The country effectively shutdown for half of 2020, unemployment is high (expectedly so with a slow ramp up), yet the stock market is on track to be at all time highs by the end of the year?!? WTF?!? Call me crazy but this sounds fishy!

In case you missed it at least 3 Trillion dollars of economic stimulus has been flushed into the system.

Could this be what is pumping the stock market with fake money?

When is the air going to be let out of the stock market again?

Do you remember how you felt back in March 2020 when stocks lost a third of it’s value? Don’t forget that.

The Cares Act now allows for a 100k withdrawal from your 401k or TSP penalty free till the end of 2020 and possibly till you file your taxes in 2021. This is the time to get out of frothy paper assets and into real hard assets.

Never forget! Do yourself a favor and get out of fake assets and into real assets that produce cashflow.

The great Recession of 2008 was a systemic failure in the real estate market caused by bad mortgages, rampant home flipping and speculation, and overbuilding all contributed to the last financial meltdown.

NINJAs (No income no job no asset) were being approved for multiple home loans on the belief that housing prices would just keep going up and these loans were packaged off and sold as Wall Street derivatives.

https://youtu.be/iDcbUAh731s

Today, it is difficult for even high paid professionals like you to qualify for Fannie Mae/Freddie Mac loans. Credit scores need to be higher, debt-to-income ratios need to be lower, and lenders verify incomes much more carefully. Join our Remote Investor Incubator and we can connect you with the lender that we use.

This time around, there is a growing demand for affordable rentals housing due to increasing population, less homeowners, and the constant separation of the haves and have-nots 🙁 the much-stronger housing market isn’t the driver of the crisis—it’s the effects from COVID-19 a medical crisis. It is a true Black Swan event.

What Could Cause the Stock Market to Fall?

A severe second wave of the Coronavirus

Insufficient additional Fiscal Stimulus (which would make the bad economic fundamentals even worse)

The possibility that the markets have already priced in all the impact that the Fed’s new money creation will have on stock prices

If the Fed signals it will create less than $120 billion a month, a new “taper tantrum” would be likely to cause stocks to plunge

A political crisis in the run up to or the aftermath of the November Presidential elections

Any number of other unforeseen developments

Is this a time to sight tight and not invest?

You could do this and make 0% on your money or load it into deals that make sense, tie up good long-term under 4% debt, and hedge against inflation as the country looks for revenue sources such as taxes or debt minimizers with inflation.

I have taken a “load and stabilize” approach to my investing where I…

Load into some good deals (one at a time or every few months)

See them stabilize (harden into recession-proof after a few months)

Repeat the Process

Some may even see this as the “dollar-cost-average” approach which is similar to what were taught in stock investing 101.

I have seen pricing on assets increase every year since 2009.

I felt what you are feeling back in 2012… if I would have stopped I would have missed out on another great run!

I felt what you are feeling back in 2015… if I would have stopped I would have missed out on another great run!

I felt what you are feeling back in 2018… if I would have stopped I would have missed out on another great run!

After seeing this phenomenon happen for a few times and seeing a lot of people who never got started, I realized and had proof of concept that as long as I go into conservatively underwritten deals that cashflow I am pretty much untouchable or going to do a lot better than waiting on the sidelines.

COVID19 came and I was a little worried to see how April and May collections were. But collections remained strong and came down only 2-8% across the 3,500 unit portfolio. In some assets, collections improved! Commercial real estate pricing was pretty much unchanged and experts say that at most Cap rates went up only 0.25%. (Excluding commercial retail storefront and short term AirBNB type rental who got killed)

Now, you can see where I am coming from in my neutral-aggressive stance.

Combine that with the fact that I am around higher level Accredited investors these days who have seen the ups and downs and they say NOW we see the separation between the faint of heart and those who take their family’s legacy to the next level.

Of course… don’t be silly and choose investments in good sub-markets and have sound underwriting to ensure cashflow.

Warren Buffet said “be fearful when others are greedy, and greedy when others are fearful.”

John D Rockefeller said “The way to make money is to buy when blood is running in the streets.”

The Fed has pretty much doubled down and planning for additional stimulus plans which is ensuring the nation moves past the current COVID crisis with Infinite Quantitative Easing commitments through the year 2022 and beyond. Get on this wave now!

We were able to get a lot of interior footage on Harbor Village units on this last trip out to Huntsville!

Also included are drone shots of all recently acquired properties.

2nd half of video is Garden Place and upgraded and non upgraded units in Treehaven which are our other class C properties.

Now what?

Let’s reconnect, huddle up, and get a game plan for you as this is we start to build a legacy!

If we have not connected use this link to setup a time to chat that works best for you.

The population is still going up…

Between 2010 and 2017, population growth averaged 5.5% for the US as a whole. Delaware boasted the highest growth rate, 15.3%, over these years. A state with a relatively small population, however, needs fewer new residents to achieve such a high growth rate. The double-digit rates recorded by Texas (up 12.6%) and Florida (up 11.6%), both high-population states, are therefore that much more impressive. There were three states that posted population decline between 2010 and 2017: West Virginia (down 2.0%), Vermont (down 0.3%), and Illinois (down 0.2%). – ITR – 19.02.28

Since I feel we are in the 9th inning of an 11 inning ball game, I decided to pass on a recent Class-A apartment deal in a secondary market.

Here is my thought process…

First off, Robert Kiyosaki has a saying: “There are three sides to a coin.”

People like to argue that it is either a good time to buy or a bad time to buy. For example, they say that “MFH” is overheated or commercial is getting killed by Amazon and e-commerce. I think these are mental justifications by tire-kickers who are scared to act. I mean really how many of these people are under the accredited status (not sophisticated) or have not obtained their “Simple Passive Cashflow number.”

Lane Kawaoka

Simplepassivecashflow.com Sophisticated investors still trying to grow on the edge of the “coin.” They buy deals out of the reach of amateurs due to the amateurs’ lack of network/knowledge. These opportunities are undervalued, with undermarket rents, with value-add opportunity. Sophisticated investors are patient; they don’t stray from standards that force them to get crushed in a market correction. (Cashflow from other investments makes this possible.) They invest following the macro- and micro- trends and don’t gamble on gimmicks such as guessing where Amazon’s next HQ is going or where the hurricanes just drowned a market.The trouble is that an unsophisticated investor or an outsider (in terms of having a poor network) is figuring out which of these deals transcends the two sides of coin and is on the edge. Stating the obvious (though often ignored by many)… starting out as an investor is going to be slim-pickin’s due to the lack of network. But you have to push through this rough part. You are not able to decode the noise until after a few deals or having someone mentor you.

Get the Right Mentor – Join the Incubator

Real estate is one of the best risk-adjusted investments out there. In private placements or syndications, we are able to crowd-invest in larger & more stable assets while maintaining control with operators who are aligned in our best interests. By going into a project properly capitalized with adequate capital expenditure, budget, and cash reserves, you are able to remain steadfast through softness in the market where rents stagnate and vacancy decreases.

(If you are starting out you should start with turnkey rentals even though they are much more 🎥 volatile)

Pause there. In troubled times what happens?

