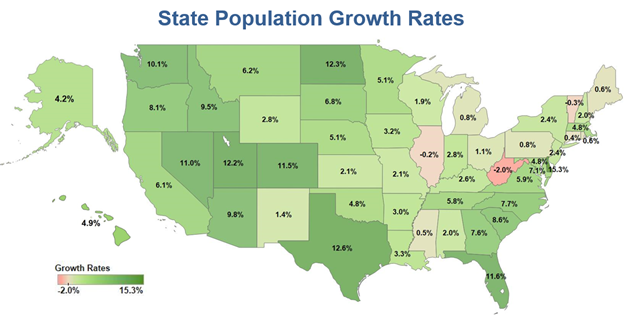

Between 2010 and 2017, population growth averaged 5.5% for the US as a whole. Delaware boasted the highest growth rate, 15.3%, over these years. A state with a relatively small population, however, needs fewer new residents to achieve such a high growth rate. The double-digit rates recorded by Texas (up 12.6%) and Florida (up 11.6%), both high-population states, are therefore that much more impressive. There were three states that posted population decline between 2010 and 2017: West Virginia (down 2.0%), Vermont (down 0.3%), and Illinois (down 0.2%). – ITR – 19.02.28

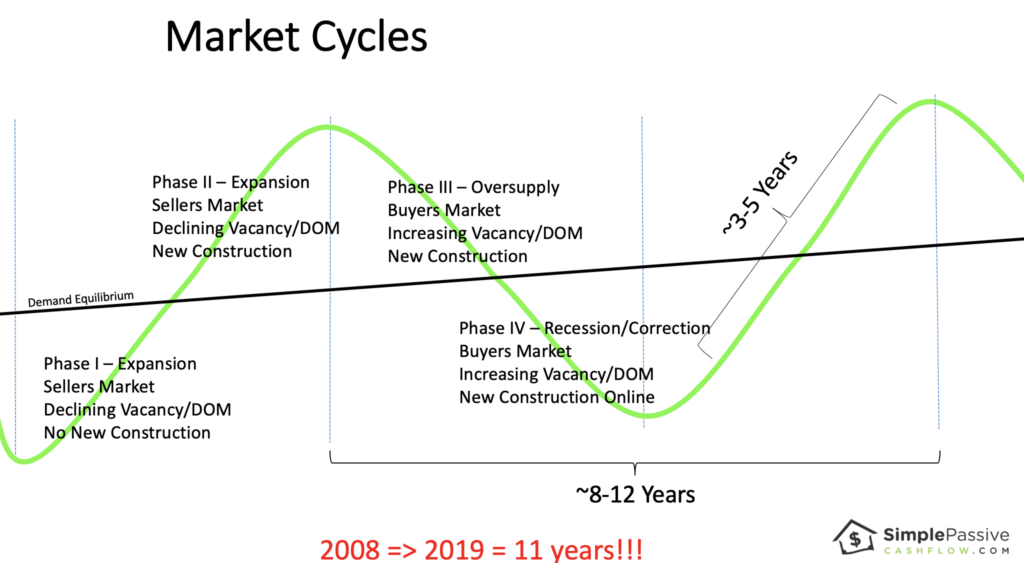

Since I feel we are in the 9th inning of an 11 inning ball game, I decided to pass on a recent Class-A apartment deal in a secondary market.

Here is my thought process…

First off, Robert Kiyosaki has a saying: “There are three sides to a coin.”

People like to argue that it is either a good time to buy or a bad time to buy. For example, they say that “MFH” is overheated or commercial is getting killed by Amazon and e-commerce. I think these are mental justifications by tire-kickers who are scared to act. I mean really how many of these people are under the accredited status (not sophisticated) or not obtained their “Simple Passive Cashflow number.”

Sophisticated investors still trying to grow live on the edge of the “coin.” They buy deals out of the reach of amateurs due to the amateurs’ lack of network/knowledge. These opportunities are undervalued, with undermarket rents, with value-add opportunity. Sophisticated investors are patient; they don’t stray from standards that force them to get crushed in a market correction. (Cashflow from other investments makes this possible.) They invest following the macro- and micro- trends and don’t gamble on gimmicks such as guessing where Amazon’s next HQ is going or where the hurricanes just drowned a market.

The trouble is that an unsophisticated investor or an outsider (in terms of having a poor network) is figuring out which of these deals transcends the two sides of coin and is on the edge. Stating the obvious (though often ignored by many)… starting out as an investor is going to be slim-pickin’s due to the lack of network. But you have to push through this rough part. You are not able to decode the noise until after a few deals or having someone mentor you.

With that out of the way let’s continue…

Real estate is one of the best risk-adjusted investments out there. In private placements or syndications, we are able to crowd-invest in larger & more stable assets while maintaining control with operators who are aligned in our best interests. By going into a project properly capitalized with adequate capital expenditure, budget, and cash reserves, you are able to remain steadfast through softness in the market where rents stagnate and vacancy decreases.

(If you are starting out you should start with turnkey rentals even though they are much more volatile)

Pause there. In troubled times what happens?

People lose their jobs and there is a bit of shuffling.

Yea, people need housing, but there will be some vacancy as some people will lose their jobs and be displaced elsewhere.

Following this train of thought…

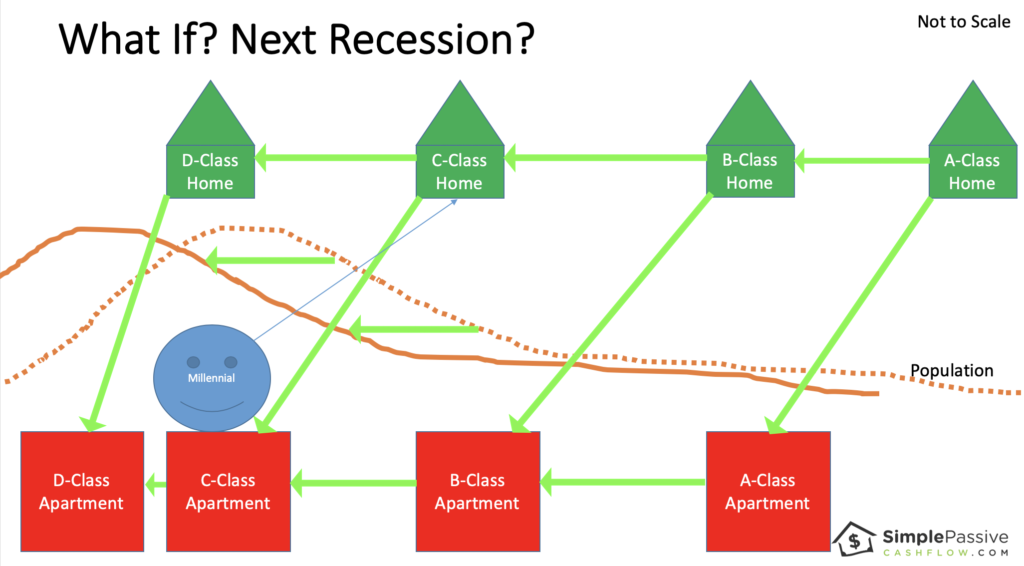

In a recession, the high end or class A will be hurt the most. It is Class A workers who fulfill much of he discretionary services. We are already seeing softness in rent by rent decreases in class A of the high-end markets such as Seattle and San Francisco.

For example a once $1,700 one bedroom is now $1,625.

Most deals model for 1-5% in annual rent increases or escalators. Other than the Cap Rate to Reversion Cap Rate truck, this is the second most manipulated assumption in investment modeling.

In this unfortunate but natural event, the A-Class renters will fall to class B housing. Some homeowners will even lose their jobs creating foreclosed investments for smaller investors in the single-family home scale.

What’s happens to the B and C class renters?

It is likely that they will also lose their jobs at higher or lower rates, but that is up to debate. In the same fashion as the A-Class renters, the Class B/C renters will downgrade to make ends meet.

I imagine this similar to a game of musical chairs (where the chairs are getting crappier and crappier). Or it looks a lot like the natural housing shuffle in the summer near colleges with people moving in and out. The landlord/investor is likely to see increased vacancy.

Multifamily occupancy varies from 85-95% in stabilized buildings. Some markets are hotter and some are colder. It is important to use the correct assumptions depending on the markets. For example, Dallas typically sees 92% occupancy while Oklahoma City sees 89%.

