1) Listen to the first 8 podcasts. These were recorded back in 2016, and since I have moved on to syndications but was created as a foundation to help people get started with rentals like I did in 2009 when I was straight out of college.

4) Join our club and get access to private opportunities. We only work with people we trust so let’s start building a personal relationship. Lets jump on a phone call!

https://www.youtube.com/watch?v=PKLrtUeCAIc&t=37s

Aloha! I’m Lane!

Welcome to the SimplePassiveCashflow.com podcast community!

I used to be an Engineer at a day job I did not like and I thought there was more to life as many of us high paid professionalsthink in our tribe. I used rental real estate as my means to financial freedom and I’m curating the content on this website and our eCourse so others can do the same.

Glad that you have joined us on this journey and hope you can help us with our Mission.

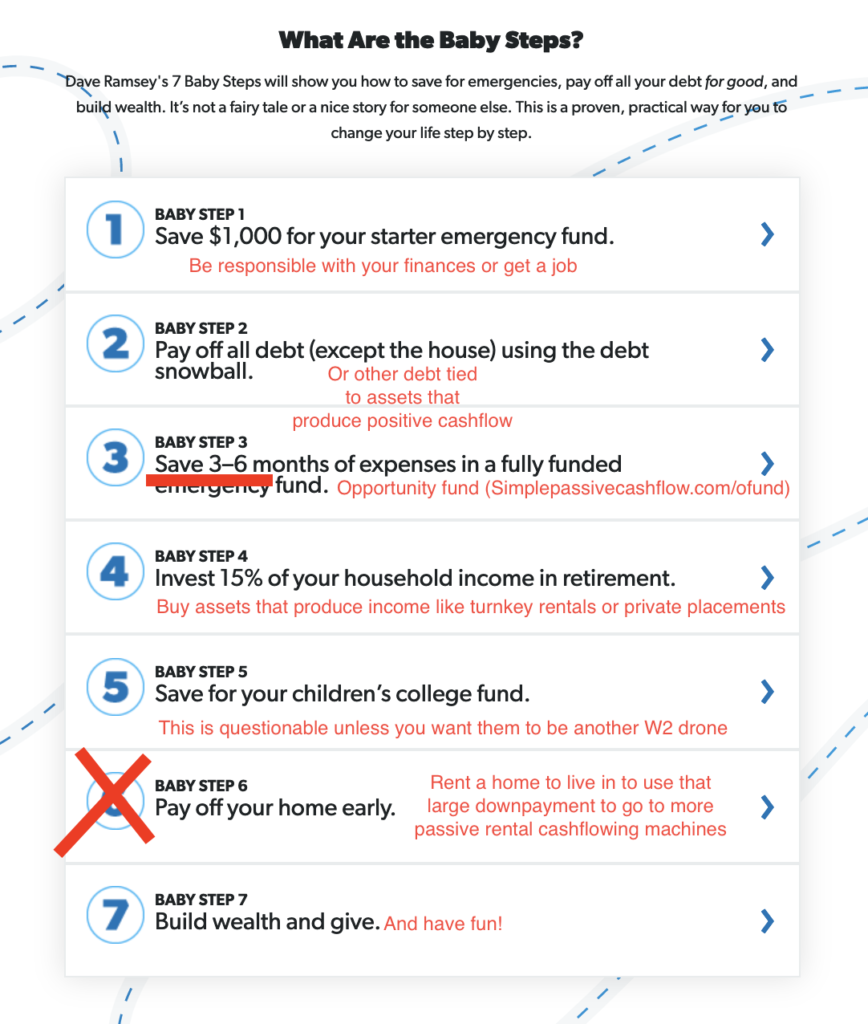

From 2009-2013, as I was buying rentals on my own I definitely made my share of mistakes. One of these was to paying down my mortgage (debt). Here is one of those checks where I paid down my debt. Little did I know that sophisticated investors don’t do this.

“My wife is officially is quitting her job at the end of this year. Thanks for helping us be able to do that. One of her friends had to go back to work 10-weeks after having their second kid because they need her income to pay the mortgage. It makes me cringe just thinking about that.” –Hui Deal Pipeline Club Member

https://youtu.be/2yvR4h9thos

The Top SimplePassiveCashflow Posts:

This website has been going through daily improvements everyday since 2016. I admit things are a bit all over the place as I learn about these investments and wealth tactics. The following are the top posts on this website and a good starting place.

I know I was beating the drum of the Turnkey rental a few years ago but now investing in Syndications. (Turnkey rentals are not passive and still a PITA) I am admittedly a work in progress and this website/podcast is my journey.

Mainstream investing (401K, stocks, mutual funds, 529, IRA, or anything retail) is based on investing for appreciation. You know buy-low-sell-high …. usually based on factors wholly outside an investor’s control.

Then one day (when you are grey and immobile) retire and live off your nest egg at 4% withdrawal rate.

We (us sophisticated investors) call this gambling not investing.

in·vest / verb

to put money to use in something offering potential profitable returns, as interest, income, or appreciation in value.

Buy-low-sell-high trading mentality encourages the churning of holdings … which generates commissions and short-term capital gain taxes. Which is another reason why we do not like commission based Financial Planners or Registered Agents. Some of these guys use hard-selling techniques. If they make enough phone calls, eventually they get someone to purchase a stock and make their commission.

“Wall Street is the only place that people ride to in a Rolls-Royce to get advice from those who take the subway” -Warren Buffet

In case you have not seen this whole financial world is an engineered system by Wall Street firms and the government which protects them, to prevent Main Street investors from building enough passive retirement income in your 30s/40s as opposed to your 70’s. The mainstream financial news never talks about yields coming from cashflow (income minus expenses). Discussions focus in the context of share prices. It’s pattering you to think buy-low-sell-high. Churn and cha-ching for those executing transitions in the industry. And for most people who are confused and freeze that’s why there is a hidden asset management fee which is an above the line expense to you.

http://www.cfiresim.com/

“We know what is going to happen if you keep investing in the same old stocks/mutual funds/bonds… you will keep working at your job with a lackluster retirement in 40-50 years. Invest in real estate for cashflow is a proven way that I created my pension today and allowed me to retire before I hit the age of 34. Do the math… the numbers don’t lie… people do” – Lane Kawaoka

The secret… Is not about appreciation but cashflow. Creating multiple mini-pensions today as opposed to hoping and praying you have enough to deplete from during your dying days.

How do we ensure not losing money?

Buying assets where the Rent-to-Value Ratio is more than 1%, is needed to be able to cashflow after expenses. You find the Rent-to-Value Ratio by taking the monthly rent dividing by the purchase price. When I am looking at potential investment properties the rent-to-value ratio is the very first metric I look at with evaluating an investment. To calculate this metric you take the monthlyrent divided by the purchase price/value. For example a home that rents for $1000/month that costs $100,000 has a rent to value ratio of 1% (1,000/100,000=1%). The higher the better. I typically look at a huge list of properties so using excel to make this calculation is the best practice.

It’s sort of like using the dating app Tinder… but with a filter…. I’ll stop there… to learn more click here.

