Erin Lowry (https://brokemillennial.com/) is the author of Broke Millenial, a book about how to stop scraping by and start getting your financial life in order.

She talks about how she learned about finances at a young age, how she gave up her dream school so she could live her dream life, and how living in New York inspired her to write her book, Broke Millenial.

“Invest your spare change,” may be a catchy line but you really can’t invest your spare change to wealth. It has to be more than spare change.

In the financial world, you are above nothing. Just because you have a college education doesn’t mean that is your way out of financial difficulty. You also need to be prepared to take non-professional jobs or jobs that might be below you.

Just like in any financial goal you have to figure out how to take a high-level idea and break it down into smaller parts. Think of whatever your long-term financial goals are and work backwards to break it down into something that is actually more achievable. A lot of people in their early twenties have beautiful, lofty dreams but no tangible steps on how to get themselves there.

Podcasts are great sources of information.

Saving is important but earning more is bigger. To earn more is a key part of building wealth.

The biggest thing when it comes to feeling in control of your money is that you have to identify what you truly value. Don’t allow other people to dictate where you should spend your money.

As a real estate investor, imagine using Cost Segregation as a real property investment strategy that will grant you tax free cash flow from fixed assets and allow you reinvest even more (and possible lower your ordinary income).

What is Cost Segregation?

This is one of the easiest and fastest ways to squeeze a little extra profit out of an investment. If you have ever played those racing video games where you modify your car (like Gran Turismo) it’s like paying for that cheap computer chip upgrade to get an extra horse-power boost, it’s a no-brainer.

For those of you who aren’t ex-gaming nerds like me, it’s “low-hanging fruit”.

A cost segregation study gives a tax benefit to the taxpayer to take advantage of current bonus depreciation laws (starting to phase out slowly in 2022) in order to depreciate their assets by taking a loss on paper.

The cost segregation specialist/engineer analyzes the components of a commercial real estate asset to create a cost segregation report to equip the tax accountant or CPA the needed breakdown of the asset in order to make the depreciation determinations.

To better understand the benefits of performing cost segregation, you must first understand depreciation.

Depreciation is where you reduce the value of your assets (in this case, your real estate properties) due to natural wear and tear over time. There is a type of depreciation wherein the value of your fixed asset (real estate properties) depreciates faster than it should be. This speedier depreciation or most commonly known as accelerated depreciation.