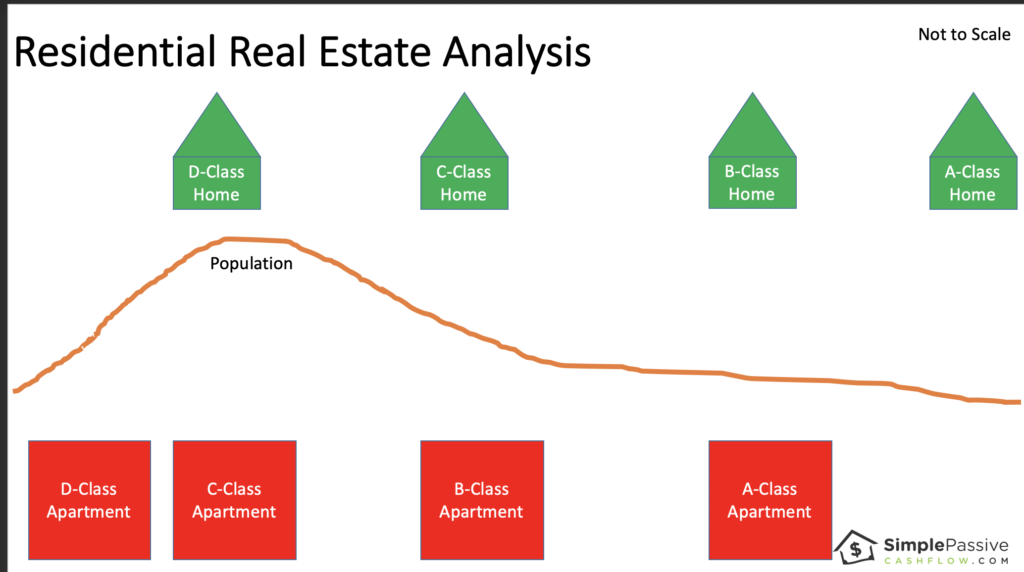

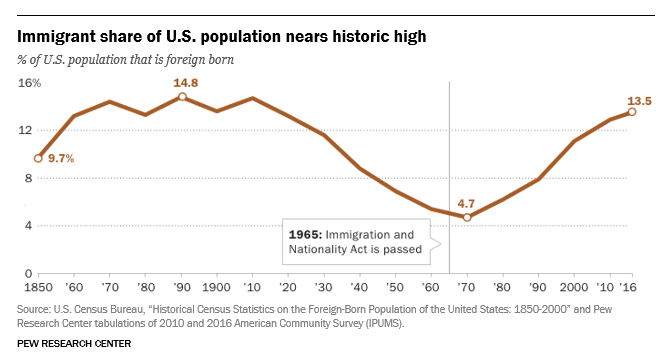

One of the reasons we love multifamily is because of the decline of the middle class and the need for more scalable workforce housing. [And those millennials can’t save] The population is increasing too.

[I like to use this image cause I make fun of millennials… this is the millennial version… cause they can’t seem to afford (or want) to own anything]

When I travel to Asia (which I see as a more mature society, for better or worse) there is a much larger wealth gap than in the USA. People are living in cramped apartments or very rare single-family homes. And they are driving a Mercedes on barely enough money to share a family moped. This is the trend that the USA is following.

As with many things, you need to look past the headlines and the general data. Instead of analyzing a whole asset class, as the media likes to do, let’s break down vacancy in terms of classes.

Here are some typical vacancy rates (notice the spread).

Class C 4.5%

Class B 5.0%

Class A 5.5%

Why? Because there is just more demand for the lower class properties cause there is more demand than supply.

Many times the business plan is the be the “best in class.” For example, businesses want to be the best mobile home park or best high end remodel because you attract the richest customers in that niche.

I like to monitor the number of new units coming online because that is your downward pressure. It is rare that new builds are for Class C or Class B.

The micro-unit trend is an attempt to build for Class C and B tenants due to the need. But often the numbers don’t make sense when you have purchased the same building materials and mobilized the same crews to build a Class B asset as opposed to a class A asset.

Let’s go through that Armageddon example again.

Class A will have to drop rents severely and see great vacancy.

Class B and C will see vacancy come up too as people are losing their jobs but should see some absorption from ex-A Class tenants.

Mom and dad will also see some absorption as deadbeat son or daughter move back home.

Shows like Friends and How I Met Your Mother will go on for another decade.

Note: one can argue that class A+ will not be affected at all which I believe is true. That’s why we are trying to invest right to enter that untouchable status.

I remember when I sat through the same economic presentation at work from 2010-2014. The sentiment at the time was that it was going to be an extremely slow recovery. It makes sense that the length between the 2008 recession and now is very long which is why I mentioned an 11-inning ball game.

This is why I took a set back from some pretty Class A deals because I asked myself the following questions:

1) What will happen to the rents if IT should happen?

2) Is the modeled 90% vacancy rate going to get blown up?

Class B and C apartments in strong submarkets will perform best over the long term. If you ensure the loan term is long enough so you don’t get hurt then you should Outlast the bumpy ride ahead.

Beware of the self-destructive behavior of not investing. You know what I mean… are you someone who self-sabotages?

Understand the micro and proceed if the numbers make sense.

I have to admit Class C and B assets are boring but work especially in a seller’s market because 1) they cashflow and 2) have a forced appreciation value-add component to give you levers to pull in tough times.

Again going back to Mr. Kiyosaki’s three-sided coin quote, investors go through three stages.

Stage 1: Go into MFH… Duh (I did well at single-family rentals let me try apartments)

Stage 2: Be a contrarian investor so go into other asset classes most decent investors are afraid or don’t even know about

Stage 3: Do special projects such as Affordable house taking advantage of tax credits or specialized operators (ie take abandoned big-box space like movie theaters and convert to the latest consumer needs)

Experienced investors who were in the downturn in 2008 say its interesting that the sentiment in 2006 was exuberance that it was going to keep going up. Now in 2018 the sentiment is fear… This is a good thing.

Remember that in this market we still have:

Historically low-interest rates

Historically high rent increases (not 8% anymore but still 2-4%)

Historically low vacancies

Things to monitor if you really need to geek out on numbers:

2 and 10 yield t curve. When that crosses you have just-a matter do time. Because its a measure of fear.

Automation and AI – huge shifts in jobs. People need to work but technology has been increasing since the beginning of time.

Wage growth

Bankers prospective: how deals are getting funded and by who (institutional or dumb capital)

There is a saying out there that real estate is location specific. However, when I invest in more stable asset classes its a National market based on the economy both USA and international. When you invest in a micro-economic fix and flips then its location specific. When you invest in commercial assets it’s with more stable tenants and based on the aforementioned larger economy.

How affordable is rent really? – “During the same span, median effective rent nationally has risen by about 26%. That rent appreciation pushed the median monthly rent nationally to around $1,220 per unit to end 2018. With the US median household income being just over $62,000, this rent accounts for 24% of monthly income. Using the typical benchmark of monthly rent being 30% of monthly household income for affordability, a margin remains for renters.” – [If you stick to using 2% and under rent growths and stay away from Tier I or Primary markets you should be fine] – ALN 19.02.24

A lot of people point to the Yield-Curve as a big indicator. In the end, I do believe that real estate will go down because of consumer instability. But if you have stocks you should sell those before even thinking of lumping it into cashflow type rental real estate.

“The guy not investing right now and hoarding cash (with net worth of under $1M… because if you can live off your cashflow then cool you can do what you want) is just afraid and lacks deal flow. Its like the person who complains that there is nothing to do during the weekend in LA (insert city with a vibrant scene) when in actuality they don’t have any friends (lack dealflow)… and by the no one likes (has a bad attitude and that person who makes excuses”

Doomsday theory: Everyone talks about national debt but we are far far behind debt to GDP ratio that of Japan. When Japan hits the wall lookout. Her is my theory… watch out post-Japan Olympics when they have to let loose the belt (after a holiday period of excess calories). Leading up to a period where Japan has to save face while they are in the Olympic spotlight (and I’m not being racist cause I am Japanese and it is a thing). I don’t have the latest data but Japan is at around 250% where the USA is at 100%.

Household debt KPIs: student debt, car loans, housing debt. Which is why I like these assets that are used by the poor and middle class! #RenterForever

Lane’s theory: I’d rather be in deals that cashflow today that do better in a recession like Class C and B assets. Say it cashflows a 8%.

The guy who is stilling on the sidelines with the “hoarding cash” mindset will lose because they will make 0%.

I, on the other hand, might dip from 8% cashflow to 4% cashflow. On paper, I might be in a market with compressed cap rates but hopefully, I have forced appreciation potential if I really needed to sell – the counter move is to get 8-12 year debt to effectively bridge you to the next side of the market cycle. In the meantime you cashflow 4% which is 4% more than the “hoarding cash guy”.

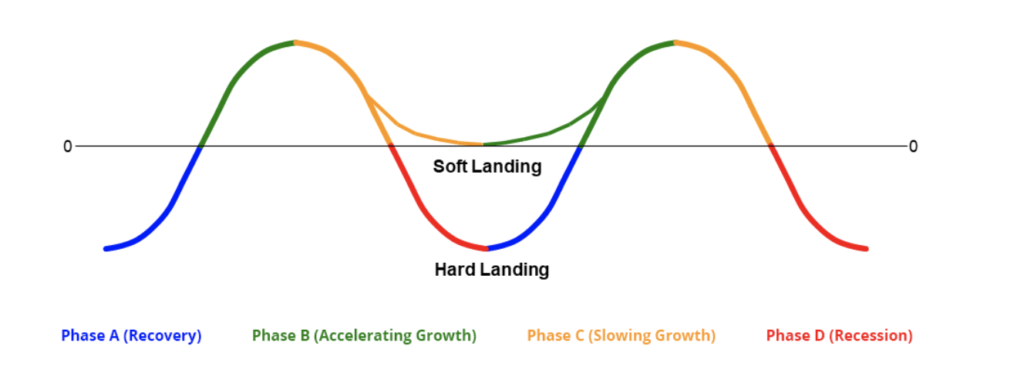

In addition, remember back in the 2008 crash. 2009-2012 people did not know if that was the bottom and it was so hard to close deals in that Phase IV (see below). “Hoarding cash guy” in 2009-2012 and the few years after the next recession will likely be in the same clueless situations.

Wouldn’t you like to be in solid Class C and B assets that continued to cashflow?!? 4% x 4 years is still 16% ahead!

Now if you are “hoarding cash guy” with no deal flow then I get it. Saving cash is the best thing to do for the guy with no deal flow or does not know how to run the numbers. I guess everything does suck.