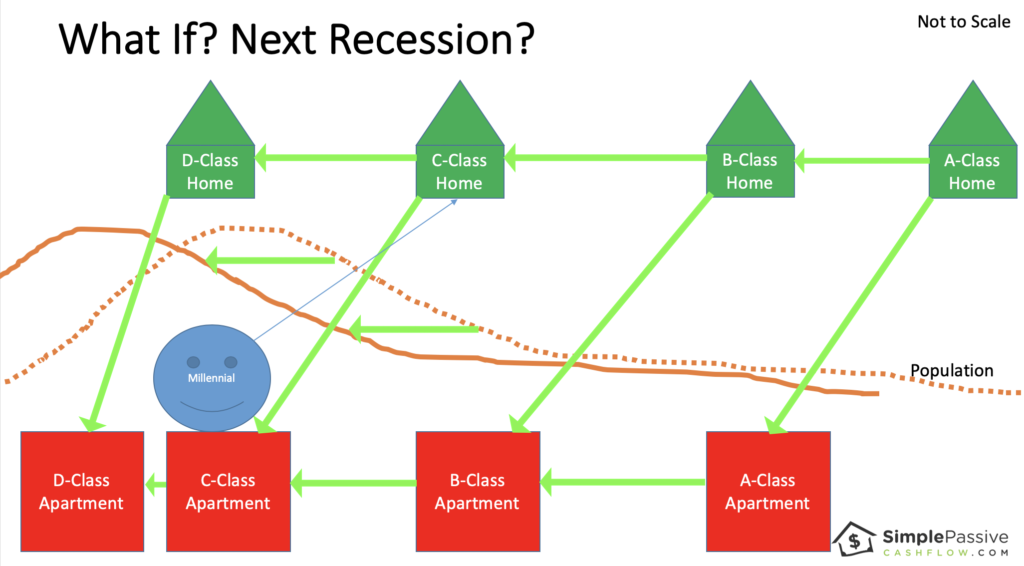

People lose their jobs and there is a bit of shuffling, let’s take a look at different the different property classes:

Previous

Next

Yea, people need housing, but there will be some vacancy as some people will lose their jobs and be displaced elsewhere.

Following this train of thought…

In a recession, the high end or class A will be hurt the most. It is Class A workers who fulfill much of he discretionary services. We are already seeing softness in rent by rent decreases in class A of the high-end markets such as Seattle and San Francisco.

For example a once $1,700 one bedroom is now $1,625.

Most deals model for 1-5% in annual rent increases or escalators. Other than the Cap Rate to Reversion Cap Rate truck, this is the second most manipulated assumption in investment modeling.

In this unfortunate but natural event, the A-Class renters will fall to class B housing. Some homeowners will even lose their jobs creating foreclosed investments for smaller investors in the single-family home scale.

What’s happens to the B and C class renters?

It is likely that they will also lose their jobs at higher or lower rates, but that is up to debate. In the same fashion as the A-Class renters, the Class B/C renters will downgrade to make ends meet.

I imagine this similar to a game of musical chairs (where the chairs are getting crappier and crappier). Or it looks a lot like the natural housing shuffle in the summer near colleges with people moving in and out. The landlord/investor is likely to see increased vacancy.

Multifamily occupancy varies from 85-95% in stabilized buildings. Some markets are hotter and some are colder. It is important to use the correct assumptions depending on the markets. For example, Dallas typically sees 92% occupancy while Oklahoma City sees 89%.

One of the reasons we love multifamily is because of the decline of the middle class and the need for more scalable workforce housing. [And those millennials can’t save] The population is increasing too.

[I like to use this image cause I make fun of millennials… this is the millennial version… cause they can’t seem to afford (or want) to own anything]

When I travel to Asia (which I see as a more mature society, for better or worse) there is a much larger wealth gap than in the USA. People are living in cramped apartments or very rare single-family homes. And they are driving a Mercedes on barely enough money to share a family moped. This is the trend that the USA is following.

As with many things, you need to look past the headlines and the general data. Instead of analyzing a whole asset class, as the media likes to do, let’s break down vacancy in terms of classes.

Here are some typical vacancy rates (notice the spread).

Class C 4.5%

Class B 5.0%

Class A 5.5%

Why? Because there is just more demand for the lower class properties because there is more demand than supply.

Many times the business plan is the be the “best in class.” For example, businesses want to be the best mobile home park or best high end remodel because you attract the richest customers in that niche.

I like to monitor the number of new units coming online because that is your downward pressure. It is rare that new builds are for Class C or Class B.

The micro-unit trend is an attempt to build for Class C and B tenants due to the need. But often the numbers don’t make sense when you have purchased the same building materials and mobilized the same crews to build a Class B asset as opposed to a class A asset.

Let’s go through that Armageddon example again.

Class A will have to drop rents severely and see great vacancy.

Class B and C will see vacancy come up too as people are losing their jobs but should see some absorption from ex-A Class tenants.

Mom and dad will also see some absorption as deadbeat son or daughter move back home.

Note: one can argue that class A+ will not be affected at all which I believe is true. That’s why we are trying to invest right to enter that untouchable status.

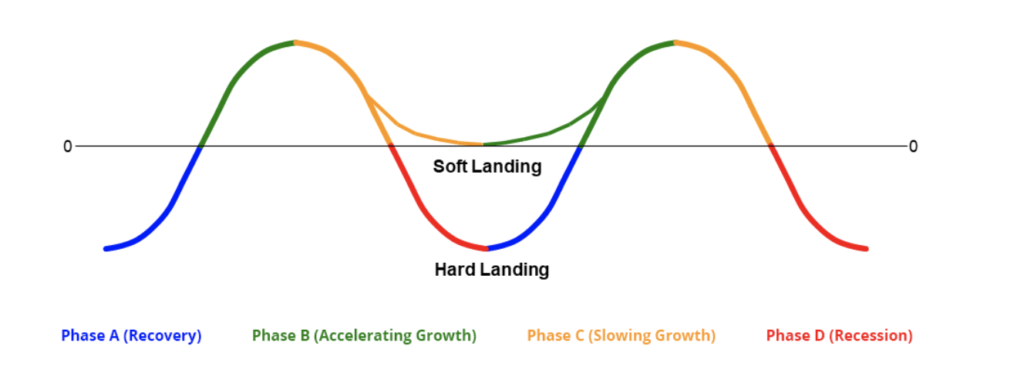

I remember when I sat through the same economic presentation at work from 2010-2014. The sentiment at the time was that it was going to be an extremely slow recovery. It makes sense that the length between the 2008 recession and now is very long which is why I mentioned an 11-inning ball game.

Previous

Next

This is why I took a step back from some pretty Class A deals because I asked myself the following questions:

1) What will happen to the rents if IT should happen?

2) Is the modeled 90% vacancy rate going to get blown up?

Class B and C apartments in strong submarkets will perform best over the long term. If you ensure the loan term is long enough so you don’t get hurt then you should Outlast the bumpy ride ahead.

Beware of the self-destructive behavior of not investing. You know what I mean… are you someone who self-sabotages?

Understand the micro and proceed if the numbers make sense.

I have to admit Class C and B assets are boring but work especially in a seller’s market because 1) they cashflow and 2) have a forced appreciation value-add component to give you levers to pull in tough times.

Again going back to Mr. Kiyosaki’s three-sided coin quote, investors go through three stages:

Do special projects such as Affordable house taking advantage of tax credits or specialized operators (ie take abandoned big-box space like movie theaters and convert to the latest consumer needs)

Experienced investors who were in the downturn in 2008 say its interesting that the sentiment in 2006 was exuberance that it was going to keep going up. Now in 2018 the sentiment is fear… This is a good thing. Remember that in this market we still have:

Historically low-interest rates

Historically high rent increases (not 8% anymore but still 2-4%)

Historically low vacancies

Things to monitor if you really need to geek out on numbers:

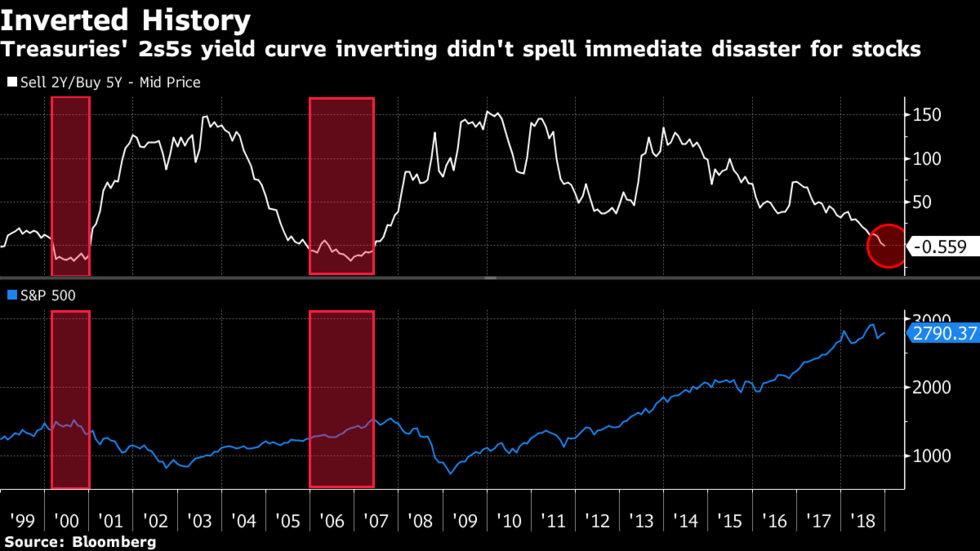

2 and 10 yield t curve. When that crosses you have just-a matter do time. Because its a measure of fear.

