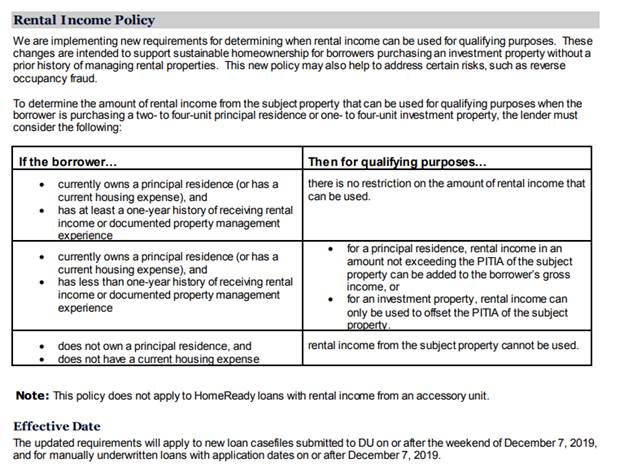

For all you investors still looking to get your own turnkey rentals or direct ownership deals there are some recent changes as of December 2019 on borrowing standards as it relates to how FNMA and FHLMC are looking at using rental income for qualifying.

Basically, if you own/rent currently and have a year history, lenders can use all of the income.

If you own/rent and don’t have a year lenders can offset the payment.

If you don’t own/rent and have no history then lenders can’t use any of the rental income. This could become an issue for some of our borrowers who live rent free and are trying to get into the investment game.

If you need a referral to a lender. Please shoot me an email at Lane@SimplePassiveCashflow.com. I don’t get paid for it (that would be illegal anyways)… I only want to help you get to financial freedom and for you to find your endgame.

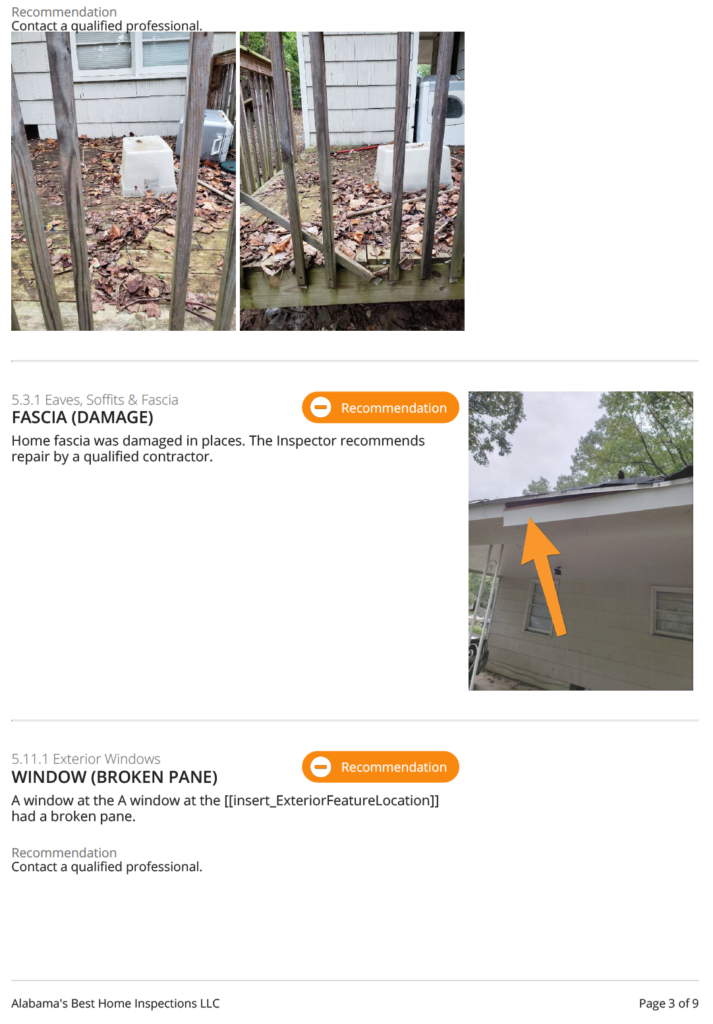

Please submit to me a signed and scanned, Letter of Intent with your Highest and Best Offer. And the name of your property inspector so we can coordinate a showing.