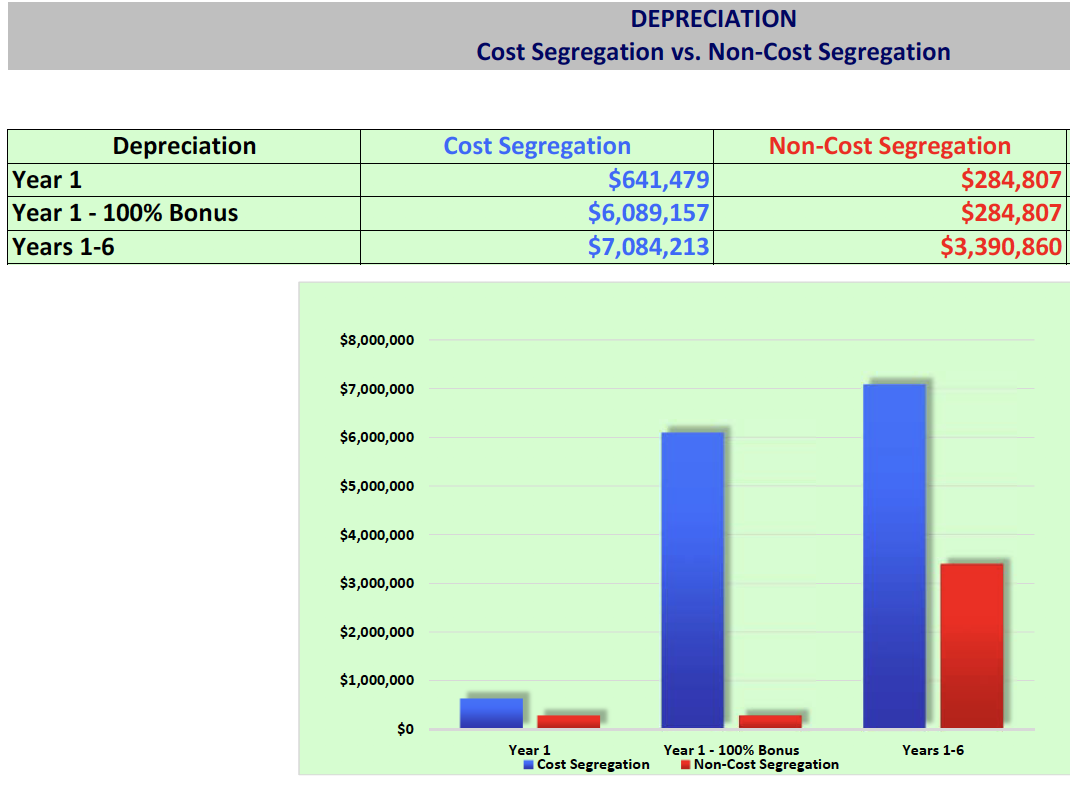

Let’s look at it in detail: If you own commercial or residential real estate investments, you can depreciate your real estate holdings. A commercial property establishes a 39-year depreciation schedule and a residential property establishes a 27.5-year depreciation schedule. These are the numbers we will use to calculate the rate of our depreciation deduction.

Above link is for smaller assets. Larger assets will likely require other vendors that we use on our assets. Join the club for access.

Real K1 from a past dealReal K1 from a past dealReal K1 from a past deal

Above: Example of a cost segregation estimate for a past deal

Below: Another estimation of regular depreciation vs the more aggressive deprecation timeline (what is coined as “bonus depreciation”)

Envision a 3 bedroom single-family home in Birmingham, Alabama that is worth $100,000. Of that, approximately $65,000 is determined to be the building value and $35,000 is determined to be the land value. Each year you can deduct 1/27.5th of the building value, which is about $2,363 a year that can offset income gains. $2,363 can be taken for the next 27.5 years until all the value on paper is depleted.

Is there a catch?

Unfortunately, you cannot deduct the value of the land unless you have made a land improvement, granting that the improvement you made has a “useful life” that is depreciable. Only the improvement will be depreciable, not the land itself.

https://youtu.be/tlI83umq-DE

When you sell the asset you will need to recapture the depreciation. This is the major disadvantage to a cost segregation.

We pay $8000-12,000 on our larger commercial assets to do a cost segregation and our advisors tell us that the general rule is to do a cost segregation if we intend to hold onto a property more than 3-5 years because if we sold quicker than the time benefit to the passive losses we got as investors you be less and might not be worth the price of the actually cost segregation study.

But, guess what?

There are some exciting new benefits to passive losses since Mr. Trump enacted a tax law where 100% Bonus Depreciation creates substantial benefits on your taxes for the acquisition year. In the future, us investors are crossing our fingers that this part of the tax code sticks around.

Paper losses from single family homes

Previous

Next

Think about this: My $3M, 52-unit apartment, is looking to get more than $266K in tax savings (at 37% tax rate) in the first year of ownership by doing a cost segregation.

If you are interested in learning more about how to best utilize your passive losses, you can learn more here.

Companies and investors who have constructed, purchased, expanded, or remodeled any kind of commercial real estate (including 1 to 4-unit residential rental properties) since 1987 can use cost segregation studies for maximize their tax savings.

The study allows the owner to take advantage of accelerated depreciation deductions and defer federal and state income taxes on the reclassified building components mentioned above.

A team of real estate investors evaluates several personal properties, residential rental property, and land improvements that can be upgraded to improve the value of the property. Those improvements are assessed with the assistance of a Cost Segregation specialist. After completing this cost segregation analysis, the property owner may deduct the depreciable life of the individual fractional interest (IFI) through a cost segregation study, with or without depreciation. If the taxpayer is eligible and has not failed to take advantage of the tax rebate, the taxpayer may claim the expense directly within the given year of the seller’s ownership.