Automation and AI – huge shifts in jobs. People need to work but technology has been increasing since the beginning of time.

Wage growth

Bankers prospective: how deals are getting funded and by who (institutional or dumb capital)

There is a saying out there that real estate is location specific. However, when I invest in more stable asset classes it’s a National market based on the economy both USA and international. When you invest in a micro-economic fix and flips then it’s location specific. When you invest in commercial assets it’s with more stable tenants and based on the aforementioned larger economy. How affordable is rent really? – “During the same span, median effective rent nationally has risen by about 26%. That rent appreciation pushed the median monthly rent nationally to around $1,220 per unit to end 2018. With the US median household income being just over $62,000, this rent accounts for 24% of monthly income. Using the typical benchmark of monthly rent being 30% of monthly household income for affordability, a margin remains for renters.” – [If you stick to using 2% and under rent growths and stay away from Tier I or Primary markets you should be fine] – ALN 19.02.24 A lot of people point to the Yield-Curve as a big indicator. In the end, I do believe that real estate will go down because of consumer instability. But if you have stocks you should sell those before even thinking of lumping it into cash flow type rental real estate.

“The guy not investing right now and hoarding cash (with net worth of under $1M… because if you can live off your cash flow then cool you can do what you want) is just afraid and lacks deal flow. Its like the person who complains that there is nothing to do during the weekend in LA (insert city with a vibrant scene) when in actuality they don’t have any friends (lack dealflow)… and by the no one likes (has a bad attitude and that person who makes excuses”

Lane Kawaoka

Simplepassivecashflow.com

Doomsday theory: Everyone talks about national debt but we are far far behind debt to GDP ratio that of Japan. When Japan hits the wall lookout. Here is my theory… watch out post-Japan Olympics when they have to let loose the belt (after a holiday period of excess calories). Leading up to a period where Japan has to save face while they are in the Olympic spotlight (and I’m not being racist cause I am Japanese and it is a thing). I don’t have the latest data but Japan is at around 250% where the USA is at 100%. Household debt KPIs: student debt, car loans, housing debt. Which is why I like these assets that are used by the poor and middle class! #RenterForever Lane’s theory: I’d rather be in deals that cashflow today that do better in a recession like Class C and B assets. Say it cashflows a 8%.The guy who is stilling on the sidelines with the “hoarding cash” mindset will lose because they will make 0%.

Use our Remote Rental Turnkey Rolodex

I, on the other hand, might dip from 8% cashflow to 4% cashflow. On paper, I might be in a market with compressed cap rates but hopefully, I have forced appreciation potential if I really needed to sell – the counter move is to get 8-12 year debt to effectively bridge you to the next side of the market cycle. In the meantime you cashflow 4% which is 4% more than the “hoarding cash guy”. In addition, remember back in the 2008 crash. 2009-2012 people did not know if that was the bottom and it was so hard to close deals in that Phase IV (see below). “Hoarding cash guy” in 2009-2012 and the few years after the next recession will likely be in the same clueless situations. Wouldn’t you like to be in solid Class C and B assets that continued to cashflow?!? 4% x 4 years is still 16% ahead! Now if you are “hoarding cash guy” with no deal flow then I get it. Saving cash is the best thing to do for the guy with no deal flow or does not know how to run the numbers. I guess everything does suck.

Previous

Next

[Investors are chasing for decreasing yield these days] – REI.com – 19.03.4

Previous

Next

[Sophisticated Investors know interest rates and caps go up and down together and their money is made in the delta between the two] – REI.com – 19.03.4

Of course, all the Pro-Apartment publications will say this: Get Ready: Recession-Proofing An Apartment Portfolio – National Apartment Association 19.03.7

But enough of this doom and gloom because most gurus out there call recession everyday just so they can have Tweetable content. And they make a living selling subcriptions to their $79/month newsletter. But we are better than the average investor! And understand that future softness could very well be slowdown before the next great bull market.

If you get a good tenant, they’ll stay in there for a long time. And that’s really very magical moment when that happens. This

0:08

is a story about a dude named Lane he moved to the mainland and bought one place to stay. And then one day he went try to rent them out. And then he became one real investor Tell me

0:22

a simple passive cash flow listeners. Today we are going to be doing a live coaching call with a physician who is fits in the category of a lower net worth but a high salary. Definitely be on the road to being an accredited investor here in the next few years. Introducing JP Kim who took me up on the offer to record their coaching call, which is still open for folks and if you guys haven’t connected with me, please sign up for the investor club at simple passive cash flow comm slash club and I reach out this cam. Thanks for doing this. I want you to give folks a little bit of quick background on You know, or you have kind of been doing the last 20 years of your life

1:03

for the last 20 years. Okay.

1:06

Well, I, I was a non traditional medical students so I decided to go into medicine enter medical school in my late 20s. And then I graduate from med school after five years and then I did my residency training. I got out of training about five years ago and then I’ve been working as a locum tenens traveling physician, seeing geriatric patients in three states, California, Arizona and Indiana. So I I started my job as a 1099, you know, independent contractor physician, so I’m not I’m not in a hospital. I’m not a hospital employee or clinic employee. I’m considered an independent contractor person. So I I only get paid when I’m working. You know, there’s no like paid time off or anything like that. The company That I work for, luckily pays for my travel likes, if I had to move to a different state, the airfare, the hotel accommodations, and then the rental car expenses are all paid for. So as a single person, it’s been a really exciting journey past five years. The money just keep stacking up,

2:21

right? I mean, no

2:22

expenses. I don’t really have any expenses. So like, I don’t have to pay for my own primary residence mortgage or rent, because it’s all you know, being paid for by my company. Yeah, I know, I don’t have a car payment. I used to have a car that I sold because I don’t use a mic my own car anymore. I always get to use a rental car to drive around. So it’s a very unique situation. But then, in about four years ago, I started noticing that, you know, I’m only making money while I’m working. And even though I like to travel and stuff like what if something happened and I can’t work anymore than My income will stop coming in. So I had read Robert Kiyosaki his book, Rich Dad, Poor Dad and the cashflow quadrant. And it really made sense to me that like I should start, you know, buying income producing assets that bring in positive passive income. So even when I’m not working, I still have enough income to pay for all my expenses so that I can help maintain a good quality of life. So I started taking, like the rich dad education seminar, I started attending some of these conferences, and I hired some mentors, who were really successful in real estate investing and learned that buying and holding cash flowing income properties as a way to is the way to get started. I was initially in California when I was working in 2017. That’s when I was going through all the real estate investment education. And I tried to buy a house there, but it was it was extremely Very expensive and competitive to to get a good deal. So after trying for several months, I kind of gave up there but then I started my fellowship at University of Arizona in Tucson. So I would go to Tucson and I noticed that in Tucson It was so much more affordable to buy houses there in comparison to California. So I thought, I thought okay, maybe I’ll buy my first single family home in Tucson, so I just kind of found a property that was going to cash flow. And I got it under contract in in late 2017. And then I closed on it using a conventional loan with 20%, down in early, early 2018. And then I was able to find a property manager who could manage it for me while I’m traveling. And they found a tenant right away and then so the tenant moved in and then they were paying down the mortgage. So it’s been pretty good and then right after that, I decided that I had since I didn’t have a primary residence, I learned that some people do house hacking. So they can use an FHA loan. So a very low downpayment loan to purchase up to a four Plex. So you can you can purchase your primary residence, that can also be a rental property at the same time. So the rent, you can live in one unit and then rent out the other three units and have that rental income from the other three units cover for all your mortgage, your expenses. So that’s what I pursued for the next few months after I closed on my first property in 2018. And this is all under the guidance you had paid like quite a bit of money right for like, quote this coaching, right? Yeah, yeah. So I spent the entire like 2017 going to all these symposiums How much did

5:49

you spend like for all this stuff? And why?