I don’t really have an asking price cause I’m too busy to figure it out. Go ahead an put in your offer assuming items are in stabilized order. If there are any glaring issues we can deduct it and get the deal done. The 5th ave, I just put in 15K of work this past month… it can be sold retail or you can turn it into a turnkey. You are basically buying it from a source (me) where I’m not trying to screw you on the deal and I try to manage issues that come up with the property as efficiently as possible.

And sorry I will not divulge how much leverage I have on this property because it is respectfully, none of your business. Also, I will not be doing seller financing (There were a couple of you who asked). Maybe you asked because it is a past joke of which you tell people “between the lines” to go screw off when someone has a ridiculous price and you inquire about seller financing. Sort of like when you don’t get selected for a job and they tell you they will “put your resume in the file.” Anyway it made me chuckle 😁

I am taking the equity that I built up and is now lazy – SimplePassiveCashflow.com/roe

After selling 7 out of 11 of my turnkeys in 2018 and blowing up my AGI… I am looking to sell the last four in 2019!

Two of my Turnkeys in Alabama are good pickups for you turnkey buyers.

I’m not desperate to sell (so don’t give me anything 10% off fair price)… that’s just annoying and wasting everyone’s time. I think I try to be transparent with everyone that these are solid properties with nothing hidden issues. The neat thing about buying from me is that you know that they are proven assets with a decreased change of buying a dud. Plus you can use my team in place so it would be very turnkey.

I’m hoping we can do a direct sale and save on the commission costs.

