Its reality (and a little morbid) that your parents are aging you be one of the main caregivers. If you reading this they you understand the saying “sandwich generation” squished between taking care of kids, a demanding career, and aging parents.

I have had calls with investors who have had their parents give a greatly appreciated property before death (losing all the step up basis tax advantages) or give an asset to only to have a person get injured at the property and now everyone in the family is on the hook for the lawsuit.

How can we plan for this proactively and strategically without falling victim to traditional methods (taxes and a commission based financial planners).

Its definitely and emotional time with a money on the line… like wedding planning… yikes!

Taking Status

Although you came from the same DNA strain and upbringing you will be surprised on what is behind the financial status of our parents. Going in with a non judgmental mindset enables you get the truth and arrange a mutual plan.

Start by gathering the following:

Bank statements

Investment portfolios

Passwords associated with these accounts

Safe deposit boxes

Outstanding loans

We have all coaching clients download and complete this personal financial sheet which help facilitate conversations.

It’s not as simple as die with less than $22 million in assets. We can help with our Family Office consultation to navigate the complex situations of designing a game plan.

Where are we?

See where the money is coming and going. Inventory current bills and whether or not those are being paid on time.

Run credit reports with Equifax, Experian, and TransUnion. Be kind when understanding that your parents will have the traditional mindset to debt than you.

Inventory social security, retirement accounts, real estate, and cash.

Medical

Inventory medical history and any current medications they’ve been prescribed. Automate appointments and get involved with the relationship with their health provider.

You may consider the power of attorney (POA) should they become incapacitated. Even if they are in good health you should have a trust setup. Let us know and we can refer you to someone we trust. A will is not acceptable because it will go into probate.

A will is not acceptable. Get a trust setup to avoid probate and giving up 2-10% of the estate value to lawyers. Smart lawyers who create wills for you know its guaranteed work for them ($$$) in the future.

Familiarize yourself with long-term care which is designed to help pay for chronic diseases and disabilities. The money can be used for medical to non-medical activities like bathing, eating, and dressing, assisted living options as we will discuss below, as well as skilled care by nurses or other professionals.

Not to scare you or feed into a insurance broker’s ploy but:

The department of health and human services says that those who are age 65 today has a ~70% chance of needing some type of long-term care services. And those aged 55-60, only 5% of them have long-term care coverage. The cost of coverage can be $2000-3000 per year.

Based on Social Security Administration info, the average lifespan of a man who has reached 65 is around 84 and for a woman who’s reached 65 is almost 87.

Learn your parents’ wishes regarding the type of care facility they would prefer based on their (and your) financial situation.

Would they want to live with others while they still can get around or would they rather live in their current home until they break their hip and can barely use the restroom themselves?

Check their insurance coverage and what the government will and won’t pay for relative to Medicare benefits. Here is where it would require a tax/legal professional (not your typical tax guy) to advise you how to equity strip your parents to quality for the most coverage while gifting off as much assets as you can.

Clients who engage in our family office and coaching clients may reach out for assistance with these issues and get setup with our best advisors.

Accessory Dwelling Unit (ADU) Option

You parents might be find going to an assisted living facility or “old people home,” however they may not have the funds to do that or you may prefer to have them nearby…

… but not too close.

One solution maybe constructing an Accessory Dwelling Unit (ADU) on your current property. One advantage to this is that you can have free childcare in the backyard and forge a stronger relationship between your kids and their grandparents 😁

Matt, and I met a few years back when we were starting to invest in apartments. Having the right network is critical and its important to grow with people. Make no mistake this type of investing is high risk high reward but it’s a whole lot of fun. When I build my base of cashflowing Class B and C apartments I will look to trophy assets like these.

You can invest as a partner in on all kinds of things… even Broadway shows!

Capitulation budget to produce the show (staff costs, set costs, etc)

$8-$10 million for a lower budget but this can go up to $20 million.

Recoupment schedule (assumptions on ticket prices and demand) – Hoping to get back money in 6 months and hoping to tour for a few years.

500-800k costs per week.

Leverage is low in comparison to real estate investing but this is a high risk!

4/5 shows don’t make it past initial run

Do it for fun and because you love the art!

But…

If a show is very popular you could be involved in the tour. Think of it of a phase 3 portion of some past assisted living and RV Park developments.

http://mjppg.com/about-us/

Erica Lynn Schwartz

Erica Lynn Schwartz is a Tony-nominated performing arts professional with a wide

variety of theatrical development and production experience.

Erica has over 15 years of experience in Live Entertainment including producing

Broadway shows. Her Broadway producing debut was Neil LaBute’s Reasons To Be

Pretty (TONY, Drama Desk & Outer Critics Circle Nominations for Best Play) and she

is currently a co-Producer on Moulin Rouge! The Musical. Erica has invested in several

shows including the smash-hit Hamilton and an international tour of Wicked.

Erica has worked on several Broadway shows including Wicked, The 25th Annual

Putnam County Spelling Bee, I Love You, You're Perfect, Now Change, Movin'

Out, Doubt, and Hairspray. She ran the licensing, booking and touring division of

Daryl Roth Theatrical Licensing, lead a $25.5 million capital campaign for MCC

Theater's newest complex and managed the reopening of Lincoln Center’s Alice Tully

Hall.

Erica is a graduate of Northwestern University where she holds the honor of being named

a Distinguished Alumnus in 2008. She is currently the General Manager for the Emerson

Colonial Theatre in Boston, Massachusetts, where she resides with her husband and their

two daughters.

For more information about Erica and Avalon Road Productions, please visit

www.avalonroad.net

Matt Picheny, PMP

Matt Picheny is the Managing Partner at MJP Property Group, a real estate investment

company. He has been involved in single family, multifamily & vacation rentals for over

13 years.

Matt has experience in property valuation, acquisition, new construction, rehab projects,

property leasing, management, financing and is a Fannie Mae approved buyer. With an

investment portfolio of over 1,350 units, he is primarily focused on acquiring and

repositioning multifamily communities.

As a PMI certified Project Management Professional, Matt has a proven track record of

delivering projects on budget, on schedule and at the highest quality standards. He is a

marketing veteran whose 20-year New York City career spanned several of the world’s

largest advertising agencies, producing award-winning projects for Fortune 500 clients

including Verizon, IBM, and Coca-Cola.

For more information about Matt and MJP Property Group, please visit www.mjppg.com

Once you have gone through the majority of podcasts feel free to sign up for a chat – Also to get into my projects please setup a call because we need to have a pre-existing relationship.

Setup a call here: https://calendly.com/simplepassivecashflow/20/

SimplePassiveCashflow.com is for working professionals who are looking for diversification and better returns outside of traditional investments such as mutual funds and stocks.

Check out my Free Resources Below:

1) The Hui Deal Pipeline Club is a free investor club where I filter investments and underwrite the numbers and partners myself.. Unlike other investor lists and groups, my investors have personal access to me and know that I personally have skin in the game investing alongside with my investors. Make sure you sign up for my Hui Deal Pipeline Club to get sent the deals I come across:

Simplepassivecashflow.com/club

Mastermind Club: If you or someone you refer invests at least $50K into one of my future deals you will be invited to my exclusive Ali’i Mastermind with other 12-20 other serious investors to discuss deals and our own portfolios. For more details: SimplePassiveCashflow.com/mastermind

2) Join a Social Club:

Note Investing: https://www.facebook.com/groups/noteinvesting/

Seattle: https://www.facebook.com/groups/SPCHUISEA/

Hawaii: https://www.facebook.com/groups/SPCHUI808/

Portland: https://www.facebook.com/groups/SPCHUIPDX/

Bay Area: https://www.facebook.com/groups/SPCHUIBAY/

So Cal: https://www.facebook.com/groups/SPCHUISOCAL/

East Coast: https://www.facebook.com/groups/SPCHUIEAS/

Central USA: https://www.facebook.com/groups/SPCHUICUS/

3) Subscribe to my podcast on iTunes or Google Play.

