Warning – If you have been following the holistic wealth building strategies at SPC you understand that debt is a tool and you need to use said tool to acquire more and more assets that produce more income, more tax write offs, and build your net worth.

The following downloadable cheat sheet was made for Hawaii residents but the concepts discussed are typical as it is a confusing game. What is a HELOC (Home equity line of credit)?

A line of credit where the collateral is the existing equity in your home. Think of a credit card where your max limit is a portion of your equity in your home with some actually good rates. Pros:

It’s a line of credit where if you don’t use it there is no interest being accrued.

Low-interest rate because it is seen as a low risk loan from the banks perspective

A good way to get access to liquidity in a pinch. Especially when starting a new investing strategy and need proof of concept. Cons:

There is a possibility of the bank calling a loan due or changing the terms as the economy changes

Its not the best way of using equity because you should just sell the asset and be deleveraging into more fixed debt (very counter-intuitive I know but most things are)

What is LTV?

Loan to value. So if your home is worth $100,000 and you have $50,000 left on your mortgage then your LTV is 50%. I’m confused… this all sounds great but just tell me what to do

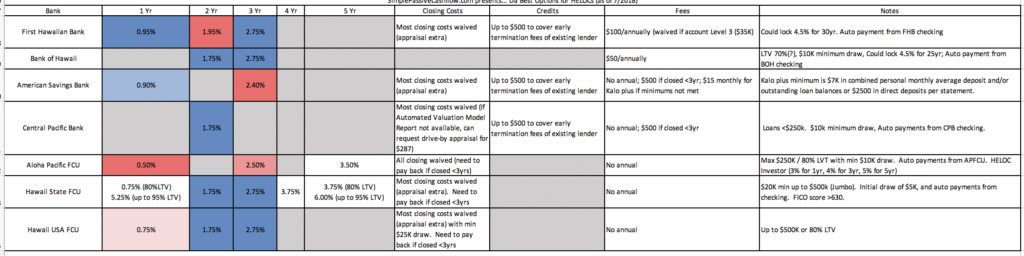

Option 1: Initiate a HELOC with Aloha Pacific CU for 1yr @ 0.5%. Then either go with ASB or CPB. They both will cover up to $500 for early termination with Aloha Pacific (which would be some of the closing costs that were waived) and no annual fee. For ASB, as long as you have $2500/month in direct deposits then there are no other fees – setup an automatic transaction from another bank recurring every month to take care of that, extra credit if you send that same $2,000 right back a few days later (that’s almost like money laundering). At the time of origination, can check rates to see if you go with another 1 yr (with ASB) or 2yr (with CPB). If you need to do a third time – a few years out, then go with whichever one you didn’t go with for the second HELOC. These rates change and so do the fee structures so try to learn this stuff and connect with other investors. A good way to do that is come to have a beer with other sophisticated investors at ReiAloha. Notice CPB is put in the 2nd order because they will waive the cancellation fees from the host bank prior. Yes, we thought this out like the Sunday arm chair quarterback strategies-out the running back rotation of the Denver Broncos.

Option 2 (for the lazy): Although this is not optimizing the rates this method is a little simpler if your time is so valuable like you are coming up with the cure to some rare form of cancer. Take the lowest of the 2-3 year HELOCs and just go with them. This minimizes movement and makes your life simpler. Perhaps it makes your life so simpler that you free up time and mental bandwidth to invest in real assets such as rental real estate or passive syndications? I’m still confused… walk me through a real-life example

Someone who just did this with a credit union… for a $200k loan, the closing cost was about $1200 (which were covered by the cu) and he paid $700 for an appraisal. He intends to hold for 3 yrs, so he didn’t get much details on how much of the closing costs he would have to pay back…. for this scenario, we estimate that all $1200 and would have to be paid (which $500 of that would be covered by the new lender). Thoughts about appraisals

In order to cut costs some banks will do a desk review to determine the value of your property. This usually is more conservative figure and hurts you because you want your home to appraise for the most that it can in order to qualify for the biggest loan. These desk reviews utilize the tax assessed value which usually lower than if you paid $500 for a real appraisal or a cheaper “drive-by” appraisal. Sometimes it might be worth it to pay the extra fees to get a real appraisal instead of the lazy man method. It might be obvious but have a conversation on which appraisal is being used or be disappointed like when Coke switched your C&H sugar for corn syrup. What about for a high leverage option (above 80%+) and low leverage option or will all of them not touch higher than 80%?

Higher leverage HELOC are available but not openly published. The author of this guide did not want to waste their time finding such fringe data since it changes so much and did not want to wait of a consultation from another bank employee. The collaborator did note that Hawaii State FCU was one of the few Credit Unions that openly published a higher LTV (up to 95%). Note – Hawaii banks are much more conservative on appraisals and terms than on the mainland. You may want to have a bank on the mainland if they will give a HELOC out of state. Typically anyone can get into most Credit Union after all they just want your money to sit in their bank paying you 0.01%. Sometimes you just have to donate $10 to some friends of the library account to gain membership. Thoughts about fees

Be cognizant of closing costs are. The credit unions don’t have an early termination fee, however, you got to pay back closing costs. For the banks, there is a $500 termination fee and rates are higher, but maybe a better route if you got to pay back waived closing costs with the credit unions… especially since ASB and CPB will cover up to $500 early termination. Why are you doing this?

Equity in your home is lazy money. It is not yielding a return and in fact it is a liability for lawsuits. The wealthy try to control everything and own nothing (encumber their assets with debt). In addition, typical investment yields range from 12-25% for stable, cashflowing assets, that hold their value even if the economy weakens. Fine tuning:

“At some point you are going to ask the following: Assuming the delta between the one and two year helot is 1% and we are talking about a 200k loan… That’s 2k. Is it worth it to run around one afternoon and move stuff around online???

Are you going with the one year one first then get the two year from the next one? At this point it may make sense to get on a coaching call for 30 minutes to get an expert opinion.

Also it is possible to get a HELOC on a non-owner occupied home (rental property) but if you are considering so read this… simplepassivecashflow.com/roe” Conclusion

Overall the process is pretty painless. You might have to run around looking for your mortgage files, HOA documents, or insurance but once setup it works just like another checking account. Download link

Flip the Script on the Banks

Summary: Pay a 30-year mortgage in 5 to 8 years by paying back your mortgage with simple interest instead of amortized interest.

I recently discussed this in my Forbes article here.

Is this something new?

We all know it’s a sellers’ market, with the lack of deals out there and the majority of the Simple Passive Cashflow Podcast listeners looking for something to invest their cash in. Good times, if you ask me. This strategy is nothing new but now the strategies that are, “trending,” like bell bottoms, tights, and neon colors but forgotten. One of these old plays from the playbook is called the Mortgage Equity Arbitrage Strategy also known as, the Australian Banking system.

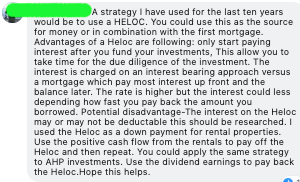

First off, let’s talk about good debt versus bad debt. Obviously, an 18% interest rate paid on something like a credit card is bad debt. But taking a 4% HELOC (Home Equity Line of Credit) or loan from your life insurance policy can be good debt. Especially, if you are putting the loan proceeds into AHP at 12%, a MFH Syndication at 20%, a Turnkey rental at 30%+, or another higher risk syndication at 35%+. Just don’t buy jet skis or other doodads with the money… I don’t know why it’s always jet skis as the example. Maybe something to do with the fact that it is a mini-boat, and boats are known as the worse purchase known to man.