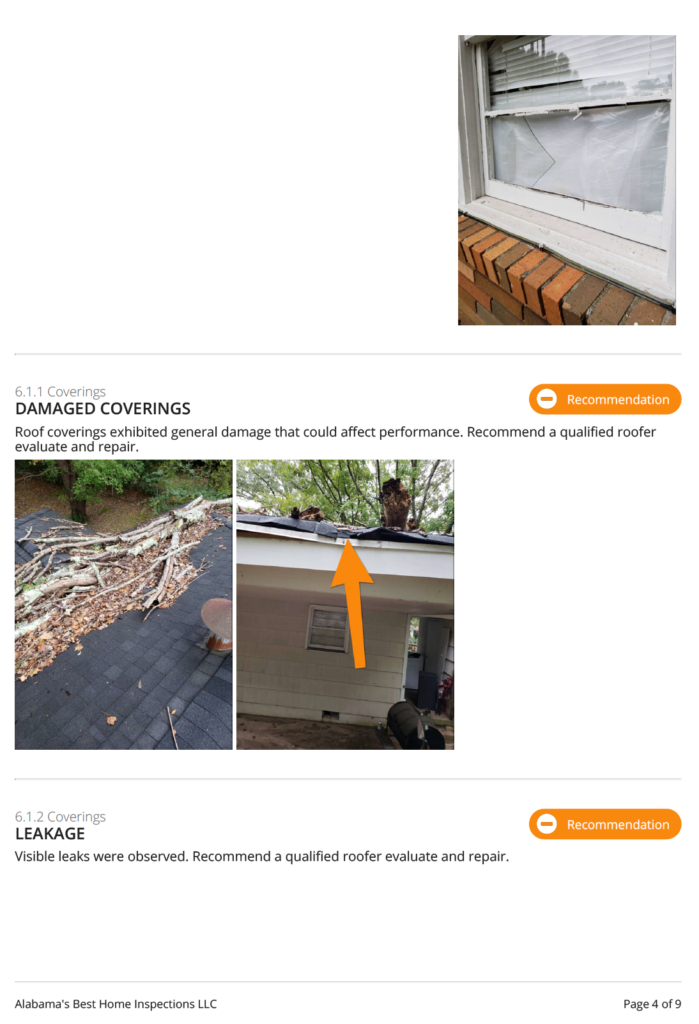

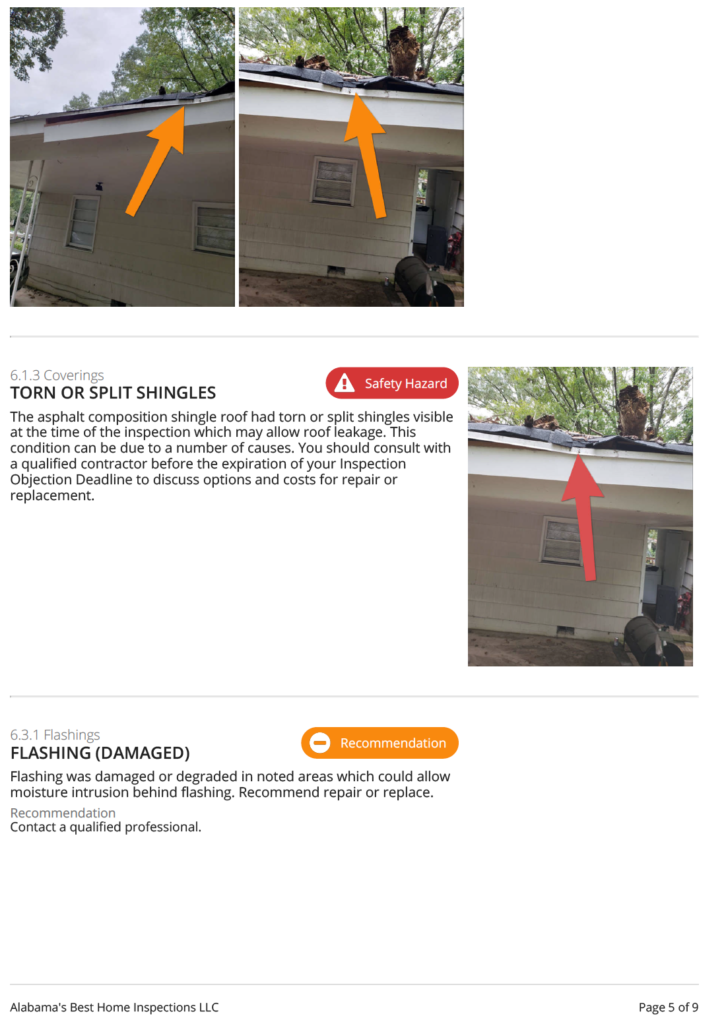

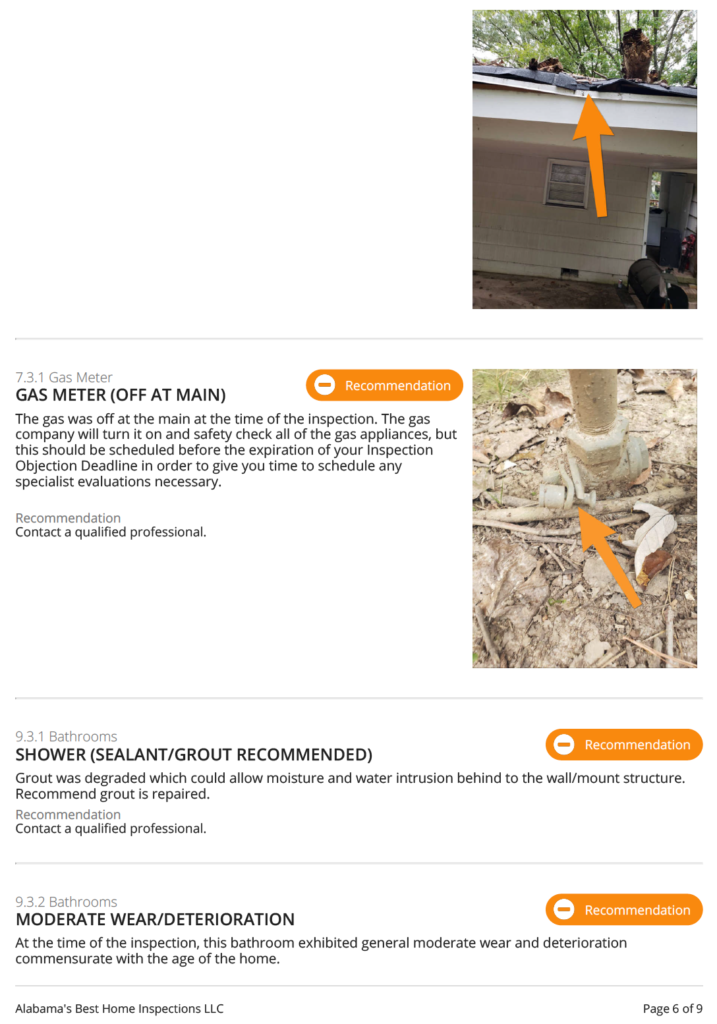

1) 509 20th Ave, Birmingham, Alabama – my most solid rental of all. Still with a renter in there since 2016. Rents are $875 a month.