What’s up folks? On today’s podcast, we are gonna be doing a coaching call where we go over the beginner questions on transitioning. Maybe you’ve owned some rental properties and you may be thinking you’re gonna 10 31 into a syndication or into a bigger deal. Guess what? , as far as I’m concerned, 1031s make absolutely no sense unless you’re going to 10 31, like something bigger than a two or 3 million capital gain and depreciation recapture.

So what we’re gonna be going into in detail today on this call is, how do you use the passive losses or how do you go into deals to get enough passive losses to totally offset the capital gain and depreciate, recapture on everything that you’re selling previously? Just experience sharing here, 2015 when I realized the old turnkey rentals wasn’t all what it was said it was going to be. And yeah, back then the pricing on that stuff was a lot better than it is today. I saw the light and I sold pretty much all my. Turnkey rental rentals in 2015. I think I sold six or seven out of the 11 of ’em that year, and I had a big capital gain in depreciation, recapture about $250,000.

But since I was investing in syndication deals prior, I had a lot of suspended passive losses built up. And I believe the form is the 82 85 form. All you guys should have that. Take a look at there and see how much suspended passive losses you have. Great exercise for you to do every single year. And also I just uploaded in the syndication e-course a video where I go through my K one tracker on how do I keep track of my suspended passive losses in this year, and then go look at my 85 82 form for previous years.

But anyway, Hope you guys enjoy the show. Make sure you sign up for the club at simple passive cash flow.com/club. We just recorded the quarterly kimono report and we’re going to be releasing that to you folks. The part one and part two. Part two goes out to the investors in actual deals. We go over all the deals that we’re in in a very transparent form, right?

There’s a lot of people out there. They say they’re in a lot of deals, but they never really, you never really hear. This stuff, nor can you really interact with other investors within the group to figure out if it’s all true or not. And this is what’s hard about being a private investor in these private syndications.

It’s really hard to do your own due diligence, which is why I have always said the. . The only way to really do this and make sure you don’t step on any landmines, and I’ve stepped on the landmines myself working with, dishonest people and people who just are faking it till they make it.

The only way to really figure out who’s legit in this business is to surround yourself with other purely passive accredited investors. Not these, fake it to you make it general partner wannabe groups, but real accredit investor, purely passive groups. I truly believe that our group is the, really, the only one out there with kind of that already have infrastructure in place.

Our family office group, we’ve started it, I believe around 2018 and really got it going 2019 and into the pandemic. I think we’re well over a hundred members in that group right now. . But if you guys wanna get more information about that, just come in, join the group@simplepastacastle.com slash club.

That form will take you maybe about a minute or two, but then we’ll set up that onboarding call with myself to get to know each other. That gives me the opportunity to see what you’ve got going on and maybe do a little bit call, like how we’re gonna be showing today on today’s podcast. But anyway, enjoy the show.

All right, folks. We’ll probably going to add this to the e-course at some point, but we have, we’ll just call them. Bob, and Amy, if I can remember that name right there, names real names so will remain private. But Bob and Amy have been investing a little bit and have some great questions.

And I think these questions are. Going to be very indicative of somebody. Who’s been through a lot of the initial education. So I’m very excited about this what we’re going to be talking about today. Hey guys let’s get this kicked off, have a good conversation here.

Hopefully other people can learn something.

Where do you want to start? You bring the questions I got I’ll try and break down some ants. Okay we’re in our later career years, put it that way. And we’ve been doing, buy and hold and we’ve been doing deeds and we’ve done some hard money loans and. And we finally got into one of your syndications.

So we were actually getting into that now also. But we’re trying to get out of our nine to five, but it’s never nine to five anymore. It’s more like six to four jobs. And so we’re looking more at investing for. More like replacing that income. Yeah. So in other words, we’re approximately is your guys’ adjusted gross income. And let me pause this.

So yeah, just profile, I move on just real quickly. A lot of it just breaks out the numbers. Where’s your adjusted gross income at today. And what is your net worth approximately? Yeah. Let’s see. What is our adjusted? Gross is like a one 70, like about 170. Okay. Approximate net worth approximate net worth is. What about. To, to something that’s went to probably about what somewhere between two and a half and 3 million. Okay. So from adjusting girls skate com side, just before we move on, you guys are not in the highest tax bracket. You’re not both below this red line of 340,000, like some of the investors, therefore, a lot of the cost segregation bonus appreciation stuff lead doesn’t really pertain to you guys too much unless you guys are selling other assets.

If that’s the case, we can talk about that later on. But but yeah, so I know you’ve got some syndication related questions, so let’s let’s start going down the list. Yeah. So we’re, know your specialty is syndications and so we’re looking for some information possibly on what type of syndication would be best for.

Someone at the stage of retiring and getting out of their normal career job into more just doing investing. Yeah. At this you can syndicate anything, right? You can sit indicate a pizza franchise, a burger, join a real estate. Real estate, you can develop properties. You can. Bye in the hope and pray property, you can do value, add, you can do different degrees of value add, right? So you can syndicate whatever you want. I think the essence of your question is what type of risks for bore profile, or it makes more sense for you guys is the question.

And the way I look at your guys’ profile, two to 3 million can mean different things to different people, right? If you guys want. In your forties or fifties, two to $3 million, isn’t too much money and you still have to grow your net worth. But it sounds very morbid, but if you guys were in the late later stages of life, two to $3 million is perfectly fine and you’re already at end game already. So when approximately were you guys at age wise, which you say We’re not quite 60 yet.

So plenty years ahead. Yeah. So for the most part, you guys still have to grow your network. Cause two to $3 million isn’t much see states, right? That said you’ve got more than most people out there that doesn’t say much. But two to three minutes to take $2 million at 10%. What does that 200 grand of passive income a year at 10% that said you would need to get fests that tire $2 million, right?

10% stuff, which isn’t going to be the case most times. And what it’s going to come down to is I’m sure you guys are familiar with asset allocation picks, right? The essence of your guys’ question is like what kind of reward risk reward profile you’re going for? Are you looking for something that’s 10%, 12%, 13%.

20 to 25% a year. Maybe we start there, right? Like I think for most people you guys probably fit this mode, investing in deals where it’s stabilized from the get go, or it’s at least, if the economy takes a tumble backwards, you at least hold onto the asset. So deals that are more, what I call the chocolate type of deals.

If you saw that other. Article that I wrote the other a few weeks ago. Those are more higher risk, higher return. Doubling, tripling your money in maybe two or three years, you don’t really eat to do that at this point. Maybe if your guys wasn’t like a million to $2 million net worth or less, that would be more lined up your ad.

Put, if you could consistently grow your money yet 10 to 14%. Conservative fee is stack winning. Is that sound okay to you guys? Or do you guys want to be more returns? No, that sounds good because we have been, we had several condos. And self-managing and the return there, all the condos were in Hawaii.

So their return wasn’t that great. It’s only five to 7%, but part of that problem was like, you paid a down, right? Your equity position was large, is what this image is pretty much displaying. A, you should have read, leverage it, got that return equity up higher, but that just happens over.