What you do with the liquidity from the debt is what really matters. Traditionally, it has been good to go into debt for a college education paying 4-8%… unless you are getting a glass blowing degree… or maybe a psychology degree so you can trick yourself into thinking college was worth it… or Asian studies degree because you are going to have to get used to ramen noodles in your adult life… or a Communications degree to be able to spin your financial reality. Ok I admit, I had a pretty depressing college experience…

Other Resources:

https://simplepassivecashflow.com/podcast-105-jordan-goodman-affiliate-connections-mortgage-rate-optimization-dolphin-mentality/

https://simplepassivecashflow.com/spc028-chris-myles-explains-downside-using-helocs-pay-off-mortgages-teaser-life-insurance/

https://simplepassivecashflow.com/heloc/

Additional reading…

Webinar – Hui Webinar – How to pay your 30-year mortgage in 4 to 8 years with Mortgage Rate Arbitrage – https://www.youtube.com/watch?v=yysbua0nOaM&t

SPC105 – Jordan Goodman – Affiliate connections + mortgage rate optimization + Dolphin mentality – https://simplepassivecashflow.com/podcast-105-jordan-goodman-affiliate-connections-mortgage-rate-optimization-dolphin-mentality/

Here is the download link for Jordan’s text on the mortgage rate optimization strategy: https://drive.google.com/open?id=1XajKX3Otl9egfIbTnPBsr49wf7pDZHsO

Helocs hurt your credit score… However if you are a Passive Investor not needing to qualify for PITA rentals, already a home (no need to qualify for a mortgage for some time), or have ample income to support a car loan… it might make sense to run the HELOC hot for a minor credit score hit (25-100 pts). Most personal finance will say absolutely say not to hurt your credit score but in our world this decision is very personal and where the investor needs to empower themself (get around the right people) to choose the right set of options moving forward.

Time is the most important resource. You can trade time for money and vice versa. It is pretty rare that you can not throw money at a problem and make it go away. And if you have kids!

Some hacks I have implemented updated 8/1/18 (See how far I have come)

Using disposable chopsticks, plates, bowls, clubs, and forks to minimize time to wash dishes and put away. Also need less space for more of this “stuff”. I think we do not realize how much not only time we waste on this but water and electricity go into this.

Use Uber as much as I can to minimize stress, the chance of an accident, 50 cents a mile per the IRS in wear and tear to your vehicle but most importantly you can bring your laptop and get some work done.

Leasing a car – such a great decision. Its fun, the numbers make sense if you are able to grow your money at more than 14% a year, and don’t have to deal with any maintenance issues.

Eat out. It just tastes better too. And no cleanup, prep, grocery shopping, etc.

Send me some of yours!

I stumbled upon a great visualization of your time. Basically, the yellow below is the time we sleep, blue is leisure, and light blue is at work. See the diagram here http://flowingdata.com/2017/05/09/adulthood-days/

Two takeaways:

If you have not started investing… when the heck when? Get a mentor and compress the learning curve, decrease costly mistakes, and get on with your life!

“Fiverr is the world’s largest marketplace of talented online freelancers who pride themselves on

getting things done for you. On time, on budget. Designers, developers, writers – everything you

need for your next project is here. Now let’s tackle your to-dos, today!”

“Fiverr’s global community of freelancers have delivered tens of millions of

high-quality Gigs from over 150 service categories across 190 countries.

Fiverr is a global online marketplace offering tasks and services, beginning at a cost of $5 per job

performed. Freelancers use Fiverr to offer services in more than 150 categories, to customers

worldwide. Currently, Fiverr lists more than three million services on its site.

Fiverr is the world’s largest marketplace of talented online freelancers who pride themselves on

getting things done for you. On time, on budget. Designers, developers, writers – everything you need

for your next project is here. Now let’s tackle your to-dos, today!

Join over 11M businesses who use Fiverr’s freelance services.

Fiverr is the world’s home for digital, creative and professional services, providing a one-stop shop

for millions of digital services, all at your fingertips.

Fiverr is a digital marketplace that allows you to make your business better, stay on budget and get

things done in just a click.

Fiverr is the easiest way to get everything done, at an unbeatable value.

Need something now? As the world’s home for digital, creative and professional services, Fiverr

provides one-stop shopping for millions of digital services, all at your fingertips.

Fiverr gives you instant access to millions of Gigs from people who love what they do, in just a click.

Need something done? Let someone else take care of it! Get everything from resume help, to

designed invitations, to cool gifts, all at an affordable price. Whether you’re building a business, or

just looking for something unique, find it on Fiverr!”

Some of you had questions about Virtual Assistants which I have had some growing pains with…

Take 1: I went to various countries/regions Craigslist where I heard there was cheap virtual labor such as the Philippines, Ukraine, Latin America, Eastern Europe, Etc. I created a generic posting for a Virtual Assistant and a link to a Google Form that I created that was supposed to farm data of willing workers and ask binomial questions such as if they had experience with graphics, audio editing, Excel, English, and how much their hourly rate was. This was a success and the idea was that I would create a database that I could BCC the emails to competitively bid projects. Unfortunately, when I sorted my list for the desired skill I was looking for, I discovered that many of the potential candidates sent generic resumes back. They did not even read the job description. I guess as the saying goes “shit in shit out.” Tim Ferriss talks about giving strange instructions to potential job candidates such as a requirement to fax in their application (in an age of limited fax access) to see which candidates follow directions and can overcome minor Resistance of not having fax machines.

Take 2: It seems like the tasks are taking a lot more time than it should. To some respect, that is to be expected. What I am trying to wrap my head around is the cultural differences not to mention the language barrier. In some of these Asian cultures, honor and face are utmost importance and sometimes it is culturally the normal to lie to save face. In America, we preach stepping up and admitting fault and moving on which I believe is a true demonstration of high value. So it’s a little frustrating… I know the internet sucks at these places but give me a break. I am just surprised they are not telling me their dog ate the GoogleDoc. Successful people take ownership and I accept this as MY fault in terms of me not having my job scope defined and linear instructions for the virtual assistant to carry out. If my virtual assistant misses on the deliverable or takes too long I take full responsibility.

Afterthoughts: A great discussion at a recent Mastermind I attended around this topic. Seems like a lot of people are backtracking from cheap (sub 8 dollar an hour labor) and opting for higher quality workers. I believe the vision of an employee is to get something done cheaper than your personal hourly rate, also get it don’t faster, and with a “Sir… I was completing task X and I found this wrong in our process so I took care of it and wanted to discuss this with you.” I don’t know if I will ever achieve this level of initiative in any person trading their time for money but one can only dream. Until then I will try to switch to a more project-based system as opposed to having a VA on call for a 10-40 hour set time. The cons of this project-based methods are that it requires more touch points for me to keep micromanaging each project and this is the exact reason I am looking for help in the first place. Time is the most important thing Jelly Bean. https://www.youtube.com/watch?v=BOksW_NabEk

The Random list of tasks to outsource:

1. Organize your travel (including learning your travel preferences). This includes making all your travel arrangements,

organizing all your flight info into your favorite travel app, and even remotely monitoring your travel to be ready to deal with

any missed flights or oversold hotels.

2. Handle billing disputes.

3. Help setting up bills onto auto payment on your credit card.

4. Address and mail cards, letters, and packages. Sure you may still handwrite the thank you, but do you really need to look up

the address and post the letter?

5. Update your contact manager (or CRM database).

6. Screen your e-mail and handle low-level responses. This includes deleting or archiving things you don’t even need to see.

7. Update your blog and social media accounts.

8. Organize and manage your filing system, both paper-based and scanned e-files.

9. Take dictation (either live or via recordings, perhaps using Voxer, one of my favorite apps).

10. Set up appointments and hold your schedule.

11. Gather all the needed data and prep information for all your appointments. For example, I ask my assistant to put to the

memo of any appointment she posts to my calendar any recent email exchanges and the contact information of the person

I’m meeting with. This saves me untold time when you compound this service over 15-20 meetings I hold each week.

12. Daily clean-up of your office, including refilling items.

13. Screen phone and e-mail so you don’t get the interruptions.

14. Take notes at key meetings and follow up with attendees on key deliverables.

15. Keep a master chart/list/calendar of your projects and deadlines and set reminders.

16. Tickler all birthdays and anniversaries, holidays, or other important dates, and even arrange for gifts, cards, or phone calls

that make you look good.

17. Update his or her own “Project List” so that all the tasks and deliverables they are responsible for in one place for you to

review.

18. Get, open, sort, forward, handle, and if need be shred your mail.

19. Coordinate with outsourced vendors when you have an IT issue. You just work from a back-up computer for the day and let

him or her troubleshoot it with your IT vendor.

20. Order things online for you and handle any product returns or service issues.

21. Handle any personal errands or schedule any household repairs. Yes this is perfectly reasonable as it saves you time that

you can reinvest in creating value for your company.