To elaborate more on Accelerate Depreciation Deductions, it is a deduction of the cost you pay to a person if you own your personal property assets. The accelerated depreciation deduction provides significant tax savings but it is not another type of benefit. The exchange of property owners whose benefit is primarily from cost segregation is a limitation in tax savings. The depreciation expense is deducted at the source rate in another year.

What are the Benefits of Cost Segregation?

Lower Property Insurance Premiums

Since it generally costs less to insure personal property, versus real property, building components reallocated as personal property should reduce your insurance costs as well which will yield potential benefits in the end.

Capture Retroactive Savings

Since 1996, taxpayers could capture immediate retroactive savings on properties added since 1987. Previous rules, which provided a four-year catch-up period for retroactive savings, have been amended to allow taxpayers to take the entire amount of the adjustment in the year the Cost Segregation is completed.

This alone is huge!

This opportunity to recapture unrecognized depreciation in one year presents an opportunity to perform retroactive Cost Segregation analyses on older properties to increase cash flow in the current year.

What Components Can I Reclassify?

Components of a specific property or qualified leasehold improvement are identified and reclassified for depreciation over a shorter time (5, 7, or 15 years). For example, 30% to 90% of the total electrical costs in most buildings can qualify for 5 or 7-year depreciation.

5- year tax-life components

Non-structural elements: carpet, decorative lighting and trim, HVAC systems, dedicated electrical and plumbing, and security systems.

7-year tax-life components

All telecommunication related systems: cabling, telephone, etc.

15-year tax-life components

Exterior land improvements: landscaping, curbs, sidewalks, fencing, and signage.

As a Passive LP investor the details of this is not needed as all you need to ensure is that your sponsor is aware of cost segregations to optimize tax benefits.

What is required to have a study done?

You need to provide as much of the original documentation pertaining to planning, construction, and current tax depreciation as you can.

This could include a complete set of:

Construction plans

Current tax depreciation records such as tax returns, building cost budget information, final AIA (American Institute of Architects) appreciation

Document of certification of payment or other cost information, change orders, direct or indirect costs paid by the owner that are not included in other documents

Other information depending on the project

How much does a Cost Segregation Study cost?

On average, the total fee will generally fall between 5% and 20% of the estimated net present value tax saving. You can often get a free preliminary analysis to help determine this. This can be impacted by how large or small the real estate project is.

In addition, the location, accessibility, and quality of the records and documents will impact the entire cost (costs typically range between $8,000-$12,000). Minimum fees can be as low as $2,000 for small projects, and some firms GUARANTEE a minimum of 500% ROI (fee vs. tax recovery) on projects over $500,000.

Cost segregation studies are typically cost-effective for larger syndication buildings purchased or remodeled at a cost greater than $100,000. Acost segregation study ismost efficient for new buildings under construction, but it can also uncover a retroactive tax deduction for much older buildings as well.

What are the steps involved in the process?

First off… if you are a Passive Investor (LP), your sponsor should be taking care of cost segregation for you so you will have one less thing to worry about.

If not, the cost segregation process can be broken down into the following steps from start to finish:

Step 1

Vet Cost Segregation Firm

Engage a reputable Cost Segregation firm that utilizes engineers and architects trained in Cost Segregation and it’s application to the proper allocation of assets. If you need a referral go here.

Step 2

Document Review

The engineer determines what documents are available (e.g. planning, construction, invoices, appraisal, and current tax depreciation) for reference and referral.

Step 3

Schedule Property Survey

The engineer then sets a schedule for surveying the subject property and gathering the available documents for review prior to arrival at the subject property.

Step 4

Document Recreation

For those documents that are unavailable, time is then scheduled into the Cost Segregation process for document recreation using known industry standard costing data (Marshall & Swift and/or RS Means costing publications). The process takes about 4 to 6 weeks after all necessary documents are acquired. The time that a Cost Segregation Study takes depends on the size of the project and the completeness of the documentation that you can supply.