Yeah we’ve gone through the hilar process and the views that for more, investing, using the equity on the properties, but we’re now, we’re now, going through the process of selling those off and investing in, in, better returns. You guys are still, probably in the simple passive cashflow 2.0 stage strangest thing from the rental properties, which are high risk, high liability, big pain in the butt for Paul cheat returns and going to be more of the passive investor.

And maybe in five years, you’ll be transitioning more to this simple passive cashflow 3.0 side, where at your guys’ age, if you guys were. Three and a half to 5 million. Then I would say you were there and then you could probably just invest some equity type of positions and be totally fine.

But just to get a sense, like personal finance point of view, do you guys have kids or just you guys just us and. Out of the what’d you, your guys, you said your AGI is about 1 50, 1 70. What do you guys save every year? I’m just trying to get a sense of your price burn rate or how much money you guys spend on fun stuff.

Yeah. Expenses wise, like you guys say 50 grand a year or 80 grand a year, or are you guys pretty cheap and able to save a hundred?

We’re pretty cheap. You gotta be when you’re investing as a private money lender. That sucks. I guess you could say. Yeah. So 60, 70 about is that believe me, I’ve seen very many levels of cheapness, so I’m looking it up.

But yeah, I don’t know if we have our, I don’t know if we have it written down anywhere. Yeah, but just gut feeling like every year you save more than 50 or 66.

Is that, what does that says last year?

Oh yeah, probably around. Probably right around. Yeah, right around 50. Let’s say wait. That’s how much we spent. Oh, okay. So we’re saving we’re saving 120 a year. Geez. Wow. You guys are pretty cheap. Isn’t that? The that’s what you got, I’m looking at I’m checking the most of the money you guys make, you guys say is basically you’re telling me over half. Yes. Okay. You guys are just really typical white Nepal sabers.

Oh yeah. Yeah. Okay. And in that case, have you heard me talk about this concept of ed game? Like four to $5 million network? don’t know if I’ve seen any I talk a lot about this and the family office group that we had we talk about this concept of getting ourselves to financial independence and then so that your money can grow and you can pass your wealth off to a couple kids who live like trust fund kids, essentially dwindle away, but long after year old dad so you guys are there in a way.

You’re not two, four or $5 million, but number one, you don’t have kids. Number two, our group is a bunch of pretty like frugal people. You guys are definitely more frugal than the average person. Oh yeah. I don’t know if that’s a compliment or not, but maybe it is in our group, but so th.

When I say most people in our group are making 200, 300 plus a year, they live in California, much more higher expenses. For them I say four or $5 million net worth. But for you guys that might be a tad under there. You may be on the bottom limits of this concept called end game. So for you guys might be to this guy wearing the green shirt.

And you might be in this position to just invest in more conservative type of deals and you don’t need to double your money every three to three years in development deals or riskier deals. So I would say at the most just focus on the vanilla deals where it stabilize cashflow line, or maybe do some private equity.

But the tricky part is. And again, telling you where to be centered around, but it’s up to you to create your portfolio. So you get that on your weighted average, if that makes sense.

Me personally, like I’ve got all, I’ve got a lot of, bit different deals. This is where, in my opinion, where I want to personally be like, I want to invest in more or. Value add type of deals that are a little bit cleaner class B acids. So that’d be centered around where my cursor is, but all of a sudden, a lot of deals are in that, right?

They’re all over here on the outside of that bullseye target, but the weighted averages, there is the point I’m trying to make for you guys, you might want to have in this. Mindset as me like same B class. Like definitely not C class assets. Cause they’re just a headache. Although you’re just passive investors, you don’t have to deal with that, but they’re still from a passive investor perspective.

Cashflow is more sporadic in class C properties because tenants, they just don’t pay with a higher frequency we’ll figure. But maybe you guys might work. I’m more of a here. Maybe we see the same way, right? We want better cleaner assets, 1960 seventies and 1980s, which is right here where my cursor’s moving back and forth.

But maybe we’re, I’m up here and I’m wanting to grow my money at the stage of my life. You guys might be a shy under here, so maybe more what we call a deep field type of deal. Or it could be, you just invest near, but you do some private equity down here and the weighted average is right here.

That makes sense. Yeah. Yeah.

But yeah. Does that kind of solve that and then give you some food for thought or the other oh yeah. Confirmation. Yeah. You guys don’t, you guys aren’t really like this, but like some of my investors they’re like, all right, I need the class to beat less class assets in that are little bit at more than value add or like value add.

And they get very precise with this and just know that nothing will ever just hit your box. You got to expand the strict. And you have to invest, especially if you have lazy dead equity it’s so that B S equity in your home that should be put to work and grew in your rental properties. I know you guys have that there or equity is if you have stocks mutual funds, that type of stuff with bonds.

I don’t know why you’d want to hold bonds at this stage.

That’s the biggest thing, right? I think that’s the biggest problem that most people have is they think that this is their strike zone and they’re very patient looking for what’s there, but they got a million dollars, not think Jack for them, that’s where the low-hanging fruit for them. So that’s where we come up with.

Deployment plan where it’d be put the years up on the top. Then we hear like the four sources of money, for you guys are saving, let’s just say you’re saving $50,000 a year, right? This is what your money is coming through. And maybe you quit in 2025 is what this is saying. And then cash may, you may not have too much cash, but you want to deploy that at some point.

And then the other two sources of capital is your home equity, which you can tap via hilar where you finance or selling the assets. I would suggest with it being polite properties with a, just speak, generally bad rental properties through states where you have bad laws and it’s more an appreciation play, which doesn’t help you at the stage of your guys’ life for qualified retirement plan money, which isn’t your retirement.

Self-directed IRAs, 401ks, et cetera. So you start to build this plan where you draw it out and you’re taking money out, not so that your AGI blows up by taking out the IRA money out prematurely. But you leaking it out slowly as the general idea, but this is the name of game you’ve got to deploy it.

Cause I’ve had investors. Say I’m in a dozen deals, but it’s still a while to being to financial freedom. I don’t like, yeah. A dozen deals at $50,000. It’s just like half a million dollars, half a million dollars deployed. Isn’t going to get you anywhere at this know, especially from a cashflow standpoint, you can do the math on that five, 8% on I went to grant is nothing.

What do you got? We got there. You got questions.

Oh so we’ve got a bit in the self-directed IRAs and the 401ks. We’ve got some money in there and I know you’ve gone over. Starting to pull money out of there, but we’re at the 59 and a half, so we can start pulling money out. Yeah. Let’s kinda talk about this cause like how much money would you say you had in the foam equity out of your let’s just call it $3 million net worth.

How much is like as home equity in your rentals and your primary residence. 625. Okay. And then your retirement funds, how much would you say? I’ve got

three to 400,000. Okay. Perfect. It just like the last guy. And it’s more than one. We’ve got a couple of, yeah, but you’re not working at those companies anymore, so it’s fair game to take them out. One of them yeah, I’ve got an ESOP that I’m still working, so that’s still growing.

Okay. But yeah, the result of you taking money out of your IRA. You’re at art you’re I think you’re at that age where you’re not going to hit get the penalty, which is fine, which isn’t much anyway, 10% who really cares about that. The biggest thing is when you take the money out, your AGI will go up and that may push you into the 22% into the 24.