Google Android Phones: https://playmusic.app.goo.gl/?ibi=com.google.PlayMusic&isi=691797987&ius=googleplaymusic&apn=com.google.android.music&link=https://play.google.com/music/m/Iizwgws56nif7jllsr5zqk74gh4?t%3DSimple_Passive_Cashflow_Podcast%26pcampaignid%3DMKT-na-all-co-pr-mu-pod-16

Apple iPhone: https://itunes.apple.com/us/podcast/simple-passive-cashflow-podcast/id1118795347?mt=2

Youtube: https://www.youtube.com/channel/UC3cIIsGKx3osVU5rt2P0HfQ

Stitcher: http://www.stitcher.com/podcast/lane-kawaoka/simplepassivecashflowcom-podcast

Spotify: https://open.spotify.com/show/1TrHc3fc8ZGw4mX3yK76rS

iHeart Radio: https://www.iheart.com/podcast/simple-passive-cashflow-podcast-29238009/

4) Need a legal, insurance, Virtual assistant, CPA, or other referral?. Shoot me an email Lane@simplepassivecashflow.com with a short bio.

5) Please leave a review for the podcast!

http://getpodcast.reviews/id/1118795347

6) Coaching Program to get you to your first rental in 90 days!

simplepassivecashflow.com/coaching

7) Summary of every Simple Passive Cashflow Podcast: https://docs.google.com/spreadsheets/d/1gJc_p0RCKUPlKRiF17FgtXvcIkvZS-iHjGNo8Vts3K0/edit?usp=sharing

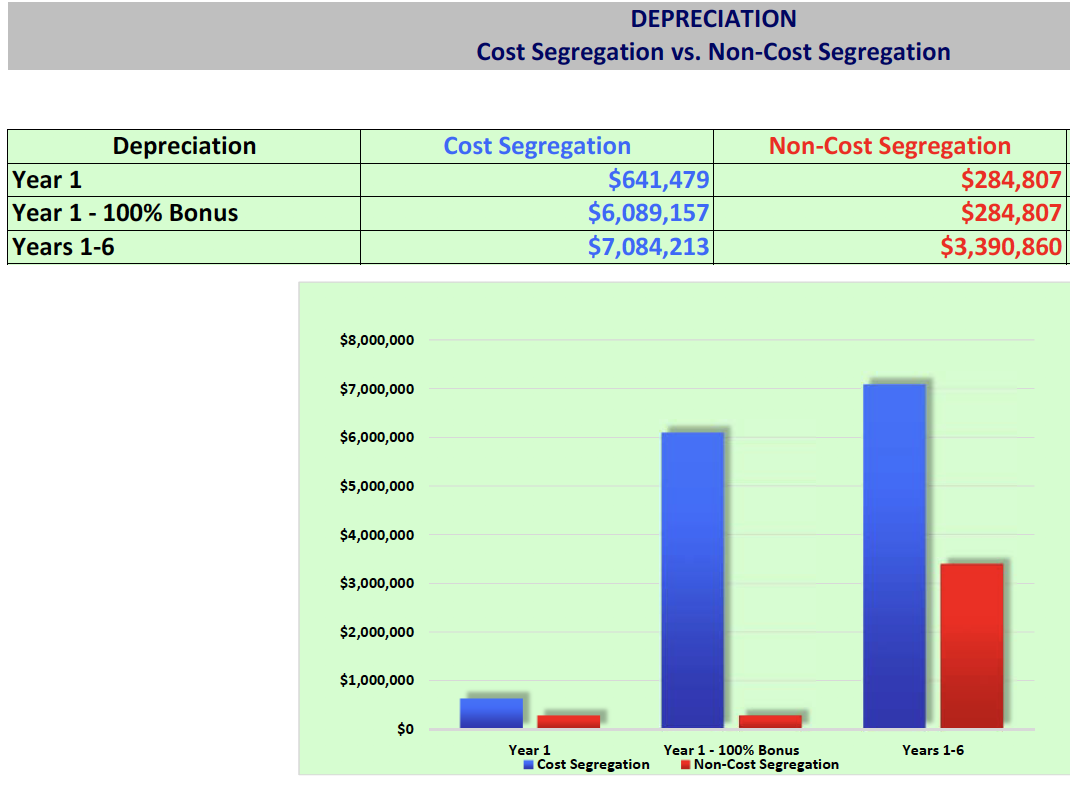

As a real estate investor, imagine using Cost Segregation as a real property investment strategy that will grant you tax free cash flow from fixed assets and allow you reinvest even more (and possible lower your ordinary income).

What is Cost Segregation?

This is one of the easiest and fastest ways to squeeze a little extra profit out of an investment. If you have ever played those racing video games where you modify your car (like Gran Turismo) it’s like paying for that cheap computer chip upgrade to get an extra horse-power boost, it’s a no-brainer.

For those of you who aren’t ex-gaming nerds like me, it’s “low-hanging fruit”.

A cost segregation study gives a tax benefit to the taxpayer to take advantage of current bonus depreciation laws (starting to phase out slowly in 2022) in order to depreciate their assets by taking a loss on paper.

The cost segregation specialist/engineer analyzes the components of a commercial real estate asset to create a cost segregation report to equip the tax accountant or CPA the needed breakdown of the asset in order to make the depreciation determinations.

To better understand the benefits of performing cost segregation, you must first understand depreciation.

Depreciation is where you reduce the value of your assets (in this case, your real estate properties) due to natural wear and tear over time. There is a type of depreciation wherein the value of your fixed asset (real estate properties) depreciates faster than it should be. This speedier depreciation or most commonly known as accelerated depreciation.

Let’s look at it in detail: If you own commercial or residential real estate investments, you can depreciate your real estate holdings. A commercial property establishes a 39-year depreciation schedule and a residential property establishes a 27.5-year depreciation schedule. These are the numbers we will use to calculate the rate of our depreciation deduction.

Above link is for smaller assets. Larger assets will likely require other vendors that we use on our assets. Join the club for access.

Real K1 from a past dealReal K1 from a past dealReal K1 from a past deal

Above: Example of a cost segregation estimate for a past deal

Below: Another estimation of regular depreciation vs the more aggressive deprecation timeline (what is coined as “bonus depreciation”)

Envision a 3 bedroom single-family home in Birmingham, Alabama that is worth $100,000. Of that, approximately $65,000 is determined to be the building value and $35,000 is determined to be the land value. Each year you can deduct 1/27.5th of the building value, which is about $2,363 a year that can offset income gains. $2,363 can be taken for the next 27.5 years until all the value on paper is depleted.

Is there a catch?

Unfortunately, you cannot deduct the value of the land unless you have made a land improvement, granting that the improvement you made has a “useful life” that is depreciable. Only the improvement will be depreciable, not the land itself.

https://youtu.be/tlI83umq-DE

When you sell the asset you will need to recapture the depreciation. This is the major disadvantage to a cost segregation.

We pay $8000-12,000 on our larger commercial assets to do a cost segregation and our advisors tell us that the general rule is to do a cost segregation if we intend to hold onto a property more than 3-5 years because if we sold quicker than the time benefit to the passive losses we got as investors you be less and might not be worth the price of the actually cost segregation study.

But, guess what?

There are some exciting new benefits to passive losses since Mr. Trump enacted a tax law where 100% Bonus Depreciation creates substantial benefits on your taxes for the acquisition year. In the future, us investors are crossing our fingers that this part of the tax code sticks around.

