You print too many dollars and people lose faith in the dollar. The only reason we’re able to pull this off is because we issue the world’s reserve currency and the whole world has to suck up all these dollars. The problem is if someone were to come along like a china and say, hey, we’ve got 20,000 tons of gold, not eight, and we have a big manufacturing economy, and we’re willing to back up our currency with gold, then everybody would move out of the dollar and into gold, and the dollar would collapse. All those excess dollars would come home, and we would end up in America with hyperinflation. And that’s the kicker, right? You hear all the stories about Zimbabwe and all these other countries have ever had hyperinflation, they don’t have that kicker that the United States has. Yeah, I mean, our exorbitant privilege is that we have the ability to print as many dollars as we want, spend as much money as we want, and the rest of the world has to provide it for us because there’s always a bid on the dollar just like there’s always a bid on goal.

Blogs

Repo Market Using COVID as a Cover-up? w/ Russell Grey (Part 1 of 2)

0:00

Introducing the new remote investor, incubator and ecourse we had the mastermind and we are going to break off from that being mostly an accredited investor group. And I wanted to create something that was helping out the little guy get started guys getting their first properties. And we’re calling this the incubator group. Get More details at simple passive cash flow, comm slash incubator, but basically what we’re doing here is we’re getting a group of professionals looking to build your network with others starting this journey to financial freedom, the ecourse that’s going to accompany this group is going to have eight modules in a closed membership site plus two bonus modules and download kit all geared toward educating the remote investor in this group, we’re going to have biweekly zoom video calls. And if you join up, you’re gonna get all past turnkey rental recordings. Now these calls are designed to ask whatever questions you have and hear the other questions from other investors in your shoes and we’re going to run this like a boot camp style. This is going to be a five month program. We’re gonna walk you through the best practices for tax and legal as you acquire your first remote rental. We’re going to walk you through the due diligence and offer process we’re going to have staff membership coordinators for extra support to get you over the sticking points to connect you with

1:16

one of the biggest

1:23

you guys were basically spoon feeding this to you if you’ve been on the fence and it’s time to get your first rental property go to simple passive cash flow calm slash incubator and by the way for those accredited investors, we are looking for new members go to simple passive cash flow calm slash journey and join the flagship simple passive cash flow mastermind there after the pandemic to new world out there having a network around you is so much more important.

1:58

This is the story of About a dude named Lane he moved to the mainland and bought one place to stay. And then one day he went try to rent them out. And then he became one real investor.

2:12

Hey simple passive cash flow listeners today I have Russell gray one of my mentors that kind of got to me where I’m at today. How long has it been almost like four or five years now since we first met I listened to the real estate guys, podcasts. You guys check it out in iTunes, Google Play. It’s one of the few podcasts out there that wasn’t designed to put you into some syndicated deal. It’s more of an educational podcasts that I clicked on to a long, long time ago. And I eventually met up with these guys join their mastermind a few years back and things like there’s so many influences you guys had on kind of what I do today like interacting with my investors one on one phone calls, which I still do, but you guys can still go on the website and book that if we haven’t had a chance to talk but should you say Russell gray, how’s it going?

2:57

Good. Happy to be here. Excited to end Congratulations on your success. It’s always fun when people come into our world and then take the things they learn and act on them. You know, our motto is education for effective action.

3:08

Yeah. And the kids always come back right one of these years I got to come back to the goals seminar, which you guys do I think, what every January, February Yeah, I mean, I originally went to your guys secrets of successful syndication, which is a great precursor on how do you do bigger deals, but I think most people will say your guy’s goals seminar, people who come routinely say, that’s your guy’s best at that you guys put on, you know,

3:29

we don’t do a lot of events where we looked at the marketplace and looked at what people needed and what we felt like we were qualified to do, and we tried to stay in our lane. But you know, after the 2008 crisis, we just thought there was going to be a huge opportunity in private capital and syndication was going to be the way to go. And we didn’t see many people out there really teaching it or doing it and those that were were more interested in raising money than they were interested in and really seeing people become successful real estate entrepreneurs. So we did that course back from the time we were working with anybody Real estate investors and you know, we still do that or you know, encouraging people to be syndicators ultimately real estate, whether you’re doing it in your own account or you’re doing it on behalf of other investors as a business or whether you’re investing passively through a syndicator however, you’re approaching it. It’s just a vehicle to accomplish your goals which presupposes you know what those goals are. And so before you start investing, you need to have a team before you have a team, you need to have a market that you think has the right conditions to deliver the kind of financial program you’re looking for. And before you can pick that market, you have to have an idea what you need your money to do for you. So you need a personal investment philosophy and that personal investment philosophy grows out of your personal goals. So we do that. And then we do the annual summit, usually for 17 years in a row on a cruise ship this last year. We had to do it. We call it summit on screen or somebody in place because we did it virtually but it was great. We had Kiyosaki and Chris martenson and Adam Taggart, G, Edward Griffin and Peter Schiff. And Tom Hopkins, you know, a whole cast of the regular real estate thought leaders that we’ve had. So it was another great event. But those are primarily it. I teach a sales training class once a year that we cancelled this year because of COVID. And the rest of the stuff that we promote are really things that we see other people doing that we think they’re doing well.

5:17

So check out the real estate guys and subscribe to the newsletter, Russell writes it himself. And I thought I’d bring you on and kind of talk about some of these concepts that you’re talking about in your newsletter. And this is what frustrates me about mainstream media is nobody reads more than 500 words, right? Nobody has that capability to do stills it’s always on based on headline. And I guess the first topic I’d like to unpack for people is this repo market. And you know, if you haven’t heard about this before, I mean, I haven’t started to read your content, probably like what the heck is this? Right? Yeah. For people who have no idea what this is, maybe take us back to when this story first broke?