[Investors are chasing for decreasing yield these days] – REI.com – 19.03.4

[Sophisticated Investors know interest rates and caps go up and down together and their money is made in the delta between the two] – REI.com – 19.03.4

Of course, all the Pro-Apartment publications will say this: Get Ready: Recession-Proofing An Apartment Portfolio – National Apartment Association 19.03.7

But enough of this doom and gloom because most gurus out there call recession everyday just so they can have Tweetable content. And they make a living selling subcriptions to their $79/month newsletter. But we are better than the average investor! And understand that future softness could very well be slowdown before the next great bull market.

To join our Hui Deal Pipeline Club and stick with the group join below:

MFH is the obvious choice when it comes to jumping into syndications because it is the shorted logical leap for a single family home investor.

Here are some other reasons:

We need more housing for class-C and class-B renters due to population increasing and rising interest rates

Inflation favor hard assets

We are no longer a buying nation we rent (think millennials)

[This is the millennial version… cause they can’t seem to afford (or want) to own anything]

The government is trying their best to incentive investors – Follow the money people!

2018 tax changes with bonus depreciation make it better for projects like large apartments to get better tax treatment than ever before via a cost segregation.

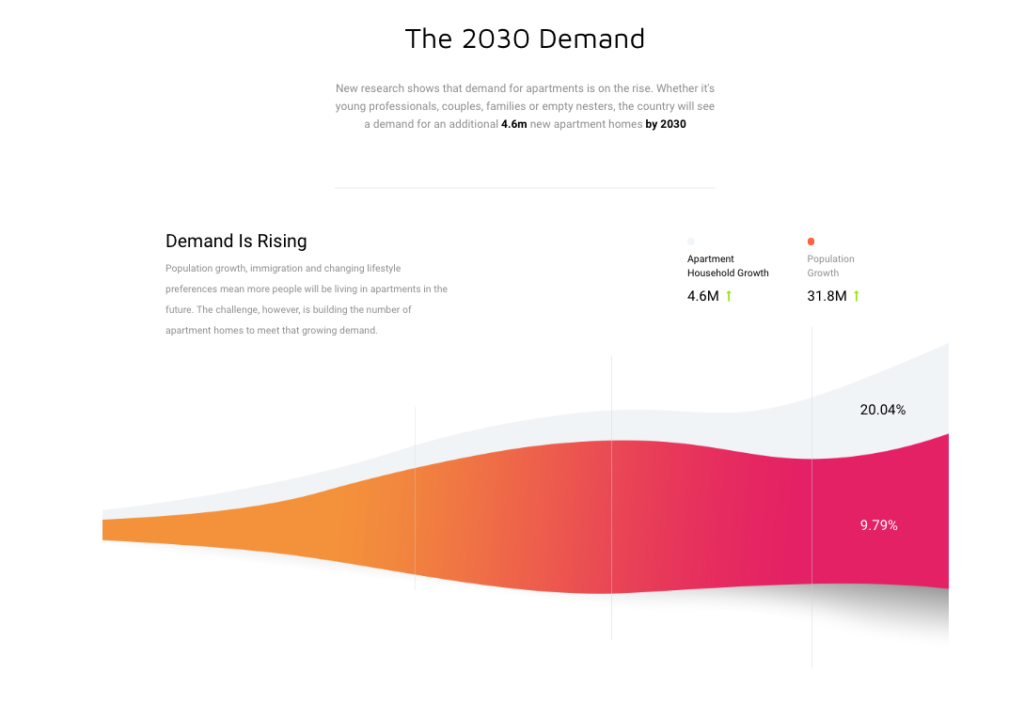

The country needs 4.6m new apartments by 2030 (Source). We need more class C and B housing. Our country is becoming more like Asian Countries where the is a bigger divide in the wealth gap and need for low-income communities.

60+ units or more to get economies of scale and to have dedicated staff on site

1970-1980s Class B or C buildings

Utilize Fannie Mae or Freddie Mac Non-Recourse debt with up to 12-year loan terms

Buy right – rehab units with $2,000-8,000 per unit – reposition by improving operations and stabilizing rents for exit

Property cashflows day one after purchase

Re-brand (new signage and online presence)

Value-add:

Poor existing property management

Old tired units or leasing center

Outdated amenities

Creative improvements using best practices and technology

Additional opportunity for extra income

Miscellaneous ideas for thought:

2010 to 2015 is the golden era of Multifamily. Many rents were going up 5-10% per year (average 2-3% in a good market).

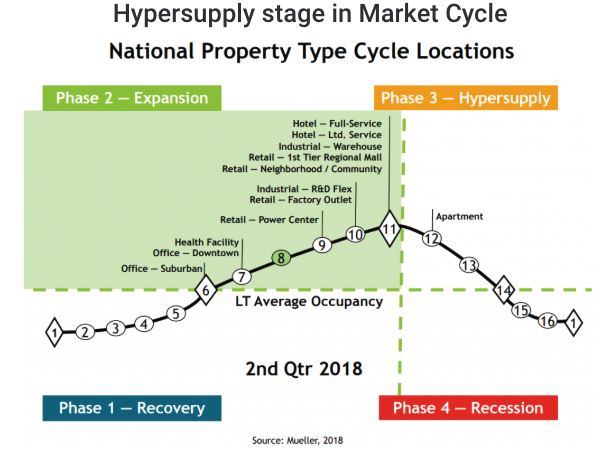

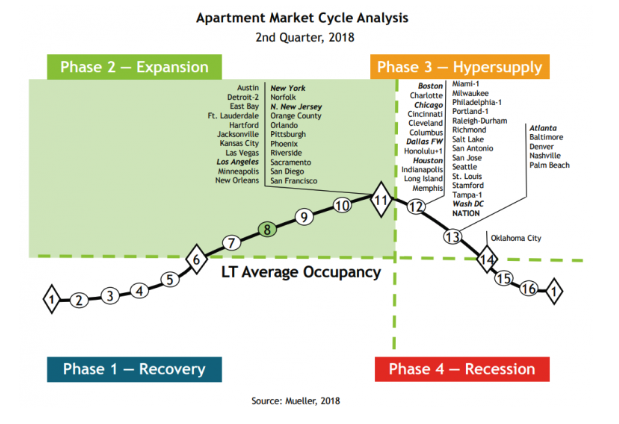

The (Global/National) markets go in cycles, the sub-markets (physical locations) go in cycles (see below)

Asset Classes go in cycles but hopefully, you are investing with the pros who transcend the high-level norm.

Lending

Unit Mix Discussion

When looking at the unit mix profile take notice of the mix of studio/efficiency units and 1,2,3 bedrooms. This can throw off your rent per square foot metric which is important when comparing comps. A sudio/1 bedrooms will have higher rent per square foot amounts however the tenants will be more transient.

The 2/3/4 bedroom units will yield lower revenue per square foot but will attract more of a family type renter and improve the intangible community aspect.

Headwinds

Millennials Leaving the Renter Pool?

Once they get married and have kids, they move out to the suburbs into a single-family house. 82% of couples between the ages of 25-39 married with 2 or more children live in a single-family home. The only difference today is that Millennials are getting married and having kids later in life so they stay in the renter pool longer. And the lack of affordable homes caused by the great recession of 2008 has delayed new builds to be created which creates more demand as population increases. New builds are really starting to come online.

The 73 million Americans aged 18 to 34 are beginning to cycle their way out of apartments and into homes. In fact, the net growth of 18-34-year-olds falls to zero by 2024.

Fun facts about new builds:

2009 and 2010, multifamily housing starts hit a low of about 100,000 per year.

The 40-year historical average (1970-2010) is 355,000 starts per year.

Multifamily housing starts gradually increased, peaking at 383,000 units in 2015. Production then declined modestly, to 381,000 in 2016 and 345,000 in 2017 but reverted to 354,000 in 2018.

Annualized multifamily housing starts stood at 289,000 units in January 2019, up from 278,000 units in December 2018, but down from the one-month annualized peak of 435,000 in January 2018.

Multifamily statistical models forecast about 401,000 average annualized starts in each of 2019 and 2020, 389,000 in 2021, and 390,000 in 2022, all of which are modestly above the 40-year historical average of 355,000 multifamily housing starts per year.

The cumulative 17-year shortfall of multifamily housing starts (benchmarked against historical norms) peaked at over one million units in 2013 but is on a choppy decline, standing at 905,000 as of February 2019.

Zelman & Associates are forecasting multifamily starts to increase 3% year-over-year in 2019 and another 1% in 2020, as opposed to a decline which many researchers previously forecasted.

MFH is great but you need to be aware of new Class A apartments being built to put downward pressure on pricing – Source MHN

MFE 2-6-19 – 2018’s Record Deal Volume Suggests Positive Trajectory for 2019 – “driven in large part by increased interest in the student housing sector, which accounted for 17% of all deal activity in the third quarter, compared with a consistent 4% over the past 13 years” – [I don’t like student housing as I am seeing an education bubble with all the lending. It’s crazy how dorms get renovated every few years]

MFE 2-6-19 -Freddie Mac Sets Multifamily Production Record – “$78 billion in total production bests the company’s prior record of $73.2 billion set in 2017. Overall, the company financed more than 860,000 rental units, more than 90% of which are considered affordable to low- and moderate-income families making 120% of area median income (AMI) and below.” – [More more more!!!]

Past performance is no indicator of future success. Many operators in Dallas 2012-2014 were able to double investors money in just a year or two – come to find out they only implemented 20% of the rehab. It was mostly market appreciation which is out of our control and can bail out a bad operator.