Paper losses from single family homes

Previous

Next

Think about this: My $3M, 52-unit apartment, is looking to get more than $266K in tax savings (at 37% tax rate) in the first year of ownership by doing a cost segregation.

If you are interested in learning more about how to best utilize your passive losses, you can learn more here.

Companies and investors who have constructed, purchased, expanded, or remodeled any kind of commercial real estate (including 1 to 4-unit residential rental properties) since 1987 can use cost segregation studies for maximize their tax savings.

The study allows the owner to take advantage of accelerated depreciation deductions and defer federal and state income taxes on the reclassified building components mentioned above.

A team of real estate investors evaluates several personal properties, residential rental property, and land improvements that can be upgraded to improve the value of the property. Those improvements are assessed with the assistance of a Cost Segregation specialist. After completing this cost segregation analysis, the property owner may deduct the depreciable life of the individual fractional interest (IFI) through a cost segregation study, with or without depreciation. If the taxpayer is eligible and has not failed to take advantage of the tax rebate, the taxpayer may claim the expense directly within the given year of the seller’s ownership.

To elaborate more on Accelerate Depreciation Deductions, it is a deduction of the cost you pay to a person if you own your personal property assets. The accelerated depreciation deduction provides significant tax savings but it is not another type of benefit. The exchange of property owners whose benefit is primarily from cost segregation is a limitation in tax savings. The depreciation expense is deducted at the source rate in another year.

What are the Benefits of Cost Segregation?

Lower Property Insurance Premiums

Since it generally costs less to insure personal property, versus real property, building components reallocated as personal property should reduce your insurance costs as well which will yield potential benefits in the end.

Capture Retroactive Savings

Since 1996, taxpayers could capture immediate retroactive savings on properties added since 1987. Previous rules, which provided a four-year catch-up period for retroactive savings, have been amended to allow taxpayers to take the entire amount of the adjustment in the year the Cost Segregation is completed.

This alone is huge!

This opportunity to recapture unrecognized depreciation in one year presents an opportunity to perform retroactive Cost Segregation analyses on older properties to increase cash flow in the current year.

What Components Can I Reclassify?

Components of a specific property or qualified leasehold improvement are identified and reclassified for depreciation over a shorter time (5, 7, or 15 years). For example, 30% to 90% of the total electrical costs in most buildings can qualify for 5 or 7-year depreciation.

5- year tax-life components

Non-structural elements: carpet, decorative lighting and trim, HVAC systems, dedicated electrical and plumbing, and security systems.

7-year tax-life components

All telecommunication related systems: cabling, telephone, etc.

15-year tax-life components

Exterior land improvements: landscaping, curbs, sidewalks, fencing, and signage.

As a Passive LP investor the details of this is not needed as all you need to ensure is that your sponsor is aware of cost segregations to optimize tax benefits.

What is required to have a study done?

You need to provide as much of the original documentation pertaining to planning, construction, and current tax depreciation as you can.

This could include a complete set of:

Construction plans

Current tax depreciation records such as tax returns, building cost budget information, final AIA (American Institute of Architects) appreciation

Document of certification of payment or other cost information, change orders, direct or indirect costs paid by the owner that are not included in other documents

Other information depending on the project

How much does a Cost Segregation Study cost?

On average, the total fee will generally fall between 5% and 20% of the estimated net present value tax saving. You can often get a free preliminary analysis to help determine this. This can be impacted by how large or small the real estate project is.

In addition, the location, accessibility, and quality of the records and documents will impact the entire cost (costs typically range between $8,000-$12,000). Minimum fees can be as low as $2,000 for small projects, and some firms GUARANTEE a minimum of 500% ROI (fee vs. tax recovery) on projects over $500,000.

Cost segregation studies are typically cost-effective for larger syndication buildings purchased or remodeled at a cost greater than $100,000. Acost segregation study ismost efficient for new buildings under construction, but it can also uncover a retroactive tax deduction for much older buildings as well.

What are the steps involved in the process?

First off… if you are a Passive Investor (LP), your sponsor should be taking care of cost segregation for you so you will have one less thing to worry about.

If not, the cost segregation process can be broken down into the following steps from start to finish:

Step 1

Vet Cost Segregation Firm

Engage a reputable Cost Segregation firm that utilizes engineers and architects trained in Cost Segregation and it’s application to the proper allocation of assets. If you need a referral go here.

Step 2

Document Review

The engineer determines what documents are available (e.g. planning, construction, invoices, appraisal, and current tax depreciation) for reference and referral.

Step 3

Schedule Property Survey

The engineer then sets a schedule for surveying the subject property and gathering the available documents for review prior to arrival at the subject property.

Step 4

Document Recreation

For those documents that are unavailable, time is then scheduled into the Cost Segregation process for document recreation using known industry standard costing data (Marshall & Swift and/or RS Means costing publications). The process takes about 4 to 6 weeks after all necessary documents are acquired. The time that a Cost Segregation Study takes depends on the size of the project and the completeness of the documentation that you can supply.

Step 5

Conduct Site Survey

The site survey is executed and completed. Surveys can be completed within as little as an hour, but it varies between each survey. Measurements are taken and all areas are photographed for IRS verification and substantiation of asset values during the survey.

Step 6

Calculations

The engineer returns to the office and crunches the numbers. The number crunching process is when all documents are reviewed in detail, assets are verified, and measured against known costing data, and asset reallocation is applied.

Step 7

Review

A review committee then examines the results of the analysis completed by the engineer of record to verify its veracity and confirms it meets and exceeds IRS guidelines per the Cost Segregation Audit Techniques Guide.

Step 8

Compile Report

Once approved, the study results are compiled into a final report that includes: all IRS tax code to substantiate the reallocated assets, spreadsheets identifying all assets categorized according to their building codes, representative photographs of the reallocated assets, and the engineer’s credentials for IRS review.

Step 9

Issue Report

The final report is issued. The client and CPA of record receives digital copies via email, for application to the client’s tax return.

When Should Cost Segregation Be NOT Considered?

There’s an attempt to sell within within 5 years

Not being able to use the losses- planning 5 years ahead and looking back 5 years for taxes; income isn’t enough or PAL restricted.

No savings of at least 2X cost of study (not depreciation but the existing cash savings)

Be wary of 1031 exchanges- there are 2 ways to calculate the depreciation to carryover

5. Check that the federal 1031 doesn’t open you up to exuberant state taxation on the state 1031. Note: Many states do not follow federal guidelines for depreciation and personal property ineligibility.

6. Discern if 179 expensing method is a better option (due to presence of limitations)

7. Possess your real estate in S Corps due to many reasons: basis and step-up

Cost Segregation Example #1

Depreciation is distributed to investors on the K-1 Form in syndications.

Not making any promises as depreciation amount is primarily based off building specifics and the amount of leverage used in a deal, but here is a real-life example from a $50K LP investment in a Class C apartment syndication in the first year K-1 in 2018 which yielded a $36K paper loss by utilizing a cost segregation. Extract 10-20x what you normally able to deduct in the first year alone! Take these passive losses and employ the “Simple Passive Cashflow Gravy Train” strategy where you offset your ordinary/W2 income with real estate professional status. For more details on that check out our Master Tax Guide.

I paid 4% in taxes in 2018. All because of the passive losses that real estate gave me.

Previous

Next

If this is a new concept to you, you may be able to go back to previous years taxes and get back some benefits this year. Oftentimes, getting a quote is free and quick.

A recent quote I got back for a few properties:

Previous

Next

Cost Segregation Example #2

We purchased a $20M apartment and are about to write off $6M in the first year! The total capital raised from investors was $5.5M, that meant almost a dollar for dollar deduction in year one!