5:52

Yeah. So there’s a lot of components to the financial system. Think of it like an automobile or a big building. You know, there’s different systems. There’s different pieces of substructure that kind of put the whole thing together. And some of it is, you know, you see it, you understand it, there’s like if you get in a car, you see the steering wheel, you can see the controls, you operate the seats, there’s things you see. And there’s a whole lot of stuff going on under the hood and in the chassis that you don’t see. And so the financial system is like that after 2008 when things that were way off the radar of most people, even myself and I was in the mortgage business at the time, you know, these derivatives and mortgage backed securities and collateralized debt obligations, and all these structured investment vehicles and all this stuff that was happening in the bowels of the financial system under the Wall Street gamblers, operating all that machinery, I took a real interest in it and I started realizing like I if I start watching this stuff, I might not understand it. But at least if I see smoke coming out from under the hood, then I’ll know that I should call somebody smarter than me like you know, a financial system mechanic and go Hey, what the heck is this? Well, that’s what happened in September. I saw a headline that interest rates in the repo market had spiked to over 10%. Well, you know, anytime interest rates spike, it’s because people are charging a risk premium. It tells you there’s more risk in the system, you just look at what interest rates are, the lowest interest rates typically are treasuries because you’re borrowing and getting paid back in dollars, and you’re borrowing from the people who issued the dollars. And so they’re considered to be the safest investment you can make. And we could debate whether that’s true or not, but from an interest rate perspective, that’s the way it is. So anything that moves out the rings of risk from that center point of the riskless investment you add interest to as risk premium Think of it like an insurance premiums, that’s kind of way interest rates work. So spiking interest rate tells you that there’s more risk in the system. So it’s like okay, I looked at it so there’s there’s something going on, right because these interest rates are 10 times what they should be and they boomed and the feds response was to pump in 100 $200 billion a day. And of course, you know, we hear these big numbers all the time. And we think they just kind of go in one ear out the other. We don’t have any context to understand. But back at the height of the 2008 financial crisis when they were doing quantitative easing, which was basically papering over bad debt by printing money, they were printing at 5 billion a month, and in September way before COVID-19, way before economic shut down. The Fed was pumping in as much as a trillion dollars a week. clearly something was wrong. So I dug into what the repo market is and just to keep it super, super simple, it’s basically a pawn shop for banks. So imagine a pawn shop, you’re short on cash, and you’re like, Okay, what do I have, I got a, I got a watch or I got a gun or I got, you know, some old jewelry, and you go down to the pawn shop, and you basically sell it to the pawn shop operator, but you have the ability to redeem it in a certain period of time and they charge you interest for the use of the money but presumably, whatever you are Hawking your asset for is important enough that the premium you have to pay to get access to that is there. And of course, the interest or the rate that you pay is, you know, kind of based on the risk. So anyway, so banks are showing up in the repo market and they’re bringing in their treasuries and they’re Hawking them. They don’t want to sell their treasuries or they don’t want to be divested of them who have the right to get them back it basically seeing the banking system is low on cash. That’s what activity in the repo market is and just like maybe you’re not proud to tell all your friends Hey, I had to Hawk my watch, right? the banking system, they’re not like proud that they had to go Hawk their treasuries to raise cash, it’s an indication of dollar shortage in the system. And the Fed accommodated that by printing a lot of dollars, and

9:42

what did they need that liquidity for to pay off their notes? So why did things come to that? Do that

9:47

something’s going wrong. I mean, you don’t know it’s the smoke coming from under the hood? It’s like, Well, okay, nope, we don’t know. I called Chris martenson because he’s a smart guy. And he watches this stuff, too. And I said, Hey, Chris. In fact, I think we did a show on it with him. I know I wrote a couple of newsletters about it. We did a cruise in the news episode, but I’m pretty sure we did a radio show where we actually interviewed Chris martenson. From peak prosperity. We talked about it. And he was in the same place because yeah, clearly something’s wrong. We don’t know what it is. But there’s a lot of smoke coming from under the hood. So we all agreed, hey, this is something we should be watching the indication that there was a real problems when interest rates spiked to 10%. Because when interest rates went that high, that tells you that whoever is bringing the dollars in lending money that they’re fearing counterparty risk, they wanted 10 times the risk premium. That’s the concern is this person may not pay me back. Okay. So that’s where the concern was. And so why would these banks not trust each other? That’s a concern. So you know, nobody knows what the answer is, but they were pumping money into it right up until COVID-19. And then when COVID-19 hit, they pumped money into everything, and this whole repo thing just kind of faded away, but it was really like the canary in the coal mine and the post mortem on what is been going on in the banking system is probably not going to happen until we get to the other end of this just like a lot of what happened in 2008 didn’t come out into, you know, really a public understanding until people kind of sorted through all the rubble and reverse engineered what happened and explained it. And there were a lot of great books written about 2008. I think there’s gonna be a lot of great books written about 2020. But we’re not there yet. This COVID-19 could be and again, I don’t mean to be a purveyor of conspiracy theories, but there are smart people that I hang out with, as you know, and a couple of them are convinced that this is an overreaction to a real disease for the purpose of being able to take extreme economic measures, printing money, spending money in order to cover up a problem that pre existed and the symptom of that problem was what happened in the repo market. And that’s about the extent of it from my perspective.

11:50

If you’ve been following my journey, I’ve been selling my initial real property and transitioning into syndication deals lately. For more purely passive investment strategy. One critic Part of my portfolio is the American Home preservation fund, or what folks in the we call HP for short. George Newbery once apartment owner, operator and mentor to me, is now sponsoring the podcast is private fun, which by the way, also accepts non accredited investors cuts the middlemen out and allows you to invest directly with him to fight the mortgage crisis in America. join him by purchasing distressed mortgages while getting a double digit annual return paid monthly. Find something else better out there. Well, let me know. Feel good knowing that you are helping families stay in their home after buying their underwater note at a huge discount, invest as low as $100 by going to HP servicing comm slash investors. And if you want the free burns on book, please send me an email Lane at simple passive cash flow calm

12:54

Well, that’s your light bill.

13:01

Yeah, so when people say, you know, the Fed is printing money, right, where does the money flow into like bank stocks or

13:07

Yeah, so technically they don’t print money. There’s a fairly infamous or notorious interview Ben Bernanke on 60 minutes, probably back in 2009, or 2010. Trying to explain quantitative easing, and in the one breathy saying we don’t print money. And on the other breath, he’s saying it’s effectively like printing money. But what it is, is they just add digits to a computer screen. So it’s all digital. They just they conjure these numbers out of thin air. And the way they put the money into play is they purchase treasuries. So the US government needs to spend more than it brings in which it’s very good at so that it can issue new treasuries. And when those treasuries are issued, they’re sold on the open market through market makers and those market makers individual investors around the world sovereign wealth funds, governments, other central banks. All by treasuries for their reserves, the Federal Reserve manipulates interest rates by bidding on those bonds also through their FOMC, which is the feds Open Market Committee. And what they do is they set an interest rate target. So when the Fed comes out and saying, Hey, we’re we’re lowering the interest rate, what they’re doing is they’re lowering their interest rate or changing their interest rate target. And the target is what they’re aiming at doesn’t necessarily mean what they hit. And they certainly don’t dictate to private lenders what rates should be. But again, if you go back to my early explanation, that treasuries are at the center of the rings of risk for interest rates. If I raise that interest rate at the core, then everything else outside pushes out, and rates go up. So if that ring that the Treasury is in and the interest rates shrinks, then everything that has a risk premium built on it shrinks to and so mortgages are a ring of risk out from treasuries they’re considered To be very, very safe, but not as risk free as Treasury. So mortgage rates are higher than Treasury rates. And if Treasury rates go up, mortgage rates go up, if Treasury rates come down, mortgage rates come down, alright, so the Fed goes out and they they print money out of thin air actually conjure money onto their computer system, and they bid on the bonds in the open market. And in order to drive the rate down, they have to bid the price up. So it’s just like cap rates on apartment buildings. If your audience is primarily real estate investors as ours is, then they understand that right if I go buy a property, and it’s got a five cap, it’s listed as five cap and it sells for a four cap. It isn’t that the rent changed, it’s that the somebody bid the price up, they bid the price up higher, which means that the return on invested capital the purchase price went down. There’s an inverse relationship between yield net operating income and a cap rate. There’s an inverse relationship between the cap rate and the price of the apartment building, the higher the apartment building price, the lower the cap rate and vice versa. Same is true with treasuries. So the Fed creates interest rates by bidding on those bonds bid it up drives interest rates down. So that explains negative interest rates. Because you say, Well, why would anybody buy a bond at negative interest rate? Because they’re convinced that the Fed is going to come in and bid even more for it. They’re speculating on the price of the bond. They’re not buying the bond for the yield, there is no yield. They’re buying it knowing that the Fed is going to buy even more, and I could tell stories about that out of the news, but I’ll let that lay. Did that answer your question? Lee?