Or what we don’t want to happen is to go over the 32%. So let’s just say your age has one 50. If you take out a hundred grand, it’ll push you to two 50, which is still cool. It’s no big deal. So 24%, but if he pushed you to take, if you take out an additional hundred, which is 200,000 a year, go from one 50 to three 40.

Now it’s starting to hurt a little bit more. This is subjective, right? Most of our clients are in your guys’ situation of that AGI between one 50 to three 50. So that’s the general thought, of course this is personal finance, right? This is you guys need understand how this works and make the best decision and surround yourself with other like-minded individuals.

I don’t understand that stuff too, to ultimately get the best decision for you guys, but let’s just let’s just let’s just go with this right. And see where it takes us. So if we take out. A hundred. What I say a hundred, say we go 150 in the first year. That’ll take you. You’re still under that three 40 line.

And then maybe you would do 150 or 150, or, maybe you just play it out like this. I would rather see you take the money out of your home equity first quicker, because to me, this is the money not. It’s the boss most, yes, there, basically. If you’ve heard the analogy of the wartime general, the, all these dollars right here, you have, or think of them like sold shoes, you’re trying to fight the war. You got 600 of them right here. These guys aren’t doing jacks. Neither of these guys much, but at least they’re like sharpen and pencils are cleaning their guns.

They’re doing something. We know we got to get them out, doing something, they don’t need to be doing kamikaze runs or shooting on the front lines because you guys are already at end game, like you said, but we got to get them out doing something at least harvesting, passive losses for you, but let’s just not do this out of haste.

Do it too quickly. Where your AGI goes up, but I guess just to throw something out there and I’d like to hear your thoughts on this, what I would do is I would go heavy on the hilar first, and I’m just going to do some kind of cascading numbers here to get to your 600. The reason why I’m leaving this at 1 5100, 100, 100, or I really, maybe it shouldn’t be 1 50, 1 50, 1 50 to get it all out in a few years.

I’m just trying to stay under that three 40 AGI, just so that when you play around with these numbers yourselves, you know why I’m playing it. But then this is to me is the biggest thing here.

Yeah, we try to use our Wheelock for investments. That’s what we do now. We’ve got some hard money loans at 12%. So the hard money loans, I would be very cautious of those number one that is ordinary income. You do not want. And number two, you don’t get past losses, private money, and number three, be very careful who you lend money to because there are a lot of people out there that act as marketers too.

And they run these like lending platforms where they act as a conduit to put your money with lower grade operators. People that really should be charging. You should be getting for the level of their expertise or track record. You really should be getting 15 to 20% return on your money, but the middleman was marketing you, that loan is taking the Delta.

That’s very common. But I think just for the sheer ability of getting passive losses and it being not the board is why you’re trying to get away from the private money. Plus all your money is tied up in one deal too, but yeah as you phase out of that, the idea is you’ve got to sell the rental properties.

Cause most of your stuff is in a vocab area, right?

Yeah. No mainland metals, no. We have a property on the mainland, but, and we Airbnb it. Yeah. That’d be the last set I sell. Yeah, that one’s right. That one’s been handed down in the family. That one won’t be going anywhere. Oh, why you say that? Bush? No attachment. Amy’s dad built it.

They want to sell it.

And I think about it when people start to see you, cause they trip and fall. Maybe you might want to reconsider that one, but Hey, I’m okay with it. We can decide in 20, 26, but it’s working and that’s all I’m happy. What to me is the biggest thing is. For hardworking folks.

Like you guys work hard more, especially you guys saved really hard. What your money’s not working for. You’re working harder than your money. Yup. So let’s go off the low hanging fruit first. So that’s the home equity in the local rentals and the primary residents get a hilar, but at some point you have to make the decision to sell those assets.

Unless you think that there are good investments, which are there in our hall, either not put at best, they’re just right. Yeah. We’ve sold two of the four already. And of course there, 10 31 exchanges oh, we don’t want to do those. Yeah. We don’t do any of those type of stuff.

We. Had somebody help us out. We did some I dunno, outside the box workings with those properties. So you used to own property, so that’s the hard part. And in the next three to five years, you’ll be in the same predicament. Yeah no, we don’t, yes. With the the remaining amount, which is.

What less than half, about half the value of the property was yeah, the we there in DSTs. Oh, no, you did a DST and those DST guys get paid so well with all the fees with that stuff. Unless you’re take kicking a capital gain of over a million or $2 million, those types of things are complete scams.

Should be able to offset those, that tax school gain with passive losses.

We might not be doing, don’t be doing it again, shoot. I did it too. I did a 10 31 back in 2000 and well. 14. I don’t know. I got, been there, done that I made the same mistake. Just don’t make the same mistake again. The analogy I use for the 10 31 or DSCs is it’s like a hot air balloon, right?

The hot air balloon goes up when you buy the property, it starts to go up and you can sell it and take a lot and pay your taxes and jump out of the hotter. And in the beginning, the higher balloon necessarily it’s four feet under. You jump out. Ideally you start to get on the passive investing bandwagon.

You start to get these passive losses piling up through normal depreciation bonus depreciation. You’re going to start to accumulate excess suspended, passive losses so that when your hot air balloon goes up and you jump out, you have a pillow of passive activity losses. So that’s what happened to me back in 2000 and.

17. So that’s down here. I had a $200,000 on Jeanette, $8,000 capital gain depreciated capture, but because I was investing into vacations and private placements, which did a lot of cost segregations, I had several hundred thousand dollars of passive losses and I strategically views 200 of it to offset that gate.

And thus. Allowed me to not to have to do a 10 31 exchange, which again, going back to the higher balloons, it’s like the hotter blade continued. When you go into the next property, you go into this hotter bunny Eagle higher. So the next time when you have this debt equity in the asset and you want to get it out or solely.

Instead of four feet up in the air. Now you’re 20 feet up in there. You jump out of that hot air balloon. You’re going to break a leg at the very least, not even hit your head a die. And that’s essentially what the 10 31 it’s ESTs do they see you’re stuck in a spotter for me, and it makes it harder, harder for you to accumulate for more passive activity losses that we can have you jump out and get to more of a portfolio where it’s all broken up into little pieces at a time.

Then these bigger chunks and that’s what we don’t want. We don’t want our portfolio for any one of our, any one asset to have more than five to 10% of our net worth into one thing. That’s not diversification, you’ve done the T the DST I, the psycho I did the 10 31 exchange. The best thing you can do right now is to start keeping passive losses because you’re in this.

You should’ve got out when it was four feet, you’re eight feet, 10 feet in the air, but there’s still a chance Bob and Amy, you get a much passive losses. You can offset it. Just like how I personally did it right here when I finally got out of that. But it was one of those things. Like you have to get around other high net worth investors and get away from the salesmen selling these DSTs these sub 10 30 ones.

It from a high, from like a marketing perspective, the layer taxes. Yeah. Yeah, that’s right. But they’re just trying to sell their product. And the product is not really the right tool for the job. And in most cases, the situation where a DST 10 31 exchange makes sense is say like a client is selling a dentist franchise that they started for $10,000.

