Have you ever found yourself browsing endlessly online to simply know more about Cost Segregation to save on taxes without all the superfluous tax talk? Search no more!

As a real estate investor, imagine using Cost Segregation as a real property investment strategy that will grant you tax free cash flow from fixed assets and allow you reinvest even more (and possible lower your ordinary income).

What is Cost Segregation?

This is one of the easiest and fastest ways to squeeze a little extra profit out of an investment. If you have ever played those racing video games where you modify your car (like Gran Turismo) it’s like paying for that cheap computer chip upgrade to get an extra horse-power boost, it’s a no-brainer.

For those of you who aren’t ex-gaming nerds like me, it’s “low-hanging fruit”.

A cost segregation study gives a tax benefit to the taxpayer to take advantage of current bonus depreciation laws (starting to phase out slowly in 2022) in order to depreciate their assets by taking a loss on paper.

The cost segregation specialist/engineer analyzes the components of a commercial real estate asset to create a cost segregation report to equip the tax accountant or CPA the needed breakdown of the asset in order to make the depreciation determinations.

To better understand the benefits of performing cost segregation, you must first understand depreciation.

Depreciation is where you reduce the value of your assets (in this case, your real estate properties) due to natural wear and tear over time. There is a type of depreciation wherein the value of your fixed asset (real estate properties) depreciates faster than it should be. This speedier depreciation or most commonly known as accelerated depreciation.

Let’s look at it in detail: If you own commercial or residential real estate investments, you can depreciate your real estate holdings. A commercial property establishes a 39-year depreciation schedule and a residential property establishes a 27.5-year depreciation schedule. These are the numbers we will use to calculate the rate of our depreciation deduction.

Envision a 3 bedroom single-family home in Birmingham, Alabama that is worth $100,000. Of that, approximately $65,000 is determined to be the building value and $35,000 is determined to be the land value. Each year you can deduct 1/27.5th of the building value, which is about $2,363 a year that can offset income gains. $2,363 can be taken for the next 27.5 years until all the value on paper is depleted.

Is there a catch?

Unfortunately, you cannot deduct the value of the land unless you have made a land improvement, granting that the improvement you made has a “useful life” that is depreciable. Only the improvement will be depreciable, not the land itself.

When you sell the asset you will need to recapture the depreciation. This is the major disadvantage to a cost segregation.

We pay $8000-12,000 on our larger commercial assets to do a cost segregation and our advisors tell us that the general rule is to do a cost segregation if we intend to hold onto a property more than 3-5 years because if we sold quicker than the time benefit to the passive losses we got as investors you be less and might not be worth the price of the actually cost segregation study.

But, guess what?

There are some exciting new benefits to passive losses since Mr. Trump enacted a tax law where 100% Bonus Depreciation creates substantial benefits on your taxes for the acquisition year. In the future, us investors are crossing our fingers that this part of the tax code sticks around.