16:35

Yes. So manipulating, so when they create like a $2 trillion stimulus package? Is that their mechanism for putting cash into the system?

16:42

Yeah, well, they buy the treasuries and then the government spends the money. So there’s there’s what’s called a fiscal stimulus, which is when the government and the Federal Reserve and the government are not one in the same if you’re not sure about that read the creature from Jekyll Island G. Edward Griffin does a great job explaining it but the Federal Reserve A private banking cartel and they have a contract or a deal that’s baked into the 16th amendment that allows them to issue the currency instead of the Treasury. That’s why you have Federal Reserve Notes and not Treasury notes, or treasury bills. And they then manage the money supply theoretically, outside of political influence. They’re supposed to be independent. So this was what the system was set up in 1913. Of course, it’s like most systems changed quite a bit over time. And some could argue it’s become a bit corrupt and politicized, but be that as it may, the Federal Reserve prints the money and then they give it to the government by buying the bonds. And then the government puts it into circulation by spending the money. So monetary stimulus is the Federal Reserve, lowering interest rates, which is effectively meaning they’re going to print money to buy more bonds, but it has to be married to fiscal stimulus, which is where the government spends the money and puts it into circulation. And of course right now both of those things are happening. We have a thing Three and a half trillion dollar deficit. So we’re spending gobs and gobs and gobs of money. We’re injecting it directly into people’s bank accounts. And the Fed is printing trillions and trillions of dollars. In fact, I read an article the other day that the Fed has purchased 100% of all Treasury issuance, in other words, every IOU every bond, every borrowing that the federal government has done in 2020. The Fed has purchased China hasn’t purchased it. Japan hasn’t purchased it. private investors haven’t purchased it. Nobody’s purchased it. But the Fed net. I mean, there’s been trading for sure, but net net, the Fed has printed more money or as much money as bills have been issued or notes have been issued by the Treasury. So that’s it. That’s how the money gets in play. Now they’re buying ETFs you know, Bond ETFs are buying commercial mortgages. They’re putting money in through Fannie Freddie. So they do it by funding credit markets. The short answer, maybe I gave too big of an answer, but the short answer is they print money out of thin air, and they purchase debt instruments in the credit markets, primarily treasuries, but now money Other things, and then that money finds its way into circulation, we’re probably a hop skip and a jump before they start buying equities, stock ETFs and so on to prop up the stock market. It’s a full court press to prevent asset values from collapsing because that’s a natural reaction to a cessation of economic activity is asset prices collapse problems when asset prices collapse? It takes credit markets with it, because debt goes bad and that’s the big risk right now.

19:27

So when COVID hit and people lost a third of their portfolio in their stocks, and then it kind of bounce right back up. Is that a byproduct of just more money flooded into the system and not really what the headlines on Yahoo Finance says that, oh, people are sentiments getting better. What’s

19:45

the I mean, that’s ridiculous. I mean, get the Atlanta fed coming out going GDP is going to be negative 40 or 50%. They’re coming out with these unprecedented unbelievably horrible things. We got 40 million or whatever people unemployed, right? Unemployment rate. And then the Great Depression, there is no logical reason based on earnings for companies to stock to be going up. There’s nothing that looks good economically. The stock market though, has become a proxy or a barometer in many people’s minds for economic health. And it’s not true. And of course, it creates a huge amount of income or wealth inequality because the people who own stocks are the beneficiaries of the free money and the people who don’t are on the outside looking in just watching the cost of food and other things that they need go up. So there’s a reason why a lot of people are angry right now whether they understand the economics underneath the disparity or not, but this isn’t a left or right issue. This is a big government, big banking system, big corporation. It’s the big guys versus the little guys and the little guys get crushed when these types of games get played.

20:51

So right now we kind of establish that something’s happening. Something’s under the hood that’s smokin and I just want to kind of speak to little guy, the person listening on the podcast right? Now they’re going to hear that and they’re going to say, Oh my goodness, maybe I should put everything in gold or put cash under my mattress or dig a hole. Well, what’s the real play here, especially for guys who have less than a million dollars net worth, you can’t just buy gold, you got to grow your money to