5:53

That $26,000 plus traveling fee, I would say about like, 30 grand on that.

6:01

Yeah,

6:02

I mean, I mean, I’m actually calling on my mission just kind of destroy these type of companies out there taking this money. I mean, I think you’re fine. Like you you had money to invest. So it kind of made sense. I mean, it’s a starting point, right? What a problem like a lot of these guys, they cater towards people without any money. And you’ve kind of reached the, the limits with them kind of where your net worth, or earning potential is, like a lot of these guys, like the best stuff they have for high paid working professionals is the house hacking thing or quadplex, which I think as you’re seeing as you kind of go through our group, I mean, it’s it’s the tip of the iceberg, what the wealthy people are doing, and they just don’t have any insight into that type of world.

6:44

Right, right. But because I had never bought a house before and I never owned any property before. I think it was a good learning experience, just to know, just to get to know how your qualifying for loan works and how to how to put it off.

6:56

right and i think you know, like that. Just kind of Your profile here we have a lot of folks that are kind of in your category where lower net worth kind of starting out in wealth building, again, net worth of a quarter million dollars. And but very high earning potential. Your current active income is about $20,000 a month. So do the math that’s around, you know, quarter million dollars. I mean, most, most doctors are making over, you know, specialists, especially they’re making over three to 500,000 at least a year. So a lot of this is, you know, I think you found this at the right time, and we’ll get you to where you need. We’ll take you from 25 miles an hour up to 70 pretty quickly here.

7:46

Well, yeah, that’s great. That’s Wait,

7:48

that’s the plan.

7:51

So um, here’s the big question. I asked a lot of people, so we have your net worth here. And then your active income is about Not quarter million a year. But you know, with your expenses right now how much you actually stick in the bank every year? How much of it Do you not spend on like food or your lack of car, you said,

8:12

save a lot of money because I don’t really, I don’t have kids yet I’m not married. And I don’t have to spend money on utilities or car payment, like car registration fees or insurance. So I would say like, maybe like 70 of my 80% of my monthly income, I’m saving in the bank, and I’m using it towards either downpayment for for investing or I’m using it for going to these networking events, conferences for real estate investing. I’m also in the process of learning how to build an online health business as well to build another stream of passive income. So for that, I mean, I’m, I’m pursuing like a mastermind group as well, mastermind education So I basically I spend most of my money on on those things, educational activities and self development, growth books, courses,

9:09

just to get it sounds like it’s, you know, 80% of a quarter million. I mean, you’re able to put away 150, at least a year, which is phenomenal. I mean, I, let’s say most people in our investor club, some of the beginners are at 30,000 a year, some of the ones are a little bit better than most are about 50 a year. But I mean, in theory, you’re able to buy 123 probably five turnkey rentals a year, right, which is phenomenal. Not saying I mean, you wouldn’t want anything to do with rental properties. I mean, it’s just not scalable for your, your, your earning power at this point. But I mean, just it’s just the kind of thing.

9:46

Yeah, so owning the single or

9:52

have a good property management company employees. And I had I had to go through a lot of trials and errors during that because because good ones, they got burnt out easily and they quit after a few, you know, a few months, and then I would get a new property manager on that I never had a rapport with and then they would do something that would just that wouldn’t be in alignment with my my investment goals. And then I’ve had a lot of turnover from with my, with every single one of my properties. And that’s been costing me a lot of money. So I’m noticing it wasn’t, I mean, it’s so much headaches that I don’t really feel like I want to pursue buying more or more of these properties anymore. by attending some of the events where there’s more seasoned real estate investors, I learned that people with high net worth and you know, billionaires, they tend to invest in syndications. They network with people who find a really good deals. So it’s like a totally passive investment so you don’t have to be so involved in managing your property manager so that you You can just do invest your money sign that sign the documents and then you just get your your cash flow and then your your appreciation and then all the tax benefits coming in but without having to deal with those headaches. So right. I just learned about that in October 2019 by going to Hawaii and that’s where I met you lane. Right. And then I learned about your syndication deal. So, in February 2020 right before the covid pandemic hit us I I invested my you know, in my first syndication deal, which has been good so far, right?

11:42

Yeah, yeah, checks are coming out here soon.

11:46

We after we read after we closed on the deal, so my goal for the rest of the year is to network with other syndicators and then just learn about these syndication projects and I’m hoping that I can sell these the single family home And for four Plex. Luckily, the Tucson market has been pretty hot. And the the property values have gone up. And I’ve met with the, with a realtor or listing listing agent who who did, who kind of did the comparative marketing market analysis recently. And she says that I will be able to sell those properties at a significant profit. So my goal is to sell those in the next within the next month or so and then use the game to to participate in more syndication deals by the end of this year or early next year.

12:40

Well, and, and a lot of, you know, I would say you’re, you’ve got a lot more time on your hands than the average folk out there. So you’re able to kind of go around and network a lot more travel around the conferences, which is exactly what you need to be doing as a passive investor since your network is your net worth. But for those of you guys listening, you know, that’s why We have the passive investor accelerate mastermind, it’s our online group of it’s kind of a pay to pay program. But you know, it’s the way of building relationships with those, you know, high net worth mostly accredited investors to get deal flow that way and build relationships. jp, let’s you had some, you know, a few questions you had, I think the first one was like about student loans, once you kind of go over, like what you what you are doing in that category for you up to now and then we can kind of talk through the path for it there.

13:30

Yeah, so when I was grad when I graduated from medical school back in 2011, I had about a little bit over $200,000 in student loans. You know, during residency, I was only paying off a little bit like minimum amount and it was only paying off a little bit of interest, so kept on going and growing and growing. So once I, you know, finished, got finished with residency training and started working as a local physicians, you know, making like six figure income was paying off my loans back then the loan payments, the monthly payments were over $3,000 a month, I thought it was kind of high. So by then I had established better credit, my credit score went up. So I checked in with some, like student loan private student loan companies, and they were able to refinance me at a lower interest rates. So it was able, I was able to lower my monthly payments down to 1200 and $48 a month.

14:32

What What did the rate go from? And then now it’s what 5.8 All right. Well, yeah, initially,

14:38

my my student loan rates were like 8.75% when I came out of med school, so now I refinance, to like 5.875%

14:52

were those first loans, the higher rate ones were they like government subsidized or like kind of like a Stafford Loan or anything like that. Or would they just privatize government subsidized loans? Yes.

15:04

Okay. So I think I think that’s, there’s a lot of US companies like so fi that will do it. And we have some of the resources on my website that will do this for folks with a lot of student loans. I’m a little skeptical, though. I mean, I think I mean, everything from the high level looks fine, like the interest rate lowers, and obviously, that lowers the monthly payments. But what I’m concerned with, and I mean, what you’ve done already is done, it’s over. But if you guys are listening to this in the future, I think something to look into, is where you’re going from like a government subsidized loan to a privatized loan. I don’t know. I mean, even if it’s a lower interest rate, you may or may not be worth it. But just something to think about if you guys are doing this in the future, if you guys are listening to this, but did you did you do any kind of research on that? I mean, I mean, you just kind of looked at the interest rate. I mean, you’re gonna pay it off. Anyway, I guess. It’s just more about payment,

16:01

right? So I was debating if I should focus my efforts on, on paying off the student loan first before jumping into real estate investment. But then when I hired the real estate mentor, she mentioned that dumping all that money into trying to pay off the student loan first is actually it’s a sunken cost. And because if you if you find good real estate investments, and you can bring these income producing assets that will bring in more cash flow than the monthly payment, or student loan payment, so even if I were to not work, the income producing assets will pay for my student pay down my student loans, and then when the student loans are all paid off, I’ll still have those assets. Right.