And now they are selling it for three to $4 million. At that point, it’s pretty hard to accumulate that much passive losses. So the option that a lot of high net worth people will do at that point is the DST or monetize stall. So something like that, because it’s just such a huge capital gain depreciation recapture.

But if it’s less than like a quarter million, certainly even less than half a million, sometimes even a million dollars. I’ve seen people get a million dollars plus a passive activity loss. It can’t be done to get you or that hotter, but just food for thought now. Okay. Yeah. But a lot of this is simple.

But the hard thing is that there’s all these kinds of products out there. Like DSTs qualified retirement plans. Is that a lot of my huge fan of everybody just trying to sell you stuff right. I think it for me, I don’t give a shit what you do. Like I just tell you what makes sense to me and what other people I’ve learned from do I don’t care what you do, I just don’t like this.

You spend $4,000 on something that only is really good for the person selling you at and not the best for your situation, but I’m not getting financial advice. Of course. Not at all,

but yeah. Yeah. But I think, like I said, man, like I did the same thing. So welcome to the club. I, after a while you stopped listening to these, get salesmens in suits. All right, what’s next? What’s next? You guys got a good one.

Got a you hit it a little bit tax questions though, but go ahead.

Yeah, Amy’s got some tax questions, but I’m not a CPA or a tax attorney, but try my best their job is really just to do the forms. Yeah. I think you hit on it already with the accumulated passive losses. Yeah. Go look at your I think it’s 80 to 8,500. I think it’s on the taxpayers of opacity, castle.com/tax, but that form will have the breakdown of how much it passed suspended, passive losses you guys have because you guys have been investing for quite a while.

So you should have most cases. People have more than they think they have put it that way, but a little trick of the trade, like CPAs, don’t really, don’t like to give that to you because they want to know when you’re shopping and. So most cases you won’t have that form in your documents. You certainly won’t have all the backend computer calculations.

It’ll just be the PDF printout, which is useless for our planning purposes. It’s useful. If you have the numbers there. To go elsewhere to portable or go to a better CPA. That’s actually good. Which in our world, 95% of my clients, they typically change their CPA.

What do you got there?

As you guys have seen the syndicator or the investment side, right? The three steps of simple passive cashflow first step invest with honest people that aren’t going to steal your money or use money, right? That’s the simple part. But that’s the part that unlocks all this other stuff, which is part two, the taxes.

You can’t really do this unless you have the passive activity losses to start to maybe implement real sick professional status to. So you have to go into the deals, unfortunately, which is I think the hardest part, who do you trust? Because anybody can do deals these days, right? Like not most people, they, if they’re new, if they’re under a half, a million dollars for half a billion dollars, $500 million of assets, and we’re well over a billion dollars at this point in 2022, But trying to find reputable operators that kind of give your money to, to be good stewards with your investment capital.

But then they’re really like, it’s simple, right? From the investment side, what you’re looking for. The biggest, low hanging fruit is the taxes. And then the, like the infinite banking too. We can talk about that also, but those that’s like 1, 2, 3 step. All this other stuff, DSTs cure pure BS, all these other products out there that to me are extraneous and in certain situations it makes sense.

And that’s my job is, based on your guys’ situation, it doesn’t make sense. Like for example, I think a cure appeal only makes sense. If you will have an extremely high income adjusted gross income of over 3 43 50, plus which you guys don’t. So does it make sense to use it? Okay.

So step one, you’re saying, they deal with the honest people. So you’d have to basically you’re building your your team basically. Yeah. But you’ve got to go about it a little bit roundabout way, right? Like eight, I think going on the internet, going through the podcast logs, finding people to work with is the wrong way to do it because you’re just finding the people who are good at.

Yeah, this is where it’s. There’s a kind of my spin on it. You have to find other colleagues and peers and credit investors around you that are already investing in this stuff and build long time relationships. I don’t know if you guys have ever come out to us, we’ll pass a cashflow event, but that’s the stuff you need to be.

You need to come out, break bread with people, build organic real relationships because. That’s where you’re going to find out the goods, who to invest with who to stay away from in the initially. The networking and social capital is really the currency of the wealthy. And like you said, you guys are already there to engage.

It was just it’d be good to find people on the same trajectory as your guys’ selves, this blind. Do you have another meetup in Hawaii? No. I would suggest joining the family office Ana it’s a pay to play program, but it’s hard and while you’re right, there’s barely any people, they only meet up groups or like the free ones, which are a bunch of broke guys trying to flip houses or wholesale houses, or do a bunch of birds.

Which in my opinion, what you do is when your network is under half a billion dollars, but that’s beta play, man. That’s what I mean. I went from 2009 to 2015, trying to do it all myself and I never wanted to pay for anything, but then I hit the wall and until I started to pay for mastermind groups to get around other higher network investors, just look at my unit count, didn’t really tick up. That’s why I started to do that. That’s you can try and do it on your own. But I think in Hawaii, it’s impossible to find other people, this type of stuff is you can’t go to wildlife country club because it’s just a bunch of rich trust fund kids there, or high-paid executives who do things differently with their money, not investing in workforce, boring investments, such as we do.

Okay. But yeah, you guys are investing far. The part of the club just know that the network is not completed.

Network is a separate part, a mastermind group, family office salon, a simple passive castro.com/journey for more details. But I think that’s the next step. If you’re investing more than a quarter million, I think it’s a no brainer at that point.

But yeah. You guys have been progressing pretty nicely, right? That’s good question. That seems like a lot of these concepts it’s it’s hard because it talks about this type of stuff.

Your 401k. Who talks about even private money lending on house flips. And we’re like 10 levels above that at that point. Yeah. When you talk to friends and family and you say, oh yeah, I’m going to syndication. They’re like, you’re in the mop. Yeah. That’s what I said. In 2013, I was like, isn’t that look like on this games?

Come on.

Yeah, but now nowadays, that’s where all my money is scattered amongst other people

still sounds, seems a little crazy to me still though, but I think that’s when you find other people that kinda, this is all the way they invest and you start to realize it is a very small community of. Passive investors. It is a lot more comfortable, but I think the hard part where you guys are at, and you just need to have a handful of close compadres, organic relationships around you, that also are starting with you guys.

And that’s the next step. Yeah. Yeah, any other final question, syndication, personal finance tax legal in front of banking.

This is kinda your, this was your guys. This was your guys slide, have you ever had to try and get a hilar on. LLC owned property, rental business property. It shouldn’t matter. He locks are always difficult to get on non owner, occupied properties, regardless if it’s an LLC or not.

If you’re working with the Hawaii banks, the blade banks are very bureaucratic and logical. And if you think they do, because they have no competition here, so they don’t have to. Do anything that’s outside the little box. So that might be the reason why you’re running into that problem. I would just go to a maintenance thing for that type of stuff.

Better rates or competition there. Yeah. But what is this for? Hawaii rental? Yeah. Yeah, just dude, just sell it. What is the, what is it worth today? We’ve got two different condos yet. One one’s about

2 65, the other one’s about 400, 400.

What is that moment? Is it.