21:15

well, gold is not an investment. And gold only preserves you against the failure of a currency. So I think the first thing is to understand the context and kind of the sequence of events as this thing rolls out. So we had a health crisis, whether it was real or perceived, whether it was overreacted to you can’t worry about that. The fact is, they shut the economy down worldwide and they’re opening it up very slowly, and maybe it’s going to be open it up a little bit and pull it back. The short of it is the health crisis led directly to an economic crisis and the economic crisis means businesses stop generating revenue, employees stop getting paychecks, which means that businesses and employees that have debts can’t To service those debts. So there’s been some temporary injections and some getting out in front with forbearance agreements and workouts and all this different stuff that’s been going on unlike how they handled 2008. But at the end of the day, those are temporary stopgap measures intended to keep the wheels on the bus until economic activity can restart. It’s kind of like being put on a heart lung machine until you can start breathing and your heart starts beating on its own. That’s where we’re at. We’re on life support, and that life support is coming directly from the Fed. So the economic crisis is the cessation of cash flow, think about having an economic heart attack currencies not flowing because people aren’t able to buy they’re not able to go out they’re hesitant to spend, they can’t make payments, right that that’s an economic heart attack. That’s where we’re at the next level is a financial system meltdown. And that happens when the banking system and the bond markets and credit markets begin to fail. There was some indication there were problems in those markets. For as we talked about in the repo market, they needed huge injections of cash. So there was already problems all COVID-19 was did was accelerate what was already happening and maybe provide cover for an extreme reaction that maybe they wouldn’t have been able to pull off outside of a very visceral, very visual, understandable crisis. People don’t understand financial crises. It’s all geek speak. But you can understand if you go out to the grocery store, and everybody has masks on and you can’t stand the six feet apart and all the restaurants are closed, all sudden, it’s like very conscious, hey, there’s a big problem here. And if you tend to believe the narrative, then you accept it and you accept whatever needs to be done to fix it. Again, I’m not saying that there’s a nefarious motive behind it, but I’m just saying people are a lot more forgiving. Of these extreme debts. Extreme spending measures extreme expansion of the Fed’s balance sheet because they are believed Meaning that we’re in the midst of an unprecedented crisis. And the idea is that extreme times, you know, require extreme measures. So health crisis to economic crisis to financial system crisis where the credit markets collapse, like we had a mini financial crisis in 2008. Here’s the next crisis in order to save the financial system. And to put the economy on life support, the Fed is printing and the government is spending trillions and trillions and trillions of dollars. So to give you kind of a historical perspective, in the entire history of the United States up until 2008, or the entire history of the Federal Reserve from 1913, up to 2008, almost 100 years, they grew their balance sheet to 800 billion after the financial crisis of 2008. By 2012 or so their balance sheet had grown from 800 billion to 4.5 trillion. They tried to taper and they tapered it down to 3.7. They raised it or tried to raise interest rates by 50 basis points half a percentage. And the result was the stock market started to retreat and the economy started to slow down. And so they realized that was going to be a problem. And so they lowered interest rates and they stopped tapering. Soon as COVID-19 hit their balance sheet has exploded to over 7 trillion. So it’s more than doubled since COVID-19. The last four months, the Federal Reserve has gone from 3.7 to over 7 trillion that’s all freshly printed money that is, is working its way into the system. It’s propping up the stock market. It’s keeping interest rates down when there’s tons of risk and people should be charging a risk premium, but you can’t because there’s too much debt in order to stop all that they’re printing dollars. Here’s the thing if you print too many dollars, and people lose faith in the dollar, now you’re Zimbabwe you’re Venezuela. Going back in history, you’re why Mar Germany, the only reason we’re able to pull this off is because we issue the world’s reserve currency and the whole world has to suck up. These dollars problem is if someone were to come along like a china and say, hey, we’ve got 20,000 tons of gold, not eight, or four, and we have a big manufacturing economy and we’re willing to back up our currency with gold, then everybody would move out of the dollar and into gold, and the dollar would collapse, all those excess dollars would come home and we would end up in America with hyperinflation.

26:25

And that’s the kicker, right? You hear all the stories about Zimbabwe and all these other countries have had hyperinflation. They don’t have that kicker that the United States has.

26:33

Yeah, I mean, our exorbitant privilege, if you will, is that we have the ability to print as many dollars as we want, spend as much money as we want. And the rest of the world has to provide it for us because there’s always a bid on the dollar just like there’s always a bid on gold. So people who are buying gold right now we’re buying it as an alternative to having something liquid that hedges against $1 collapse or Just a continuation of 113 year, a downward spiral of the dollar, right. That’s why people own gold, but you can’t gain purchasing power with gold, you only retain it which is worth doing. But when you pair gold with debt, now that’s different. Let’s say for example, I go pull a couple hundred thousand dollars out of a piece of real estate, and I take half of it and I put it into gold, and then the gold doubles in dollar price because of inflation. Now my gold will pay off all my debt and so the debt and the dollar go together. And the problem with going into debt to buy gold is you have to make the payments unless the thing that you go into debt with provides the payments. Now can you think of a vehicle that you can purchase with debt that actually provides the payments to make the payments can you think of one

27:45

of these couple of guys, they built their whole platform on real estate?

27:50

Real Estate and so what I found is that I’ve kind of crossed over and become this bridge between the gold community and the real estate community from a financial strategy. perspective and when you pair gold with debt and real estate, now you have a chance to outperform in an environment where the dollar is falling. And so that to me is the way to play this game right now because all of the pressure to support the entire global economy is landing squarely on the dollar

28:23

this website offers very general information concerning real estate for investment purposes every investor situation is unique. Always seek the services of licensed third party appraisers and inspectors to verify the value and condition of any property you intend to purchase. Use the services of professional title and escrow companies and licensed tax investment and or legal advisor before relying on any information contained here. Information is not guaranteed as an every investment there is risk. The content found here is just my opinion and things change and I reserve the right to change my mind. Above all else, do your own analysis and think for yourself because in the end, you’re the only person who is going to look out for have your best interests.

How can I use part of my Roth IRA to buy passive income property?

How can I use part of my Roth IRA to buy passive income property, what you’re going to need to do to investor author is you’re going to need to probably move over to a IRA custodian that allows you to self direct. Now, a lot of these guys like Vanguard or fidelity was at something America with these big firms that offer investment options. They have what I call a fake self directed IRA accounts. We’ll call it self directed IRA accounts, but all it really does is allow you to invest in dirt or other garbage mutual funds and stuff like that. They’re not true self directed IRA accounts, what you’re trying to find as a self directed IRA custodian, such as you know, a lot of our investors will use quests, I used to use IRA services, they’re pretty good, cheap option, but these guys they’re just custodians who just hold on to your money and they administer the money. Once you get the money to these guys, then you can invest it or where you want. Of course, there’s you know, you have to follow a prohibited transaction. rules you can Google that I think you can’t buy things like artwork, or there’s all this list of like things you can’t buy. But if you’re buying income property, you should be fine. Some things to know when you’re transferring from your current IRA company to the IRA, self directed IRA custodian, it’s going to be hard, these guys aren’t going to make it easy for you, you know, you’re breaking up with one company, the customer service on that end is not going to be as good as it was on the way and so it might take two or three months, or two or three weeks of you constantly kind of badgering them. But once you kind of get it out of there, and you have it in the account, some of them will set up like a checkbook IRA, where you can just easily make or write a check. The one I had, I had to do all this paper, you know, a couple pages without what I was investing in, and then the key is that they they’re sending money on your behalf and you’re kind of staying out of it so that you don’t blow up your IRA account. I personally am not a big believer in any retirement accounts, Roth IRAs or Any pre tax IRAs unless your net worth is over two to $4 million. At that point, maybe you should do a Roth, a lot of like syndication deals and just real estate in general, you get a lot of good tax benefits from depreciation that comes from the property. When you’re investing within a IRA account or retirement account, you do not get to partake in those advantages. Another reason why I don’t like IRA accounts is because you have to wait till you’re like 60 or 70 years old. I’m trying to live for today I want to, I’m trying to I’m buying income property so I can create mini pensions today and work backwards and create cash flow today that grows and grows and grows so I can buy more and more investments so I can grow more and more. I am probably going to reach retirement, the pinnacle of retirement what we all think, which is more of a financial freedom number well before I hit 60 now not saying that’s for everybody, but I think for a lot of us who are investing the right way, it usually takes five to 10 years of doing this method. To be out of the rat race, and at that point, you’re not going to want that money locked up in some Roth IRA account or IRA. So that’s why a few years ago, I made the conscious decision to never invest in that stuff ever again and I just invest out of my own liquidity out of cash accounts.