16:48

Right. Exactly. And, you know, kind of, for me to explain it in a different way. A lot of you know, just interest rate arbitrage from a certain extent So, I mean, I have an article at simple passive cash flow calm slash returns, where I kind of just break down the returns that you get from just a typical turnkey rental and you’re looking at 20 plus percent. I mean, 20% is greater than 6% here, so it’s a no brainer, right? But, you know, most people are able to make more than eight to 10% in their, you know, crappy stock investments, right? So you can see why for most people, it would make sense to pay off your your student loans or pay down your mortgage first, but I mean, maybe since I mean, you’ve come to this, this realization, what was for you that kind of tipped the scale in your head that kind of get it? If you think kind of remind remember, sick kind of lot of people are just on the fence, right?

17:48

Well, I mean, there’s always an opportunity cost of doing something so if you spend all your effort on paying off your student loans, your that’s going to delay being able to buy income producing assets. If you Like, like my mentor said, if I if I’m able to buy a income producing asset that not only has good cash flow, but also appreciation, and then the tax benefits, then that really Trumps you know, the interest rate of a student loan. So she was telling me just set you know, refinance my student loans to the lower monthly payment. So you can always pay more if you wanted to pay sooner, but if you but if you keep your student loans at a, you know, higher monthly payment, what if something happens, you lose your job, you get sick, you get into a car accident, then you can’t make your loan payments, and you’re more likely to default on it right? It looks better on your credit. So she was telling me it’s easier if you just kind of refinance it and minimize your monthly payments. And then if you feel like if you’re making good money at certain points in your life through your cash flowing assets, then you can choose to make extra payments to pay down your principal and paid off sooner. But like it just gives you more options to refinance it and minimize your payment obligations as well.

19:00

Well, so good doctor, well said.

19:04

And this kind of carries over also to the whole argument of you do like a 30 year mortgage or a 15 year mortgage mortgage. Right? Like, I mean, like you said, in our camp, we do the longest that we can. And if we choose to, we can pay it off, but debt elimination and is not really correlated with financial freedom. But yeah, I agree. Yeah, delay, you’re paying off your your student loans as long as you can, you know, a lot of people are doing they do this like 10 year, and they work in like a low income area, and they forgive other student loans. Have you kind of looked into that option?

19:40

I looked into that option, but I also heard that if even if you get your loans forgiven, you get taxed on that amount. So you’re gonna have to pay tax during during that time when you get forgiven and it’s really hard to qualify for that too. Yeah, I mean, I’ve heard people you know, spending all that time doing public service and then after After the term, they realized they didn’t qualifier so

20:06

been investing with hp since 2017. To buy distressed mortgages and discounts to offer struggling families sustainable solutions to stay in their homes or homes were vacant. HP recognized that lenders frequently struggled as they tried to limit their losses. That’s why owner George Dewberry founded pre aureo, a platform that gets these vacant properties into the hands of local investors like us during the foreclosure process, which mitigates losses to lenders and accelerates returns for investors a win win. I’m very excited about this platform that connects local investors with board appointed receivers in their area to cost effectively repair, lease and maintain and rent vacant homes during the foreclosure process and ultimately make a profit. I’ve been checking out local properties here in Hawaii and I think it’s a great way to finally pick up my home to live in. Even though I think homes, the buyers are the best You can learn more about pre Rio by going to simple passive cash flow calm slash v. Rio.

21:09

Yeah, I,

21:11

I’ve heard of this, this these companies that they’ll put your stuff in like an LLC, and then they create a nonprofit. And then what they’re doing is they’re gonna show it give you a kinetic excuse to write it off for a nonprofit for 10 years, which I think is kind of shady. Or you can create your own nonprofit and kind of do it but that’s like, you know, that’s more more technical, I guess, then what we’re looking to do. But, yeah, I mean, any other questions on the student loan thing or what’s kind of the next issue at hand that you want to tackle?

21:46

So I have different arguments about you know, so my rental properties right now I’m going through some turnovers because one of my tenant died. She was an old lady. She was really good paying tenant and then now that she died unexpectedly. In May, we’re having to find a new tenant we’re dealing with, like, you know, turning over the property. We are, of course, increasing the rents, but it’s going to take, I don’t know, maybe it’s going to take maybe a few days or weeks to return it over. There might be more than maintenance issues. I’m kind of waiting for that call from a company manager about what’s going to happen about maintenance issues. So is it really worth keeping those properties? So I’m right now I’m deciding if I want to just sell them,

22:28

when which which property? Is this or what’s the what’s the monthly rents on this one?

22:34

Or if some people were telling me I should keep those rental properties because I have direct control over it? Because, you know, sometimes if you get involved in syndication deals, sure. It’s passive, but you might lose control over your money.

22:49

Which which rental property are we talking about here? Just the 1200 a month one?

22:53

Well, I was thinking about selling both

22:57

and what are the rents now

23:00

single family home brings in 11 $95 per month of rent, and then the mortgages 860. And then the four Plex the rents are like 30 $100 a month and the mortgage is 1600 and $9.

23:16

So, I mean, just to kind of follow my logic here, like with your net worth and your kind of your, your high value in time as opposed to money. If you had, like $60,000 property pieces of junk, I would say yeah, unload it, like yesterday, near single family home, it’s probably it’s a decent property, right? It’s more of a B class property and then your duplex and that’s probably a lower class asset. But you know, I mean, it’s there’s some decent scale on that thing. I would say you know, right now you’re you’re kind of one foot in the syndication private placement world in the other foot still in direct ownership, right? You a lot of investors in my group They’re kind of been very the same thing. And at some point, and I think we could both agree maybe in the next three, five, certainly before you know, you retire, you’re going to be all in on the private placements and syndications. But, look, I mean, you got to just when you’re comfortable, you know, you sell these assets. But I have no problem. You know, you kind of holding on to it a little bit longer. You know, if you have enough time, right? If your life gets busier, then yeah, you unload them, but I wouldn’t be buying more properties. You know, I mean, like direct ownership. And yeah, if somebody had the same situation, but they had like, lower crop class properties, more headaches. Yeah, I would try to unload them as soon as possible. That kind of makes sense.

24:44

Yeah, so I’m looking into maybe selling the four Plex because the type of tenants that I’ve been attracting were like lower income people and then we had to go I mean, we had to deal with evictions.

24:59

Which is Not so cool.

25:01

Yeah. And I get the feeling like just your personality, you kind of, I mean, you’re not too bad. But you know, you stress out about this stuff a little bit, right? Like you’re kind of a hands on person in a way.

25:12

No, I like to have a little bit of control over my properties. But at the same time, I didn’t like I really did not enjoy it hassle dealing with the eviction, like my property manager. I mean, she was a new new person that I’d never met before. So I had to kind of wait and see to see if we had an a rapport. Sometimes we had some conflicts, and that that caused a lot of stress. So I’m kind of debating if it’s really worth having to deal with that situation anymore. So luckily, I will be making a lot of profit if I if I were to choose to sell this in the next month or so. Because the Tucson market, they weren’t really affected too much by the pandemic. I mean, they’re their business are still operating and people are still working. So The tenants had been paying rent, you know, a lot of people are still paying rent. And they say the rental market is pretty hot these days. So they’re able to find tenants right away good paying tenants. So, if the listing agent turns out that she’s able to market the property really well, that I will be able to sell it at a pretty good price, and then move that money over to doing more syndications in the future, you know,