Pretty simple if you understand the way to utilize them and how they play together in real estate transactions

Applies a lot in larger transactions (multifamily), but can be applied as well in smaller (single family) transactions

Income (types):

Different ways you can make money on a property

Rent – not what is on the contract, but what the market would yield for the space that you have

Other Income

Pet Fees

Laundry

Reserve Parking

Late Fees

Gross Market Rent:

Sum of all the different types of income you can earn from the property

Deductions that can be taken from the Income types (can also be called Efficiency deductions):

(Loss to) Lease:

Loss of income based on the market value of the property minus the amount you are renting the property for

Example: You have a property you are renting out at $750/month. The current market value of the property is actually $825/month (based on listings in Craigslist, etc.) You have a $75 Loss to Lease per month on that property

This is money that will never be gained, as the market changes so much

This has to be factored in when looking at properties, and you should constantly monitor the market you’re in to see what kind of Loss to Lease you’re taking on

(Loss to) Vacancy:

Especially on bigger properties – you will never have it leased all the time

Normally, there is a week or two of vacancy, sometimes more (up to a month or even longer) between tenants

A lot of people like to estimate 5% loss due to vacancy, but should be considered more scientifically than just stating a number. For example, if it’s a single family home, you’ll want to factor in at least one month’s rent, which would be equivalent to 8%. If it’s a duplex you’ll want to factor in one month’s rent for your most expensive unit. The more units you have, the more you can expect that vacancy rate to go down. But be conservative when you’re writing up a deal – the smaller the deal, the higher your vacancy rate. So start at 10 if it’s a one or two unit deal, and then drop accordingly.

(Loss to) Collections:

Isn’t just money you will be getting back from tenants who are late on payments

Includes loss of money from tenants who move out and are not able to pay their balance

You need to factor it on your own in the market you are in and what the economy you are dealing in is

Example: If you are dealing in C or D type neighborhood, you will have to factor in [Loss to] Collections. If you’re in a B or A type neighborhood, then you can lower Collections down to zero and assume the loss will just come out of Vacancy

Physical Occupancy vs. Economic Occupancy in Apartment Investing:

Note this is mostly used as an example of what LP’s should be aware of. In most cases LP’s either know too little for example they just look at the Pro-Forma returns and don’t look at the assumptions that the operator used to get there. Or they spend so much time evaluating things that have little impact to the numbers for example running away when they hear of minor foundation issues or rodents that can be remediated with a few thousand dollars of seller concessions. In the Passive Investor Accelerator & Mastermind we try to focus on what is really important but obviously that is not free (but going into a bad deal is costly too). Vacancy in apartments decreases top line income and getting occupancy as high as possible is the goal. There are two different types in apartment investing 1)

Physical Occupancy and 2) Economic Occupancy. Physical occupancy (number of units that have a tenant with a signed lease, occupying a unit) is what most people are familiar with in apartment investing and what is often overlooked when a passive investor reviews the underwriting assumptions of a syndicator. This is shown on the rent roll with the tenants name next to the unit number which also needs to by physically audited with boots on the ground verification. Physical occupancy is a percentage calculated by dividing the number of occupied units by the total number of units for example a 100 unit apartment with 8 units vacant has a physical occupancy is 92% (92 ÷ 100).

Pay attention here… if a rent roll shows a unit is occupied, doesn’t necessary mean it’s also generating income. A tenant might be a deadbeat or the nice way of putting it there might be “loss to lease.”

Economic occupancy is the amount of money of actual rents received as related to the occupancy. This also takes into account tenants who don’t pay the full rent and also things like concessions ($200 move in specials, discounts to motivate tenant prospects). This is the net rents received (not including other income). The net income will deduct for bad debts/loss to lease. The economic occupancy is calculated by dividing net rent received by the gross rents possible.

On the same 100 unit apartment, assume each unit rents for $1000/mo. There’s a gross potential of $1,200,000/year (100 units x $1000 = $100,000/mo x 12 = $1,200,000/year). Using the same physical example say there are an additional 10 deadbeats (that the previous seller stuffed in there right before the sale) and 10 people only able to pay half the rent… then you are looking at an economic occupancy of 75%.

This might be a little too much info for a LP but Economic occupancy can be a sign of the following:

Bad Management and bad collection practices

Bad tenant qualification practices

PM stealing money

Bad rent collection practices

Lack of maintenance, causing tenants to leave

Or a clear sign of opportunity!

Effective Gross Income (EGI):

Gross Market Rent minus whatever loss will come out during operations (Efficiency deductions)

Real money that comes in through the property

From your EGI, you will still need to deduct your expenses (listed below)

Expenses:

Insurance

Professional Services – Leasing commissions and/or other professional services you bring in (legal, accounting fees, etc.). If you’re an LLC, you will need to put in your budget the cost (tax) for the LLC every year ($400 – $500), IRS

Regular Maintenance (landscaping, snow removal, heater service, pest control, touch-ups and minor renovations on unit before tenant moves in, fixes like clogged-up toilets, etc.)

Rule of thumb for Regular Maintenance: Brokers will place it 3% of your EGI, but is more effective to think it as dollars per unit.

Example: If property is something you bought, did a full renovation on, put tenants in, and then got it refinanced (BRRRR – Buy Rehab Rent Refinance Repeat), your maintenance should be lower because you’ve done everything and should be able to call for a warranty call at the very beginning if it’s something the contractor who did the work on your property didn’t do. If you’re very good at turning these properties over, then you should have very little maintenance going in

If it’s a newer rental, could be anywhere from $300 – $400 every year

If it’s something you’re inheriting (inheriting maintenance issues as property already has current tenants and will need to deal with it as you go), you will want to go with higher maintenance numbers: $700 – $900 per unit per year

Will really depend on how much you project it to be (check out the property thoroughly, and/or if there are existing tenants, ask them what are the maintenance issues) as it can really kill or make you a lot of money on your deal.

Property Management Fee – 6%

Property Management means looking after the property and make sure operations is running smoothly

If you are managing the property, you will want to put that in your own pocket

Asset Management Fee – 2%

If you are hiring a Property Manager, you will also need to hire an Asset Manager, or you can be the Asset Manager and that money will also go into your own pocket

Fee of managing the Property Manager

Asset Manager will be the one to pay mortgage, ensure real estate taxes are being paid, monitor the markets and ensure that the right rents are being charged, will also have veto power to veto work orders that might come up that you don’t want to have done because they’re too expensive, etc.

Asset Manager is also there to look at the real value of return on the asset

Utilities

Everything from heat, water, sewer, even CCTV systems, phone lines

You will want to look at the prior owner’s expenses for utilities were (around 18 months’ worth), or look to see what the market or other people are paying

Make a good guesstimate on what your utility projections are going to be and go from there

Real Estate Taxes

(Above the) Line:

Term sometimes used by brokers when grouping Gross Market Rent, Efficiency deductions, EGI and Expenses (everything that gets deducted out to determine the profitability of the deal)

Note: I don’t really talk in terms of Cap rates because you can manipulate the “above the line” assumptions to get whatever you want

Net Operating Income (NOI):

EGI minus all the expenses that can be deducted from it

Does not include mortgage payments or Debt Service (money you have to borrow to buy the property)

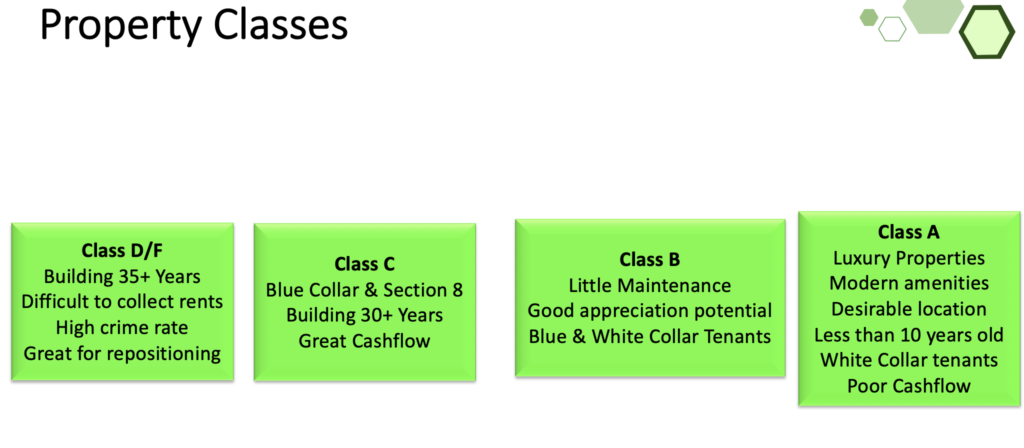

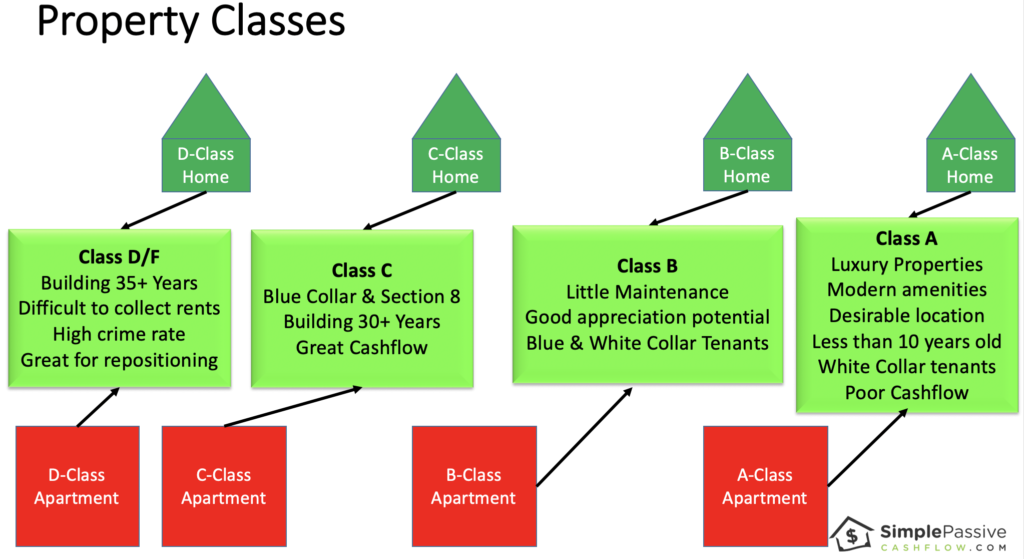

Classes:

Class A

Built in last decade and are more luxury

Struggle in recessions as white-collar workers drop back to Class B Assets

People are jogging around at night

Class B

Generally 10-25 years old

Younger white-collar and blue-collar residents

Cap rates are higher than Class A and lower than Class C

Females not advised to take that evening jog around the block

Class C

1970-1985 built

Mix of blue-collar to lower, single mothers etc

Good cashflow but comes with issues that property management must keep in check

In a recession, a lot of B and A class renters fall back to Class C

Its ok during the day but personally I would not want to be there at night

There is crime but you want to look for minimal violence/homicide

Class D

1960s and older

Generally Section 8, government-subsidized residents such as LURA, LURK with rent restrictions

You don’t even want to get out of the car to walk around during the day

High crime area, security needed

Can be amazing rewards for taking on this risk

Capital Expenditures (Cap Ex):

Also usually referred to as Below the Line expenditure but is also sometimes considered as Above the Line, depending on whether you are selling or buying a property

Long-term improvements to your building/ property

Major renovations to bring unit/ property up to market standard (replacing the roof, replacing the furnace, full renovation on a unit)

Any expense that will add long-term value to your building

You will need to set aside money for this (Cap Ex Reserve)

Not taxable as it is just money you are earning but will be setting aside in a savings account

CAP Rate:

NOI divided by the price you’re buying the property for

Determines the money that the property will give you

Example:

If NOI is $100k and the price of the property was $1 million, then CAP Rate would be 10%

Intended to be used when valuing buildings (especially commercial real estate)

Cash Flow (CF):

NOI minus Debt Service

Also determines your Return on Investment (ROI) on the property

Debt Services Covered Ratio (DSCR):

Looked at by the banks

How many times the deal can cover the Debt Service

Calculation: NOI divided by debt service

Most banks will want to see a DSCR above 1.25%, you will want to see a DSCR of above 1.5% to get a higher ROI

Green Credits:

Breaks in your interest rates for employing energy saving means

Many buildings have asbestos from the 1960-1970s. We have a binder in each office that shows how to handle different situations should the asbestos be exposed. All the managers go through training as well. As long as we don’t disturb the drywall than it’s safe. This is consistent with how many organizations do things outside of real estate… I know because I am a facilities Engineer as a day job.

How can you increase the value (increase income or decrease expenses)?

Application Fees

Late Fee

Pet Rent

Early Termination

Month to Month Fee

Lapse in Renters Insurance Fee

Redecoration Fees

Resident Discount Program (This seems counter-intuitive unless we’re at CostCo.)

Marketing Coordination Fee (to pay for social media at the property)

Eviction Holdoff Fee (You can’t pay, so we’re going to charge you not to kick you out)

“We also have community gardens which we charge for”

Offer a steam cleaner, power washer, or other useful tools for rent by residents.

Place native ads/sponsored posts from relevant local/lifestyle businesses on your community blog.

Offer furniture rental packages.

Sell ads on the digital signs in your leasing office/elevator lobby/parking garage.

Create moving kits with tape, boxes, packaging, etc. Sell them from your website, or build a set of items you can resell through Amazon. One-click buy and move!

Shared sponsored posts from local businesses on your property Instagram account.

Upsell garages, bike lockers and/or storage space.

Upsell smart home technology packages.

Offer RentPlus to help residents build long-term credit. They charge a small fee to the resident, you get a cut.

Offer interior design consulting through Havenly. Make affiliate income when your renters buy goods and services through the app.

Buy cable and Internet services in bulk at wholesale rates. Resell them to residents at a discount and make money off the markup.

Host resident events. Partner with brands who are willing to pay to get in front of your renters as a target audience. (There are lots of them out there.)

Publish a resident newsletter (print or digital). Sell ad/editorial space to local businesses.

Rent space to Amazon so they have a place to put their lockers.

Turn your move-in gift into a subscription box trial. Make money when new renters upgrade to an ongoing subscription.

Host “premium” resident events that get people excited. Charge a small admission fee. Open them to the public and charge more for non-residents.

Sell the furniture and items you showcase in your model. Partner with Wayfair, West Elm, or a local furniture store on this.

Sign up for Amazon Associates (or any other affiliate marketing network). Create timely gift/necessity guides (Mother’s Day, spring cleaning, back to school) that are relevant to your residents.

Article Link: Text “simple” to 314-665-1767 to download the Hui Google Drive files and the 2018 Rental Property Analyzer

For a free electronic version of my bestselling book in 12+ categories text the word “ebook” to 587-317-6099.

Please help the show by leaving a review: http://getpodcast.reviews/id/1118795347

Join the Hui Deal Pipeline Club! SimplePassiveCashflow.com/club

Pardon the grammar – I’m an Engeneer, Enginere, Engenere… I’m good with math!

________Here are the Show Notes________

Jake and Gino have a great podcast and definaetly fit in the category as guys who are growing and doing things right

Let’s work together to redirect money from the Wall-Street casinos and corrupt financial institutions…To help the endangered ‘Middle Class’ savers find safer, more profitable investments in Main Street opportunities benefiting local communities. Join Hui Deal Pipeline Club and check out the sSimplePassiveCashflow.co/mission

Gino Barbaro from Jackandgino.com who focuses on MFH real estate.

Group owns 848 units valued at >$50 million. Expecting to go up this year.

Took 5 years to get $25K-30K/month in passive cash flow.

Fumbling around in the beginning with smaller cash flow amounts, but snowballs over time.

Came from the corporate world to managing a family restaurant. 2008 transitioned to real estate to make better use of time outside of the kitchen.

Highly recommend reading “The E-Myth” by Michael Gerber. Need a visionary, manager, and technician for any business.

Believes you need a Connector, Executer, and the Backbone. Can’t do all 3 – pick 1 or 2 and hire out.

95% of blocks are internal. The rest are external. So, focusing on resolving limiting beliefs and get a life coach.

Google Tony Robbin’s 6 human needs. Have to continue to grow and contribute in a large way.

Relocated to Florida and aiming to obtain $40K/month by end of this year.

Have lifestyle work for his business; not his business work for his lifestyle.

Becoming more efficient by hiring a VA and Digital Marketer for jackandgino.com. Wants to spread content and message; not work on menial tasks.

Focus on 1 or 2 niches for real estate and become an expert at it.

MFH has more barrier-to-entry v. stocks, crytocurrencies, etc. The more people in it, the less profit margin there will be.

Share weekly successes. It’s not bragging, it inspires people and surround yourself with the right people.

Be present in the moment. When you’re at work, with family, etc. focus on dealing with that situation.

Visit www.jackandgino.com. Also on FB, LinkedIn, Twitter, and Instagram. E-mail works too: gino@jackandgino.com.

Text “simple” to 314-665-1767 to download the Hui Google Drive files and the 2018 Rental Property Analyzer For a free electronic version of my bestselling book in 12+ categories text the word “ebook” to 587-317-6099. Please help the show by leaving a review: http://getpodcast.reviews/id/1118795347 Join the Hui Deal Pipeline Club! SimplePassiveCashflow.com/club Pardon the grammar – I’m an Engeneer, Enginere, Engenere… I’m good with math! ________Here are the Show Notes________

Why professionals are trained to go through the system

The two excuses why not to leave the professional system

Wealth formula – Mass (money) x Velocity (Leverage) = wealth

You need to make money

What happen to assisted living project?

Taking shots and trying things out? Where is the transition point from taking singles to going to homers?

We are talking about Jorge from Simplepassivecashflow.com/ahp

SPC listeners are usual creatures. Get me in a room with a bunch of W2 workers talking about their frequent flier miles and their cars and I’m completely turned off. What are your thoughts on coping with this?

What are some ways you teach the entrepreneurial spirit with your kids?

What if they just want to work for the man or do peace corps?

Simplepassivecashflow.com/buck to get the free 1-hour coaching offer from Buck.

—————————————————–

Our worst W2 moments which were our Han Solo Moments

How to make it as a medical professional? – Kiss Butt 😁

We are robots.

For more content go to Simplepassivecashflow.com/buck

“Retirement accounts (with so-called tax benefits) only make sense if your AGI is over 340k AND you have a substantial amount in your IRA already (400k+). The wealthy people I meet don’t use these things as a primary wealth building too because it does not help them on their taxes today. These retirement accounts are tools to be used in certain situations, read on to see when it makes sense for you.”

“If you income is under 340K and/or your IRA/QRP/Retirement funds is under 500k and/or you are less than 55 years old I think dumping your IRA/QRP money (in a controlled manner managing your AGI not going too high) is the way to go.”

Like these coaching calls? Get access to dozens of them for free when you opt in to our community here.