Sheltering Capital Gains Without Painful 1031 Exchanges

So I’m cashing out some of my real estate that was inherited because the net income is very low given the asset value considering cashing out on a property that I bought 30 years ago in Arizona even though the rent ratio is amazing the income to asset ratio is low thought is to hold on to cash and wait for a buying opportunity which seems to be coming however, we’ll end up with a 30% capital gains federal and state on 500 to 600 thousands of capital gains the first thing I always ask folks like this is like what’s the rent to value ratio fits under 1%? Well, it’s not going to cash flow so you should probably sell it It could appreciate but that’s just not what the kind of investor I am I want the Sure thing which is cash flow as opposed to hoping and praying and gambling that the property value is going to go up. Somebody might get lucky and rub it in my face but you know, I’m more about cash flow and and that type of stuff these days. Once you’ve determined that you got to sell the property

You got to figure out how much capital gain you’re going to have. And this person mentioned, they’re going to be looking at 500 to $600,000 in capital gain. Now you have a couple options. You can do a cash out, refinance, buy some other properties, maybe you go into some syndications. And then you build up some passive losses from those syndications and then sell the property and then realize those capital gains. But by doing that strategy, you’re able to build up the passive losses that kind of cushion your fall, there’s a 1031 exchange option, but I think 1031 exchanges are pretty horrible because think about like this analogy is like you’re kind of in a in a hot air balloon, you’ve been in this boom for 30 years, and you’re now you have to look at like a 500 to $600,000 capital gain or dropping of air balloon, you’ll probably break a bunch of legs at that point, but by doing a 1031 exchange, you’re kind of delaying the inevitable you’re going to be in the situation again, but unfortunately, you might be looking at a 1 million or a million and a half capital gain way. I think

Kind of kind of mentor my folks who’s like just cut bait Now jump out of the basket. And you might break a leg leg or sprained ankle, if you’re at a height of like 50 feet. $100,000 is a lot of capital gains. So likely, what you’re going to need to do is cushion your fall. And in this case, practical advice is to go into some deals, get some passive losses to cushion your fall, maybe you invest $100,000, and you get a $98,000 in passive losses that first year and you go into three deals like that to you now you’re almost the $300,000 cost of losses. Now you take that $500,000 long term capital gain, and you minus that passive losses, and now you’re only looking at a $200,000 capital gain. At that point, say your adjusted gross income was 100. You know, you add that to the 200 and you’re at 300. You’re not in a bad tax bracket at that point, if you kind of sheltered the big stuff out of the you know, $326,000 and above that, those are

A couple ways of doing it. Every situation is different but that’s the way I would think of it. You know, we talk a lot about this stuff in our in our mastermind group about, you know, strategizing specifics about this one piece of the puzzle I don’t have that this person didn’t put in here. It’s like, I want to know what your adjusted gross income because maybe you’re not working this year and your AGI is really low. Well take it out. Take just take the capital gain hit on the chin

How to invest proactively in a Pandemic?

Get more insider news and full webinars =>

See Investor Club Only Content

https://youtu.be/2Fs7CYzzGrMhttps://youtu.be/4eVAskRng9Q

Source: Richard Duncan

Our government is giving huge tax incentives for those who invest into our country.

https://youtu.be/aqPWoki-MP8https://youtu.be/FTj-nJEGi-4

What is making the stocks go back up?

The country effectively shutdown for half of 2020, unemployment is high (expectedly so with a slow ramp up), yet the stock market is on track to be at all time highs by the end of the year?!? WTF?!?

Call me crazy but this sounds fishy!

|

In case you missed it at least 3 Trillion dollars of economic stimulus has been flushed into the system. Could this be what is pumping the stock market with fake money? When is the air going to be let out of the stock market again? Do you remember how you felt back in March 2020 when stocks lost a third of it’s value? Don’t forget that. The Cares Act now allows for a 100k withdrawal from your 401k or TSP penalty free till the end of 2020 and possibly till you file your taxes in 2021. This is the time to get out of frothy paper assets and into real hard assets. |

| Never forget! Do yourself a favor and get out of fake assets and into real assets that produce cashflow. |

https://youtu.be/2t6t4Lw5Mu0https://youtu.be/UrSzupI0H28

Why real estate? Is this another 2008?

The great Recession of 2008 was a systemic failure in the real estate market caused by bad mortgages, rampant home flipping and speculation, and overbuilding all contributed to the last financial meltdown.

NINJAs (No income no job no asset) were being approved for multiple home loans on the belief that housing prices would just keep going up and these loans were packaged off and sold as Wall Street derivatives.

https://youtu.be/iDcbUAh731s

Today, it is difficult for even high paid professionals like you to qualify for Fannie Mae/Freddie Mac loans. Credit scores need to be higher, debt-to-income ratios need to be lower, and lenders verify incomes much more carefully. Join our Remote Investor Incubator and we can connect you with the lender that we use.

This time around, there is a growing demand for affordable rentals housing due to increasing population, less homeowners, and the constant separation of the haves and have-nots 🙁 the much-stronger housing market isn’t the driver of the crisis—it’s the effects from COVID-19 a medical crisis. It is a true Black Swan event.

What Could Cause the Stock Market to Fall?

- A severe second wave of the Coronavirus

- Insufficient additional Fiscal Stimulus (which would make the bad economic fundamentals even worse)

- The possibility that the markets have already priced in all the impact that the Fed’s new money creation will have on stock prices

- If the Fed signals it will create less than $120 billion a month, a new “taper tantrum” would be likely to cause stocks to plunge

- A political crisis in the run up to or the aftermath of the November Presidential elections

- Any number of other unforeseen developments

Is this a time to sight tight and not invest?

You could do this and make 0% on your money or load it into deals that make sense, tie up good long-term under 4% debt, and hedge against inflation as the country looks for revenue sources such as taxes or debt minimizers with inflation.

I have taken a “load and stabilize” approach to my investing where I…

- Load into some good deals (one at a time or every few months)

- See them stabilize (harden into recession-proof after a few months)

- Repeat the Process

Some may even see this as the “dollar-cost-average” approach which is similar to what were taught in stock investing 101.

I have seen pricing on assets increase every year since 2009.

I felt what you are feeling back in 2012… if I would have stopped I would have missed out on another great run!

I felt what you are feeling back in 2015… if I would have stopped I would have missed out on another great run!

I felt what you are feeling back in 2018… if I would have stopped I would have missed out on another great run!

After seeing this phenomenon happen for a few times and seeing a lot of people who never got started, I realized and had proof of concept that as long as I go into conservatively underwritten deals that cashflow I am pretty much untouchable or going to do a lot better than waiting on the sidelines.