The average price per square foot is 78.26 you home has 1,008+/- square footage so $78,886.08 for retail sale. But this is a freshly rehabbed. Our plan is to wait till spring February to sell to buyer.

I would encourage you to get your own inspector ($300) and we can split the lawyer fees to sell with title warranty and do the paperwork.

Article Link: Text “simple” to 314-665-1767 to download the Hui Google Drive files and the 2018 Rental Property Analyzer

For a free electronic version of my bestselling book in 12+ categories text the word “ebook” to 587-317-6099.

Please help the show by leaving a review: http://getpodcast.reviews/id/1118795347

Join the Hui Deal Pipeline Club! SimplePassiveCashflow.com/club

Pardon the grammar – I’m an Engeneer, Enginere, Engenere… I’m good with math!

________Here are the Show Notes________

Graham Parham: New Awards:

#1 in units at Highlands Residential Mortgage for 2017

#11 in state of Texas and 92nd in the US according to The Scottsman Guide and

Mortgage Executive Magazine – 1% top originators in the US

Top Ranked – Ask A Lender

Discussion today is 1-4 unit income properties, not owner-occupied.

20% down on first ten financed properties? 25% for 2-4 units?

DTI considerations when using HELOC from primary residence to invest?

Credit scores down to 620. Max. credit score that helps?

Reserves?

New Fannie Mae Reserve Requirements for Investors with Multiple Properties Owned

The Old requirements were six months Principle, Interest, Taxes, and Insurance (PITI) on the subject property and two on all other properties up to 4 leveraged 1 – 4 family properties excluding the primary residence. Properties 5 – 10 would require six month PITI on all properties.

The New requirements are based on a percentage of the unpaid principal balance on each loan excluding the primary residence.

If a borrower has 2-4 financed properties, the reserves of 2% of the unpaid principal mortgage balances are required, excluding the principal residence and the subject property.

If a borrower has 5 – 6 financed properties, 4% of the unpaid principal mortgage balances are required, excluding the principal residence and the subject property.

If a borrower has 7 to 10 financed properties, 6% of the unpaid principal mortgage balances are required, excluding the principal residence and the subject property.

The aggregate UPB calculation does not include the mortgages and HELOCs that are on

the subject property,

the borrower’s principal residence,

properties that are sold or pending sale, and

accounts that will be paid by closing.

The subject property will still have monthly reserve requirements based on the total mortgage payment (PITI). Reserves are funds that you have access to liquid or non-liquid. Reserves are funds you need to have after the closing your transaction. Funds for reserves cannot be your funds for down payment or closing cost.

Fannie Mae now will allow for 100% of the Non-Liquid funds, not 60%

Non-Liquid funds can be used for reserve requirements.”

IRA’s

401K’s

SEP Funds

Gifts are NOT allowed on an investment property.

Investor interest rates how much higher than owner-occupied?

Mortgage sequencing. Example: if buyer wants to buy in Memphis today, Jacksonville next month, how should they plan?

Overall, lending climate more lose or tighter than 1 year ago? 5 years ago?

What should a prospective borrower do before contacting you?

1031 exchanges Cost and funding

What cost are covered in the exchange

What is UP with interest rates?

4 Factors that determine your mortgage interest rate:

Credit Score

Credit Scores Adjustments

740 +

740 – 720

720 – 700

700 – 680

680 – 640

640 – 620

% of down payment 20% or 25%

Loan Amount Adjustments

Property Type

What about the 15 Year fixed?

Does it make since to pay points?

What is the difference between Mortgage Brokers and Mortgage Bankers?

What are overlays?