22. Notarize your documents by becoming a Notary Public in your state.

23. Help you to streamline your office—filing, sorting, and systematizing wworkflow

24. Basic updates to your Web sites.

25. Create and continue to refine the “expert system” for how to be your assistant (this one should be part of their job function

right from the start). This way if you promote your assistant they have created the core system for your next hire. If they leave

you to work elsewhere, the transition is much less painful.

26. Dealing with tech troubles on your phone or tablet computers. They can do this during the day when you’re in the office doing

other more valuable work.

27. Any parts of your projects that he or she is capable of doing for you. Constantly be on the lookout for things to try them out

doing. For example, my assistant helped expand the syndication reach of my business articles by over 100,000 annual

readers.

28. Download movies or audiobooks

29. Search for contacts of people you need to meet

30. Bookkeeping with a CPA or without one

31. Edit videos

32. Make calls

33. FInd sellers

34. Take Calls from leads

35. Call banks to find a portfolio lender

36. Assemble a list of podcast guests to contact

“Retirement accounts (with so-called tax benefits) only make sense if your AGI is over 340k AND you have a substantial amount in your IRA already (400k+). The wealthy people I meet don’t use these things as a primary wealth building too because it does not help them on their taxes today. These retirement accounts are tools to be used in certain situations, read on to see when it makes sense for you.”

“If you income is under 340K and/or your IRA/QRP/Retirement funds is under 500k and/or you are less than 55 years old I think dumping your IRA/QRP money (in a controlled manner managing your AGI not going too high) is the way to go.”

Like these coaching calls? Get access to dozens of them for free when you opt in to our community here.

I agree that retirement plans are bad. When you contribute to a 401K, IRA or other deferred compensation plan, you are voluntarily giving the IRS a tax lien on all of the retirement money and the growth on that money. Also, with tax rates likely to be higher in the future, the amount of the tax lien will increase.

Hui Members – please reach out via email for the current vendor we are using these days

0:01 This is a story about a dude named Lane he moved to the mainland and bought one place to stay. And then one day he went try to rent them

0:10 out, and then he became one. That’s still me.

0:15 Hey everybody, this is Lane with the simple passive casual podcast. Today we are going to talk about self directed IRAs. If you guys didn’t know you guys can take your retirement account and roll it into a self directed IRA, either a Roth form or a regular IRA form, but you’re going to need to get it out of the hands of those who can say the names that the Vanguard’s fidelity’s all those like big brokerages that you know they got in cahoots with the government way back when in the 80s in the 70s. I don’t know if this is true American history here but it created this thing called the mutual fund to keep your money locked up so they could extract a gazillion hidden fees. Those of you guys listening on the podcast will also have a nice presentation slides. Hear that? If you guys want to go to the YouTube channel you guys can check out there or I will put this up on our retirement fund account page at simple passive cash flow calm slash q Rp. So again, that’s slash q RP if you guys want to check out the video there, but I got a special guest today, Jason from new view trusts. How’s it going, Jason?

1:20 Hey, Lane. How are you? Thanks for having me.

1:22 All right, so we’ve got about nine slides here. Less than 10 so people don’t go to sleep. But yeah, let’s quickly go over what the heck is a self directed IRA? And, you know, how can we use this to turbocharge our investing

1:37 share? Well, you know, you kind of hit on something. And I don’t know if it’s an old wives tale or if it is reality in terms of American history and the origin of the mutual fund. But I think we’d all agree, the financial markets as a whole are just not designed for the average retail investor unless they happen to get in and get out at the right time. And, you know, I think we’re seeing that out in the market today, you know, as we see it going up and going down and I read an article that you’ve got three different companies that are in the process of filing for bankruptcy that are up over 30% you know, which conventional wisdom would tell you you get out of a stock before they file bankruptcy, not get into them. And so what do we know is just individual investors, right? We’re all unfortunately left holding the bag. But as you mentioned, kind of the Vanguard’s the Schwab’s the fidelity’s, they’re in the business of providing retirement account custody, right, just like we are, but their business is to hold investments that are traditional stocks, bonds, mutual funds, Navy just exist in the same manner to hold investments that are not stocks, bonds, mutual funds, so we’re here to provide the same level of custody, but we’re allowing you as a client to pick your own investments to include things like real property or mortgage notes, private equity, right? All the passive investments, you know, that Lane talks to you guys about all the time. All of those can be done in an IRA and for those that are looking Looking at the screen, you know, we one of the things that we make clear from the get go is we’re not advisors, we’re not tax accountants, we’re not, you know, legal professionals, we’re custodians, we’re just here to hold your account, take your direction and hold the assets that you want. Self direction, gives you control. So the self and self direction means you find your own investments, you evaluate them, you do your own due diligence, and we go by and when you’re ready. So that’s really the role we play the role you play in the value, you know, to some degree of a self directed account. That’s right. We are here here for giving information and what do I know, right? I mean, I just bought some rental properties and quit my day job about 12 years later. And that’s what really upsets me about all that retirement funds stuck in these mutual funds. Like when I had a rental property, I was making like 30% a year when I was, you know, my leverage position was good, but then you look at my like the stocks and mutual funds like you’re making, what, seven 8% a year. It’s like where the heck did all my money go? And you look at these expense ratios and doesn’t it’s not all inclusive of all the He’s certainly right. I think what what is such a challenge for so many people and we hear it all the time is, you know, you charge me account fees, you know, fidelity doesn’t charge me account fees. And I think to myself, and I’ll sometimes say depending on the customer, you know, do you really think fidelity advertises on every possible television channel with all big buildings in town? Because they don’t charge you anything. You know, just because you go and you get a, a water for free or your drinks included, doesn’t mean you’re not paying for it somewhere, right? You’re paying a higher price on something. So you’re absolutely right. Mutual funds are notorious for for hidden fees and a lot of money gets raked out of those before an investor ever sees $1 in both good times, and bad.

4:45 Don’t get me started with financial planners, you guys can check out all the big rant page at simple passive cash flow calm slash. FP is one of those HBO comedy special videos in there too. If you guys think poking fun at financial planners, let’s kind of go through Some of this slide deck, Jason and then chime in with questions here. They’re the listener

5:05 perfect. Well, yeah, this is a slide that that I think really helps underscore. And it’s probably the thing that the story I like to tell the most in this. And if you can just leave that first one up for a second lane, and we’ll we’ll get to the kind of the grand finale here if, if it doesn’t pop up, but, you know, one of the things that so many people get focused on is they focus on investments, right. And, and naturally, we all do that, obviously, you’re, you know, you spend a lot of time talking about it. And and it’s so mission critical. Unfortunately, in the world that we occupy, what a lot of people step over is, can I buy the same investment in a different vehicle and yield better results? And that’s really what this slide is going to illustrate for you. I’ll kind of tell you the story. And so one of the things that happens right is as investors we look for the best investments, right? We assume that if we can just buy good investments, we can win the game. And I think it’s really two parts prior to that, and, and laying your story is so fascinating to me because you know, you didn’t have to go in and syndicate deals because you save the money. So you could be a passive investor, right. So you’re more successful as an investor because you had money to invest. And that gives people a big leg up. So we’re going to talk about the value of saving, and the value of saving in the right vehicle. So if you were to go out, and I’m just going to use a simplistic example. And again, those if you’re not, if you don’t have the slides that encourage you to go to the website and grab them, because it illustrates a little bit better, but just to illustrate how much taxes impact our investments, so if you said I want to go out and become an investor, and I’ve got $1, right, I’ve got $1 to invest and I’m going to invest it every year and it’s going to double year after year. So I’m going to invest $1, it’s going to become two I’m going to invest two, it’s going to become four, four becomes eight becomes 16. You get the idea. If you double that dollar for 20 years, right? 20 years $1 if you do that in a time taxable account, assuming there’s a 25% annual tax on your profits, you’re going to end up turning $1 into 72,000 bucks right now at face value, right? If you were to talk to anyone that turned $1 into 72,000 bucks, they look like a financial genius, right? And we’d all celebrate and we’d say that’s awesome. But what people overstep is what if I took that same dollar made the same investments that doubled every year for 20 years. But instead of having Uncle Sam partnering with me for 25%, or a little bit more or less, depending on your tax bracket, what if I simply put that money into a retirement account? First, let’s just say a Roth IRA. I paid tax on $1. Right, so if the tax rate was 25%, it cost me a quarter. And then I invested that money the same way I did outside of my IRA, doubling it every years, every year for 20 years, instead of $72,000. I’m going to end up with Just over a million dollars, right? So if everyone can kind of let that sink in for a second, same investor, same investment, same amount of time, one person made the investment with their personal money, the other person put it into a Roth IRA from the get go and then made all the same investments. One investor has $1,048,000 and the other investor has $72,000. Now, when I asked you what type of investor Do you want to be? The answer is so painfully obvious. And that’s what self directed IRAs do, is they allow you to take the investments that you’re making with your personal money today, and simply duplicated them into your IRA tax free. And obviously, the slide speaks for itself but the amount of money that you can make as a result is staggering. Not because you were a better investor, because you put it in the right vehicle and this is the exact reason

9:00 How we’re gonna pay for this all these stimulus packages, right? This is how the government makes money.