Step 5

Conduct Site Survey

The site survey is executed and completed. Surveys can be completed within as little as an hour, but it varies between each survey. Measurements are taken and all areas are photographed for IRS verification and substantiation of asset values during the survey.

Step 6

Calculations

The engineer returns to the office and crunches the numbers. The number crunching process is when all documents are reviewed in detail, assets are verified, and measured against known costing data, and asset reallocation is applied.

Step 7

Review

A review committee then examines the results of the analysis completed by the engineer of record to verify its veracity and confirms it meets and exceeds IRS guidelines per the Cost Segregation Audit Techniques Guide.

Step 8

Compile Report

Once approved, the study results are compiled into a final report that includes: all IRS tax code to substantiate the reallocated assets, spreadsheets identifying all assets categorized according to their building codes, representative photographs of the reallocated assets, and the engineer’s credentials for IRS review.

Step 9

Issue Report

The final report is issued. The client and CPA of record receives digital copies via email, for application to the client’s tax return.

When Should Cost Segregation Be NOT Considered?

There’s an attempt to sell within within 5 years

Not being able to use the losses- planning 5 years ahead and looking back 5 years for taxes; income isn’t enough or PAL restricted.

No savings of at least 2X cost of study (not depreciation but the existing cash savings)

Be wary of 1031 exchanges- there are 2 ways to calculate the depreciation to carryover

5. Check that the federal 1031 doesn’t open you up to exuberant state taxation on the state 1031. Note: Many states do not follow federal guidelines for depreciation and personal property ineligibility.

6. Discern if 179 expensing method is a better option (due to presence of limitations)

7. Possess your real estate in S Corps due to many reasons: basis and step-up

Cost Segregation Example #1

Depreciation is distributed to investors on the K-1 Form in syndications.

Not making any promises as depreciation amount is primarily based off building specifics and the amount of leverage used in a deal, but here is a real-life example from a $50K LP investment in a Class C apartment syndication in the first year K-1 in 2018 which yielded a $36K paper loss by utilizing a cost segregation. Extract 10-20x what you normally able to deduct in the first year alone! Take these passive losses and employ the “Simple Passive Cashflow Gravy Train” strategy where you offset your ordinary/W2 income with real estate professional status. For more details on that check out our Master Tax Guide.

I paid 4% in taxes in 2018. All because of the passive losses that real estate gave me.

Previous

Next

If this is a new concept to you, you may be able to go back to previous years taxes and get back some benefits this year. Oftentimes, getting a quote is free and quick.

A recent quote I got back for a few properties:

Previous

Next

Cost Segregation Example #2

We purchased a $20M apartment and are about to write off $6M in the first year! The total capital raised from investors was $5.5M, that meant almost a dollar for dollar deduction in year one!

Cost segregations are not new. On the contrary, they have been in existence since 1954, when the IRS allowed for certain personal assets to be accelerated into a shorter life class. However, it wasn’t until Hospital Corporation of America sued the IRS in 1997, and won, that the IRS revisited the issue of accelerated depreciation. The IRS ruled that property qualifying as tangible personal property under the former Investment Tax Credit (ITC) rules, would also qualify for purposes of federal income tax depreciation under MACRS (Modified Accelerated Cost Recovery System).

The IRS Chief Attorney wrote a memo saying, “. . . Cost Segregation, for it to be properly applied, had to involve those with competencies in architecture, engineering, or construction and/or construction techniques, in order for personal property assets to be accurately identified and segregated.” As a result of this memo, cost segregation became a viable tax-saving strategy allowed by the IRS.

CPAs are not qualified according to the IRS guidelines. However, most Cost Segregation firms will gladly work with them on a consulting basis to complete the work for you. Remember, the IRS Chief Counsel issued a memo that made it clear what constitutes proper “methodology” in applying Cost Segregation, and it must be done by people who are competent in architecture, engineering or construction and/or construction techniques. You will want to ensure you are working with a cost segregation specialist to follow correct protocols. See ” Is Cost Segregation something new? ” above.