26:28

yeah, so what I mean, I made this decision that I was going to I was in one foot in syndication one foot and my 11 single family home rentals back in 2015 16. And then, in 2016, I kind of made that defining point. You know, I think your podcast ad I think was that was that point where I just where I kind of made that decision and for you, this could be three to six months from now, right? When you finally make the decision, it could be a year or two but I took it took me all of 2017 the cell actually hurts yet 2018 to sell seven properties 2019 to sell two and 2020 to sell the remaining two. So you don’t really need to sell this right away. But I would say, maybe the best strategy for now I don’t, I don’t, you know, you don’t need to do something out of haste, but maybe put the duplex on the market and just let it sit there for whatever it takes six months to two years and get your price that you want. You know, you can be that unmotivated seller and maybe do that the same thing for that single family home. I mean, with a single family home, what I would do is if the tenant if you have a good paying tenant, those guys are gold. Maybe you haven’t realized that yet. Because people get it they internally understand that after about a few years of rental property landlording if you get a good tenant, they’ll stay in there for a long time. And that’s it. Really very magical moment when that happens. But if you might have that in this property, and if so that’s cool. But as soon as this current tenant moves out, what I would do is I would fix it up to go retail. So you might have to put in 1020 $30,000. But you’re going to sell this to a nice retail buyer who’s an emotional buyer is going to pay, you know, potentially over 200 250,000 for this thing, and that’s your exit strategy. But you know, that Domino could could topple six months from now, three, four years from now, we don’t know. But your destiny is shaped in your decisions, as Tony Robbins says, and yeah, you’ve made the decision, you’re going to move to private placements, but you don’t need to take the action on it now. Just let it let it happen. Okay. But I think that’s the by doing that strategy, you’re able to extract the most amount of dollars out of it. And, look, I mean, there’s still good rental properties or cash flowing for you. I would say the other question I had that maybe it may impact this decision. is how much liquidity Do you have right now? And how much dry powder? Do you have to invest? sure the deal come up, you know, next month in the in the syndication deal. I’m just looking. Yeah, that number kind of at the top of your head, how much liquidity you have to go?

29:18

Well, assuming that I’ll be continuing to work. I mean, luckily, my job. I mean, I didn’t really get impacted so much with the COVID-19. I know a lot of doctors got furloughed and we had to stop working. But for me, I was doing telemedicine, I had consistent income. So I still making money and I’m still going to be working. I’m still working. So I will continue to have $20,000 $20,000 per month.

29:44

Yeah, you’re saving what 80% of that amazing, right? But currently, I’m just I mean, looking at some of these accounts. I’m in it looks like you have not including our self directed Roth which you can take that out context free. Because you’ve already paid the taxes and penalty free on the on the contributions, but, you know, you probably have about 100 grand on liquidity. So that’s enough to go on to two deals at 50 grand. I mean until you burn through that I wouldn’t I see no reason for you to unload these two rentals. I mean, maybe if you had no liquidity then it would be you’d be a little more motivated but yeah, just you know, this is where your your lazy equity is not doing anything. Get that working first before you you get this stuff for me and for the bottom as much money as you’re able to save. You may never run out quiddity

30:43

is a cool place to be.

30:44

Yeah, but it’s assuming that I’m still healthy that I never get coronavirus infection, you know, and I’m still you know, working at my hundred percent capacity. Yeah,

30:52

I mean, you know, you know, you’re you’re kind of amazing because most doctors I come across, they have this false sense of self Security where they think that well they make so much freakin money. Right? And they never think to invest outside of the normal financial planner stocks. I mean, it’s good that you’re investing in this stuff that you’re very unique.

31:13

Right? Well, I made that mistake during residency. So I What, what I did was that I did contribute to my 401 b during residency training. And the residency director had some some GL advisor, like some company who was like a financial manager company for physicians. They came and gave a presentation and they talked about how they can manage the doctors money because the doctors are so busy

31:38

doctors, which is a complete scam. Usually these guys get kickbacks for that. And

31:44

so I actually hired them to manage my money and what happened during those during those several years that I was in residency, they were managing me money, I would maximize my contribution to my Roth IRA, 401 b and everything. And then they were they were invested. That into like mutual funds, but like, the money wasn’t growing, you know, except for me country contributing. And then towards the end, like after like a year after I got out of residency all of a sudden I found out that that company was prosecuted because they were they were caught frauding with the investors money so they totally like went out of business and all of a sudden my my 401 b money and then my Roth IRA account money was left without a manager without a financial manager and I was like, holy crap, what am I supposed to do and I had no knowledge about finances. So that’s when I like started reading, you know, Rich Dad Poor Dad cash flow game, and that’s when I started scrolling through Facebook to look for information about real estate investing. And then when I you know, that’s when I went, Oh, you know, with mutual funds and stocks, you really don’t have any control over your money, right. And then You can’t stick it out until you’re certain age, whereas real estate you can, you can really find the right cash flowing investments and start making money right now start making cash flow right now that’s generating passive income that can cover for my student loan payment. So that’s, that’s the route that I took after I after making that huge mistake. But luckily, during that time, we just kept it at, you know, at the same amount

33:24

when it comes to something. That’s an amazing story.

33:28

I mean, I don’t know where’s your Where’s your headspace on it. I mean, in in hindsight, I was probably the best thing to happen at the time. Right. So you know, you live and learn, right? Yeah, I mean, so many doctors out there that are just totally still believing in the Easter Bunny and the tooth fairy is going to give them money. 401k is going to work right. You know

33:48

what, like a lot of doctors, you know, when they were hit by COVID. They’re realizing

33:54

everyone’s just kind of in a panic mode. Right now. We’re like learning how to invest in generate other You know, multiple students with passive income so a lot of doctors are getting into the investing world right now, like outside of stocks and mutual funds. Realize like our job is no longer secure anymore and like, the way like the hospital ministration cheated a lot of doctors like rolling doctors and cutting, arbitrarily cutting their salaries to like, you know, if I have a lot of private practice doctors, you know, the doctors, orthopedic surgeons or neurosurgeons or, you know, plastic surgeons, they a lot of they make all their money through elective cases and they’re not able to operate their business and they, they still have to pay their employees, you know, you know, fixed salaries, but they don’t have any revenue coming in because the COVID-19 and now they’re all realizing, oh, you know, we’re not no longer high income earners anymore, you know, during this pandemic, so, I think a lot of doctors are scrambling right now to learn about other other passive income generating opportunities.

34:56

Yeah, I mean, we have like a lot of guys in our kuih that work. You know, general dentists and they were all out of the job. And yet they were the ones gone through life in residence or all their training, thinking that everybody’s going to need their teeth clean come hell or high water, but well, boy, were they wrong. But I mean, at the end of the day, it’s

35:17

like, multiple streams of income is what reigns supreme.

35:22

Right? And there’s no guarantee in anything, right? Yeah.

35:29

But um, let’s say you have one last thing here. I wanted to get to you have you you’re in a place in life where you’re not, you know, you’re not accredited yet in terms of network. But you’re going to be there very quickly. And I like how you kind of like you have some bigger goals, right, that are kind of bigger than yourself, where you want to build enough wealth to build a new medical school at your alma mater, maybe talk to us about how that idea came about. And how, how kind of you’re pulling yourself to that goal,

36:01

well like for me, like personal experience, I went to college on a full scholarship. So when I graduated from college, I didn’t have any debt. But when I went to med school, I had to take out like significant amount of student loans like more than $200,000 even though I went to a public school in California, and it just really it’s been, you know, weighing down heavily on my chest like I always feel like I have an elephant sitting on my chest and a lot of doctors come out there to like he said, You know, my my medical school, going going to medical school, I had to take out a lot of student loans and coming out of training, I always felt this heaviness in my chest with that debt, burden of debt, and, and then the lack of financial education. So I really want to contribute to the society by utilizing my knowledge of business investment. To starting a medical school that focus on integrative medicine but also like on business and investing education so that the future doctors can come You know, they’re not only good clinicians but also really savvy business investors too.

37:16

So what’s um, how much money are you going to need for that? Or what’s the what’s the plan timeline like that.