9:06 That’s exactly right. And the beauty of IRAs is it is a it is a tax free, tax advantaged account from the get go, meaning they’ve been designed this way since inception. So this isn’t a loophole that if you’ve got a good enough CPA or you’re wealthy enough to understand this is every single run of the mill investor can participate in this program, and it’s perfectly permissible and perfectly legal.

9:36 Well, it’s kind of a loophole, right? It’s the guys in Congress make these programs so they themselves can take advantage of them.

9:42 Well, this one’s interesting, right? Because, you know, what were the challenges is, it’s not whether or not you can do it, it’s whether or not you come across the opportunity and so many investors, you know, they just never learned that this is an option. Right? And, you know, we’ve been added I personally have been in this This business for 15 years, and we’ve been telling the story, and I can tell you 15 years ago, that people were telling the story to, you know, then is much different than today, right? 15 years ago, one out of 100, people even knew what this looked like, let alone how to do it. And now, probably 50 out of 100, people I talked to are at least familiar with it. So the message is getting out more and more people are turning to this opportunity, because it doesn’t make any sense to own an investment in your personal account, if you could own it in your retirement account and never pay tax on it. Right. I mean, that’s the beauty of, of setting up a self directed account. So when we talk about, you know, accounts, you know, I’ll just quickly highlight kind of how these plans work and the different types of plans that exist and I won’t get necessarily too deep in the weeds here. But, you know, a lot of times people kind of view retirement accounts as a one size fits. All right, there’s one plan, maybe two, and the reality is there’s not. There’s four different types of IRAs. So all of which you can park money into a traditional Roth IRAs Sep and as simple as Sep kind of being the unique one because it’s for those that are self employed HSA, for those that are on high deductible insurance plans, you can actually have an HSA and go self directed into passive investments, educational savings accounts. So for those with kids and grandkids, you can actually contribute to an ESA just like a Roth for your kids or grandkids and that money can all grow into whatever investments you choose completely tax free. And then you can use it to pay your your your kids, grandkids, etc. You can use it to pay their qualifying educational expenses. So not only can you use it to build retirement wealth, right, you can also use it to build tax free wealth for health expenses, and you can use it to build tax free wealth for educational expenses. And then the last plan the solo 401k the QR p if you will, that plan allows people to utilize the N q RP simply stands for qualified retirement plan. The q RP allows people to To take all the benefits of a so of a 401k plan, right, much higher contribution limits a lot more investor flexibility, etc. And you can do all of that inside a solo 401k plan and buy whatever investments that you want. So for those that are listening today are joining us, if you’re self employed, that tool is fantastic. Those that aren’t self employed yet, right? Maybe you’re taking kind of Lane’s approach, right, which is, you know, get some investments and give yourself enough passive income to to, to quit your day job. While you’re still employed. You may want to utilize some of these other tools that traditional the Roth solo, or sorry, the HSA, the ESA, we can walk you through that process and talk you through that. But key key takeaway here, everybody, is it, you there’s lots of different vehicles to save money. And if I go back to that slide of Dublin for $1, right? Well, what if you put $1 into a Roth $1 into an HSA and $1 in it to an ESA and you went out invested all three of those right and You doubled it $1 every every year, and you ended up with a million dollars in three different accounts, it sure beats a million dollars in just one account. So, lots to think about there. I don’t want to belabor it, and I don’t want to bore you with it. But I always want to share the value that that there are different plant types and a lot that have different levels of value for you.

13:18 And just for example, I’ve got it had an HSA account, and I put a coffee farm parcel in there. So I think what we’ll talk about some of the more exotic things you can invest in and then the a lot of a lot of my guys are doing a solo 401k is grps these days, and you know, they don’t necessarily run a traditional business. But, you know, there’s some ways around that. Of course, we’re not giving legal advice here. We’re just telling what other people are doing they’re kind of Thrive kicking butt.

13:45 So I you know, this this is kind of the the part where we talk about what are the rules, right? I mean, obviously the the government is not going to hand out tax free accounts without having some limitations and that makes sense. The biggest concern The government has really is, are you going to use this money to try to funnel or get money in or out either above the limits or without penalty. And so the IRS really has two sets of rules they enforce. Number one, you can’t buy life insurance and you can’t buy collectibles. Pretty straightforward and pretty easy, right? No Life Insurance, no collectibles. So this isn’t a tool to go buy artwork or you know, metals or gems unless they’re bought for their intrinsic value. But if you’re buying numismatics or you’re buying, you know, a painting or something, the IRS simply doesn’t let you do that in an IRA. There’s just too much stuff to try to manage market value in that. The second rule that they have is really less geared around what you buy and it’s more geared around who the IRA is tax free or tax advantaged entity does business with and in the case of a retirement account, they don’t want that that account doing business with you, your spouse, most of your close family members, certainly people above you and below you from a family tree. Right, your ancestors, parents, grandparents, your descendants, children and grandchildren. And business is owned by those parties. So what it says is my IRA could go invest with Lane, right? We’re not related as it as it as it is compared to this list. So my IRA could go do business with Lane tomorrow. So I could invest passively in a deal that that Lane was sponsoring, or I could I could buy a property that Lane was selling or whatever the deal was, but I couldn’t go do that. If Lane, you know, if I invested into with Lane and Lane was a child of mine, right? Because the IRS says that’s too close to the flame, we’re not certain that you’re going to be able to behave yourself in a in a, you know, parental with a child type transaction. So it’s not the deal that’s prohibited. It’s the fact that that our relation crosses the line, so smallest to people, right? The beauty of passive investing and what we’re really spending most of our time talking about is it’s exactly that right? It is passive If it is with unrelated parties, it’s mailbox money. And all of those deals, which we’re going to talk about here in a second are perfectly permissible in an IRA.

16:07 And what Jason is talking about is what we call the prohibited transaction. So we kind of self deal with ourselves. And what you’re kind of alluding to is pretty is it is actually pretty cool advanced technique that a lot of people in my mastermind do. what they’ll do is they’ll You know, they’re active investors but they’ll invest in their buddies deal with their self directed IRA. A lot of people will do that within the syndications to other sponsors and just can’t you got to make sure that like, you know, nobody gets married in the family right with it’s kind of like brothers in law. I don’t, I don’t know if you can do that or not, but maybe be careful may not be worth it. But you can’t actively be in you’re adding value to your your investment, right. Like if you own a rental property, you can’t be the property manager. You can’t trim the hedge, you can’t paint the property. You can’t fix anything. You have to be armed. Link transaction.

17:01 Yeah. And if you think about this in the stock world, right, it would be like, you know, the IRS doesn’t want Bill Gates buying Microsoft stock in his IRA, because they don’t want him having tax advantaged opportunities to grow money of a business that he controls, right. But there would be nothing that would prevent Bill Gates from investing into apple. Right? Because there’s no related party there. Even if he is great friends with Tim Cook and understands everything about Apple’s business model. It makes him a good investor. And there’s nothing prohibited about that. They just don’t want him investing into his own business or doing anything that gives him that sweat equity as you kind of alluded to. So you know, this isn’t necessary. This is far from a deal breaker. In fact, I would suggest if this catches you up, you’re probably kind of missing the true intent of really passive investing. But this is a you know, we got to follow the rules. And if we want to have the tax benefits, we gotta follow a real small set of rules.