Cost segregations are not new. On the contrary, they have been in existence since 1954, when the IRS allowed for certain personal assets to be accelerated into a shorter life class. However, it wasn’t until Hospital Corporation of America sued the IRS in 1997, and won, that the IRS revisited the issue of accelerated depreciation. The IRS ruled that property qualifying as tangible personal property under the former Investment Tax Credit (ITC) rules, would also qualify for purposes of federal income tax depreciation under MACRS (Modified Accelerated Cost Recovery System).

The IRS Chief Attorney wrote a memo saying, “. . . Cost Segregation, for it to be properly applied, had to involve those with competencies in architecture, engineering, or construction and/or construction techniques, in order for personal property assets to be accurately identified and segregated.” As a result of this memo, cost segregation became a viable tax-saving strategy allowed by the IRS.

CPAs are not qualified according to the IRS guidelines. However, most Cost Segregation firms will gladly work with them on a consulting basis to complete the work for you. Remember, the IRS Chief Counsel issued a memo that made it clear what constitutes proper “methodology” in applying Cost Segregation, and it must be done by people who are competent in architecture, engineering or construction and/or construction techniques. You will want to ensure you are working with a cost segregation specialist to follow correct protocols. See ” Is Cost Segregation something new? ” above.

As investors, we like paper depreciation to occur earlier because that offsets gains earlier and gets more money in our pocket earlier. Just like how you give a mouse a cookie…. Give an investor a dollar early and… they will turn em’ and burn em’.

In other words, you are not creating more depreciation, you are shifting it earlier to take advantage of the time value of money concept.

On the project-level in a single asset LLC arrangement, the more you can lower your tax liability, the more you can significantly increase your passive income and create more value for investors.

A cost segregation study, in effect, gives you an interest-free loan from the government for the first 15 years, which you will then repay interest-free over the remaining 25 years. Wouldn’t you rather have your money now? There are also advantages in doing a study if the building is going to be sold (via 1031 exchange) or if the owner of the building dies.

Most cost segregation firms will perform a free analysis if you provide your basic property information and tax rate. From the information you provide, they can calculate a conservative estimate of the accelerated benefits you can expect, as well as their fixed fee proposed for the final study.

Typically, tax savings from 5% to 10% of the building’s original tax-basis are generated, but there are instances where it can be substantially more. Each property and circumstance is unique, so it requires a case-by-case approach to give you a definitive answer.

Certain types of commercial properties can be grouped together to give us an idea of the percentage of those types of buildings eligible for accelerated depreciation. Your results may be greater, or less than those quoted here, but in general, property that falls into one of the following categories is most likely to result in accelerated depreciation within the specified ranges.

A study conducted by a reputable Cost Segregation firm should strictly adhere to the IRS Cost Segregation Audit Techniques Guide . The type of study most firms perform places you in Internal Revenue Code Tax Compliance, which actually decrease your chances of an audit. However, you should be aware there are six different Cost Segregation methods allowed by the IRS, and not all are of equal merit. There is currently no standard method, and there is still some ambiguity about which method is best. If you have heard conflicting information about what is, and is not possible regarding Cost Segregation, it really depends on which method is being used.

A reputable Cost Segregation firm can assist you in the event of an audit. They will focus on doing the Cost Segregation Study to create documentation and support for conclusions so that these are easily communicated and resolved with the IRS. In fact, you should expect a final report that is “all inclusive”. The report should quote specific Internal Revenue Codes related to the reallocated assets. Additionally, it should provide photographic evidence of these same assets for complete substantiation of the assessment. A properly documented Cost Segregation Study helps resolve IRS inquiries at the earliest stages.

A cost segregation study can still be performed even if you lack some of the necessary documentation. Construction, engineering, and other specialists will do an extensive site visit. They will measure and estimate using currently accepted costing techniques and pricing guides (such as the IRS-recommended costing publications Marshall & Swift and RS Means ) to determine the costs that qualify for shorter recovery life periods.

Paying ~2% fees per year on my Health Saving Account driving me crazy that I withdraw it and invest cash.

I’m going to start out by saying please do not take this as legal/tax advice!

One rule I follow is “pigs get fat but hogs get slaughtered.”

But if there is a tax code or loophole within reason/ethical good faith you should exploit it as much as possible.

In 2017, I purchased a half acre in a turnkey Coffee farm in Panama in my Health Savings Account (HSA) for about $15,000.

HSA’s are truly awesome! You add money to an account tax-free (like a pre-tax 401k), don’t get taxed on the gains (like any retirement account), and you don’t have to pay taxes when you use it on Eligible Health Expenses (like a RothIRA).

You need a High Deductible health plan to be eligible for an HST. I’m going to get a little political here… health costs are on the rise because it bails people out for not being accountable (good diet, sleeping habits, stress, and exercise program). The company famous for the yellow Twinky bars cited rising health cost as their reason for going bankrupt… go figure.

You WILL have health expenses, MAY have retirement expense… in other words, you will likely die and have health expenses before you retire. So it makes sense to fund an HSA account before any 401K, Roth IRA, IRA, etc.

Here is some information for your entertainment purposes to see what you can start to use your HSA for:

Getting a doctor to sign off on your medical purchase as necessary will need a template:

Sample Letter of Medical Necessity for Hyperhidrosis Treatment

[Date]

[Insurer name]

Attn: [Name of individual]

[Address]

re: [Patient name]

[Policy number]

Dear [Insurer name]:

I am writing on behalf of [Patient name] to document the medical necessity of [insert treatment option here] for the treatment of hyperhidrosis. This letter provides information about the patient’s medical history and diagnosis and a statement summarizing my treatment rationale.

Hyperhidrosis, or excessive sweating, is a medical condition that can have a devastating effect on a patient’s quality of life, causing physical discomfort, secondary skin problems, social/emotional sequelae such as anxiety and depression, and disruption of occupational and daily activities. This has certainly been true for [Patient name], who has been impacted by hyperhidrosis for [insert duration of symptoms here]. Specifically, [he or she] has had difficulties with [insert quality-of-life, social/emotional and/or career/daily living problems here].

[Discuss patient’s diagnosis, treatment history, and degree of illness]

[Insert patient’s name] has tried the aforementioned therapies thus far without success and I, therefore, recommend [insert treatment option here] as the next logical choice for treating [his or her] hyperhidrosis.

In light of this clinical information, and this patient’s condition, [insert treatment option here] is medically necessary and warrants coverage. Please contact me at [(000) 000- 0000] if you require additional information.

Sincerely,

[Physician’s name]

Here is what I put together to get massages for stress from dealing with SPC listeners who don’t listen to the podcasts before booking a call or people who don’t take action:

I am writing on behalf of Lane Kawaoka to document the medical necessity of massage for the treatment of mental stress and muscular discomfort. This letter provides information about the patient’s medical history and diagnosis and a statement summarizing my treatment rationale.

“Mental stress and muscular discomfort”, is a medical condition that can have an effect on a patient’s quality of life, causing physical discomfort, secondary skin problems, social/ emotional sequelae such as anxiety and depression, and disruption of occupational and daily activities. Specifically, he has had difficulties with discomfort performing his duties at work and exercise routine [insert quality-of-life, social/emotional and/or career/daily living problems here].

[Discuss the patient’s diagnosis, treatment history, and degree of illness]

Lane Kawaoka came into the office in early 2018 where we ran a cardiovascular and blood assessment.

Lane Kawaoka has tried the aforementioned therapies thus far without success and I, therefore, recommend massage as the next logical choice for treating him.