Accredited & LP Investors – Join the Mastermind

| Collections Post-Covid in comparable Assets we operate: |

COVID19 came and I was a little worried to see how April and May collections were. But collections remained strong and came down only 2-8% across the 3,500 unit portfolio. In some assets, collections improved! Commercial real estate pricing was pretty much unchanged and experts say that at most Cap rates went up only 0.25%. (Excluding commercial retail storefront and short term AirBNB type rental who got killed)

Now, you can see where I am coming from in my neutral-aggressive stance.

Combine that with the fact that I am around higher level Accredited investors these days who have seen the ups and downs and they say NOW we see the separation between the faint of heart and those who take their family’s legacy to the next level.

Of course… don’t be silly and choose investments in good sub-markets and have sound underwriting to ensure cashflow.

Warren Buffet said “be fearful when others are greedy, and greedy when others are fearful.”

John D Rockefeller said “The way to make money is to buy when blood is running in the streets.”

The Fed has pretty much doubled down and planning for additional stimulus plans which is ensuring the nation moves past the current COVID crisis with Infinite Quantitative Easing commitments through the year 2022 and beyond. Get on this wave now!

Source: Richard Duncan

https://www.youtube.com/watch?v=M8jJ2iiDMes&feature=youtu.be

We were able to get a lot of interior footage on Harbor Village units on this last trip out to Huntsville!

Also included are drone shots of all recently acquired properties.

2nd half of video is Garden Place and upgraded and non upgraded units in Treehaven which are our other class C properties.

Now what?

Let’s reconnect, huddle up, and get a game plan for you as this is we start to build a legacy!

If we have not connected use this link to setup a time to chat that works best for you.

The population is still going up…

Between 2010 and 2017, population growth averaged 5.5% for the US as a whole. Delaware boasted the highest growth rate, 15.3%, over these years. A state with a relatively small population, however, needs fewer new residents to achieve such a high growth rate. The double-digit rates recorded by Texas (up 12.6%) and Florida (up 11.6%), both high-population states, are therefore that much more impressive. There were three states that posted population decline between 2010 and 2017: West Virginia (down 2.0%), Vermont (down 0.3%), and Illinois (down 0.2%). – ITR – 19.02.28

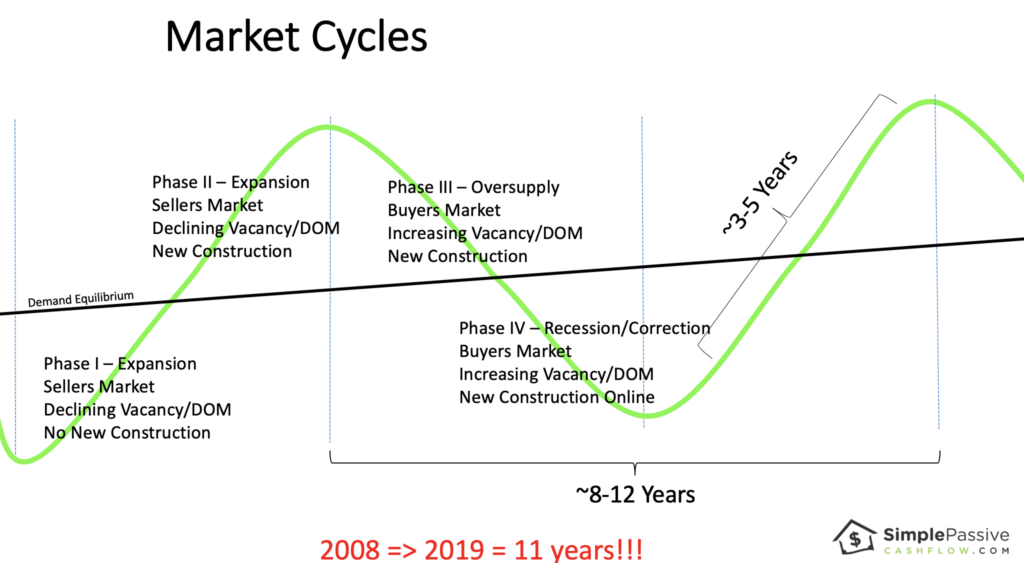

Since I feel we are in the 9th inning of an 11 inning ball game, I decided to pass on a recent Class-A apartment deal in a secondary market.

Here is my thought process…

First off, Robert Kiyosaki has a saying: “There are three sides to a coin.”

People like to argue that it is either a good time to buy or a bad time to buy. For example, they say that “MFH” is overheated or commercial is getting killed by Amazon and e-commerce. I think these are mental justifications by tire-kickers who are scared to act. I mean really how many of these people are under the accredited status (not sophisticated) or have not obtained their “Simple Passive Cashflow number.”

Lane Kawaoka

Simplepassivecashflow.com

Sophisticated investors still trying to grow on the edge of the “coin.” They buy deals out of the reach of amateurs due to the amateurs’ lack of network/knowledge. These opportunities are undervalued, with undermarket rents, with value-add opportunity. Sophisticated investors are patient; they don’t stray from standards that force them to get crushed in a market correction. (Cashflow from other investments makes this possible.) They invest following the macro- and micro- trends and don’t gamble on gimmicks such as guessing where Amazon’s next HQ is going or where the hurricanes just drowned a market. The trouble is that an unsophisticated investor or an outsider (in terms of having a poor network) is figuring out which of these deals transcends the two sides of coin and is on the edge. Stating the obvious (though often ignored by many)… starting out as an investor is going to be slim-pickin’s due to the lack of network. But you have to push through this rough part. You are not able to decode the noise until after a few deals or having someone mentor you.

The trouble is that an unsophisticated investor or an outsider (in terms of having a poor network) is figuring out which of these deals transcends the two sides of coin and is on the edge. Stating the obvious (though often ignored by many)… starting out as an investor is going to be slim-pickin’s due to the lack of network. But you have to push through this rough part. You are not able to decode the noise until after a few deals or having someone mentor you.

Get the Right Mentor – Join the Incubator

High Net Worth Investors – Join the Mastermind

With that out of the way let’s continue…

Real estate is one of the best risk-adjusted investments out there. In private placements or syndications, we are able to crowd-invest in larger & more stable assets while maintaining control with operators who are aligned in our best interests. By going into a project properly capitalized with adequate capital expenditure, budget, and cash reserves, you are able to remain steadfast through softness in the market where rents stagnate and vacancy decreases.

(If you are starting out you should start with turnkey rentals even though they are much more 🎥 volatile)

Pause there. In troubled times what happens?