17:57 Yeah, some some of the more fun techniques I hear about whether it’s legal or not, is, you know, like, note investors, they like peel off though, you know, they they make it like they’re investing $1 they peel off all the future payments is, you know, added value, and that’s how they turbocharge their self directed IRA. I mean, that’s how like, was it Nick and Romney had like a gazillion dollars in this self directed Roth, and like, you know, how the heck did he do that when you can only put in $6,000 a year right, either doing tricky things like that. But you don’t have to comment on that. Jason. I mean, that’s what we’ll have to come

18:34 to Hawaii. Best. I I don’t I think the way that I will. I will, I will. Just and you know, the beauty is of a self directed account is you are limited by your own creativity. And, you know, certainly that creativity should fall within the bounds but there’s a lot of strategies to turbocharge investments and, and find ways to really have some high profit, especially as a percentage type investments inside accounts. And as long as you’re not, you know, breaking either these rules that we just talked about, you’ve got an infinite opportunity. And you know, I love hearing stories like that, assuming they all fall within the legal realm because it’s exactly it and people like Mitt Romney don’t have to be the ones that can you know, it’s not meant for wealthy people like meant to be able to, you know, turbocharged the average mom and pop investor has that ability through an account with new view.

19:29 Jason just sells the motorcycle and it needs all

19:33 regulations, but do you want to go do some wheelies? That’s on you.

19:39 Are you a non accredited investor looking for opportunities to invest passively? How about a newer investor looking to get a bit of a track record and confidence from your spouse

19:47 who’s a little bit skeptic of what you’ve been listened to the last few months and could use the reinforcement of double digit returns paid like clockwork in the form of monthly dividends, the American Home preservation fund or a SP is currently open again, and it’s looking to bring new investors with them. I have been investing with them since 2016. And originally I use it as a means to pay for my regular expenses. I started with $60,000 as my initial investment and that paid my car payment completely for me every single month, he collaborates with existing homeowners to keep them in their homes via restructuring or selling the depths. Unlike their competitors, it’s a way to make great returns while feeling good about making a social impact. After investing myself in the fun, it was awesome when owner George Newberry saw the impact simple passive cash flow was making and eventually approached me to become a spokesperson for the company. You can start investing with as little as hundred bucks. And if you want a fee burdensome book, please send me an email at Lane at simple passive cash flow calm. For more information about investing with hp, go to HP servicing.com slash investors That’s like, going back to that what your IRA cannot invest in? Does wine fall in that category?

21:09 Believe it or not, alcoholic beverages is actually a line item under collectibles and IRS code. So, yep, wine in any other alcoholic beverages for the same reason you can’t hold a painting. Okay.

21:23 You can’t directly on artwork, but there are operators out there that will syndicate it. And but I know you can do it that way. But I think that’s where if you’re getting enjoyment out of the actual painting in your gallery or in your house or a wine that you could potentially tap and fill with purple water. That’s where they draw the line, right.

21:46 You know, that as the custodian who gets to hold all the assets right on behalf of the accounts. You know, it’s a bit disappointing that we can’t hold the artwork and wine and alcohol on behalf of our clients. And you know, I I think we all have a little experience when we were younger, figuring out how to refill the liquor bottles, at least certainly I know me and my friends did in our respective, you know, parents liquor cabinets. But yeah, it’s prohibited and you know, really laid what what, what their biggest concern is candidly is it has to do with market value and investing into a fund is investing into a business, right, and the fund managers are responsible to oversee the activity. And it’s a little bit different. If you own a Picasso in your IRA, how would the IRS ever know what your tax liability is? Right? So if if you decided to withdraw that Picasso painting from your account, which is perfectly permissible? How would they know if that’s valued at 1,000,002 million 10 million or 100 million and obviously, as a taxpayer, you’re going to try to get that valued at the lowest amount possible to limit your tax. So that was really their intention from the get go is, is obviously a personal use and personal consumption and that’s certainly a large country. Reading factor, but it also goes a step further into the behavior of the the account holder. And from a tax liability standpoint,

23:08 that’s always kind of playfully push the limits on this because it helps you understand, right? What is the intention and essentially Congress there, you know, they got to keep all US monkeys in line, so they got to draw the line somewhere. That’s right. But what about gold Boolean is that Can you can you own that in your IRA

23:27 IRA. So any precious metal, right, whether it be gold, silver, platinum, palladium, they can all be held as long as they are above purity levels. So for all metals, except for gold, because it’s a little bit softer, more malleable. The requirement of purity is point 995 for gold and point 999 for all other metals. So if you wanted to invest into Golden Eagles, let’s just say, as long as it in a golden eagle does meet the criteria to Treasury, you know, it’s a government issued and it’s not domestic, you can buy Canadian Maple Leafs and other things. But as long as the coin that you’re buying, even if it’s unmarked, has to meet certain refinery guidelines and be above the purity level. So what you can’t do is you can’t go buy a piece of gold from the Titanic, because you’re buying it for its numismatic value or its collectible value that’s prohibited. But if you bought a just, you know, one ounce gold coin that was met the refinery requirements and was point 995 percent pure above that it would be perfectly permissible.

24:35 Again, it comes back to Mike Kennedy, the market value be verified. You got it on it.

24:41 Yep. All right.

24:43 What about Bitcoin?

24:44 Yeah, Bitcoin can be held. There’s a few different ways to access it but cryptocurrencies of all different types can be held and, you know, we can set help you set up your account where you can actually go designate your own storage. Find your own, you know, Whatever crypto you want to buy, whatever the platform you’re using to buy it, whatever platform you want to use to hold it, and you can manage all of that, on behalf of the IRA.

25:10 I’m not a big fan of crypto unless you got a lot of money more than half a million dollars to play around with it. Nor am I big fan of precious metals I just think that’s what all like the Guru’s out there trying to scare people that the world is ending so they can get their Commission’s on both gold and silver Booleans. But hey, who do I know? I mean, might work. I just don’t do it. But let’s, you know, also my folks are interested in like the real estate side, whether it’s a syndication or LLC, if you can kind of expand on what people are using for that.

25:43 Sure. So So I’ve got two slides on that. And you know, before we talk about kind of the the passive approach, you know, your your IRA can own really anything that’s not prohibited. Well, what are the most common things our clients own Really it boils down into three asset classes. And all three are pretty close to the same in terms of percentage of assets. So, real estate, and this is all different types of real estate. As you can imagine, mortgages and notes, right performing non performing, it doesn’t matter, they all fall under that mortgage note, basically a loan of some sort. And then private equity and private equity covers a pretty big range, if you will, but that’s partnership deals, whether they’re, you know, whether they’re, they’re just straight passive investments or whether or not it’s private stock investment, like an active business. All of those can be held LLCs, obviously, and then we have the other category, right? And that’s the probably 10 or 15% of what we do, or what our clients do. Precious Metals falls into that cryptocurrency, tax liens, tax deeds, tax certificates. You know, we’ve we’ve got clients that have invested in race horses. We’ve had You know we’ve seen it if you can imagine it I think as it farmers it says we know a thing or two because we’ve seen a thing or two. Man we we’ve seen a thing or two, that’s for sure.

27:12 Now hands down, it’s kind of inspiring. What if I wanted to buy like one of those five or $10,000 like purebred Eagles or something like that, or like one of those like exotic cats that celebrities own like a, like a hybrid Lynx?

27:28 Sure, I mean, so long as you there’s really a couple key things. Number one is your clear ownership paperwork, right? And for a lot of these including a racehorse, yes, you cannot store it yourself. Right. So you can’t bring it to your property. And you know, for the racehorse, for example, it needs to be stored somewhere. You have to be hands off. So in the example of the racehorse or in your example of we’ll call you lane exotic you know, for free You’re some sort of Tiger, right? You could you could do it, your IRA would buy it, your IRA would pay whomever housed it. If there was training or anything that went in, you know, that that was involved, all of that would be paid for out of the IRA. And you could get this to a point where it was ready to be sold, and you could turn and go sell it, and the profit would go right back into your IRA.

28:22 What if I just want it for a lifelong friend?

28:26 That’s prohibited that’s prohibited, it’s prohibited you cannot take physical possession of anything in your IRA. So you you got to have it held somewhere else you can FaceTime it, I suppose.

