This is called “re-trading” where the buy goes under-contract with all cash offer but then starts to make demands for repairs. I know its all part of “the game” but this is again why I don’t like messing around with SFH people since they like to waste their time. It reminds me when I was at my W2 job and had to sit through stupid meetings where other people were just trying to create more work.

Onward and Upward

Now I can take this money and go into one or two syndications!

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}