Yeah, dude, it’s less than half a percent method evaluation and you having it backed up the eight. What is the HOA is on that thing?

No, it wasn’t that much. Oh, it’s 600. Yeah. So you’re making like 1500 on a $400,000. You take that money and you buy the equivalent, you could be buying for eight minus units on the main land, each writ running for a thousand bucks. No, but Hey, it’s your life? Just don’t complain when you don’t feel like you’re at financial freedom with your buddies, not for you.

And that’s a clear indicator that you must not working for your $400,000. It’s only $1,500 of revenue when you can get it to the mainland and make $4,000 and you could also be doing value add rental.

Yup. So yeah we’re getting there. Yeah, you’re getting there. And part of this is it’s a slow thing too, right? It takes a couple years to get to the swing of things cause it’s to get it. But I think it sounds like you’re heading the right direction. Like you’re thinking about what’s the next, I got my herd of cattle here, which was just the next set of tickets to the slaughter house and having nearby with, I would say that’s $400,000 or you can look at it two different ways.

First is. Which of those remaining combos are boy rentals is the most pain in the butt for you. I would probably do that. Or then just look at it from a pure numbers perspective and the pure numbers perspective. It’d be like, what trend do I have the most debt equity yet? Like the $400,000 one, or which one has the highest or the lowest loan to value would be the numbers, but looking at it.

Those are the two lens you can look through to figure out what kind of rebel you’re adding to that night. Yeah. Yeah. They probably have Hawaiian dates, right? These continents or these cattle?

No, neither one of them. Yeah.

Or they say never be here, farmer that’s right. If you want to eat them or one of the condos we actually bought in the foreclosure. Yeah. Then you should have said she should sell it. Cause you have some good equity and it was just like, people ask us like What do you guys sell these prop?

What are your exit early? If we, hit our business plan, we get hit, more than 20% a year. We can exit early. We’re going to do that because some of the property, like you guys in terrible jokes, maybe you guys are in that, but like Terra Oaks, we picked up a bat, a pretty good price.

That’s why I’m earmarking that with, to exit. Like the same situation, you guys picked up that foreclosure at a good price for us. Like we were still going to the value add process. And then when that callous factored up or take it right.

What’s up folks? I’ve been getting a lot of questions on land conservation easements after the omnibus bill seem to break the conservation easements at a two oh and a half x multiple. Is it true? Are there loopholes? We’re gonna be going through both sides of the argument here so that I kind of stay in the middle and kind of say that I just gave you all the information that I tapped from my sources.

Ultimately, you gotta make. Station, but here we go.

Hi, my name is Lane Koka. I run the Who We Do Pipeline Club. If you guys would look on to join and get involved in our deals, go to sy paso castle.com/club. Um, if you haven’t heard what a land conservation easement is, You know, you’ve probably been living under a bus or some rock or something like that, and you’re probably not an a credit investor.

If you’re not an a credit investor, don’t listen to this video. It’s just, uh, not gonna help you out very much. What this is for high income earners that are making over three to $400,000 adjusted gross income every single. So a bunch of higher roller cokes. This is something that the IRS has on their kind of watch list.

Nothing that I’m talking about is going to be construed as tax legal advice, blah, blah, blah, blah, blah, blah. This is kind of the latest and greatest of what’s been happening. What I’ve been hearing from my insiders on this issue that is all kind of stemming from in December of 2022, this omnibus bill kind of came forth and changed a lot of the tax governments and how this stuff was gonna be viewed by the IRS from the 2016 latest.

But so we don’t lose anybody here. What is a land conservation easement? But basically it is sort of like a donation, right? Where donations, if you guys aren’t familiar, you donate something and you get a tax deduction on your taxes. Real simple. But in this case, what people are doing is they’re going into syndicated land conservation easement deals where a piece of land is syn.

And that piece of land is donated to be put on a conservation easement list where there will not be any type of development. Basically, the land goes to the ducks and the wolves, basically. Nobody else can build on it. It is kind of for the sake of the environment, and this is kind of a good thing in the long run if you’re kind of one of those green people.

But the main thing we’re talking about here is the tax side. What people are doing, or what they were doing is they’ve got a million dollar piece. But they’re getting it reevaluated for a higher and better use. Maybe that land can be redeveloped to put solar panel cells or put a big high rise casino on.

Of course, that wouldn’t be very practical, right? So there’s a level of how practical the ski land can be developed. Some cases it could be developed, you know, 20 x 30 x and that was what people were doing at one time. If you’re kind of following me, What they were doing was buying a piece of land, you know, for a million dollars and saying that it’s worth 20 million in their deduction.

Now, sort of along the years, certainly around 2016 to 2020, these kind of ratios came back and kind of got rained back to earth and the five x multiple put in a million dollar property and you get it reevaluated. 5 million. To get the deduction for the people in these deals still can provide a net positive for a lot of.

Take somebody making a million dollars a year, if they’re able to drive their income down to 50% of that to $500,000, they just shelter that $500,000 from that highest tax bracket, and especially if they live, you know, in state taxes too. And that could mean that their AGI goes from a million down to half a million, but more importantly, they save 50 cents on every dollar on that delta.

So that means that they just saved a quarter million dollars in taxes right there for putting in an investment of maybe a hundred thousand dollars. Again, that five x multiple a hundred thousand dollars infusion of. To get a $500,000 deduction in their adjusted gross income, and that equates set 50 cents on the dollar, a $250,000 gain back, so pretty dang good investment, right?

Something that kind of takes overnight in a way less a hundred thousand dollars and get two 50 back, right? That’s more than double your money. Now, what was been happening in years prior to 2023? Is that these ratios were being pulled back to a five x with the omnibus. There is a little bit more of a ruling system around the governments of this multiple, and that multiple now is two and a half x.

Now, using that same example, right, A guy, you know, using one of these syndicated land conservation easements, they’re adjusted gross. Is a million dollars. But instead of that, that five x multiple, now they’re only kept at two and a half X. So they’ve gotta spend, say, a hundred thousand dollars to get $250,000 of AGI differential.

So that means with a hundred thousand dollars, they can lower their just gross income from a million dollars. Down to $750,000. Still a big amount, but is it worth it? That delta of $250,000 may only mean a, you know, tax savings of $125,000 at 50 cents on the dollar there. Remember, they spent a hundred thousand dollars.

In this investment. So that means they’re only gonna get back $125,000 a delta of $25,000 to the positive. With that, it kind of negates the whole purpose of doing this whole thing unless they’re doing it for the benefit of the ducks and the air and the rivers and you know, all the Pocahontas environment type of stuff.

But is it worth it? Right. And this is kind of what the Omnibus Bill has kind of put. Now I’m gonna be going kind of through my notes here of what I’ve been kind of collecting from my sources that wish to remain anonymous, and that’s kind of the world that we live in this stuff, because a lot of this is not to be considered as tax or legal advice.

If you’re somebody who wants to do this type of stuff, well make sure you work with the right people. This is why people join our mastermind group, our inner circle, and join our club, right to learn about things just like this and deals and you know, where do you invest. Again, you guys can join that at simple passive cash flow.com/club.