28:37 Even me out of jail.

28:41 So, you know, I one of the things I wanted to just maybe kind of wrap up on is really the the passive investment side and, you know, when we say the passive investment, right, I mean, it’s the key difference between active and passive, at least the way I try to kind of view it is active means I’m going to go out and actively find the deal. So If I want to go buy a rental property, I’m gonna go find the rental property. If I want to go right alone, I’m gonna go right alone, right? passive investments say, you know what, maybe I’ll rely on someone else’s expertise here. I will let someone else that that knows how to find the right rental properties, go build a portfolio of rental properties and all invest into that. And, and what I’m getting is two big things, right? I’m getting knowledge and experience from the person that’s creating the opportunity, but to I’m getting some diversity, right, because I don’t have enough money in my IRA to go buy 30 investment properties, I can go buy one or two. And then, you know, if one doesn’t read, obviously, I’ve I’ve lost some real diversity there. But if I own 2% of a pool of 30 properties, now I’ve gotten some real diversity in my investments. So passive investments are something we see our clients do. Really probably the most common thing our clients do. When we talk about, you know, passive real estate, obviously you have multifamily funds, you’ve got rental funds, you’ve got You know, low income housing funds, you’ve got affordable housing funds trailer park, mobile home, you know, type funds syndications. So you know, anything that’s that’s syndicated and syndications is doesn’t always have to be real estate, right? We see all kinds of things that are syndicated from an investment standpoint, you know, all the way down to ATM machines, right? as something that could be syndicated mortgage and note funds. So you may not want to be in the business of going out and figuring out who needs to borrow money, but you like the passive income that alone offers and so you can go out in the marketplace and find people that will write the loans for you and find the borrowers and negotiate all the terms. crowdfunding, you know, this is something that is becoming increasingly popular and, you know, crowdfunding gives you the ability to hop onto websites, right and take a look at at some of those offerings right on a website. You know, Which, which is really was created by the JOBS Act, you know, some years ago, and it’s really made a major impact because it’s allowed a lot more, it’s allowed a lot more access to private investors, you know, to access some of these true private investments. Because in the past a lot of the investments we’re talking about, we’re really only available for the wealthy, right? It’s why mitt romney’s you know, investment funds delivered such great results to his wealthy friends. Whereas, you know, crowdfunding gives Joe sixpack right the ability to kind of log on to the website, they got to do their own due diligence, but it gives them access to some of these more attractive, fun level deals. And then private equity and other investment funds. So, you know, the the world of private equity is huge. I mean, you know, Uber Lyft grubhub. You know, if you look at all these companies that we all know of, every single one of them started as a private equity company before it became public. And a lot of these private companies raised money and so There’s, you know, obviously the, we’re not getting calls to invest in Uber, but you’d be amazed how many businesses that that people, you know, maybe operating or starting and sometimes just asking around will give you some insight into some of these products. And so all of those opportunities present themselves.

32:17 So, you know, Jason works for new view, their self directed IRA company, and something I’ve heard lately from investors, I’m talking on the phone, which I still do these days if you guys are new investor to or if we do a pipeline club, go ahead and book a call and we’ll get to know each other a little bit better. But you know, people are like, well, I got it. I got I’m in the self directed IRA account with fidelity or Vanguard. I’m like, Great, that’s a fake self directed IRA. It’s this self directed term has sort of become a little buzzword. I feel like this past year. And the Vanguard’s and all these big brokerages are just calling it that but it’s, you’re still trapped. It’s like you’re in a prison. You just get privileges to go walk around the field but just make no mistake you’re still stuck in the in jail. Guys like Jason with a new view IRA, they are outside of the the jail cell or the jail community. And they are truly self directing accounts. And then if you want to add on to that, Jason but

33:24 yeah, and I gotta I gotta say publicly I love the the prison example because it’s so true. And, you know, if you’ve never been outside the prison walls, you think you’ve got it really good, right? You know, I typically analogize it to imagine if, if the only fast food available was burger chains, right? Yeah, you didn’t know there was such thing as Taco Bell or or chick fil a or, you know any of the other myriad of choices. And so you may think, yeah, because I got Burger King and Wendy’s and McDonald’s, man. I’ve got a lot of real choice here and each menus got a bunch of different things on it and all of a sudden Well, and then you step foot in into a taco bell or something else and realize, well, gosh, you know, this is a whole different menu with a whole different set of opportunities and self directed accounts. You’re right. It’s a term that’s gotten, you know, really kind of used over utilized because it was designed originally to say, Hey, we’re giving you the ability to make your own investments into investments that that you get to choose whereas, unfortunately, we’ve seen you know, a lot of the large brokerage houses that said, Hey, wait a minute, we offer self directed IRAs to you can pick whatever stock bond or mutual fund you want, right? And

34:36 in our in our amongst some crappy options that we That’s exactly right.

34:39 And, you know, so so new trust is is really designed to give people choice and freedom. We are a passive custodian, as I mentioned at the beginning of a city about a billion and a half dollars of assets, over 17 years of business, and people call on us and ask us and trust us to simply provide a similar role that fidelity would provide or Schwab would provide, but they do it under the auspice that they’re going to go find their own investment, do their own due diligence and not be forced into the stock market. I mean, that’s really why people come to new view.

35:12 And I thought you’re gonna go a different direction with that now and see and talk about the shower scene with the soap. How you’re getting out of paying all those fees, right.

35:22 Oh, man, you know, and we may have to talk offline on how to build on that prison analogy. There’s this sounds like there’s some opportunity there.

35:29 Yeah. Well, I’m with the final minutes here that I have with you. Can you talk about UDF fi and, you know, those are going into investments utilizing leverage?

35:40 Sure. Yeah. So one of the things that that, you know, we tell the story about tax free growth, right. And we tell the story about not having to pay tax on an annual basis. But there is an instance where the IRS may impose a tax on your IRA and I use the word May. The most common one is when you take on debt, right, the IRS Rest says if you’re going to take on debt, whether directly, you know, meaning the IRA gets the loan or indirectly through some sort of passive investment fun. The IRS says, you know, if you have 50% debt, meaning 50% of the property is leveraged, then we’re going to look at potentially taxing 50% of your game. It’s called UDF. I unrelated debt financed income. The other tax that is similar, it’s called EBIT, unrelated business income tax. And it says if you invest into an operating business that doesn’t pay tax, we pay tax on that as well. And a lot of people get scared of that. And I want to kind of share a couple of things. Number one, if you invest into Microsoft, Microsoft pays tax, they pay corporate tax, and then whatever they earn right is where you earn your money as an investor. If you invest it into a private company like Microsoft that didn’t pay tax, then the IRS says you still have to pay the tax somebody does. So you’re not getting taxed twice. Right people Realize that every publicly traded stock is a C Corp, there are, they’re all paying tax. So you’re just getting less profit because it’s after tax whereas in an IRA, you may have the opportunity to invest into a private company and get pre tax earnings, right. So you get more money and then you got to give a little bit of that back in the form of tax. Same thing on the loan side, if you take an IRA, and you take $50,000 and you go buy stock, the most stock you can buy with that IRA is $50,000. So your ROI will never exceed, right the the the maximum amount of your your the dollars that you can put in because you can’t use leverage. But in an IRA that’s self directed outside the stock market, there are banks all day long, that will take your 50 grand and lend you 50 grand and let you go buy $100,000 property. So even though you may incur a tax as a result, think about the difference. In one case you invested 50 grand right and the other case, you Put up 50, but actually invested 100 grand. So if the investment makes 10%, right? In the $50,000 example, I made five grand. In the example with leverage, I made 10 grand. So even if I pay two or $3,000 in tax, which is way more than it would be my net return, if I paid $3,000 of taxes seven grand, well, how much did I invest 50,000 bucks. If I invested 50,000 bucks and made 10%, I only made five grand. So what would I rather make 10% on the levered hundred and pay a little tax, or 10% on just the 50, right and go for cash on cash. So, levered returns make tremendous sense. Don’t let anyone out there, regardless of their sales tactics or scare tactics, tell you that you bid is is something you shouldn’t do. It should be considered it should be evaluated. But I can draw up examples all day long, where a good investment that’s levered will yield you far better results even after tax. So and I’ll end with this If you if you are buying real estate specifically levered and you qualify for the self directed solo 401k, which we can help you do, that tax doesn’t even apply to you. Right? It’s not applicable in a solo 401k, which is awesome.