In light of this clinical information, and this patient’s condition, massage is medically necessary and warrants coverage. Please contact me at [(000) 000-0000] if you require additional information.

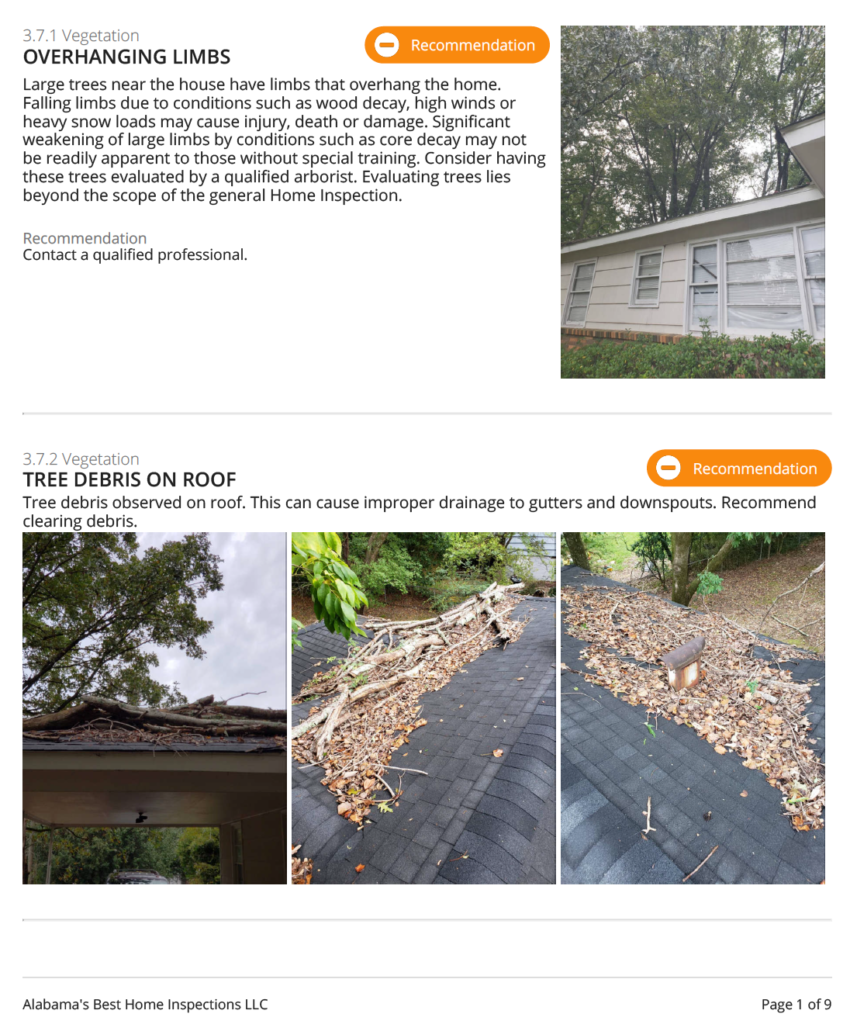

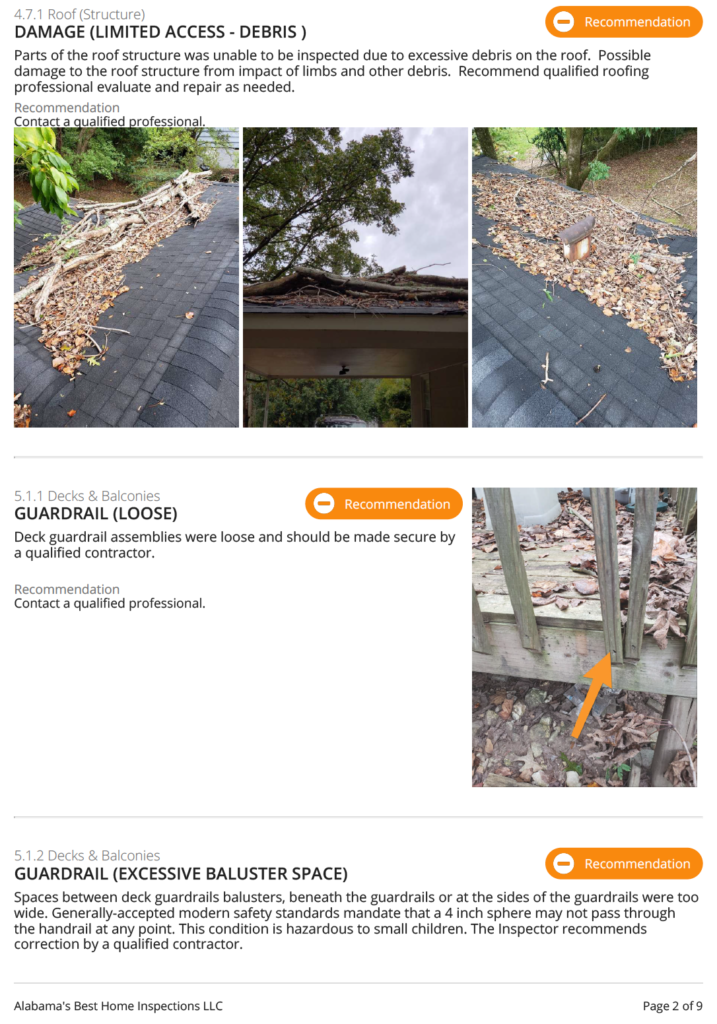

I would say this is a bad report because it’s not Prescriptive. It is very important to have a chat with your inspector so they know it’s not going to be a warm and fuzzy home to live in but a rental property. They will need to avoid citing nitpicky things because the seller is likely another investor and more sophisticated than a regular homeowner and will call BS at your repair requests.

This is where an hour of coaching will go a long way to maximize what you get at the negotiation table.

List of SDIRA Custodians in no particular order based off feedback from other Hui Deal Pipeline club members.

Accuplan

Advanta IRA

American Estate & Trust

American IRA

Asset Exchange Strategies

Broad Financial

CamaPlan

Capital IRA

Central Bank

Checkbook IRA

Community National Bank

Crowdfund IRA

The Entrust Group

Equity Trust Company

First Trust Company of Onaga

GoldStar Trust Company

Guidant Financial Group, LLC

Horizon Trust Company

iPlanGroup

IRAvest

IRA Advantage

IRA Club

IRA Express, Inc.

IRA Innovations

IRA Resources

IRA Services Trust Company

Kingdom Trust Company

Lincoln Trust Company

Madison Trust Company

Midland IRA

Millennium Trust Company

Mountain West IRA

Nevada Trust Company

New Direction IRA

New Standard IRA

Next Generation Trust Services

Nexus Direct IRA

NuView IRA

PENSCO Trust Company

PGI Agency

PolyComp Trust Company

Preferred Trust Company

Premier Trust

Provident Trust Group

Quest IRA

RealTrust IRA Alternatives

Safeguard Advisors

Self Directed

Self Directed IRA Services, Inc.

Sense Financial

Sovereign International Pension Services

Specialized IRA Services

Summit Trust Company

SunWest Trust Company

Trust Company of America

uDirect IRA

Vantage IRA

401kCheckbook

The Self-Directed IRA Graveyard

American Pension Services

I don’t personally like these accounts for my own investing even though the future gains and withdrawals are tax-free because you can’t use the best Fannie Mae or Freddie Mac loan products when investing in your IRA.

Unless you are using a QRP (Qualified Retirement Plan).

With syndications using leverage (as most good deals do) you will be likely opening yourself up to UDFI etc taxes.

In the end, I want the freedom to enjoy the money now and not have to wait till I am 60 something.