I agree that retirement plans are bad. When you contribute to a 401K, IRA or other deferred compensation plan, you are voluntarily giving the IRS a tax lien on all of the retirement money and the growth on that money. Also, with tax rates likely to be higher in the future, the amount of the tax lien will increase.

Hui Members – please reach out via email for the current vendor we are using these days

0:01 This is a story about a dude named Lane he moved to the mainland and bought one place to stay. And then one day he went try to rent them

0:10 out, and then he became one. That’s still me.

0:15 Hey everybody, this is Lane with the simple passive casual podcast. Today we are going to talk about self directed IRAs. If you guys didn’t know you guys can take your retirement account and roll it into a self directed IRA, either a Roth form or a regular IRA form, but you’re going to need to get it out of the hands of those who can say the names that the Vanguard’s fidelity’s all those like big brokerages that you know they got in cahoots with the government way back when in the 80s in the 70s. I don’t know if this is true American history here but it created this thing called the mutual fund to keep your money locked up so they could extract a gazillion hidden fees. Those of you guys listening on the podcast will also have a nice presentation slides. Hear that? If you guys want to go to the YouTube channel you guys can check out there or I will put this up on our retirement fund account page at simple passive cash flow calm slash q Rp. So again, that’s slash q RP if you guys want to check out the video there, but I got a special guest today, Jason from new view trusts. How’s it going, Jason?

1:20 Hey, Lane. How are you? Thanks for having me.

1:22 All right, so we’ve got about nine slides here. Less than 10 so people don’t go to sleep. But yeah, let’s quickly go over what the heck is a self directed IRA? And, you know, how can we use this to turbocharge our investing

1:37 share? Well, you know, you kind of hit on something. And I don’t know if it’s an old wives tale or if it is reality in terms of American history and the origin of the mutual fund. But I think we’d all agree, the financial markets as a whole are just not designed for the average retail investor unless they happen to get in and get out at the right time. And, you know, I think we’re seeing that out in the market today, you know, as we see it going up and going down and I read an article that you’ve got three different companies that are in the process of filing for bankruptcy that are up over 30% you know, which conventional wisdom would tell you you get out of a stock before they file bankruptcy, not get into them. And so what do we know is just individual investors, right? We’re all unfortunately left holding the bag. But as you mentioned, kind of the Vanguard’s the Schwab’s the fidelity’s, they’re in the business of providing retirement account custody, right, just like we are, but their business is to hold investments that are traditional stocks, bonds, mutual funds, Navy just exist in the same manner to hold investments that are not stocks, bonds, mutual funds, so we’re here to provide the same level of custody, but we’re allowing you as a client to pick your own investments to include things like real property or mortgage notes, private equity, right? All the passive investments, you know, that Lane talks to you guys about all the time. All of those can be done in an IRA and for those that are looking Looking at the screen, you know, we one of the things that we make clear from the get go is we’re not advisors, we’re not tax accountants, we’re not, you know, legal professionals, we’re custodians, we’re just here to hold your account, take your direction and hold the assets that you want. Self direction, gives you control. So the self and self direction means you find your own investments, you evaluate them, you do your own due diligence, and we go by and when you’re ready. So that’s really the role we play the role you play in the value, you know, to some degree of a self directed account. That’s right. We are here here for giving information and what do I know, right? I mean, I just bought some rental properties and quit my day job about 12 years later. And that’s what really upsets me about all that retirement funds stuck in these mutual funds. Like when I had a rental property, I was making like 30% a year when I was, you know, my leverage position was good, but then you look at my like the stocks and mutual funds like you’re making, what, seven 8% a year. It’s like where the heck did all my money go? And you look at these expense ratios and doesn’t it’s not all inclusive of all the He’s certainly right. I think what what is such a challenge for so many people and we hear it all the time is, you know, you charge me account fees, you know, fidelity doesn’t charge me account fees. And I think to myself, and I’ll sometimes say depending on the customer, you know, do you really think fidelity advertises on every possible television channel with all big buildings in town? Because they don’t charge you anything. You know, just because you go and you get a, a water for free or your drinks included, doesn’t mean you’re not paying for it somewhere, right? You’re paying a higher price on something. So you’re absolutely right. Mutual funds are notorious for for hidden fees and a lot of money gets raked out of those before an investor ever sees $1 in both good times, and bad.

4:45 Don’t get me started with financial planners, you guys can check out all the big rant page at simple passive cash flow calm slash. FP is one of those HBO comedy special videos in there too. If you guys think poking fun at financial planners, let’s kind of go through Some of this slide deck, Jason and then chime in with questions here. They’re the listener

5:05 perfect. Well, yeah, this is a slide that that I think really helps underscore. And it’s probably the thing that the story I like to tell the most in this. And if you can just leave that first one up for a second lane, and we’ll we’ll get to the kind of the grand finale here if, if it doesn’t pop up, but, you know, one of the things that so many people get focused on is they focus on investments, right. And, and naturally, we all do that, obviously, you’re, you know, you spend a lot of time talking about it. And and it’s so mission critical. Unfortunately, in the world that we occupy, what a lot of people step over is, can I buy the same investment in a different vehicle and yield better results? And that’s really what this slide is going to illustrate for you. I’ll kind of tell you the story. And so one of the things that happens right is as investors we look for the best investments, right? We assume that if we can just buy good investments, we can win the game. And I think it’s really two parts prior to that, and, and laying your story is so fascinating to me because you know, you didn’t have to go in and syndicate deals because you save the money. So you could be a passive investor, right. So you’re more successful as an investor because you had money to invest. And that gives people a big leg up. So we’re going to talk about the value of saving, and the value of saving in the right vehicle. So if you were to go out, and I’m just going to use a simplistic example. And again, those if you’re not, if you don’t have the slides that encourage you to go to the website and grab them, because it illustrates a little bit better, but just to illustrate how much taxes impact our investments, so if you said I want to go out and become an investor, and I’ve got $1, right, I’ve got $1 to invest and I’m going to invest it every year and it’s going to double year after year. So I’m going to invest $1, it’s going to become two I’m going to invest two, it’s going to become four, four becomes eight becomes 16. You get the idea. If you double that dollar for 20 years, right? 20 years $1 if you do that in a time taxable account, assuming there’s a 25% annual tax on your profits, you’re going to end up turning $1 into 72,000 bucks right now at face value, right? If you were to talk to anyone that turned $1 into 72,000 bucks, they look like a financial genius, right? And we’d all celebrate and we’d say that’s awesome. But what people overstep is what if I took that same dollar made the same investments that doubled every year for 20 years. But instead of having Uncle Sam partnering with me for 25%, or a little bit more or less, depending on your tax bracket, what if I simply put that money into a retirement account? First, let’s just say a Roth IRA. I paid tax on $1. Right, so if the tax rate was 25%, it cost me a quarter. And then I invested that money the same way I did outside of my IRA, doubling it every years, every year for 20 years, instead of $72,000. I’m going to end up with Just over a million dollars, right? So if everyone can kind of let that sink in for a second, same investor, same investment, same amount of time, one person made the investment with their personal money, the other person put it into a Roth IRA from the get go and then made all the same investments. One investor has $1,048,000 and the other investor has $72,000. Now, when I asked you what type of investor Do you want to be? The answer is so painfully obvious. And that’s what self directed IRAs do, is they allow you to take the investments that you’re making with your personal money today, and simply duplicated them into your IRA tax free. And obviously, the slide speaks for itself but the amount of money that you can make as a result is staggering. Not because you were a better investor, because you put it in the right vehicle and this is the exact reason

9:00 How we’re gonna pay for this all these stimulus packages, right? This is how the government makes money.

9:06 That’s exactly right. And the beauty of IRAs is it is a it is a tax free, tax advantaged account from the get go, meaning they’ve been designed this way since inception. So this isn’t a loophole that if you’ve got a good enough CPA or you’re wealthy enough to understand this is every single run of the mill investor can participate in this program, and it’s perfectly permissible and perfectly legal.

9:36 Well, it’s kind of a loophole, right? It’s the guys in Congress make these programs so they themselves can take advantage of them.

9:42 Well, this one’s interesting, right? Because, you know, what were the challenges is, it’s not whether or not you can do it, it’s whether or not you come across the opportunity and so many investors, you know, they just never learned that this is an option. Right? And, you know, we’ve been added I personally have been in this This business for 15 years, and we’ve been telling the story, and I can tell you 15 years ago, that people were telling the story to, you know, then is much different than today, right? 15 years ago, one out of 100, people even knew what this looked like, let alone how to do it. And now, probably 50 out of 100, people I talked to are at least familiar with it. So the message is getting out more and more people are turning to this opportunity, because it doesn’t make any sense to own an investment in your personal account, if you could own it in your retirement account and never pay tax on it. Right. I mean, that’s the beauty of, of setting up a self directed account. So when we talk about, you know, accounts, you know, I’ll just quickly highlight kind of how these plans work and the different types of plans that exist and I won’t get necessarily too deep in the weeds here. But, you know, a lot of times people kind of view retirement accounts as a one size fits. All right, there’s one plan, maybe two, and the reality is there’s not. There’s four different types of IRAs. So all of which you can park money into a traditional Roth IRAs Sep and as simple as Sep kind of being the unique one because it’s for those that are self employed HSA, for those that are on high deductible insurance plans, you can actually have an HSA and go self directed into passive investments, educational savings accounts. So for those with kids and grandkids, you can actually contribute to an ESA just like a Roth for your kids or grandkids and that money can all grow into whatever investments you choose completely tax free. And then you can use it to pay your your your kids, grandkids, etc. You can use it to pay their qualifying educational expenses. So not only can you use it to build retirement wealth, right, you can also use it to build tax free wealth for health expenses, and you can use it to build tax free wealth for educational expenses. And then the last plan the solo 401k the QR p if you will, that plan allows people to utilize the N q RP simply stands for qualified retirement plan. The q RP allows people to To take all the benefits of a so of a 401k plan, right, much higher contribution limits a lot more investor flexibility, etc. And you can do all of that inside a solo 401k plan and buy whatever investments that you want. So for those that are listening today are joining us, if you’re self employed, that tool is fantastic. Those that aren’t self employed yet, right? Maybe you’re taking kind of Lane’s approach, right, which is, you know, get some investments and give yourself enough passive income to to, to quit your day job. While you’re still employed. You may want to utilize some of these other tools that traditional the Roth solo, or sorry, the HSA, the ESA, we can walk you through that process and talk you through that. But key key takeaway here, everybody, is it, you there’s lots of different vehicles to save money. And if I go back to that slide of Dublin for $1, right? Well, what if you put $1 into a Roth $1 into an HSA and $1 in it to an ESA and you went out invested all three of those right and You doubled it $1 every every year, and you ended up with a million dollars in three different accounts, it sure beats a million dollars in just one account. So, lots to think about there. I don’t want to belabor it, and I don’t want to bore you with it. But I always want to share the value that that there are different plant types and a lot that have different levels of value for you.