As investors, we like paper depreciation to occur earlier because that offsets gains earlier and gets more money in our pocket earlier. Just like how you give a mouse a cookie…. Give an investor a dollar early and… they will turn em’ and burn em’.

In other words, you are not creating more depreciation, you are shifting it earlier to take advantage of the time value of money concept.

On the project-level in a single asset LLC arrangement, the more you can lower your tax liability, the more you can significantly increase your passive income and create more value for investors.

A cost segregation study, in effect, gives you an interest-free loan from the government for the first 15 years, which you will then repay interest-free over the remaining 25 years. Wouldn’t you rather have your money now? There are also advantages in doing a study if the building is going to be sold (via 1031 exchange) or if the owner of the building dies.

Most cost segregation firms will perform a free analysis if you provide your basic property information and tax rate. From the information you provide, they can calculate a conservative estimate of the accelerated benefits you can expect, as well as their fixed fee proposed for the final study.

Typically, tax savings from 5% to 10% of the building’s original tax-basis are generated, but there are instances where it can be substantially more. Each property and circumstance is unique, so it requires a case-by-case approach to give you a definitive answer.

Certain types of commercial properties can be grouped together to give us an idea of the percentage of those types of buildings eligible for accelerated depreciation. Your results may be greater, or less than those quoted here, but in general, property that falls into one of the following categories is most likely to result in accelerated depreciation within the specified ranges.

A study conducted by a reputable Cost Segregation firm should strictly adhere to the IRS Cost Segregation Audit Techniques Guide . The type of study most firms perform places you in Internal Revenue Code Tax Compliance, which actually decrease your chances of an audit. However, you should be aware there are six different Cost Segregation methods allowed by the IRS, and not all are of equal merit. There is currently no standard method, and there is still some ambiguity about which method is best. If you have heard conflicting information about what is, and is not possible regarding Cost Segregation, it really depends on which method is being used.

A reputable Cost Segregation firm can assist you in the event of an audit. They will focus on doing the Cost Segregation Study to create documentation and support for conclusions so that these are easily communicated and resolved with the IRS. In fact, you should expect a final report that is “all inclusive”. The report should quote specific Internal Revenue Codes related to the reallocated assets. Additionally, it should provide photographic evidence of these same assets for complete substantiation of the assessment. A properly documented Cost Segregation Study helps resolve IRS inquiries at the earliest stages.

A cost segregation study can still be performed even if you lack some of the necessary documentation. Construction, engineering, and other specialists will do an extensive site visit. They will measure and estimate using currently accepted costing techniques and pricing guides (such as the IRS-recommended costing publications Marshall & Swift and RS Means ) to determine the costs that qualify for shorter recovery life periods.

A pretty impressive event. Its where 2000 financial bloggers, you-tubers, and podcasts this year gathered around all this money.

In 2006, I started reading financial blogs. Sole of my favorite was getrichslowly, Wallet Hacks, and of course mr money mustache. FinCon started in 2011 with just a couple hundred people.

Real estate investing is a minority. 95% of people are debt adverse and about the 4% rule. Buying cash so so debt. Living small is selfish? Make 150k a year and retire when you are 35…

The Millionaire Next Door book is not the type of lifestyle I would like to live.

I am cool with how it is enough to be happy and content.

Other Findings:

New investment account that incorporates mobile interfaces and suto-AI. Mint app has click to invest and banking apps have click to refi. It’s a little dangerous.

A cool 5% instant liquidity online savings bank that invests in inventory loans. Let me know and I can connect you with that as I try to do more due diligence on my own.

Liberty health share – religious-based health insurance

Side gigs – consistent theme from high performing growth mindset W2 employees who are not getting fulfillment at their bureaucratic day jobs.

Interviews to follow in video…

Please share this with friends because if you don’t soon you won’t have any friends to have mid-day lunch with when you not doing anything

Article Link: Text “simple” to 314-665-1767 to download the Hui Google Drive files and the 2018 Rental Property Analyzer

For a free electronic version of my bestselling book in 12+ categories text the word “ebook” to 587-317-6099.