37:24

In the next 10 years I you know, want to build wealth through doing real estate. It’s mostly like passive syndications and also network with other high net worth people and collaborate so it’ll be about at least 100 million dollars to do that project of building a new medical school and also want to make it very tuition free for all the students who get accepted. So I’ll have to have like a scholarship foundation as well which is like a nonprofit. So once I have a you know, a nice vehicle of money making money More money every year, that can be a lasting legacy that, you know, continues on and on even after I die, you know, I can hire people who can carry on the legacy. I mean, if I have a goal like that, that will keep me motivated to keep pushing through all the hardships and challenges in life. Right?

38:18

Right. Right. And you know, kind of very similar, just different, you know, different end goal. I don’t want to make a medical facility but I would rather I’m trying to create like a financial education program that’s more free and affordable for networking professionals. The LLC is called f5 for the worthy you will find that financial independence is not for everyone, but I kind of want to bring it to the working financially responsible for masses. So yeah, I mean, exactly what you’re doing, you know, trying to put my own oxygen mask on for for now, pretty much there. But um, you know, you need capital to make these big dreams happen, right? So, so for me maybe would be a few more years, maybe 510 more years to get myself up to that point where I’m set up personally and then maybe even the next year or two, I start the nonprofit LLC. I know you’re a little familiar with that. But um, yeah, I’ll let you know how it goes. I mean, the that’s really how big things happen and how money can grow tax free. There’s so many benefits of being a nonprofit. And it’s all predicated, of course, you using that money for good, right? Not just personally benefiting from it. But if you have some bigger dream, that nonprofit is the way to go. But of course, um, you know, there’s definitely going to be some learning lessons down the road, but I’ll let you know how it goes.

39:44

Yeah, yeah. I mean, we’re both. I mean, we have

39:49

tax advisors and CPAs who were really

39:54

they specialize in, you know, real estate investing and then setting up these business entities and nonprofit organizations to protect you from having to pay too much income taxes, right? So I think that helps to, you know, legally minimize income taxes and you can generate more profit and then use that money towards investing in more income producing assets and go from there. So, I think we’re all learning,

40:19

right? And if you guys want to, um, I have a little working page on this whole concept of a nonprofit and simple passive cash flow, calm slash legacy has a whole list of things on there that the benefits to having a nonprofit, you know, like, just kind of reading some of them real quick. I just looked it up. Actually, I don’t have it up. But like things like you until you look forward. Like you don’t realize how many like tax benefits nonprofits have and that really helps you grow your money on restricted to kind of do these bigger, bigger things. But um, Miss Kim, anything else you want to talk about or think for now?

40:59

Oh, Do you have any recommended resources to, for me to keep expanding my network? You know, I need to I mean, in order to get to where I want to be quicker and faster, I need to leverage, you know, good people, right good network and people with the knowledge, the skills and then people who have already have good networks.

41:21

Yeah, I mean, like the, like, the best thing that my guidance for that is like, you got to start with the right people, right. So people with money, and going to the local Ria, and, you know, a lot of free internet forums out there, we all know those websites are some of the worst places to go, because they’re just the cheapskates that are trying to get rich get rich quick. I mean, I’ve I’ve been fortunate to do this podcast where I just attracted you know, all these passive and high net worth passive accredited investors and I find the ones that are kind of thinking the same way as us and, you know, they join my passive investor accelerator mastermind, you know, maybe we can move Work out something I mean, as a current investor in the week club, you know, we can talk offline about that. But for other people listening in you know, that’s that’s kind of the option, right? Like you can either fly I mean, I did it for years, right? You go to all these silly like real estate conferences and you just find it’s a big pitch fest with people on the stage. They’re really not that proven. It’s just like there’s all these Internet’s and ships and stations overnight in real estate and you start to realize that you go there and you meet you meet a lot of cool people, you have some cool drinks but like you, you you go home with like a dozen business cards, and never never formulates to anything and you wasted like $1,000 in the conference and other thousand dollars on the hotel and food and all your time you spent you wasted that you only have so many vacation days. I mean, you really have to be selective. I mean, you know, I would I would invite you out to like the hooey mastermind that we have once a year in January. Last Yeah, last time we did was you can check out the video at simple passive cash flow calm slash QE three. Sure the next one will be called hooey for. But yeah, I mean, just I try and cultivate a group of like high quality genuine people, you know, that have, you know, bigger goals outside themselves. So it’s a good community. And, you know, we kind of kind of play watchdog out for each other, but that’d be my suggestion. Yeah, I mean, other than that, you know, you have the other options are going to the country club, or I know some guys they go to like the cigar room, and they kind of rub shoulders with high net worth people. But the problem there is you’re meeting with a lot of second third generation wealth, right? Like you and I are first generation wealth. We’re kind of building this legacy now. We didn’t nothing really got given to us. So it’s a different mindset. They’re the very narrow band of people you’re trying to find. Yeah, thanks for doing that. So we can do do a little check in next year to you probably get a lot different place, I mean, you’ll probably be very well fit the next three years. If you kind of keep hitting on this trajectory,

44:12

we’ll see how it goes like I will I do want to attempt to sell these rental properties that I have so that I have more cash and more liquidity to kind of jump into the good syndication deals in the next few months or so. So keep me in the loop please. Okay, okay.

44:31

This website offers very general information concerning real estate for investment purposes, every investor situation is unique. Always seek the services of licensed third party appraisers and inspectors to verify the value and condition of any property you intend to purchase. Use the services of professional title and escrow companies and licensed tax investment and or legal adviser before relying on any information contained here and information is not guaranteed, as in every investment there is risk. The content found here is just my opinion and things change. I reserve the right to change my mind. Above all else, do your own analysis and think for yourself because in the end, you’re the only person who is going to look out for your best

https://youtu.be/5_Slm_guB8EBRRRR is an acronym for buy, rehab, rent, refinance, repeat.

If you have done one of these deals before good job you probably made a bunch of equity and likely got into a deal for no money. For my outsiders’ prospective its successful most times (~70%) but it always takes Time. As higher net worth investors, for some of us at least time is more important than getting the best deal. When you add in an element of risk it makes the decision closer. Most Accredited investors would not bother with a Turnkey rental and a BRRR because of scalability. The sub-$200,000 bro might get really excited about getting into a cool $60,000 property with no equity after a successful BRRRR however $20,000 of manufactured equity means very little for an Accredited investor.

Other Considerations

Have you done a partnership deal with this GC before? Is this a small-time GC or a medium/larger sized builder? Either way, I’d be very skeptical of the deal unless he is incentivized to do you a favor in return for future referrals or some type of reciprocation down the road. I would be super careful before getting into bed with a GC on a project..especially if this is the first partnership type deal you are doing right now.

Maybe I’m just cynical but I feel the business proposition puts all the risk on you and he is free-rolling and possibly incentivized to screw you over.

Assuming as-is value is $160k, $40k construction price, ARV of $250k.

Off the bat, the renovation could easily go over (as larger renovations typically do) which may translate to 25% overage on the $40k estimate. That’ll put the reno at $50k.

Let’s say the builder has other higher-paying renovation jobs/priorities or that he concentrates on other items and the home reno goes until ~March.

You are looking at best-case scenario may be a ~$20k profit if everything goes perfectly for shouldering all the risk.

There is no backup plan if the house doesn’t sell. The ownership of the property is convoluted and you won’t be able to execute a cashout refinance (unless you pay him off for the renovation costs in full, but then how do you calculate his profit margins since the GC is not going to work for free). Say the appraisal comes back at ~$250k, but the best offer you get is ~$210k? At a sales price of ~84% of appraisal, I’d rather just refinance at ultra-low interest rates, turn the house into a rental (long-term or corporate rental, etc.), ride out the COVID craziness and re-assess in a year or later down the road.