Previous

Next

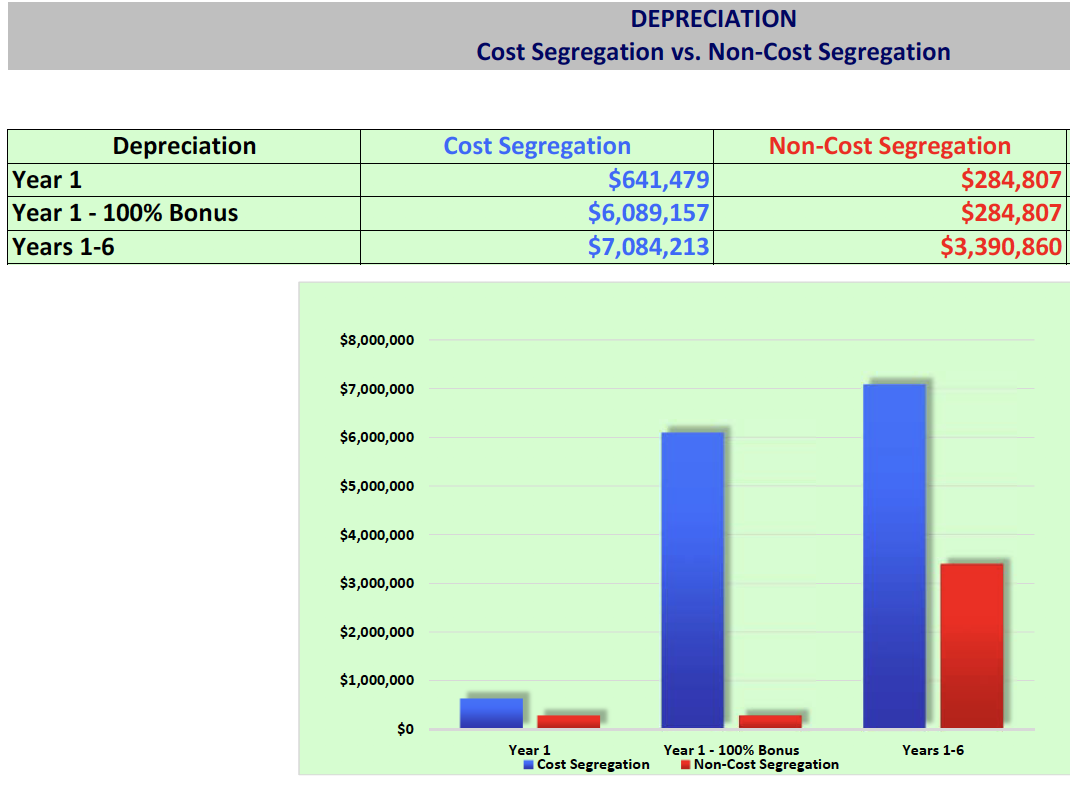

Think about this: My $3M, 52-unit apartment, is looking to get more than $266K in tax savings (at 37% tax rate) in the first year of ownership by doing a cost segregation.

If you are interested in learning more about how to best utilize your passive losses, you can learn more here.

Cost Seg Tips and Best Practices

https://www.youtube.com/watch?time_continue=2&v=fjlUugCApaI&feature=emb_title&ab_channel=SimplePasiveCashflowdotcomhttps://www.youtube.com/watch?v=revK1FkH6-Y&ab_channel=LaneKawaoka

What is a Cost Segregation Study?

Companies and investors who have constructed, purchased, expanded, or remodeled any kind of commercial real estate (including 1 to 4-unit residential rental properties) since 1987 can use cost segregation studies for maximize their tax savings.

The study allows the owner to take advantage of accelerated depreciation deductions and defer federal and state income taxes on the reclassified building components mentioned above.

A team of real estate investors evaluates several personal properties, residential rental property, and land improvements that can be upgraded to improve the value of the property. Those improvements are assessed with the assistance of a Cost Segregation specialist. After completing this cost segregation analysis, the property owner may deduct the depreciable life of the individual fractional interest (IFI) through a cost segregation study, with or without depreciation. If the taxpayer is eligible and has not failed to take advantage of the tax rebate, the taxpayer may claim the expense directly within the given year of the seller’s ownership.

To elaborate more on Accelerate Depreciation Deductions, it is a deduction of the cost you pay to a person if you own your personal property assets. The accelerated depreciation deduction provides significant tax savings but it is not another type of benefit. The exchange of property owners whose benefit is primarily from cost segregation is a limitation in tax savings. The depreciation expense is deducted at the source rate in another year.

What are the Benefits of Cost Segregation?

-

Lower Property Insurance Premiums

Since it generally costs less to insure personal property, versus real property, building components reallocated as personal property should reduce your insurance costs as well which will yield potential benefits in the end.

-

Capture Retroactive Savings

Since 1996, taxpayers could capture immediate retroactive savings on properties added since 1987. Previous rules, which provided a four-year catch-up period for retroactive savings, have been amended to allow taxpayers to take the entire amount of the adjustment in the year the Cost Segregation is completed.

This alone is huge!

This opportunity to recapture unrecognized depreciation in one year presents an opportunity to perform retroactive Cost Segregation analyses on older properties to increase cash flow in the current year.

What Components Can I Reclassify?

Components of a specific property or qualified leasehold improvement are identified and reclassified for depreciation over a shorter time (5, 7, or 15 years). For example, 30% to 90% of the total electrical costs in most buildings can qualify for 5 or 7-year depreciation.

-

5- year tax-life components

Non-structural elements: carpet, decorative lighting and trim, HVAC systems, dedicated electrical and plumbing, and security systems.

-

7-year tax-life components

All telecommunication related systems: cabling, telephone, etc.

-

15-year tax-life components

Exterior land improvements: landscaping, curbs, sidewalks, fencing, and signage.

As a Passive LP investor the details of this is not needed as all you need to ensure is that your sponsor is aware of cost segregations to optimize tax benefits.

What is required to have a study done?

You need to provide as much of the original documentation pertaining to planning, construction, and current tax depreciation as you can.

This could include a complete set of:

- Construction plans

- Current tax depreciation records such as tax returns, building cost budget information, final AIA (American Institute of Architects) appreciation

- Document of certification of payment or other cost information, change orders, direct or indirect costs paid by the owner that are not included in other documents

- Other information depending on the project

How much does a Cost Segregation Study cost?

On average, the total fee will generally fall between 5% and 20% of the estimated net present value tax saving. You can often get a free preliminary analysis to help determine this. This can be impacted by how large or small the real estate project is.