Please help the show by leaving a review: http://getpodcast.reviews/id/1118795347

Join the Hui Deal Pipeline Club! SimplePassiveCashflow.com/club

Pardon the grammar – I’m an Engeneer, Enginere, Engenere… I’m good with math!

________Here are the Show Notes________

I worked with Matt’s team way back when in 2014 buying turnkeys. Simplepassivecashflow.com/turnkey Since then it is interesting as times change how his strategy has changed.

We just completed the last deal for an Mobile home park. Which is a little different than apartments.

Please leave an iTunes review – Help fight negative one-star review

Earning $30,000/mo through single-family homes and seller-financed notes.

Epic Real Estate started selling turnkey properties in 2009.

Built successful portfolio, but returns lowering. However, real estate always a good purchase to buy and hold long-term.

Amortization, depreciation, appreciation, and leverage (wealth multiplier) all make real estate investing attractive.

Focusing more on lease options now for C- and D-class properties to rent properties and eventually sell them to tenant.

Went from 7-figure year as a musician to bankrupt at 34. Found real estate mentor at grocery store and life changed.

Real estate is the final frontier for the average person to have a legitimate shot a creating wealth.

Paid $22,000 for mentorship in 2006. Everyone thought it was insane, but helped him get started.

People who made it were ready for it. “Move faster than your doubts.”

Find the deal first and then the money will find you.

Authored book “Do Over” that chronicled struggles and how he built his real estate empire.

Be intentional with who you surround yourself with. Peer pressure works.

Always be looking for a coach and outgrow them. Results accelerator.

Spends $100,000/year on masterminds – worth being around the right people of doers.

Goal was to increase passive income and decrease expenses. In 4 years became “retired,” but wants to be wealthy; not just financially independent.

Bookkeeper should be the first role you should outsource. Transaction coordinators and marketing person also helpful.

Hardest part of the business is to find the deal and get into contract.

Visit www.epicrealestateinvesting.com to check out the Epic Real Estate Investing Podcast.

Article Link: Text “simple” to 314-665-1767 to download the Hui Google Drive files and the 2018 Rental Property Analyzer

For a free electronic version of my bestselling book in 12+ categories text the word “ebook” to 587-317-6099.

Please help the show by leaving a review: http://getpodcast.reviews/id/1118795347

Join the Hui Deal Pipeline Club! SimplePassiveCashflow.com/club

Pardon the grammar – I’m an Engeneer, Enginere, Engenere… I’m good with math!

________Here are the Show Notes________

Estate planning

Guests I have are giving insights but always hire your own person because these things require personalization

I try to bring guests on and ask the questions that I think you folks would ask.

I believe you need to have a basic level of knowledge before engaging with a professional

For those of you who are in the Mastermind and my current investors you will hear about my Fort Knox strategy which makes LLC enitites creation look like childs play

Email me any questions to feature on the next ask Lane podcast or monthly email newsletter

Andrew L. Howell is the Co-Founder of the law firm, York Howell, with a focus on asset protection.

Many useful tools out there, but where do you as an investor fall on the asset protection spectrum?

Two fundamental risks: 1) Asset-based risks 2) Direct-based risks

Real estate considered as “hot” assets because liability risks are greater – more than equity.

Liabilities both inside and outside the asset.

Typically form a holding company to hold limited liability companies to abate asset- and direct-based risks.

Holding properties in one LLC basket is good, but still risks if something happens in one property.

Concentrate on family protection first (trust, wills, etc.). Then move to next level of asset protection planning.

If own property out-of-state, advise on setting up a parent LLC in states with charging-order protection.

Tough LLC rules and taxes for poor California residents!

Need to do your due diligence on reviewing PPM’s – especially who you are doing business with.

Asset does not create liability risk for LP’s; only GP’s.

If you get personally sued, can go after your MFH syndications and other assets even as LP.

6% of current generation feels obligated to give back to kids. Instead of giving, create a bank.

Create purpose when setting up your trust.

Please reach out to teamandrew@yorkhowell.com and visit www.yorkhowell.com.