13:18 And just for example, I’ve got it had an HSA account, and I put a coffee farm parcel in there. So I think what we’ll talk about some of the more exotic things you can invest in and then the a lot of a lot of my guys are doing a solo 401k is grps these days, and you know, they don’t necessarily run a traditional business. But, you know, there’s some ways around that. Of course, we’re not giving legal advice here. We’re just telling what other people are doing they’re kind of Thrive kicking butt.

13:45 So I you know, this this is kind of the the part where we talk about what are the rules, right? I mean, obviously the the government is not going to hand out tax free accounts without having some limitations and that makes sense. The biggest concern The government has really is, are you going to use this money to try to funnel or get money in or out either above the limits or without penalty. And so the IRS really has two sets of rules they enforce. Number one, you can’t buy life insurance and you can’t buy collectibles. Pretty straightforward and pretty easy, right? No Life Insurance, no collectibles. So this isn’t a tool to go buy artwork or you know, metals or gems unless they’re bought for their intrinsic value. But if you’re buying numismatics or you’re buying, you know, a painting or something, the IRS simply doesn’t let you do that in an IRA. There’s just too much stuff to try to manage market value in that. The second rule that they have is really less geared around what you buy and it’s more geared around who the IRA is tax free or tax advantaged entity does business with and in the case of a retirement account, they don’t want that that account doing business with you, your spouse, most of your close family members, certainly people above you and below you from a family tree. Right, your ancestors, parents, grandparents, your descendants, children and grandchildren. And business is owned by those parties. So what it says is my IRA could go invest with Lane, right? We’re not related as it as it as it is compared to this list. So my IRA could go do business with Lane tomorrow. So I could invest passively in a deal that that Lane was sponsoring, or I could I could buy a property that Lane was selling or whatever the deal was, but I couldn’t go do that. If Lane, you know, if I invested into with Lane and Lane was a child of mine, right? Because the IRS says that’s too close to the flame, we’re not certain that you’re going to be able to behave yourself in a in a, you know, parental with a child type transaction. So it’s not the deal that’s prohibited. It’s the fact that that our relation crosses the line, so smallest to people, right? The beauty of passive investing and what we’re really spending most of our time talking about is it’s exactly that right? It is passive If it is with unrelated parties, it’s mailbox money. And all of those deals, which we’re going to talk about here in a second are perfectly permissible in an IRA.

16:07 And what Jason is talking about is what we call the prohibited transaction. So we kind of self deal with ourselves. And what you’re kind of alluding to is pretty is it is actually pretty cool advanced technique that a lot of people in my mastermind do. what they’ll do is they’ll You know, they’re active investors but they’ll invest in their buddies deal with their self directed IRA. A lot of people will do that within the syndications to other sponsors and just can’t you got to make sure that like, you know, nobody gets married in the family right with it’s kind of like brothers in law. I don’t, I don’t know if you can do that or not, but maybe be careful may not be worth it. But you can’t actively be in you’re adding value to your your investment, right. Like if you own a rental property, you can’t be the property manager. You can’t trim the hedge, you can’t paint the property. You can’t fix anything. You have to be armed. Link transaction.

17:01 Yeah. And if you think about this in the stock world, right, it would be like, you know, the IRS doesn’t want Bill Gates buying Microsoft stock in his IRA, because they don’t want him having tax advantaged opportunities to grow money of a business that he controls, right. But there would be nothing that would prevent Bill Gates from investing into apple. Right? Because there’s no related party there. Even if he is great friends with Tim Cook and understands everything about Apple’s business model. It makes him a good investor. And there’s nothing prohibited about that. They just don’t want him investing into his own business or doing anything that gives him that sweat equity as you kind of alluded to. So you know, this isn’t necessary. This is far from a deal breaker. In fact, I would suggest if this catches you up, you’re probably kind of missing the true intent of really passive investing. But this is a you know, we got to follow the rules. And if we want to have the tax benefits, we gotta follow a real small set of rules.

17:57 Yeah, some some of the more fun techniques I hear about whether it’s legal or not, is, you know, like, note investors, they like peel off though, you know, they they make it like they’re investing $1 they peel off all the future payments is, you know, added value, and that’s how they turbocharge their self directed IRA. I mean, that’s how like, was it Nick and Romney had like a gazillion dollars in this self directed Roth, and like, you know, how the heck did he do that when you can only put in $6,000 a year right, either doing tricky things like that. But you don’t have to comment on that. Jason. I mean, that’s what we’ll have to come

18:34 to Hawaii. Best. I I don’t I think the way that I will. I will, I will. Just and you know, the beauty is of a self directed account is you are limited by your own creativity. And, you know, certainly that creativity should fall within the bounds but there’s a lot of strategies to turbocharge investments and, and find ways to really have some high profit, especially as a percentage type investments inside accounts. And as long as you’re not, you know, breaking either these rules that we just talked about, you’ve got an infinite opportunity. And you know, I love hearing stories like that, assuming they all fall within the legal realm because it’s exactly it and people like Mitt Romney don’t have to be the ones that can you know, it’s not meant for wealthy people like meant to be able to, you know, turbocharged the average mom and pop investor has that ability through an account with new view.

19:29 Jason just sells the motorcycle and it needs all

19:33 regulations, but do you want to go do some wheelies? That’s on you.

19:39 Are you a non accredited investor looking for opportunities to invest passively? How about a newer investor looking to get a bit of a track record and confidence from your spouse

19:47 who’s a little bit skeptic of what you’ve been listened to the last few months and could use the reinforcement of double digit returns paid like clockwork in the form of monthly dividends, the American Home preservation fund or a SP is currently open again, and it’s looking to bring new investors with them. I have been investing with them since 2016. And originally I use it as a means to pay for my regular expenses. I started with $60,000 as my initial investment and that paid my car payment completely for me every single month, he collaborates with existing homeowners to keep them in their homes via restructuring or selling the depths. Unlike their competitors, it’s a way to make great returns while feeling good about making a social impact. After investing myself in the fun, it was awesome when owner George Newberry saw the impact simple passive cash flow was making and eventually approached me to become a spokesperson for the company. You can start investing with as little as hundred bucks. And if you want a fee burdensome book, please send me an email at Lane at simple passive cash flow calm. For more information about investing with hp, go to HP servicing.com slash investors That’s like, going back to that what your IRA cannot invest in? Does wine fall in that category?

21:09 Believe it or not, alcoholic beverages is actually a line item under collectibles and IRS code. So, yep, wine in any other alcoholic beverages for the same reason you can’t hold a painting. Okay.

21:23 You can’t directly on artwork, but there are operators out there that will syndicate it. And but I know you can do it that way. But I think that’s where if you’re getting enjoyment out of the actual painting in your gallery or in your house or a wine that you could potentially tap and fill with purple water. That’s where they draw the line, right.

21:46 You know, that as the custodian who gets to hold all the assets right on behalf of the accounts. You know, it’s a bit disappointing that we can’t hold the artwork and wine and alcohol on behalf of our clients. And you know, I I think we all have a little experience when we were younger, figuring out how to refill the liquor bottles, at least certainly I know me and my friends did in our respective, you know, parents liquor cabinets. But yeah, it’s prohibited and you know, really laid what what, what their biggest concern is candidly is it has to do with market value and investing into a fund is investing into a business, right, and the fund managers are responsible to oversee the activity. And it’s a little bit different. If you own a Picasso in your IRA, how would the IRS ever know what your tax liability is? Right? So if if you decided to withdraw that Picasso painting from your account, which is perfectly permissible? How would they know if that’s valued at 1,000,002 million 10 million or 100 million and obviously, as a taxpayer, you’re going to try to get that valued at the lowest amount possible to limit your tax. So that was really their intention from the get go is, is obviously a personal use and personal consumption and that’s certainly a large country. Reading factor, but it also goes a step further into the behavior of the the account holder. And from a tax liability standpoint,

23:08 that’s always kind of playfully push the limits on this because it helps you understand, right? What is the intention and essentially Congress there, you know, they got to keep all US monkeys in line, so they got to draw the line somewhere. That’s right. But what about gold Boolean is that Can you can you own that in your IRA

23:27 IRA. So any precious metal, right, whether it be gold, silver, platinum, palladium, they can all be held as long as they are above purity levels. So for all metals, except for gold, because it’s a little bit softer, more malleable. The requirement of purity is point 995 for gold and point 999 for all other metals. So if you wanted to invest into Golden Eagles, let’s just say, as long as it in a golden eagle does meet the criteria to Treasury, you know, it’s a government issued and it’s not domestic, you can buy Canadian Maple Leafs and other things. But as long as the coin that you’re buying, even if it’s unmarked, has to meet certain refinery guidelines and be above the purity level. So what you can’t do is you can’t go buy a piece of gold from the Titanic, because you’re buying it for its numismatic value or its collectible value that’s prohibited. But if you bought a just, you know, one ounce gold coin that was met the refinery requirements and was point 995 percent pure above that it would be perfectly permissible.