39:16 You know, the funny thing is like, I think most CPAs and accountants don’t have a clue what EFI is. I’ll even know if they would put it on your tax form.

39:26 No, we have a good handful of accountants that we refer, you know, clients to, because clients will ask and we’ll tell them, you know, go do the math, right. I just got it.

39:35 This is how it’s supposed to be done. But hey, man, if your professional doesn’t do it the right way. That’s on down. That’s right. But yeah, I mean, you know, you got to work with the right people. But help me understand this. So like, if I go invest in Microsoft, Microsoft is has I’m sure they’re levered, right? They have debt, to some extent to probably a great extent. How’s that different than if somebody invests in a 75% levered deal? And then, you know, why is there a difference? It’s the same thing. I feel like I live in unfair world.

40:14 Well, you won’t hear me say this very often lame, but but it actually is fair. And I’ll all kind of help you understand why. If I go invest into Microsoft, yes, Microsoft is levered. But all of those profits, including the levered profits are subject to tax at the corporate level. Microsoft will pay a corporate tax on levered profits. So the government is getting their, you know, proverbial hand in the cookie jar on it. If I go invest into a passive fund that has 75% lever, there is no corporate tax at the fun level. So the money itself, there’s levered profits that are not being taxed. If they passively give those to lane, an individual. You got to pay tax on your levered profits as a whole. Whole, right because you bought it personally, if Lane’s IRA invest, they’re not going to tax lien on all the profits, they’re only going to tax lien on levered profits. So if there’s been this world that’s built up out there that would suggest that that leverage in an IRA is scary. And I turn around and say leverage in an IRA is the best thing. And I’ll give you kind of a quick example. If you took an investment lane, and let’s just use 50% leverage, because it’s math I can do in my head, if that’s fair, but if you put $100,000 into an investment, and let’s just say it doubled, right, you made $100,000. When you get that return, personally, right. You don’t have to pay tax on anything but your profit, your profit was 100,000 bucks. If you’re in a 25% tax bracket using all round numbers, right? That would cost you 25 grand. So you invested 100 made 100 pay 25 in tax and ended up in theory with 75 grand right? So you’re you’re rich Turn on investment was 75%.

42:03 After tax

42:05 after tax, if you did the same investment, right, and instead of using your personal money for that hundred grand used your IRA, you put in the same hundred got out the same hundred in profit. In this case, instead of the whole hundred being subject to tax, only the levered portion is, so if it’s 50% leverage, only 50% of your profit in this case is taxable. And again, I’m using round numbers. If you take the 50% and let’s assume that the tax is 30% that cost you $15,000 or a little over like $16,000 in taxes. So if you take the hundred that you made, subtract out the $17,000 rounding up, right, you you would now have a profit of $83,000. Well, if you compare that to doing it with your personal money, you have 83% return instead of 75. percent return, you’re actually coming out ahead. Yet there’s people out there that would say you shouldn’t do it in your IRA because the tax is bad. And I’m making a worst case scenario. You know case you’re saying the tax Yes, it sucks to pay tax. But what it what it sucks is not to take advantage of levered gains, because the power of leverage is so great. And the beauty is, if you qualify, we can set you up in a solo 401k where you can put in 100 make 100 and not pay a penny of tax even though it was levered because 401k plans are exempt from UDF phi. So three different scenarios all paint the picture that doing this in your personal money is the least efficient, the IRA is the second most efficient and the solo one 401k is the most efficient in that Tax Scenario. A few

43:51 you guys might be thoroughly confused, which is great, which is on the path of progress. And then this is what we do in Are you know our coaching our journey program you guys can take a look at that it’s simple passive casual comm slash journey which is our accelerator mastermind. And you know if you guys want to get fine tuning coaching on this go to simple passive cash flow comm slash coaching for more of the family office offering services but if you guys want to replay this webinar and take a look at the slides go to simple passive cash flow calm slash q Rp. shoot me an email if you want to get connected with Jason. Yeah, this is a good stuff good stuff. Oh, if you want to get the cool ideas, the fun ideas like you know, Jason’s lightning, the bottle technique. You’re gonna have to come out to Hawaii at the next mastermind in January. But appreciate Jason for coming out, man.

44:49 Hey, thanks for having me. It was a good time for sure. And I don’t know if that was an open invite to me, but maybe I’ll see out there in January. It sounds fantastic.

44:58 Yeah. And now you want to come all the way out here to hold Florida well we’ll get you out there on this

45:04 awesome thanks les

45:10 this website offers

45:11 very general information concerning real estate for investment purposes every investor situation is unique always seek the services of licensed third party appraisers inspectors to verify the value and condition of any property you intend to purchase. Use the services of professional title and escrow companies and licensed tax investment and or legal adviser before relying on any information contained here and information is not guarantee as an every investment there is risk. The content found here is just my opinion and things change and I reserve the right to change my mind. Above all else, do your own analysis and think for yourself because in the end, you’re the only person who is going to look out for your best interests.

How can I use part of my Roth IRA to buy passive income property, what you’re going to need to do to investor author is you’re going to need to probably move over to a IRA custodian that allows you to self direct. Now, a lot of these guys like Vanguard or fidelity was at something America with these big firms that offer investment options. They have what I call a fake self directed IRA accounts. We’ll call it self directed IRA accounts, but all it really does is allow you to invest in dirt or other garbage mutual funds and stuff like that. They’re not true self directed IRA accounts, what you’re trying to find as a self directed IRA custodian, such as you know, a lot of our investors will use quests, I used to use IRA services, they’re pretty good, cheap option, but these guys they’re just custodians who just hold on to your money and they administer the money. Once you get the money to these guys, then you can invest it or where you want. Of course, there’s you know, you have to follow a prohibited transaction. rules you can Google that I think you can’t buy things like artwork, or there’s all this list of like things you can’t buy. But if you’re buying income property, you should be fine. Some things to know when you’re transferring from your current IRA company to the IRA, self directed IRA custodian, it’s going to be hard, these guys aren’t going to make it easy for you, you know, you’re breaking up with one company, the customer service on that end is not going to be as good as it was on the way and so it might take two or three months, or two or three weeks of you constantly kind of badgering them. But once you kind of get it out of there, and you have it in the account, some of them will set up like a checkbook IRA, where you can just easily make or write a check. The one I had, I had to do all this paper, you know, a couple pages without what I was investing in, and then the key is that they they’re sending money on your behalf and you’re kind of staying out of it so that you don’t blow up your IRA account. I personally am not a big believer in any retirement accounts, Roth IRAs or Any pre tax IRAs unless your net worth is over two to $4 million. At that point, maybe you should do a Roth, a lot of like syndication deals and just real estate in general, you get a lot of good tax benefits from depreciation that comes from the property. When you’re investing within a IRA account or retirement account, you do not get to partake in those advantages. Another reason why I don’t like IRA accounts is because you have to wait till you’re like 60 or 70 years old. I’m trying to live for today I want to, I’m trying to I’m buying income property so I can create mini pensions today and work backwards and create cash flow today that grows and grows and grows so I can buy more and more investments so I can grow more and more. I am probably going to reach retirement, the pinnacle of retirement what we all think, which is more of a financial freedom number well before I hit 60 now not saying that’s for everybody, but I think for a lot of us who are investing the right way, it usually takes five to 10 years of doing this method. To be out of the rat race, and at that point, you’re not going to want that money locked up in some Roth IRA account or IRA. So that’s why a few years ago, I made the conscious decision to never invest in that stuff ever again and I just invest out of my own liquidity out of cash accounts.

“A couple weeks ago I created a couple LLC’s for my IRAs (one traditional and one Roth) for investments in syndications. I talked briefly to my CPA today and I think I’m throwing in the towel and canceling all investments using debt (all of them) with my IRA’s. The cost of money (LLC’s annual fees, XYZ of SDIRA Custodian annual investment fees, the 990-T income tax returns) and time and energy eat up too much of the profit and are too time consuming to make the syndications in SDIRAs make sense for me.