Article Link: Text “simple” to 314-665-1767 to download the Hui Google Drive files and the 2018 Rental Property Analyzer

For a free electronic version of my bestselling book in 12+ categories text the word “ebook” to 587-317-6099.

Please help the show by leaving a review: http://getpodcast.reviews/id/1118795347

Join the Hui Deal Pipeline Club! SimplePassiveCashflow.com/club

Pardon the grammar – I’m an Engeneer, Enginere, Engenere… I’m good with math!

________Here are the Show Notes________

Jake and Gino have a great podcast and definaetly fit in the category as guys who are growing and doing things right

Let’s work together to redirect money from the Wall-Street casinos and corrupt financial institutions…To help the endangered ‘Middle Class’ savers find safer, more profitable investments in Main Street opportunities benefiting local communities. Join Hui Deal Pipeline Club and check out the sSimplePassiveCashflow.co/mission

Gino Barbaro from Jackandgino.com who focuses on MFH real estate.

Group owns 848 units valued at >$50 million. Expecting to go up this year.

Took 5 years to get $25K-30K/month in passive cash flow.

Fumbling around in the beginning with smaller cash flow amounts, but snowballs over time.

Came from the corporate world to managing a family restaurant. 2008 transitioned to real estate to make better use of time outside of the kitchen.

Highly recommend reading “The E-Myth” by Michael Gerber. Need a visionary, manager, and technician for any business.

Believes you need a Connector, Executer, and the Backbone. Can’t do all 3 – pick 1 or 2 and hire out.

95% of blocks are internal. The rest are external. So, focusing on resolving limiting beliefs and get a life coach.

Google Tony Robbin’s 6 human needs. Have to continue to grow and contribute in a large way.

Relocated to Florida and aiming to obtain $40K/month by end of this year.

Have lifestyle work for his business; not his business work for his lifestyle.

Becoming more efficient by hiring a VA and Digital Marketer for jackandgino.com. Wants to spread content and message; not work on menial tasks.

Focus on 1 or 2 niches for real estate and become an expert at it.

MFH has more barrier-to-entry v. stocks, crytocurrencies, etc. The more people in it, the less profit margin there will be.

Share weekly successes. It’s not bragging, it inspires people and surround yourself with the right people.

Be present in the moment. When you’re at work, with family, etc. focus on dealing with that situation.

Visit www.jackandgino.com. Also on FB, LinkedIn, Twitter, and Instagram. E-mail works too: gino@jackandgino.com.

Article Link: Text “simple” to 314-665-1767 to download the Hui Google Drive files and the 2018 Rental Property Analyzer

For a free electronic version of my bestselling book in 12+ categories text the word “ebook” to 587-317-6099.

Please help the show by leaving a review: http://getpodcast.reviews/id/1118795347

Join the Hui Deal Pipeline Club! SimplePassiveCashflow.com/club

Pardon the grammar – I’m an Engeneer, Enginere, Engenere… I’m good with math!

________Here are the Show Notes________

Brian Hamrick is from Rental Property Owners Association (RPOA) and runs Rental Property Owner and Real Estate Investor Podcast.

Currently owns 380 units, which cash flow makes 50% of W2 job salary.

Paydays not only about cash flow. Cash out refi and syndication benefits once and twice a year exceed W2 job salary.

Was sitting on cash waiting for next downturn. However, in past year, became a silent investor in commercial property, a NPN, and a self-storage facility.

Expects rents to plateau in future, but not to 2008 levels.

Started off investing in high-load tech funds, but bubble burst in early 2000’s and stocks tanked.

Rich Dad, Poor Dad inspired Brian to begin investing in real estate and obtain more control.

California is cash-flow negative market, so looked at positive cash-flowing out-of-state markets.

Transitioned to multi-family investing in 2008 for better scalability and profitability.

As passive investor, focusing on leveraging partners’ strengths for new passive investments.

Down the road, looking at developing the “missing middle” properties (small MFH 2-10 units).

Visit www.higinvestor.com to get in touch with Brian.