Now, if the builder/GC is shady…and I’ve had awesome GC’s and I’ve also personally had to fire at least 8-10 for a myriad of reasons. But for the sake of example:

GC takes there time and overcharges you for the renovation, he makes up a bunch of BS and charges you $80K for the renovation even though the actual cost of the renovation is $40K. The extra $40k he’s charging could be to pump up his overhead rates and fake billing hours, he could supply receipts for materials that he will (or has already used) on another project, mark up other jobs or artificially increase the scope, or have items “stolen” and need to be repurchased, send you pictures of problems that need to be fixed from another house, the GC could have friends/relatives in other trades that markup their rates via a kickback scheme, etc. These are extreme examples but they happen more than you’d think. The all-in break-even point is now over $240k. And if the house sells for only $220k…guess what – the GC is going to be screaming that it’s YOUR fault…yada yada and say he needs the $20k shortfall to pay his people or he’ll put a contractor lien your house, sue you, etc. etc.

What if the renovation goes sideways and you need to fire him midway through the job?

To be honest…I would strongly advise against this partnership deal and just go the simple and straight-forward time tested route of getting bids for the renovation from multiple licensed GCs (through a referral from other investors if possible).

Set up a standard draw schedule based on project completion milestones

A full scope of work and signed construction contract

All the other standard stuff that comes along with a renovation… we can help you this in the Incubator

This option you have multiple exit strategies and have the ability to fire the GC for subpar work. Plus you are taking all the risk anyways with the partnership route, so this option is a much better risk/reward proposition in my opinion. It is very easy to get into partnerships….but HARD to get out of them and this small sfh could become a huge pain in the ass if the project goes sideways…believe me from experience. I would 100% prefer to keep the lines very clear between the owner of the property and the contractor doing a fixed scope of work to be delivered by a specified date at a predetermined price.

My two cents anyway 🙂

For those who are able to save more than $30k a year or have substantial liquidity (over 200k), being a landlord and especially flipping is a lot of work. If you like it cool/good for you… but just remember why we got into this… To be free from a JOB. A lot of us (80%) who stumble upon simplepassivecashflow.com and start drinking Kool-Aide will be financially free in 4-7 years pending taking action. So I always urge people to start with the end in mind and take a more passive approach.

Focus on being an Investor not a Landlord.

Do the math here… with 300 dollars per property (2 months of work to buy a turnkey rental) you are going to need 20-40 of these to replace your income. I have 10 of these and have systems in place but have 1-2 evictions a year and 3-4 big things that happen. Image if I had 30, just 3 x those numbers.

Directly investing in a turnkey rental or small MFH is a good way to start to learn and build up the war chest to go into my scaleable investments such as private placement syndications.

If your net worth (income minus expenses) is under $300,000 or barely save $30,000, syndications are not for you. Stick with these Turnkey rentals despite what Gurus (who are trying to sell you their program) tell you for now. They have a little higher gains (a lot more volatility) but a syndicator who is willing to put you in a deal with more than 10-20% of your net worth is asking for trouble.

*PS never like the idea of wholeselling where you basically steal houses from people at 50 cents on the dollar and say you are “helping people solve problems”

My last BRRR ever 😁 No more direct ownership rentals

https://youtu.be/qzErI3chAZ4

This is process on my Last 2021 BRRR – its a complete PITA

China/India, macro economic trends, w/ David McAlvany

Explain your business and clientele

Where do you think this economy is going

China growth is slowing

2.9% projected growth – 2.5% is technically in a recession

Corona virus is impacting growth

Europe lacking main growth indicators

US markets have never been better

Why gold?

How is gold better than mix commodities such as real estate?

TRANSCRIPTION:

0:00

So significant issues, significant issues for us to address for our policymakers to address. And as far as I’m concerned, this is not a time to put a tremendous amount of faith in a few guys and gals with PhDs, I think they think they know more than they do. This is

0:16

a story about a dude named Lane, he moved to the mainland and bought one place to stay. And then one day he went to try to rent them out. And then he became one

0:27

that still makes

0:30

us in China, or what the the kind of the leading indicators, right are the big folks in the boat that can potentially tip us over? What are some of the trends domestically that you’re kind of looking at or following?

0:41

Yeah, you know, one of the things you know, where we met, one of the things I wanted to highlight in the presentation that I gave you a month ago, is that we’re doing pretty well in the US. In fact, in some respects, by some measures, we’ve never done better. And so what does that mean when you’ve never done better you’ve got household net worth here in the United States at 113 trillion dollars, it’s never been better. I can tell you in the past when things have never been better, that’s usually been the end of a trend, not the beginning of a trend. If you just look at sort of, again, going back to that idea of business cycle, moves from sort of low levels to high levels and kind of oscillating back and forth, you go from employment, like what we have now, if 50 year, records of low employment, this is fantastic. Everybody’s at work, everybody’s being paid more. But it’s important to keep in mind that these things tend to ebb and flow. And it’s been 50 years since things have been this good. What happens generally, when you get to these kinds of points is that they are in fact inflection points where it hadn’t been this good and 50 years networth hasn’t been this good ever and you start seeing reason actually for mean reversion. mean reversion is just a fancy way of saying, We operate according to a law of averages and if things are great, now they’re not always great and They’re they’re typically pretty good. But if they’re super great now, the law of averages and mean reversion suggests that we we’ve got some downside downside in the stock market downside and bonds, you know real estate’s tricky because real estate is tied to interest rates. In many respects, if you follow a real estate portfolio, it’s it’s very similar to a bond portfolio where the cost of capital, the rate of interest is one of the key defining factors in value. If you look at cap rates, we could never have compressed cap rates like we have today, if interest rates weren’t on the floor globally and here in the United States, with rising interest rates comes rising cap rates. And yeah, I think we know what that means in terms of value for the asset as well. So the real challenge in the Americas is will the investor today benefit from Central Bank intervention in the market in order to extend these trends? keep interest rates low not because of a normal natural market? function. But just because by policy edict we want rates low, we’re going to sit on them. You know, when I went to school, the idea was that interest rates were determined by buyers and sellers not by policy edict. Right? This is the nature of the free markets correct. Where interest is is is a component, and it reflects risk, and it reflects the solidity of the borrower. And if you’re not a good borrower, you pay more if you’re a very good borrower, you pay less. Well, today, interest rates are being crushed down to very low levels across the board, by policy edict. So we have a scenario unfolding, where you could see pressure on stocks, bonds and real estate, except that real estate is in this weird category. Where if they’re able to effectively hold interest rates low indefinitely, who knows what happens to the value of real estate, people are clamoring for income people have to have income, our demographic thick, sort of big in the Python so to say is this move of baby boomers towards retirement is you probably know the numbers at least 10,000 a day, who are retiring and guess what they want, they want their retirement assets working for them paying them for something, right. And it used to be that if you had a million dollars and you’re earning 5%, you can have a laddered cd portfolio at the bank, take very little risk, never go into principal and have $50,000 a year supplementing your Social Security income, you can’t do that anymore. Today, if you’ve got a million dollars sitting at the bank, you can buy a few cups of Starbucks throughout the year. That’s it. That’s it. So you know, real estate as it is a very interesting thing. I think there’s some vulnerabilities there. But, you know, as you said, this gets very specific. We’ve talking very macro to do well in real estate, I think is to hone in on the property and try to adjust many of the risk variables by preference preference. For a certain style of property, a certain place for that property, it doesn’t come back to the three words that you think everyone knows about real estate, location, location, location.

5:12

I think and, you know, kind of going back to what you’re saying, I think there was a statistic that somebody threw throughout that, that mastermind were very soon there’s gonna be more like 60, people turning 65 and babies born. And they’re going to want to convert their assets that they that they accumulated to this accumulation mentality, which I think is wrong. And finally transition into cash flow, the stuff that we aspire to now, and then kind of going back to your earlier point, in like, as an investor, I don’t care what the interest rates are. Because as an investor, I make money off of the delta between interest rates and cap rates. I think I think you kind of mentioned they kind of float based on one another. They kind of track the same way. I’ll throw out a recommendation For folks listening, and maybe you can do one to David, but, you know, I’ll say like, Look, don’t don’t just stop investing. But if you have equity not doing anything that just went up with the tide, like like that $500,000 in your primary residence not doing anything, I think it’s time to get that out or cash it out or get a new loan and lock in those long term interest rates, especially if you’re going to retire soon and lose that w two documented income. But any other ways you see playing this?

6:31