A lot of this is based on your personal financial situation. This may not be for you, but certainly if you’re making over, you know, a few hundred, 400, $500,000 adjusted girls income. Probably is something you should learn more about. I’m gonna be going into a little bit more of these details from my notes.

So in years prior, you could kind of be in a deal and as long as you’re in the deal for one year, you could kind of make that election, or the syndication could make that election to make this donation. But now with the omnibus, now they’re saying you need to be in it for three years. Now I don’t know where this magical three year comes from, right?

A lot of these bills and government, you know, regulations don’t make any. The closest thing I can subject that where it comes from is maybe they’re trying to emulate long-term passive income, which, you know, my CPA tells me to hold onto an asset more than a couple years to get at better capital gains treatment. But it is what it is. Three years is what it says.

Another nuance is in years prior, you know, when people were going five x 24 x, 15 x under multipliers, there was some wiggle room. Now what they’re saying is if you go any higher than 2.5, you essentially brick your entire deal. You know, in years prior, you would’ve gone up to maybe 2.4, 2.5.

Anything higher than that would’ve just been, eh, yeah. You know, you’re not gonna be able to count that. But now they’re saying if you’re going higher, It’ll get all disallowed and thrown out Again, these are just, you know my notes, right? Not saying that what will happen if you get audited and what will really happen in the enforcement.

These are just kind of ideas that have been thrown around that I just want to kind of put into your guys’ head. For some of you folks who did conservation easements in years prior, maybe in 2022, and you’re probably freaking out, you’re probably like, oh my goodness, my conservation easement is gonna get thrown out because it’s higher than 2.5.

Here’s the deal from what I’m hearing, as long as your deal was first off, voted for, it was filed into the law in that jurisdiction and everything was kind of wrapped up in a bull before the omnibus came. Through in December of 2022. You should be fine in terms of being kind of grandfathered under the old regime.

Now, of course, you know, nobody wants to do this and I don’t really, I don’t condone any of this, right. But there’s a probably gonna be a lot of people out there who are doing this stuff, who made back date documents, forge documents to get it in before the conception of the omnibus bill in December, 2022.

I’m not, I’m not condoning any of that again, right? That’s not good. But I, again, I think I’m saying that because we talk a lot about entities, legal protection. When people wanna sue you for frivolous reasons, that’s the kind of garbage they’re going to do and pull on you. And this is why having, you know, if you’re a higher net worth individual, just having some LLCs probably isn’t gonna help you too much in terms of protection.

And this is why, you know, the wealthy people go through great extremes to totally eliminate liability or more protect themselves to a certain higher. Because there are a lot of unscrupulous people who do stuff like this, and it’s very easy kind of to fudge a date here and there. All somebody has to do is the CPA Turner who’s gonna be doing stuff like this.

Hey, gimme an extra X amount of dollars, it’s a consulting fee, and I’ll make this work for you. Scribble some dates back here that are completely illegal. I hear about it now. The omnibus bill is pretty rock solid in terms of saying, Hey, 2.5 x multiple, no more. There are some hopes here. Now the new commissioner is coming in and we don’t know how that person is going to be.

Are they going to audit this stuff? Well, we know that the old commissioner would audit everything from 2016 and beyond, so we know that for a fact. But what to what? Right. So one of the due diligence things when you do look at these types of deals was to go into a deal that had a healthy legal budget.

Why? Because if you had a healthy legal budget, maybe seven figures, to keep a battle going, at some point it may not be worth the effort for the iris to fight you, and it will just lead to a. These things are always settled. It just really never gets to the end, like law and Order where there’s a judge that says this or that, it typically gets settled just like any other litigation.

This one’s no different just with tax court. So if you’re able to fight it and be a pester, the theory is that you can, you may be able to get a better multiple or just ski through the system on escape. That is if they audited you, which if you work off years prior, you probably. But I think this is the biggest thing that people who are still doing this conservation easements are kind of looking towards as they’re kind of saving grace of, well, you know, at least I got the tax savings in the meantime.

And if I grew my money, if I double my money in the last two to three years anyway, or maybe even five or six years, by the time this work its way through the audit system as I would imagine something like this would just taking forever. You know, you’ve gotten that time benefit of money. Now, maybe the counterpoint to that is they, maybe they would backdate the penalties and.

And this and that. But if you’re able to grow your money, maybe you’re able to beat that taxes and, and, and penalties. Just another thought. Now we’ve kind of beat up this conservation easement. At this point, I would probably think at home that, yeah, I’m not gonna do this stuff. Now the other side of the coin is, here we go.

And again, no tax legal information on my part. I’m just telling you what people on the streets are talking about, that I kind of interact. So first off, we kind of mentioned it, right? Let’s just say the evaluation is two and a half or five x is what it used to be. There’s a certain amount that your evaluation can go down to that you still get a net positive benefit to.

That’s up to your personal situation, and I think that’s something that I can kind of help out in helping you determine if it makes sense for you or maybe there’s just some other mechanism, maybe real estate, professional status and passive activity. Losses are just a better way of going than this.

Little bit more risky. We’ve got the Tax Pal fund. I’ll get more into that at the end of this video as a more safer option, in my opinion, to get passive losses that are not recaptured. But you know, this is the counterpoint, right? This is kind of the devil’s advocate approach. One thing that I think people have to realize is why do you have this whole conservation easement thing in the first place?

Well, the purpose of it is to designate land that you cannot develop it for the sake of the environment. And whether you kind of believe. Yes or not, kind of do need it, and the government wants a certain degree of this right now. This is just a tug of war game. The omnibus bill has pushed things very in favor of just killing all these conservation easements.

The good ones, the ones that want to go through are not because of this is kind of killing the deal. The only people who are able to do this are big, big players not to doing it in the syndication space or so they. And these are kind of the loopholes. They’re kind of being evaluated by a lot of people right now.

If this year kind of passes by and maybe 2023 passes by and there’s not that much land being designated conservation easement, they may look to ease back on some of these regulations. Or what I kind of feel like is they put these types of loopholes in here. So as a means to allow for future land conservation easements, it’s actually to fulfill it Our.

But they kind of have the ability to award it specifically, or for people who have the legal team to fight it through. That loophole that I’m kind of getting at is right now there are regular conservation easements and these simple conservation easements. Regular conservation easements, the rights are kind of given up.

Land is not really donated, and those are more the traditional conservation easements that I think a lot of us are used to. You are able to, in the syndicated deals, you can use the benefits up to 50% of your adjusted gross income. If your adjusted gross income was $1 million a year, you could buy up all these conservation easement.

Maybe only at a two x two and a half X multiple. Nowadays, we don’t know yet, but you can drive it down to 50%. The other method is this fee simple, which may not be under the omnibus jurisdiction, and I’ll explain why later, but what they’re saying is you can possibly still use these fees, simple type of arrangements where the land is completely given up.

It’s not just the rights. Be simple, just donated and given away. The downside to this is instead of a 50% ability to lawyer h ei, you pony unlimited to 30%, which may be good enough. And what I would probably recommend most people to do is see your tax mitigation strategy, not as just a one trick pony with conservation easements, for example, but to use a conjunction of different mitigation.