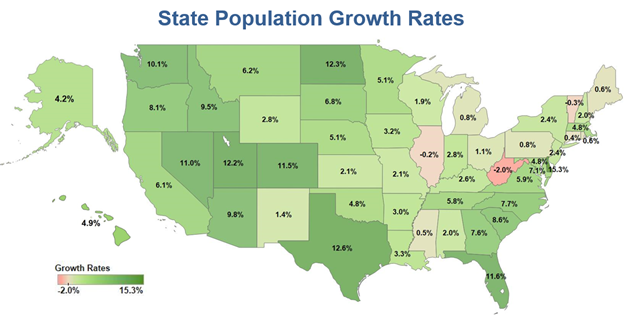

Between 2010 and 2017, population growth averaged 5.5% for the US as a whole. Delaware boasted the highest growth rate, 15.3%, over these years. A state with a relatively small population, however, needs fewer new residents to achieve such a high growth rate. The double-digit rates recorded by Texas (up 12.6%) and Florida (up 11.6%), both high-population states, are therefore that much more impressive. There were three states that posted population decline between 2010 and 2017: West Virginia (down 2.0%), Vermont (down 0.3%), and Illinois (down 0.2%). – ITR – 19.02.28

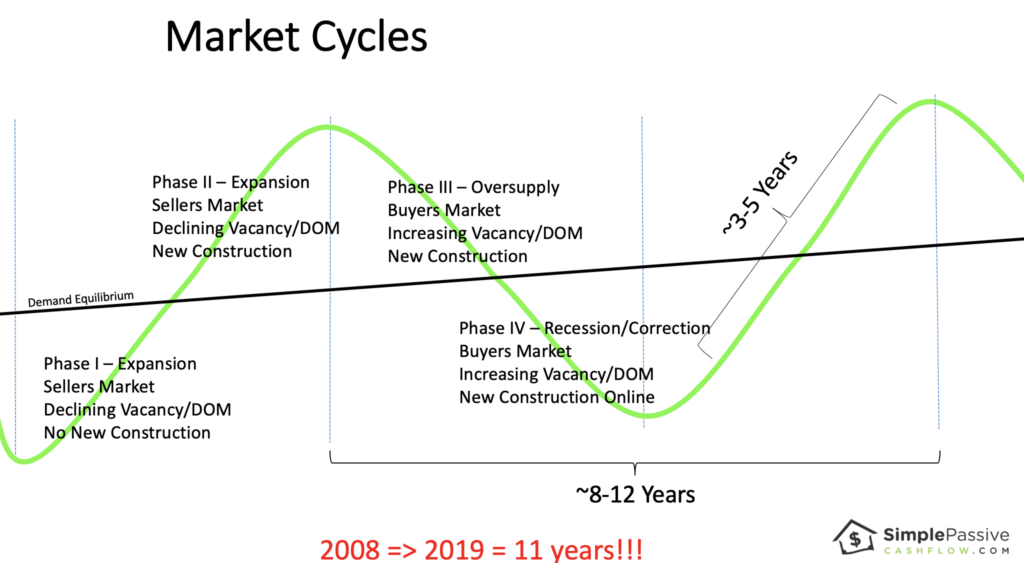

Since I feel we are in the 9th inning of an 11 inning ball game, I decided to pass on a recent Class-A apartment deal in a secondary market.

Here is my thought process…

First off, Robert Kiyosaki has a saying: “There are three sides to a coin.”

People like to argue that it is either a good time to buy or a bad time to buy. For example, they say that “MFH” is overheated or commercial is getting killed by Amazon and e-commerce. I think these are mental justifications by tire-kickers who are scared to act. I mean really how many of these people are under the accredited status (not sophisticated) or not obtained their “Simple Passive Cashflow number.”

Sophisticated investors still trying to grow live on the edge of the “coin.” They buy deals out of the reach of amateurs due to the amateurs’ lack of network/knowledge. These opportunities are undervalued, with undermarket rents, with value-add opportunity. Sophisticated investors are patient; they don’t stray from standards that force them to get crushed in a market correction. (Cashflow from other investments makes this possible.) They invest following the macro- and micro- trends and don’t gamble on gimmicks such as guessing where Amazon’s next HQ is going or where the hurricanes just drowned a market.

The trouble is that an unsophisticated investor or an outsider (in terms of having a poor network) is figuring out which of these deals transcends the two sides of coin and is on the edge. Stating the obvious (though often ignored by many)… starting out as an investor is going to be slim-pickin’s due to the lack of network. But you have to push through this rough part. You are not able to decode the noise until after a few deals or having someone mentor you.

With that out of the way let’s continue…

Real estate is one of the best risk-adjusted investments out there. In private placements or syndications, we are able to crowd-invest in larger & more stable assets while maintaining control with operators who are aligned in our best interests. By going into a project properly capitalized with adequate capital expenditure, budget, and cash reserves, you are able to remain steadfast through softness in the market where rents stagnate and vacancy decreases.

(If you are starting out you should start with turnkey rentals even though they are much more volatile)

Pause there. In troubled times what happens?

People lose their jobs and there is a bit of shuffling.

Yea, people need housing, but there will be some vacancy as some people will lose their jobs and be displaced elsewhere.

Following this train of thought…

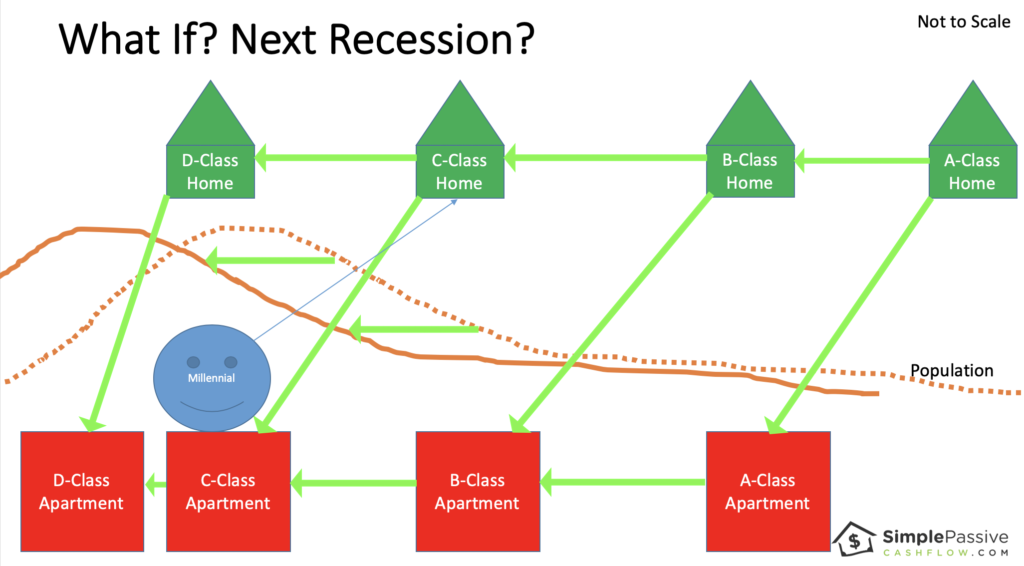

In a recession, the high end or class A will be hurt the most. It is Class A workers who fulfill much of he discretionary services. We are already seeing softness in rent by rent decreases in class A of the high-end markets such as Seattle and San Francisco.

For example a once $1,700 one bedroom is now $1,625.

Most deals model for 1-5% in annual rent increases or escalators. Other than the Cap Rate to Reversion Cap Rate truck, this is the second most manipulated assumption in investment modeling.