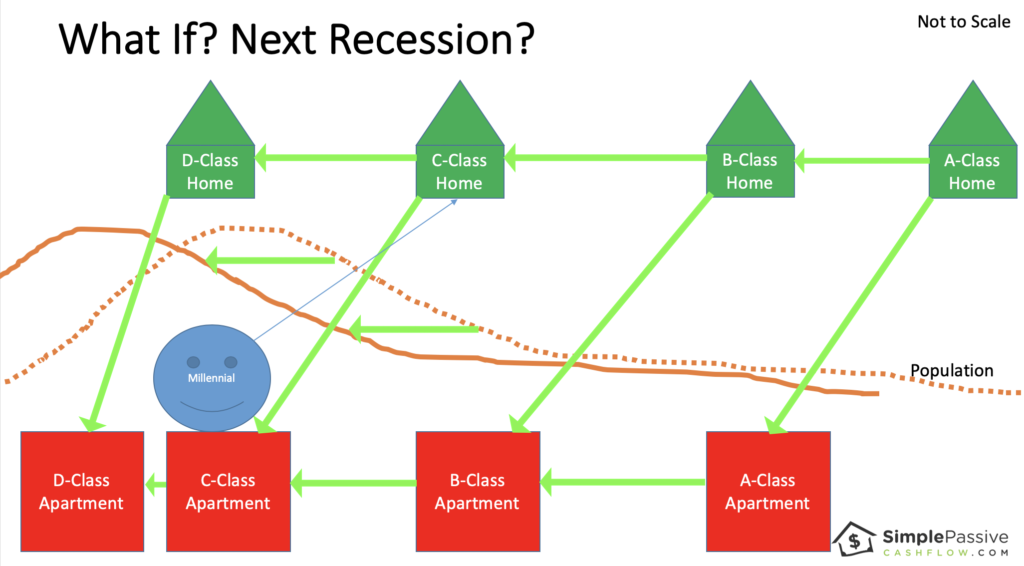

People lose their jobs and there is a bit of shuffling, let’s take a look at different the different property classes:

Previous

Next

Yea, people need housing, but there will be some vacancy as some people will lose their jobs and be displaced elsewhere.

Following this train of thought…

In a recession, the high end or class A will be hurt the most. It is Class A workers who fulfill much of he discretionary services. We are already seeing softness in rent by rent decreases in class A of the high-end markets such as Seattle and San Francisco.

For example a once $1,700 one bedroom is now $1,625.

Most deals model for 1-5% in annual rent increases or escalators. Other than the Cap Rate to Reversion Cap Rate truck, this is the second most manipulated assumption in investment modeling.

In this unfortunate but natural event, the A-Class renters will fall to class B housing. Some homeowners will even lose their jobs creating foreclosed investments for smaller investors in the single-family home scale.

What’s happens to the B and C class renters?

It is likely that they will also lose their jobs at higher or lower rates, but that is up to debate. In the same fashion as the A-Class renters, the Class B/C renters will downgrade to make ends meet.

I imagine this similar to a game of musical chairs (where the chairs are getting crappier and crappier). Or it looks a lot like the natural housing shuffle in the summer near colleges with people moving in and out. The landlord/investor is likely to see increased vacancy.

Multifamily occupancy varies from 85-95% in stabilized buildings. Some markets are hotter and some are colder. It is important to use the correct assumptions depending on the markets. For example, Dallas typically sees 92% occupancy while Oklahoma City sees 89%.

One of the reasons we love multifamily is because of the decline of the middle class and the need for more scalable workforce housing. [And those millennials can’t save] The population is increasing too.

[I like to use this image cause I make fun of millennials… this is the millennial version… cause they can’t seem to afford (or want) to own anything]

When I travel to Asia (which I see as a more mature society, for better or worse) there is a much larger wealth gap than in the USA. People are living in cramped apartments or very rare single-family homes. And they are driving a Mercedes on barely enough money to share a family moped. This is the trend that the USA is following.

As with many things, you need to look past the headlines and the general data. Instead of analyzing a whole asset class, as the media likes to do, let’s break down vacancy in terms of classes.

Here are some typical vacancy rates (notice the spread).

Class C 4.5%

Class B 5.0%

Class A 5.5%

Why? Because there is just more demand for the lower class properties because there is more demand than supply.

Many times the business plan is the be the “best in class.” For example, businesses want to be the best mobile home park or best high end remodel because you attract the richest customers in that niche.

I like to monitor the number of new units coming online because that is your downward pressure. It is rare that new builds are for Class C or Class B.

The micro-unit trend is an attempt to build for Class C and B tenants due to the need. But often the numbers don’t make sense when you have purchased the same building materials and mobilized the same crews to build a Class B asset as opposed to a class A asset.

Let’s go through that Armageddon example again.

Class A will have to drop rents severely and see great vacancy.

Class B and C will see vacancy come up too as people are losing their jobs but should see some absorption from ex-A Class tenants.

Mom and dad will also see some absorption as deadbeat son or daughter move back home.

Get that first Remote Rental – Join the Incubator

Build your net worth with other Accredited Investors

Note: one can argue that class A+ will not be affected at all which I believe is true. That’s why we are trying to invest right to enter that untouchable status.

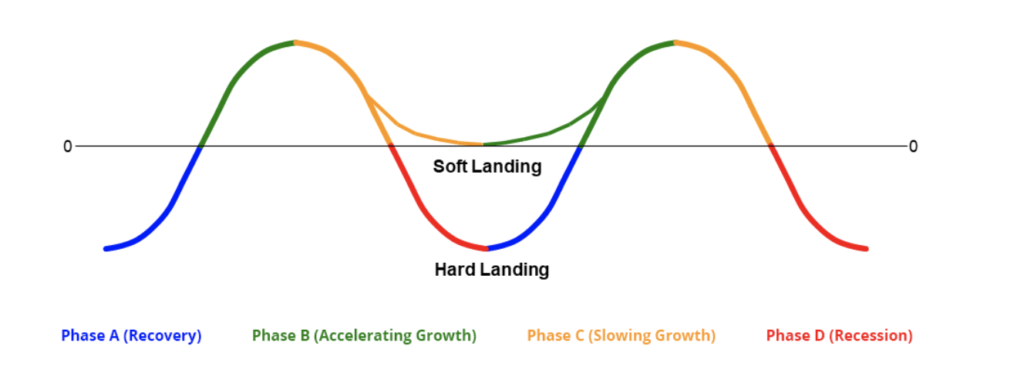

I remember when I sat through the same economic presentation at work from 2010-2014. The sentiment at the time was that it was going to be an extremely slow recovery. It makes sense that the length between the 2008 recession and now is very long which is why I mentioned an 11-inning ball game.

Previous

Next

This is why I took a step back from some pretty Class A deals because I asked myself the following questions:

1) What will happen to the rents if IT should happen?

2) Is the modeled 90% vacancy rate going to get blown up?

Class B and C apartments in strong submarkets will perform best over the long term. If you ensure the loan term is long enough so you don’t get hurt then you should Outlast the bumpy ride ahead.

Beware of the self-destructive behavior of not investing. You know what I mean… are you someone who self-sabotages?