I’m still trying to think if there are other investments I can make with this cash that does not involve the leverage, but I will most likely just suck it up and put it back at Vanguard in crappy index funds and try to pull it out as I can over the next few years without getting into too high of a tax bracket.

Hui Investor

Over it with QRPs

Brace yourself!

I am very against 401Ks because you can only choose from crappy option that have heavy fees.

I don’t really like Self Directed Roths or any tax sheltered retirement accounts either because you are subject to UDFI (more details below) and cannot leverage your investment which is a pillar in real estate investing. If you want to do one here is a big list of them. Knock yourself out but I cashed out mine a while ago because I plan to live off my cashflow and retire well before the Government allows you to tap into your retirement account.

If you have distrust on where this country is going you need to expect that taxes will go up in the future. How else will we pay out for all these bank bailouts and quantitative easing.

Why cash out your retirement and use it to invest

You will pay taxes now or later and you will likely to pay more taxes in the future because you will make more money… so pay it now. Most people think they will be in a lower tax bracket in the future because they plan to downgrade their lifestyle… this is again incorrect money myths that are so prevalent.

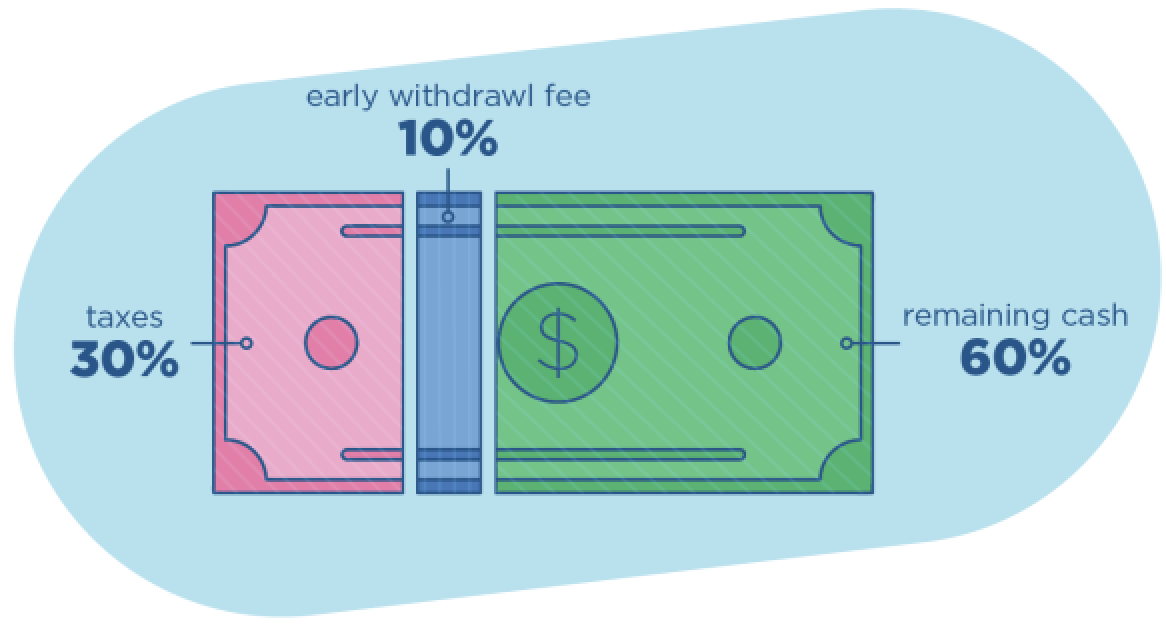

By taking you money out early you will incur a 10% penalty but if you understand how you can easily get 20-30%+ returns in real estate a year that 10% penalty is nothing. You can recoup that in 6-18 months.

It’s a no brainer… the numbers don’t lie. Do the math.

But my family will disown me!

Yes taking money out of your retirement account is a sin for most people.

Just make sure you don’t buy jet skis and put it in cash flowing assets like rentals or syndications. Or start a business if your are exceptional at business.

In-Service Withdrawals (401k)

Unless you are age 59.5, fired, die, or leave your current employer you company sponsored/owned 401(k) are stuck where they are.

In-service withdrawals can be made as a hardship withdrawals if the plan allows if there is a “immediate and heavy financial need” per the IRS. Straight forward examples of these are medical care expenses, or educational costs and payments needed to prevent eviction from a principal residence. You just need to be able to explain how you exhausted all other distributions or nontaxable loans under the plan. You can only take our the employee’s elective contributions. The income or the money that you made can’t be taken as a hardship withdrawal. If the plan allows, the employer’s matching and discretionary contributions can be factored into a hardship calculation.

Most withdrawals will have a 10% early withdrawal penalty however, the 10% premature penalty tax can be waved if the in-service withdrawal or hardship distribution is used to cover medical expenses that exceed 7.5% of adjusted gross income (AGI) or if it is used to make a court-ordered payment to a divorced spouse, child or dependent. Other exemptions are defined by the IRS.

Read up on the IRS website, ask your HR department, and make sure you talk to some who gets it.

The Silver Bullet

QRPs or qualified retirement plans (Solo 401ks, checkbook IRAs, etc) are the answer to that person with a bunch of money in their existing 401K or IRA.

It’s pretty typical that someone listens to the Simple Passive Cashflow podcast, signs up for the investor club, and books a free intro call has 200k-600k locked up in garbage retail investments AKA 401K.

Stop whatever you do don’t roll-over an old employers 401K into your current employers 401K. If you have money in your current employers 401K its stuck there. You need to quit your job. Well there is this one obscure tactic if you live in a Red state that could work but for you it’s easier to take a loan from the existing 401K to start investing in hard assets.

Anyway let me know you would like a referral to my checkbook ira contact. And get the free book on QRPs!

If you are conservatively using prudent leverage and finding decent deals there is no reason you should not be able to retire in 10 years or less and thus negating the very reason for these accounts that you can’t touch till you are old.

When you have money in these accounts it sounds good that you are not taxed on gains but you are restricted from getting a Fannie Mae loan. Using SDIRA’s you have to get second tier financing options because its more risk for the bank, for example, a Roth IRA can buy real estate on leverage, however, will need a non-recourse loan which is often a fraction high-interest rate and lower LTV. No Bueno!

Caveat: If you are late to the game and already have a 401k over $100,000 then you should convert it to a solo401k. At that point, you should think about putting it into a syndication since you are restricted on how you can leverage it.

I work with people to come up with a strategy to withdraw their 401k to minimize taxes. Sometimes we need to get creative with oil & gas investments, land conservation easements, or bonus depreciation.

Let’s say you choose to make an early 401k withdrawal of $100,000. (You personal tax bracket will be different):

Federal income tax of 25% = $25,000

State income tax of 7% = $7,000

Penalty tax of 10% = $10,000

Technically you can get a early withdrawal but withdrawals made under the age of 59½ will not be subject to the 10% early withdrawal tax under any the following circumstances:

You pass away and the funds are withdrawn by your chosen beneficiary

You become permanently disabled

You terminate employment and are at least 55, or 50 if you work for the government

You withdraw an amount less than is allowable as a medical expense deduction

Your withdrawal is related to a Qualified Domestic Relations Order after a divorce

You begin a series of “substantially equal payments”

You are a qualified military reservist called to active duty

What is the largest source of Revenue for the US IRS?

401K, SDIRA, IRAs, even Roth’s when not if they can change the tax laws. Basically qualified retirement money.

People are not spending it and you can bet the IRS is going to get it.

What is a QRP Retirement Plan? It’s a tax-sheltered investment vehicle that you can invest in pretty much anything where your money grows tax-free but it is intended for retirement and the downside (why I don’t do one personally) is that you can’t touch the money until you are old 🙁

If you are running low on cash because you have been picking up deals left or just broke because you have been listening to mainstream dogma and you have money in your retirement plans this is for you!

Here is the webinar! Enjoy and send me questions to post the answer below.

If you are late to the game of investing in alternative investments like real estate (imagine that) and already have a large 401K over $100,000 then you should convert it to a Solo401K or Solo401k Roth version. At that point you can slowly take money out to minimize your taxes (not go into the highest tax bracket) and invest in the meantime as you “leak” the money out of the Governments control.

Follow up to Hui Questions for the QRP and other retirement plans

What I personally do