Does Fannie Mae have a black list?

Are Appraisals regulated and by who?

Is there an appraisal black list?

What happens if the appraisal does not come in a contract price?

Closing cost differences between lenders

Should I pay cash for my investment properties or use leverage?

The next example will show the benefits of using 20% down leveraging for properties versus buying one property and paying CASH.

If you pay $150,000 in cash for one property, your net cash flow is $1245.00. By putting 20% down with an 80% loan to value and a 5% interest rate, your net cash flow is reduced to $600.81. Let’s not stop there. Keep in mind that 20% down payment on a $150,000 home is only $30,000. If you bought FIVE $150,000 homes and put 20% down on each with the same loan terms and monthly rents, you could increase your return on investment by $1759.05 a month to $3004.05. Invest your money wisely.

The net cash flows do not take into account the annual city, county and state property taxes and the annual hazard insurance. The numbers may vary considerately by the taxing authorities. You will have to include that information in your bottom line.

Graham W. Parham has been a Mortgage Loan Officer for over 18 years with 25 years

in sales and marketing. He is a leader of financial expertise in the North Texas

residential real estate market, developing a significant following among homebuyers

and investors. Known and respected industry-wide, Graham’s production consistently

ranks him as a top producer in this market place. According to Scottsman Guide

Graham ranked 92 nd in the US loan originators.

Graham offers invaluable insight into a purchaser’s likely requirements, providing an

exceptional business ethic of customer service and respect, catering to their needs from

pre-qualification to closing. He is a truly dedicated person, who strives to ensure that

each transaction is handled in a timely and stress free manner. By employing these

standards, Graham has established a solid reputation for going the extra mile to put

together the absolute best financing available for his clients. Graham prides himself on

staying ahead of the curve, keeping up to date with the latest products and industry

trends.

As an active investor himself, Graham has a strong insight on what his investment

buyers are looking for to accomplish their short and long term goals. Knowing that

investment loans strongly scrutinized, it is up Graham his team of underwriters who

understands rental property loans versus that of an owner occupied residence. His

general knowledge of REO properties and Turnkey providers coupled with a strong

operational staff allow his loan closings to be seamless and “On Time Every Time”

Highlands Residential Mortgage, LTD. is completely submerged in the real estate

investing industry and has access to many lenders nationally. Our clients benefit from

up to date guidance on all conventional investor loan programs, and less known

creative financing strategies. Knowing that an investment loan will be far more

scrutinized, it is Graham Parham and his team of underwriters who understand a loan

processed for a rental property versus that of an owner occupied residence.

Just as you would not seek legal counsel from someone who does not have a law

degree, nor should you trust a loan originator for your investment property loan from

someone that is not an investor themselves. Highlands Residential Mortgage, LTD. is

an unparalleled mortgage lender whose delivery sets us apart!

Graham Parham’s team mission is to consult every investor based on those

individualized situations and goals. Whether you are buying your first home or

investment property, we carefully look at your options that will give you the best

opportunity for success. Because we know how important your investment financing

strategy is, our extensive research and knowledge of those programs will be brought

forward in educating you as an investor, throughout the lending process.

“My goal is to continue assisting my clients for life and help them meet the ever-

changing needs life throws our way!”

To get access to the lending guide please sign up below:

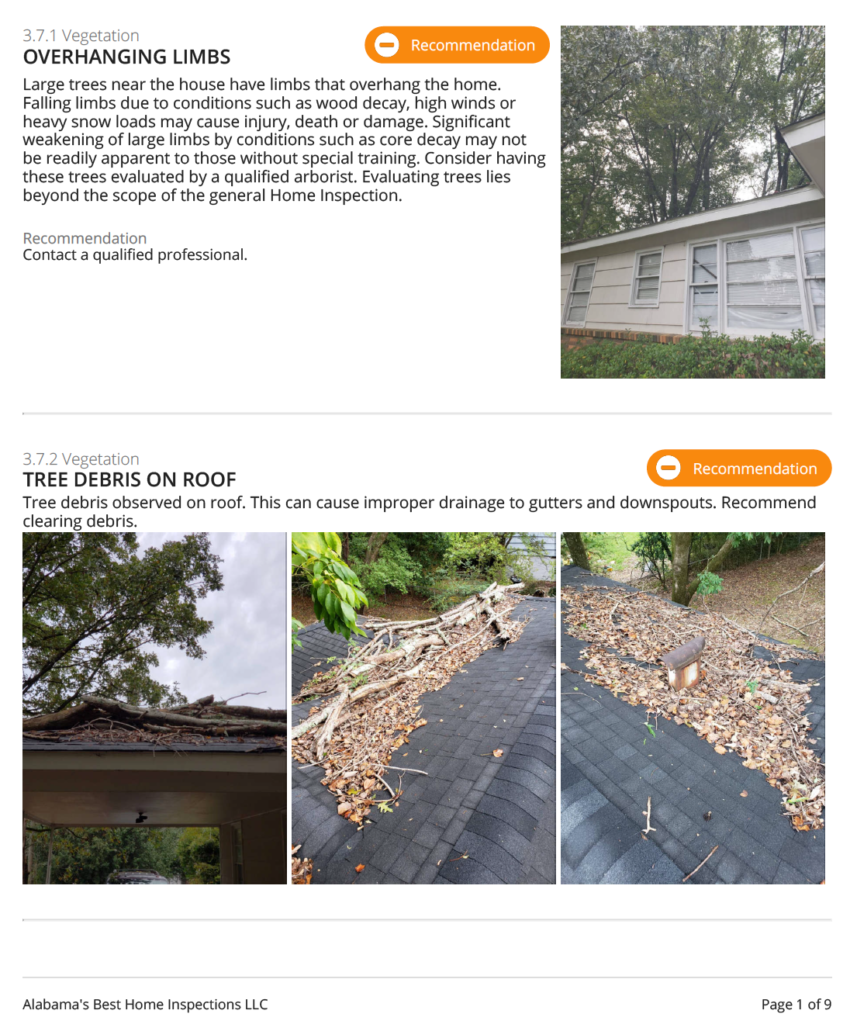

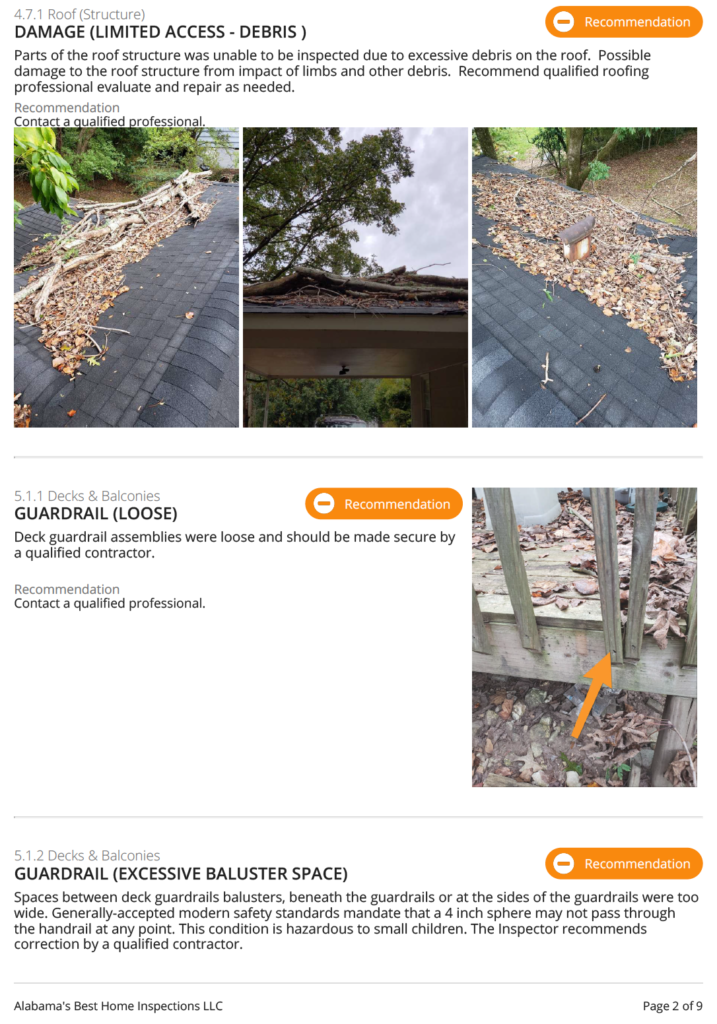

I would say this is a bad report because it’s not Prescriptive. It is very important to have a chat with your inspector so they know it’s not going to be a warm and fuzzy home to live in but a rental property. They will need to avoid citing nitpicky things because the seller is likely another investor and more sophisticated than a regular homeowner and will call BS at your repair requests.