In addition, the location, accessibility, and quality of the records and documents will impact the entire cost (costs typically range between $8,000-$12,000). Minimum fees can be as low as $2,000 for small projects, and some firms GUARANTEE a minimum of 500% ROI (fee vs. tax recovery) on projects over $500,000.

Cost segregation studies are typically cost-effective for larger syndication buildings purchased or remodeled at a cost greater than $100,000. A cost segregation study is most efficient for new buildings under construction, but it can also uncover a retroactive tax deduction for much older buildings as well.

What are the steps involved in the process?

First off… if you are a Passive Investor (LP), your sponsor should be taking care of cost segregation for you so you will have one less thing to worry about.

If not, the cost segregation process can be broken down into the following steps from start to finish:

Vet Cost Segregation Firm

Engage a reputable Cost Segregation firm that utilizes engineers and architects trained in Cost Segregation and it’s application to the proper allocation of assets. If you need a referral go here.

Document Review

The engineer determines what documents are available (e.g. planning, construction, invoices, appraisal, and current tax depreciation) for reference and referral.

Schedule Property Survey

The engineer then sets a schedule for surveying the subject property and gathering the available documents for review prior to arrival at the subject property.

Document Recreation

For those documents that are unavailable, time is then scheduled into the Cost Segregation process for document recreation using known industry standard costing data (Marshall & Swift and/or RS Means costing publications). The process takes about 4 to 6 weeks after all necessary documents are acquired. The time that a Cost Segregation Study takes depends on the size of the project and the completeness of the documentation that you can supply.

Conduct Site Survey

The site survey is executed and completed. Surveys can be completed within as little as an hour, but it varies between each survey. Measurements are taken and all areas are photographed for IRS verification and substantiation of asset values during the survey.

Calculations

The engineer returns to the office and crunches the numbers. The number crunching process is when all documents are reviewed in detail, assets are verified, and measured against known costing data, and asset reallocation is applied.

Review

A review committee then examines the results of the analysis completed by the engineer of record to verify its veracity and confirms it meets and exceeds IRS guidelines per the Cost Segregation Audit Techniques Guide.

Compile Report

Once approved, the study results are compiled into a final report that includes: all IRS tax code to substantiate the reallocated assets, spreadsheets identifying all assets categorized according to their building codes, representative photographs of the reallocated assets, and the engineer’s credentials for IRS review.

Issue Report

The final report is issued. The client and CPA of record receives digital copies via email, for application to the client’s tax return.

Cost Segregation Example #1

Depreciation is distributed to investors on the K-1 Form in syndications.

Not making any promises as depreciation amount is primarily based off building specifics and the amount of leverage used in a deal, but here is a real-life example from a $50K LP investment in a Class C apartment syndication in the first year K-1 in 2018 which yielded a $36K paper loss by utilizing a cost segregation. Extract 10-20x what you normally able to deduct in the first year alone! Take these passive losses and employ the “Simple Passive Cashflow Gravy Train” strategy where you offset your ordinary/W2 income with real estate professional status. For more details on that check out our Master Tax Guide.

Previous

Next

If this is a new concept to you, you may be able to go back to previous years taxes and get back some benefits this year. Oftentimes, getting a quote is free and quick.

A recent quote I got back for a few properties:

Previous

Next

Cost Segregation Example #2

We purchased a $20M apartment and are about to write off $6M in the first year! The total capital raised from investors was $5.5M, that meant almost a dollar for dollar deduction in year one!

52-Unit in Des, Moines Iowa Case Study:

Previous

Next

Other FAQ’s

Are cost segregations something new?

Cost segregations are not new. On the contrary, they have been in existence since 1954, when the IRS allowed for certain personal assets to be accelerated into a shorter life class. However, it wasn’t until Hospital Corporation of America sued the IRS in 1997, and won, that the IRS revisited the issue of accelerated depreciation. The IRS ruled that property qualifying as tangible personal property under the former Investment Tax Credit (ITC) rules, would also qualify for purposes of federal income tax depreciation under MACRS (Modified Accelerated Cost Recovery System).

The IRS Chief Attorney wrote a memo saying, “. . . Cost Segregation, for it to be properly applied, had to involve those with competencies in architecture, engineering, or construction and/or construction techniques, in order for personal property assets to be accurately identified and segregated.” As a result of this memo, cost segregation became a viable tax-saving strategy allowed by the IRS.

Can’t my CPA do a study for me?

CPAs are not qualified according to the IRS guidelines. However, most Cost Segregation firms will gladly work with them on a consulting basis to complete the work for you. Remember, the IRS Chief Counsel issued a memo that made it clear what constitutes proper “methodology” in applying Cost Segregation, and it must be done by people who are competent in architecture, engineering or construction and/or construction techniques. You will want to ensure you are working with a cost segregation specialist to follow correct protocols. See ” Is Cost Segregation something new? ” above.