24:35 Again, it comes back to Mike Kennedy, the market value be verified. You got it on it.

24:41 Yep. All right.

24:43 What about Bitcoin?

24:44 Yeah, Bitcoin can be held. There’s a few different ways to access it but cryptocurrencies of all different types can be held and, you know, we can set help you set up your account where you can actually go designate your own storage. Find your own, you know, Whatever crypto you want to buy, whatever the platform you’re using to buy it, whatever platform you want to use to hold it, and you can manage all of that, on behalf of the IRA.

25:10 I’m not a big fan of crypto unless you got a lot of money more than half a million dollars to play around with it. Nor am I big fan of precious metals I just think that’s what all like the Guru’s out there trying to scare people that the world is ending so they can get their Commission’s on both gold and silver Booleans. But hey, who do I know? I mean, might work. I just don’t do it. But let’s, you know, also my folks are interested in like the real estate side, whether it’s a syndication or LLC, if you can kind of expand on what people are using for that.

25:43 Sure. So So I’ve got two slides on that. And you know, before we talk about kind of the the passive approach, you know, your your IRA can own really anything that’s not prohibited. Well, what are the most common things our clients own Really it boils down into three asset classes. And all three are pretty close to the same in terms of percentage of assets. So, real estate, and this is all different types of real estate. As you can imagine, mortgages and notes, right performing non performing, it doesn’t matter, they all fall under that mortgage note, basically a loan of some sort. And then private equity and private equity covers a pretty big range, if you will, but that’s partnership deals, whether they’re, you know, whether they’re, they’re just straight passive investments or whether or not it’s private stock investment, like an active business. All of those can be held LLCs, obviously, and then we have the other category, right? And that’s the probably 10 or 15% of what we do, or what our clients do. Precious Metals falls into that cryptocurrency, tax liens, tax deeds, tax certificates. You know, we’ve we’ve got clients that have invested in race horses. We’ve had You know we’ve seen it if you can imagine it I think as it farmers it says we know a thing or two because we’ve seen a thing or two. Man we we’ve seen a thing or two, that’s for sure.

27:12 Now hands down, it’s kind of inspiring. What if I wanted to buy like one of those five or $10,000 like purebred Eagles or something like that, or like one of those like exotic cats that celebrities own like a, like a hybrid Lynx?

27:28 Sure, I mean, so long as you there’s really a couple key things. Number one is your clear ownership paperwork, right? And for a lot of these including a racehorse, yes, you cannot store it yourself. Right. So you can’t bring it to your property. And you know, for the racehorse, for example, it needs to be stored somewhere. You have to be hands off. So in the example of the racehorse or in your example of we’ll call you lane exotic you know, for free You’re some sort of Tiger, right? You could you could do it, your IRA would buy it, your IRA would pay whomever housed it. If there was training or anything that went in, you know, that that was involved, all of that would be paid for out of the IRA. And you could get this to a point where it was ready to be sold, and you could turn and go sell it, and the profit would go right back into your IRA.

28:22 What if I just want it for a lifelong friend?

28:26 That’s prohibited that’s prohibited, it’s prohibited you cannot take physical possession of anything in your IRA. So you you got to have it held somewhere else you can FaceTime it, I suppose.

28:37 Even me out of jail.

28:41 So, you know, I one of the things I wanted to just maybe kind of wrap up on is really the the passive investment side and, you know, when we say the passive investment, right, I mean, it’s the key difference between active and passive, at least the way I try to kind of view it is active means I’m going to go out and actively find the deal. So If I want to go buy a rental property, I’m gonna go find the rental property. If I want to go right alone, I’m gonna go right alone, right? passive investments say, you know what, maybe I’ll rely on someone else’s expertise here. I will let someone else that that knows how to find the right rental properties, go build a portfolio of rental properties and all invest into that. And, and what I’m getting is two big things, right? I’m getting knowledge and experience from the person that’s creating the opportunity, but to I’m getting some diversity, right, because I don’t have enough money in my IRA to go buy 30 investment properties, I can go buy one or two. And then, you know, if one doesn’t read, obviously, I’ve I’ve lost some real diversity there. But if I own 2% of a pool of 30 properties, now I’ve gotten some real diversity in my investments. So passive investments are something we see our clients do. Really probably the most common thing our clients do. When we talk about, you know, passive real estate, obviously you have multifamily funds, you’ve got rental funds, you’ve got You know, low income housing funds, you’ve got affordable housing funds trailer park, mobile home, you know, type funds syndications. So you know, anything that’s that’s syndicated and syndications is doesn’t always have to be real estate, right? We see all kinds of things that are syndicated from an investment standpoint, you know, all the way down to ATM machines, right? as something that could be syndicated mortgage and note funds. So you may not want to be in the business of going out and figuring out who needs to borrow money, but you like the passive income that alone offers and so you can go out in the marketplace and find people that will write the loans for you and find the borrowers and negotiate all the terms. crowdfunding, you know, this is something that is becoming increasingly popular and, you know, crowdfunding gives you the ability to hop onto websites, right and take a look at at some of those offerings right on a website. You know, Which, which is really was created by the JOBS Act, you know, some years ago, and it’s really made a major impact because it’s allowed a lot more, it’s allowed a lot more access to private investors, you know, to access some of these true private investments. Because in the past a lot of the investments we’re talking about, we’re really only available for the wealthy, right? It’s why mitt romney’s you know, investment funds delivered such great results to his wealthy friends. Whereas, you know, crowdfunding gives Joe sixpack right the ability to kind of log on to the website, they got to do their own due diligence, but it gives them access to some of these more attractive, fun level deals. And then private equity and other investment funds. So, you know, the the world of private equity is huge. I mean, you know, Uber Lyft grubhub. You know, if you look at all these companies that we all know of, every single one of them started as a private equity company before it became public. And a lot of these private companies raised money and so There’s, you know, obviously the, we’re not getting calls to invest in Uber, but you’d be amazed how many businesses that that people, you know, maybe operating or starting and sometimes just asking around will give you some insight into some of these products. And so all of those opportunities present themselves.

32:17 So, you know, Jason works for new view, their self directed IRA company, and something I’ve heard lately from investors, I’m talking on the phone, which I still do these days if you guys are new investor to or if we do a pipeline club, go ahead and book a call and we’ll get to know each other a little bit better. But you know, people are like, well, I got it. I got I’m in the self directed IRA account with fidelity or Vanguard. I’m like, Great, that’s a fake self directed IRA. It’s this self directed term has sort of become a little buzzword. I feel like this past year. And the Vanguard’s and all these big brokerages are just calling it that but it’s, you’re still trapped. It’s like you’re in a prison. You just get privileges to go walk around the field but just make no mistake you’re still stuck in the in jail. Guys like Jason with a new view IRA, they are outside of the the jail cell or the jail community. And they are truly self directing accounts. And then if you want to add on to that, Jason but

33:24 yeah, and I gotta I gotta say publicly I love the the prison example because it’s so true. And, you know, if you’ve never been outside the prison walls, you think you’ve got it really good, right? You know, I typically analogize it to imagine if, if the only fast food available was burger chains, right? Yeah, you didn’t know there was such thing as Taco Bell or or chick fil a or, you know any of the other myriad of choices. And so you may think, yeah, because I got Burger King and Wendy’s and McDonald’s, man. I’ve got a lot of real choice here and each menus got a bunch of different things on it and all of a sudden Well, and then you step foot in into a taco bell or something else and realize, well, gosh, you know, this is a whole different menu with a whole different set of opportunities and self directed accounts. You’re right. It’s a term that’s gotten, you know, really kind of used over utilized because it was designed originally to say, Hey, we’re giving you the ability to make your own investments into investments that that you get to choose whereas, unfortunately, we’ve seen you know, a lot of the large brokerage houses that said, Hey, wait a minute, we offer self directed IRAs to you can pick whatever stock bond or mutual fund you want, right? And

34:36 in our in our amongst some crappy options that we That’s exactly right.

34:39 And, you know, so so new trust is is really designed to give people choice and freedom. We are a passive custodian, as I mentioned at the beginning of a city about a billion and a half dollars of assets, over 17 years of business, and people call on us and ask us and trust us to simply provide a similar role that fidelity would provide or Schwab would provide, but they do it under the auspice that they’re going to go find their own investment, do their own due diligence and not be forced into the stock market. I mean, that’s really why people come to new view.

35:12 And I thought you’re gonna go a different direction with that now and see and talk about the shower scene with the soap. How you’re getting out of paying all those fees, right.

35:22 Oh, man, you know, and we may have to talk offline on how to build on that prison analogy. There’s this sounds like there’s some opportunity there.

35:29 Yeah. Well, I’m with the final minutes here that I have with you. Can you talk about UDF fi and, you know, those are going into investments utilizing leverage?