This is where an hour of coaching will go a long way to maximize what you get at the negotiation table.

Article Link: Text “simple” to 314-665-1767 to download the Hui Google Drive files and the 2018 Rental Property Analyzer

For a free electronic version of my bestselling book in 12+ categories text the word “ebook” to 587-317-6099.

Please help the show by leaving a review: http://getpodcast.reviews/id/1118795347

Join the Hui Deal Pipeline Club! SimplePassiveCashflow.com/club

Pardon the grammar – I’m an Engeneer, Enginere, Engenere… I’m good with math!

________Here are the Show Notes________

Jake and Gino have a great podcast and definaetly fit in the category as guys who are growing and doing things right

Let’s work together to redirect money from the Wall-Street casinos and corrupt financial institutions…To help the endangered ‘Middle Class’ savers find safer, more profitable investments in Main Street opportunities benefiting local communities. Join Hui Deal Pipeline Club and check out the sSimplePassiveCashflow.co/mission

Gino Barbaro from Jackandgino.com who focuses on MFH real estate.

Group owns 848 units valued at >$50 million. Expecting to go up this year.

Took 5 years to get $25K-30K/month in passive cash flow.

Fumbling around in the beginning with smaller cash flow amounts, but snowballs over time.

Came from the corporate world to managing a family restaurant. 2008 transitioned to real estate to make better use of time outside of the kitchen.

Highly recommend reading “The E-Myth” by Michael Gerber. Need a visionary, manager, and technician for any business.

Believes you need a Connector, Executer, and the Backbone. Can’t do all 3 – pick 1 or 2 and hire out.

95% of blocks are internal. The rest are external. So, focusing on resolving limiting beliefs and get a life coach.

Google Tony Robbin’s 6 human needs. Have to continue to grow and contribute in a large way.

Relocated to Florida and aiming to obtain $40K/month by end of this year.

Have lifestyle work for his business; not his business work for his lifestyle.

Becoming more efficient by hiring a VA and Digital Marketer for jackandgino.com. Wants to spread content and message; not work on menial tasks.

Focus on 1 or 2 niches for real estate and become an expert at it.

MFH has more barrier-to-entry v. stocks, crytocurrencies, etc. The more people in it, the less profit margin there will be.

Share weekly successes. It’s not bragging, it inspires people and surround yourself with the right people.

Be present in the moment. When you’re at work, with family, etc. focus on dealing with that situation.

Visit www.jackandgino.com. Also on FB, LinkedIn, Twitter, and Instagram. E-mail works too: gino@jackandgino.com.

Question: I am considering investing in a 506c investment on a multifamily property. They are raising a 1 million from investors, then getting a loan and making improvements to the property and repositioning it over 5-7 years.

I wanted to use my funds from my SEP IRA which is currently in a qualified intermediary trust. What is the UBIT tax? Will I be subject to that on this deal? Also, should I set up an LLC that then loans the money to their LLC? How can I structure this for tax and liability benefits?

Answer [Note: From my CPA and not this is NOT legal or professional advice – in other words do your own research]: When you invest in a business (syndicate = business) with your IRA, the IRA will be subject to UBIT (unrelated business income tax) and UDFI (unrelated debt-financed income).

For our purposes, UDFI is produced when an IRA uses debt to purchase real estate. Essentially, the portion of the property’s income considered UDFI is based on the percentage of rental income derived from debt.

For example, Property A is purchased for $100,000. You put down 25% of the purchase price as a down payment and finance the remaining 75% with a traditional mortgage from the bank. The property produces $10,000 in net income for the year. $7,500 (75%) of the net income is considered UDFI and is subject to UBIT.