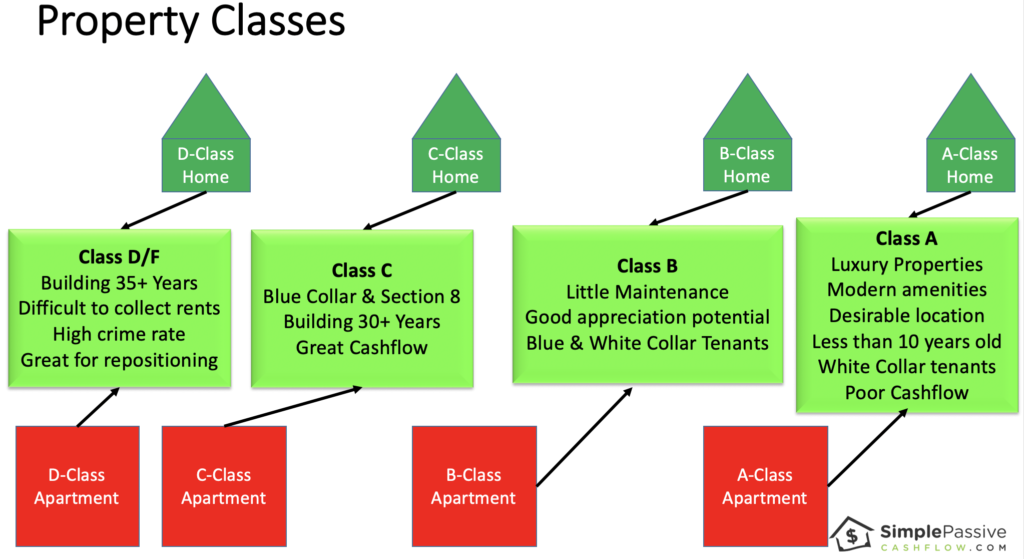

In this unfortunate but natural event, the A-Class renters will fall to class B housing. Some homeowners will even lose their jobs creating foreclosed investments for smaller investors in the single-family home scale.

What’s happens to the B and C class renters?

It is likely that they will also lose their jobs at higher or lower rates, but that is up to debate. In the same fashion as the A-Class renters, the Class B/C renters will downgrade to make ends meet.

I imagine this similar to a game of musical chairs (where the chairs are getting crappier and crappier). Or it looks a lot like the natural housing shuffle in the summer near colleges with people moving in and out. The landlord/investor is likely to see increased vacancy.

Multifamily occupancy varies from 85-95% in stabilized buildings. Some markets are hotter and some are colder. It is important to use the correct assumptions depending on the markets. For example, Dallas typically sees 92% occupancy while Oklahoma City sees 89%.

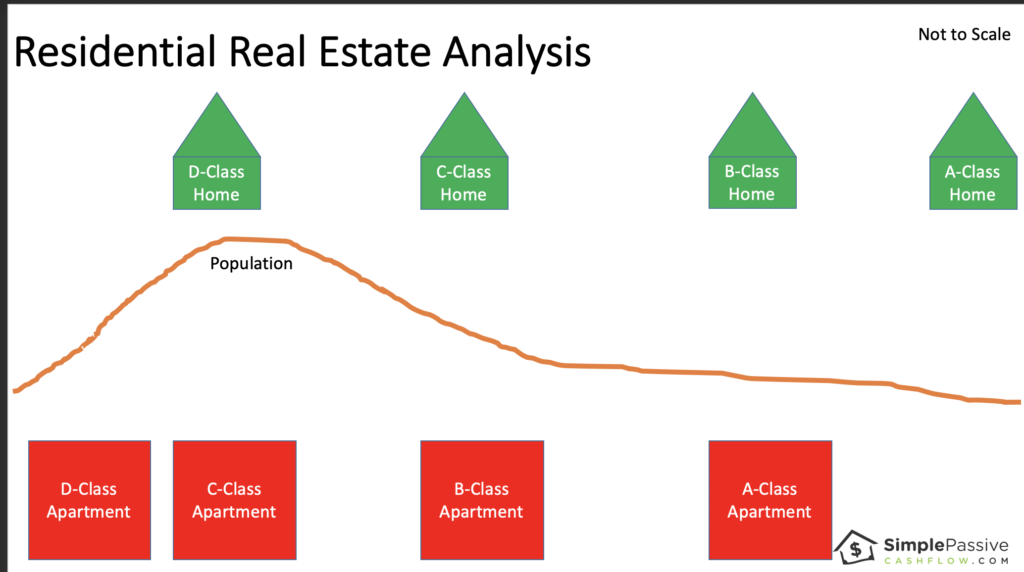

One of the reasons we love multifamily is because of the decline of the middle class and the need for more scalable workforce housing. [And those millennials can’t save] The population is increasing too.

[I like to use this image cause I make fun of millennials… this is the millennial version… cause they can’t seem to afford (or want) to own anything]

When I travel to Asia (which I see as a more mature society, for better or worse) there is a much larger wealth gap than in the USA. People are living in cramped apartments or very rare single-family homes. And they are driving a Mercedes on barely enough money to share a family moped. This is the trend that the USA is following.

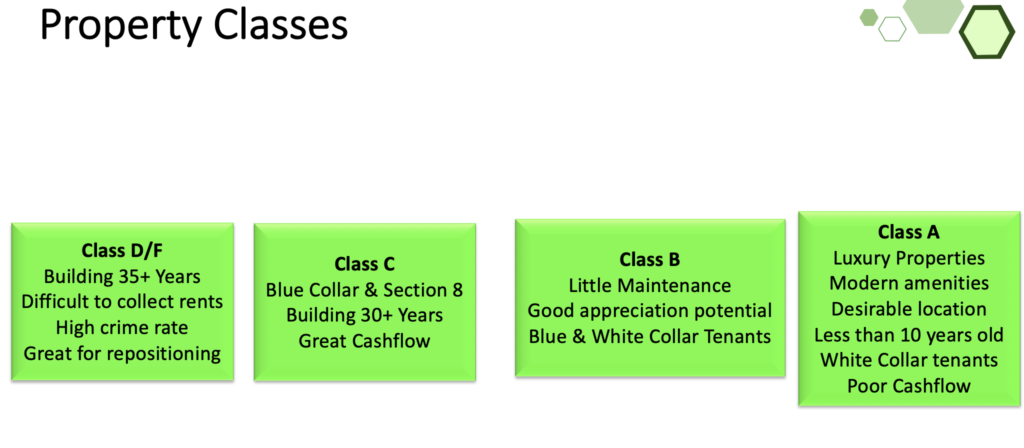

As with many things, you need to look past the headlines and the general data. Instead of analyzing a whole asset class, as the media likes to do, let’s break down vacancy in terms of classes.

Here are some typical vacancy rates (notice the spread).

Class C 4.5%

Class B 5.0%

Class A 5.5%

Why? Because there is just more demand for the lower class properties cause there is more demand than supply.

Many times the business plan is the be the “best in class.” For example, businesses want to be the best mobile home park or best high end remodel because you attract the richest customers in that niche.

I like to monitor the number of new units coming online because that is your downward pressure. It is rare that new builds are for Class C or Class B.

The micro-unit trend is an attempt to build for Class C and B tenants due to the need. But often the numbers don’t make sense when you have purchased the same building materials and mobilized the same crews to build a Class B asset as opposed to a class A asset.

Let’s go through that Armageddon example again.

Class A will have to drop rents severely and see great vacancy.

Class B and C will see vacancy come up too as people are losing their jobs but should see some absorption from ex-A Class tenants.

Mom and dad will also see some absorption as deadbeat son or daughter move back home.

Shows like Friends and How I Met Your Mother will go on for another decade.

Note: one can argue that class A+ will not be affected at all which I believe is true. That’s why we are trying to invest right to enter that untouchable status.