Just got back from Korea after my first vacation for the year. I wrote an article that you can get access by signing up for the monthly newsletter or via the Hui Deal Pipeline club.

Monthly updates and what I’m doing in my own investing

Podcasts have been piling up and I realized the need to add some context to the introductions to highlight important items to look out for. Also to call out opinions I don’t really believe in.

This podcast I had Brent Southerland what is a CFP but not one of those other quacks who get paid on commision and try to stuff you in whatever is most convenient or biggest paycheck for yourself.

Enjoy and remember to go to SimplePassiveCashflow.com/club to join our investment club

Brent Sutherland is a CERTIFIED FINANCIAL PLANNER™ practitioner, with over 11 years experience in financial services. With stops in the corporate accounting and investment world, and now the boutique financial planning arena Brent has witnessed, firsthand, how the financial services industry has fashioned itself into an overly complex machine in an effort to cause confusion, encourage mistakes, and justify fees; all to better benefit its own bottom line. He believes there is a strong correlation between financial noise and financial mistakes which further delay one’s personal financial success. Therefore, his objective is to help individuals turn off the noise and challenge the traditional approach to financial planning and thinking. In his experience as a financial advisor and personal finance enthusiast (+ early retirement advocate + semi-minimalist + real estate investor), Brent has found that most often the simplest solutions and some outside the box thinking will better help individuals on their way towards sitting firmly in the driver’s seat of their own financial world.

Why don’t financial advisors advocate for real estate investing?

Primary = Compensation conflicts of interest

Secondary = Lack of education, so pose it as a risky asset

Secondary = ERISA and how mutual funds came about with employer-sponsored 401k

How do FA make money? Similar to MLM? — (Is this short for multi-level marketing?)

Can tie this into the first topic above (compensation conflict, which is a primary reason why FA’s don’t discuss real estate investing)

Hidden fees in even low got mutual funds?

Transaction fees, Management fees (can be tiered based on assets), Loads (front-end, back-end), 12-b1 fees

What tricks do FA use?

Use of traditional planning items related to portfolio to justify: “security”, “diversification”

Use of confusion terms related to portfolio to justify fees: “alpha”, “sharpe ratio”

Use of graphics that show market returns (absent fees), but fail to discuss emotional impact on client and true returns normally witnessed

The importance of income diversification over portfolio diversification

Income diversification protects against big risks: loss of job, market crash, injury

Portfolio diversification is important, but is a secondary risk. Savings is even more important.

Why are paper assets more risky than hard assets?

Always going to be demand for hard assets, especially real estate (living, production)

Population trends are growing at an exponential rate, land and resources are not

You have more control over real estate; meanwhile the stock market is out of your hands

Why passive cash flow betters your odds of financial independence

Gets you to the point where you’re truly secure and can have peace of mind. Not worried about your boss/job, and not worried about things going on the the world, country, state (etc) economies that are out of your control. You become the boss of your personal economy.

Talk about your personal transition to direct ownership in Real estate and recovering from the lies?

Seeing it work for other people, educating myself (independent of my traditional “education”), and finally making the move to buy my first property (after some analysis paralysis and fear)

Proper planning techniques to access money tied up in your retirement accounts.

First know the rules involved (traditional IRA/401k versus Roth IRA/401k), as you don’t want to just hand a big chunk to Uncle Sam in form of taxes and fees.

Impact of cashing out plans

Strategies to more efficiently free up that money and keeping more in your pocket (Roth conversions, Substantially Equal Periodic Payments (IRS Code 72t))

What to look for in a FA?

Want someone who is fee-only (hourly or per service) and planning focused. Someone who is focused solely on managing your money for a % fee is going to always have a biased interest in moving you towards a liquid/paper portfolio).

Find someone who lines up with your values and interests. Never be afraid to interview multiple people and ask tough questions. Advisor should have conviction in what they do.

Understand that a financial planner can be very valuable, as there is much more to financial planning than how you invest your money (insurance, estate, education needs all need to work in harmony with an investment plan to best meet a person’s financial goals), but imperative that that financial planner is on the same page as you.