There is a deduction for the first $1,000 of income subject to UBIT. Income subject to UBIT over $1,000 is taxed at trust rates. For 2017, trust tax rates start at 15% and max out at 39.6% after just $12,400 of income subject to UBIT.

UBIT is paid by the IRA account. If for whatever reason UBIT is paid directly by the taxpayer, the amount paid is considered a contribution to the IRA.

Follow up question: Is there any difference in how the UDFI will apply for these: 1) SD IRA 2) SEP-IRA 3) Solo 401K 4) SD IRA (operated as an LLC) so this one is confusing… My LLC owns an LLC (syndication) which owns a property

I’m trying to decide if one is better than another for tax purposes.

Answer: The solo 401(k) is not subject to UDFI but it subject to UBIT. The IRAs are all subject to UBIT and UDFI. Note that generally the passive income flowing back to you is very low and the as a result we don’t see a huge UBIT tax.

Another idea would be to take a debt position (lending) rather than equity. The interest you would receive is free of UBIT and UDFI tax.

(This suggestion of a “debt” position or note investment with the SEP IRA to avoid UBIT and UDFI tax is a creative one… but it’s a very low chance of happening because it’s just too complicated and honestly not worth the effort from the syndicators side. It’s a very similar case of to a Tenant-In-Common (TIC) arrangement where an investor has 1031 exchange funds and wants to parlay that money into a syndication. It’s possible but from the syndicator’s perspective a lot of unneeded work when you can just raise the funds the traditional way. Caveat: if you are bringing in a huge amount of money say 50% of the raise then that might tip the scales in your favor)

Ask you can tell this is a really grey area. One CPA mentioned, the answer depends on how you structured the syndication, UBIT may or may not apply for the real estate holding for solo 401k. I would really try to toss the Operation Agreement to your individual CPAs to examine and determine ahead of time.

As much as I recommend using a third-party professional property manager. People don’t listen to me and insist on saving a few bucks and being the landlord. If that is the way you want to go then at least screen your tenants.

Introducing the Full-service tenant screening at a discounted rate off the normal $40.00 Package – With Promo Code “SPCF35”

Package to include: • Credit (Detailed VS. Scorecard attached) (Sample Download) • Nationwide Criminal with SSN Verification and Alias Search (Sample Download) • 50 state sex offender search automatically • Nationwide Eviction Search (Sample Download)

As per credit bureau compliance you do need authorization from the tenant to be able to access their credit.

Please click on the link to access the website – There are also step by step instructions attached on how to order reports. If you require the FULL details of a credit report an onsite inspection is required by the credit bureaus (the form has been attached). Without the inspection, you will receive the credit SUMMARY. (Pass/Fail ScoreCard)

Other notes:

Criminal and eviction reports are primarily a NAME match and do not use SSN information to source findings. Look for the middle name or initial and DOB if provided. Eviction and Criminal results can also be cross-referenced with the previous address information from the SSN Verification. The PASS/FAIL recommendations for the SCORECARD Report are currently set at what is considered “Industry Standards”. For more information about SCORECARD pass/fail criteria please give us a call.

Charge-off vs Collection

A charge off is a delinquent account that has been “written off” the creditor’s books (usually for tax purposes). The creditor takes a tax deduction for the loss, and no longer attempts to collect the debt from the consumer.

A collection is an account that is delinquent and has been sold (usually at a discount) to a collection agency. The consumer now owes the collection agency, not the original creditor for the debt.

The scoring system tries to identify bad actors with the following parameters (Sample Download):

INCOME TO RENT: Fail below 3.00 to 1

INCOME TO DEBT: Fail below 2.00 to 1

INCOME TO DEBT INCL RENT: Fail below 1.50 to 1

CREDIT SCORE: PASS above 600…FAIL below 500…CONDITIONAL between 500/600

DELINQUENT ACCOUNTS (24 months): Fail above 5

COLLECTION/CHARGE OFF (24 months): Fail above 2

BANKRUPTCY RECORDS: Fail if has BK within 4 years

These are ONLY recommendations and are not meant to influence your decision, which should be based on the actual RESULTS numbers and YOUR acceptable requirements in a prospective tenant