I remember when I sat through the same economic presentation at work from 2010-2014. The sentiment at the time was that it was going to be an extremely slow recovery. It makes sense that the length between the 2008 recession and now is very long which is why I mentioned an 11-inning ball game.

This is why I took a set back from some pretty Class A deals because I asked myself the following questions:

1) What will happen to the rents if IT should happen?

2) Is the modeled 90% vacancy rate going to get blown up?

Class B and C apartments in strong submarkets will perform best over the long term. If you ensure the loan term is long enough so you don’t get hurt then you should Outlast the bumpy ride ahead.

Beware of the self-destructive behavior of not investing. You know what I mean… are you someone who self-sabotages?

Understand the micro and proceed if the numbers make sense.

I have to admit Class C and B assets are boring but work especially in a seller’s market because 1) they cashflow and 2) have a forced appreciation value-add component to give you levers to pull in tough times.

Again going back to Mr. Kiyosaki’s three-sided coin quote, investors go through three stages.

Stage 1: Go into MFH… Duh (I did well at single-family rentals let me try apartments)

Stage 2: Be a contrarian investor so go into other asset classes most decent investors are afraid or don’t even know about

Stage 3: Do special projects such as Affordable house taking advantage of tax credits or specialized operators (ie take abandoned big-box space like movie theaters and convert to the latest consumer needs)

Experienced investors who were in the downturn in 2008 say its interesting that the sentiment in 2006 was exuberance that it was going to keep going up. Now in 2018 the sentiment is fear… This is a good thing.

Remember that in this market we still have:

Historically low-interest rates

Historically high rent increases (not 8% anymore but still 2-4%)

Historically low vacancies

Things to monitor if you really need to geek out on numbers:

2 and 10 yield t curve. When that crosses you have just-a matter do time. Because its a measure of fear.

Automation and AI – huge shifts in jobs. People need to work but technology has been increasing since the beginning of time.

Wage growth

Bankers prospective: how deals are getting funded and by who (institutional or dumb capital)

There is a saying out there that real estate is location specific. However, when I invest in more stable asset classes its a National market based on the economy both USA and international. When you invest in a micro-economic fix and flips then its location specific. When you invest in commercial assets it’s with more stable tenants and based on the aforementioned larger economy.

How affordable is rent really? – “During the same span, median effective rent nationally has risen by about 26%. That rent appreciation pushed the median monthly rent nationally to around $1,220 per unit to end 2018. With the US median household income being just over $62,000, this rent accounts for 24% of monthly income. Using the typical benchmark of monthly rent being 30% of monthly household income for affordability, a margin remains for renters.” – [If you stick to using 2% and under rent growths and stay away from Tier I or Primary markets you should be fine] – ALN 19.02.24

A lot of people point to the Yield-Curve as a big indicator. In the end, I do believe that real estate will go down because of consumer instability. But if you have stocks you should sell those before even thinking of lumping it into cashflow type rental real estate.

“The guy not investing right now and hoarding cash (with net worth of under $1M… because if you can live off your cashflow then cool you can do what you want) is just afraid and lacks deal flow. Its like the person who complains that there is nothing to do during the weekend in LA (insert city with a vibrant scene) when in actuality they don’t have any friends (lack dealflow)… and by the no one likes (has a bad attitude and that person who makes excuses”

Doomsday theory: Everyone talks about national debt but we are far far behind debt to GDP ratio that of Japan. When Japan hits the wall lookout. Her is my theory… watch out post-Japan Olympics when they have to let loose the belt (after a holiday period of excess calories). Leading up to a period where Japan has to save face while they are in the Olympic spotlight (and I’m not being racist cause I am Japanese and it is a thing). I don’t have the latest data but Japan is at around 250% where the USA is at 100%.

Household debt KPIs: student debt, car loans, housing debt. Which is why I like these assets that are used by the poor and middle class! #RenterForever

Lane’s theory: I’d rather be in deals that cashflow today that do better in a recession like Class C and B assets. Say it cashflows a 8%.

The guy who is stilling on the sidelines with the “hoarding cash” mindset will lose because they will make 0%.

I, on the other hand, might dip from 8% cashflow to 4% cashflow. On paper, I might be in a market with compressed cap rates but hopefully, I have forced appreciation potential if I really needed to sell – the counter move is to get 8-12 year debt to effectively bridge you to the next side of the market cycle. In the meantime you cashflow 4% which is 4% more than the “hoarding cash guy”.

In addition, remember back in the 2008 crash. 2009-2012 people did not know if that was the bottom and it was so hard to close deals in that Phase IV (see below). “Hoarding cash guy” in 2009-2012 and the few years after the next recession will likely be in the same clueless situations.

Wouldn’t you like to be in solid Class C and B assets that continued to cashflow?!? 4% x 4 years is still 16% ahead!

Now if you are “hoarding cash guy” with no deal flow then I get it. Saving cash is the best thing to do for the guy with no deal flow or does not know how to run the numbers. I guess everything does suck.

[Investors are chasing for decreasing yield these days] – REI.com – 19.03.4

[Sophisticated Investors know interest rates and caps go up and down together and their money is made in the delta between the two] – REI.com – 19.03.4

Of course, all the Pro-Apartment publications will say this: Get Ready: Recession-Proofing An Apartment Portfolio – National Apartment Association 19.03.7

But enough of this doom and gloom because most gurus out there call recession everyday just so they can have Tweetable content. And they make a living selling subcriptions to their $79/month newsletter. But we are better than the average investor! And understand that future softness could very well be slowdown before the next great bull market.

To join our Hui Deal Pipeline Club and stick with the group join below:

Article Link: Text “simple” to 314-665-1767 to download the Hui Google Drive files and the 2018 Rental Property Analyzer

For a free electronic version of my bestselling book in 12+ categories text the word “ebook” to 587-317-6099.

Please help the show by leaving a review: http://getpodcast.reviews/id/1118795347

Join the Hui Deal Pipeline Club! SimplePassiveCashflow.com/club

Pardon the grammar – I’m an Engeneer, Enginere, Engenere… I’m good with math!

________Here are the Show Notes________

Estate planning

Guests I have are giving insights but always hire your own person because these things require personalization

I try to bring guests on and ask the questions that I think you folks would ask.

I believe you need to have a basic level of knowledge before engaging with a professional

For those of you who are in the Mastermind and my current investors you will hear about my Fort Knox strategy which makes LLC enitites creation look like childs play

Email me any questions to feature on the next ask Lane podcast or monthly email newsletter

Andrew L. Howell is the Co-Founder of the law firm, York Howell, with a focus on asset protection.

Many useful tools out there, but where do you as an investor fall on the asset protection spectrum?

Two fundamental risks: 1) Asset-based risks 2) Direct-based risks

Real estate considered as “hot” assets because liability risks are greater – more than equity.

Liabilities both inside and outside the asset.

Typically form a holding company to hold limited liability companies to abate asset- and direct-based risks.

Holding properties in one LLC basket is good, but still risks if something happens in one property.

Concentrate on family protection first (trust, wills, etc.). Then move to next level of asset protection planning.

If own property out-of-state, advise on setting up a parent LLC in states with charging-order protection.

Tough LLC rules and taxes for poor California residents!

Need to do your due diligence on reviewing PPM’s – especially who you are doing business with.

Asset does not create liability risk for LP’s; only GP’s.

If you get personally sued, can go after your MFH syndications and other assets even as LP.

6% of current generation feels obligated to give back to kids. Instead of giving, create a bank.

Create purpose when setting up your trust.

Please reach out to teamandrew@yorkhowell.com and visit www.yorkhowell.com.