Why bother do a cost segregation to accelerate the depreciation? I’ll eventually get the deduction.

As investors, we like paper depreciation to occur earlier because that offsets gains earlier and gets more money in our pocket earlier. Just like how you give a mouse a cookie…. Give an investor a dollar early and… they will turn em’ and burn em’.

In other words, you are not creating more depreciation, you are shifting it earlier to take advantage of the time value of money concept.

On the project-level in a single asset LLC arrangement, the more you can lower your tax liability, the more you can significantly increase your passive income and create more value for investors.

A cost segregation study, in effect, gives you an interest-free loan from the government for the first 15 years, which you will then repay interest-free over the remaining 25 years. Wouldn’t you rather have your money now? There are also advantages in doing a study if the building is going to be sold (via 1031 exchange) or if the owner of the building dies.

For bonus depreciation, we just need to acquire. The cost segregation study can be completed in the next year (in this example, 2021).

How much will I save on taxes?

Most cost segregation firms will perform a free analysis if you provide your basic property information and tax rate. From the information you provide, they can calculate a conservative estimate of the accelerated benefits you can expect, as well as their fixed fee proposed for the final study.

Typically, tax savings from 5% to 10% of the building’s original tax-basis are generated, but there are instances where it can be substantially more. Each property and circumstance is unique, so it requires a case-by-case approach to give you a definitive answer.

How much accelerated depreciation can I get for different commercial properties?

Certain types of commercial properties can be grouped together to give us an idea of the percentage of those types of buildings eligible for accelerated depreciation. Your results may be greater, or less than those quoted here, but in general, property that falls into one of the following categories is most likely to result in accelerated depreciation within the specified ranges.

Commercial Property Types:

- Apartment Buildings 15 – 25%

- Dental/Medical 30 – 60%

- Health Care 25 – 65%

- Heavy Manufacturing 30 – 80%

- Industrial 25 – 70%

- Light Manufacturing 20 – 45%

- Office Buildings 15 – 25%

- Research & Development Facilities 30 – 75%

- Restaurant 15 – 30%

- Retail Centers 10 – 25%

- Senior Living Facilities 15 – 30%

- Warehouse 5 – 15%

Will a study increase the chance of an audit?

A study conducted by a reputable Cost Segregation firm should strictly adhere to the IRS Cost Segregation Audit Techniques Guide . The type of study most firms perform places you in Internal Revenue Code Tax Compliance, which actually decrease your chances of an audit. However, you should be aware there are six different Cost Segregation methods allowed by the IRS, and not all are of equal merit. There is currently no standard method, and there is still some ambiguity about which method is best. If you have heard conflicting information about what is, and is not possible regarding Cost Segregation, it really depends on which method is being used.

Will I be assisted in the event of an audit?

A reputable Cost Segregation firm can assist you in the event of an audit. They will focus on doing the Cost Segregation Study to create documentation and support for conclusions so that these are easily communicated and resolved with the IRS. In fact, you should expect a final report that is “all inclusive”. The report should quote specific Internal Revenue Codes related to the reallocated assets. Additionally, it should provide photographic evidence of these same assets for complete substantiation of the assessment. A properly documented Cost Segregation Study helps resolve IRS inquiries at the earliest stages.

What if I lack some of the needed documents?

A cost segregation study can still be performed even if you lack some of the necessary documentation. Construction, engineering, and other specialists will do an extensive site visit. They will measure and estimate using currently accepted costing techniques and pricing guides (such as the IRS-recommended costing publications Marshall & Swift and RS Means ) to determine the costs that qualify for shorter recovery life periods.

Who do I contact for additional info?

For more information on Cost Segregation or a free analysis, contact me for a referral Lane@simplepassivecashflow.com

Reward Yourself

Combine cost segregations with an Opportunity Fund Zone deal and wow!

Why Syndication Investors do no do 1031 Exchanges?

I paid 4% in taxes in 2018 because of the passive losses that real estate gave me.

Bonus depreciation has made 1031 Exchanges obsolete, group your passive losses on non-participatory deals as a real estate professional – more info.

(Here is a cheaper service for cost segregations for single family homes or under $2M assets, but I am personally a little skeptical).

The video below shares some of my thoughts against a 1031 exchange because you are a distressed buyer.

Additional Resources

Cost Segregation Basics

Depreciation Examples

Investor who received $98,000 in Passive Losses from investing $100K

Why Real Estate Became Better Than Gold

Do KPs or Loan Guarantors Receive Depreciation?

Nate Busch Tax Company

Sample K1 Form

Dental Office Case Study

Pre-Construction Case Study

Ranch Resort Case Study

What’s next? Join the Club!