Understand the micro and proceed if the numbers make sense.

I have to admit Class C and B assets are boring but work especially in a seller’s market because 1) they cashflow and 2) have a forced appreciation value-add component to give you levers to pull in tough times.

Again going back to Mr. Kiyosaki’s three-sided coin quote, investors go through three stages:

Go into MFH… Duh (I did well at single-family rentals let me try apartments)

Be a contrarian investor so go into other asset classes most decent investors are afraid or don’t even know about

Do special projects such as Affordable house taking advantage of tax credits or specialized operators (ie take abandoned big-box space like movie theaters and convert to the latest consumer needs)

Experienced investors who were in the downturn in 2008 say its interesting that the sentiment in 2006 was exuberance that it was going to keep going up. Now in 2018 the sentiment is fear… This is a good thing. Remember that in this market we still have:

- Historically low-interest rates

- Historically high rent increases (not 8% anymore but still 2-4%)

- Historically low vacancies

Things to monitor if you really need to geek out on numbers:

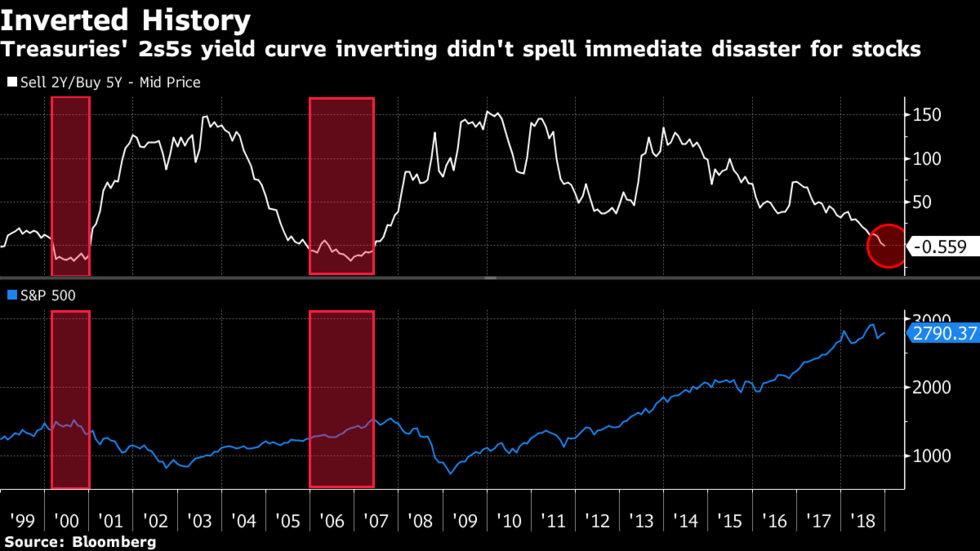

- 2 and 10 yield t curve. When that crosses you have just-a matter do time. Because its a measure of fear.

- Automation and AI – huge shifts in jobs. People need to work but technology has been increasing since the beginning of time.

- Wage growth

- Bankers prospective: how deals are getting funded and by who (institutional or dumb capital)

There is a saying out there that real estate is location specific. However, when I invest in more stable asset classes it’s a National market based on the economy both USA and international. When you invest in a micro-economic fix and flips then it’s location specific. When you invest in commercial assets it’s with more stable tenants and based on the aforementioned larger economy. How affordable is rent really? – “During the same span, median effective rent nationally has risen by about 26%. That rent appreciation pushed the median monthly rent nationally to around $1,220 per unit to end 2018. With the US median household income being just over $62,000, this rent accounts for 24% of monthly income. Using the typical benchmark of monthly rent being 30% of monthly household income for affordability, a margin remains for renters.” – [If you stick to using 2% and under rent growths and stay away from Tier I or Primary markets you should be fine] – ALN 19.02.24 A lot of people point to the Yield-Curve as a big indicator. In the end, I do believe that real estate will go down because of consumer instability. But if you have stocks you should sell those before even thinking of lumping it into cash flow type rental real estate.

“The guy not investing right now and hoarding cash (with net worth of under $1M… because if you can live off your cash flow then cool you can do what you want) is just afraid and lacks deal flow. Its like the person who complains that there is nothing to do during the weekend in LA (insert city with a vibrant scene) when in actuality they don’t have any friends (lack dealflow)… and by the no one likes (has a bad attitude and that person who makes excuses”

Lane Kawaoka

Simplepassivecashflow.com

Doomsday theory: Everyone talks about national debt but we are far far behind debt to GDP ratio that of Japan. When Japan hits the wall lookout. Here is my theory… watch out post-Japan Olympics when they have to let loose the belt (after a holiday period of excess calories). Leading up to a period where Japan has to save face while they are in the Olympic spotlight (and I’m not being racist cause I am Japanese and it is a thing). I don’t have the latest data but Japan is at around 250% where the USA is at 100%. Household debt KPIs: student debt, car loans, housing debt. Which is why I like these assets that are used by the poor and middle class! #RenterForever Lane’s theory: I’d rather be in deals that cashflow today that do better in a recession like Class C and B assets. Say it cashflows a 8%.The guy who is stilling on the sidelines with the “hoarding cash” mindset will lose because they will make 0%.

Use our Remote Rental Turnkey Rolodex

Start your own Family Office

I, on the other hand, might dip from 8% cashflow to 4% cashflow. On paper, I might be in a market with compressed cap rates but hopefully, I have forced appreciation potential if I really needed to sell – the counter move is to get 8-12 year debt to effectively bridge you to the next side of the market cycle. In the meantime you cashflow 4% which is 4% more than the “hoarding cash guy”. In addition, remember back in the 2008 crash. 2009-2012 people did not know if that was the bottom and it was so hard to close deals in that Phase IV (see below). “Hoarding cash guy” in 2009-2012 and the few years after the next recession will likely be in the same clueless situations. Wouldn’t you like to be in solid Class C and B assets that continued to cashflow?!? 4% x 4 years is still 16% ahead! Now if you are “hoarding cash guy” with no deal flow then I get it. Saving cash is the best thing to do for the guy with no deal flow or does not know how to run the numbers. I guess everything does suck.

Previous

Next

[Investors are chasing for decreasing yield these days] – REI.com – 19.03.4

Previous

Next

[Sophisticated Investors know interest rates and caps go up and down together and their money is made in the delta between the two] – REI.com – 19.03.4

Of course, all the Pro-Apartment publications will say this: Get Ready: Recession-Proofing An Apartment Portfolio – National Apartment Association 19.03.7

But enough of this doom and gloom because most gurus out there call recession everyday just so they can have Tweetable content. And they make a living selling subcriptions to their $79/month newsletter. But we are better than the average investor! And understand that future softness could very well be slowdown before the next great bull market.

Take care of yourself!

August 2020 Market Update Investor – Investor Letter #16