And this kind of actually forces you to do that because at 30% maximize use of this, what’s happening is say, take that guy who has a million dollars adjusted gross Inca. 30% of it means that he’s only able to go from $1 million to $700,000 ei. And if you’ve seen our tax videos in the past, I always try to get people around $340,000 married, filed jointly, or maybe even around $200,000.

So obviously if this guy’s at $700,000 right now, there’s a lot of room of improvement here. Maybe they implement real estate professional status, or they have a lot of passive income and they use the passive losses, which again we’ll talk about here at the end of the video. But they use those passive losses that drop them from 700 back to 300 or 400 wherever they really want to follow that particular year using conservation easements.

But again, this be simple conserv. When I started to first hear this, I was like, I thought the omnibus bill was calling out all conservation, syndicated conservation easements as a whole, and to me this was a head scratcher. I personally don’t do the conservation easements, but I know a lot of my clients use them every single year.

Which is why it’s important to get around other people actually doing this type of stuff, because if you google this stuff on your own, you’re gonna find all the content marketers who are posing as CPAs that wanna put out a puff piece like this to make them seem really conservative. So most people will go to them, but there are a lot of aggressive folks out there that are investing in the right things that the IRS wants, that wants to mitigate their taxes as much as legally possible, who are looking for the.

So where’s this like little crevice that lawyers can kind of get in here and break up the whole omnibus thing? Well, it seems kind of strange and stupid. I kind of think it’s a little stupid, but the way it was written into omnibus, it doesn’t specifically call out the whole nuance between free, simple, and regular easements.

So again, where does this lead into? Well, it leads into, well, when the conservation easement deal is being audit. It will eventually go into this audit, and this is where we pay lawyers to do this stuff. And if anybody has done silly things for some legal reason, this is the reason why we have lawyers, and thus conservation easements may not be dead.

But in my opinion, at the very least, you can’t use that 50%. You had to go with the fee simple and do the 30% is what I’m. And maybe that two and a half multiple lies. Again, I don’t know, I just personally think it’s just better to use passive activity losses to lawyer your passive income completely and to dwindle your ordinary income amount over time.

To do this, you’re gonna need to get rid of your traditional investments and get into alternative investments that give you passive activity losses, and to do this a very old fashioned and clean way without having to use conservation. To me, conservation events are kind of like a wonder drug, whereas using passive activity losses offset passive income to cancel that out, or maybe to use a conjunction into real estate professional status to use your passive losses to lawyer AGI at that point.

That’s very basic stuff, and that’s kind of like good diet and exercise in a way, instead of just using the magic wonder. But however you guys wanna do it, and I think this is really gets into your own personal situation and your own risk tolerance you have with this type of stuff. I’ve been very clear, I’m not getting tax or legal advice, but I think this is where you need to have a group of community around you.

And that’s why we always, you know, have these events where people get to see each other face to face and talk about things like this instead of just Googling stuff amongst. Now I’ve mentioned, you know, how do you get these passive activity loss, which I feel is like, is a lot better way of mitigating tax.

Good old fashioned passive activity, losses, depreciation to knock out your passive income. If you’re somebody who has moved off of your W2 job, your business, your ordinary income, now all your income is passive income and therefore you could drive your income down to none. That’s kind of like how I live personally.

I pretty much just have passive income these days, and I’m able to use the massive amount of losses I get from real estate to knock it out, and therefore my adjusted gross income is pretty much nothing. No. Completely legal. So what we have is our taxal fund where what we’re offering investors in addition to a little bit of returns, is you are going to be putting in a dollar to get $1 of passive activity losses.

Now normally with passive activity losses, when the deal is exited or the asset is sold, you have to recapture those losses, which can be a bit of a drag. But we’ve talked about other strategies to mitigate it in other videos. But in this actual opportunity that we have, the passive activity losses will not be recaptured.

In fact, if the asset is ever sold me as the general partner will be, recapturing it on my side, shielding that recapture from you. So this is kind of a game changer. So way you use this is maybe your, you’ve got half a million dollars of passive income and you wanna bring that down to 300. So you need a couple hundred thousand dollars of passive activity losses.

You go look at your 85, 82 form, you, you don’t have it there. Or maybe you only have a hundred thousand. Well, you may need to buy some, and the tax power fund that we have will provide that. We have a lot more information for folks that are in our investor club, if you wanna check that out. Simple paso castle.com/club.

But I think it actually makes this kind of arrangement a lot. More desirable, especially when you combine the fact that bonus depreciation is not a hundred percent anymore as it was in 2022. In 2023, it’s down to 80% and in 2024, it’ll go down another 20% down to 60% until it con completely phases it out, and there’s nothing out there that gives you passive losses that you do not have to recapture.

This is the only thing I’ve heard. So it’s a tool and it may be a tool for your situation. What I would say is join the investor club, so paso casual.com/club. Check out the webinar we have, it’s about an hour and a half. It’s a little technical, but if you are into saving taxes, and you certainly should, if you make over half a million dollars a year, taxes is probably your number one expense.

And with conservation easements through this omnibus bill getting tougher and tougher. Sure. There may be some hope. As I alluded to in this video, it just seems like it’s getting harder and harder. Right? Just like infinite banking or credit investor banking. You know, the terms are just kind of getting worse over, slowly over the time horizon.

But the big thing is the best time they get it was yesterday before they make it even worse. Right? Same thing. But anyway, let’s end of the video folks. Thanks for listening. If you guys have any other questions or specific questions about this, put into the common box below, we’re gonna be releasing other videos that you guys ask us to do. Our email is team@schoolpassivecashflow.com. Share this with a friend. Thanks.

What is up investors? Now on today’s podcast, we’re gonna be doing another doctor coaching call, like how we did a couple of weeks ago. But if you haven’t checked out, I think it was Brian on that coaching call, sometimes we change the names , and then that, I think that goes for if anybody wants to do these, Free coaching calls where we go into your personal financial sheet.

We’ll send you the blank personal financial sheet to fill out so that it helps expedite things and people on feedback. Do people really like to look at people’s personal financial sheet as financial voyeurs is the term. If you guys are listening to this on the podcast form, go on the YouTube channel to find this podcast, if you really want to follow along on the personal financial sheet and see all their numbers and a lot that we don’t talk about, I had a lot of questions and feedback over my analogy that I had a couple of podcasts ago, I believe, and then go back to Brian’s one for the full discussion. But this whole concept of, you know what, all right, we’re investing in deals. We are playing these different tax strategies, or at least learning it, maybe doing, getting some passive losses artificially that you don’t have to recapture through the new Taxal fund and you’re doing a little bit infinite banking or a new accredited.

or a new accredited investor banking, which you guys will probably learn as we rolled that out this year. Let me know if you want to try it out, but, it’s working, but alright, people are moving down this path and I think everybody here pretty much, they’re not trust fund kids.

They made their own money and they’re still working. working hard in their jobs or as 10 99. So their small businesses and what is the path forward and how do they keep working? Do they titrate down? Do they work, do they spouse work? How do you implement rep status? And I introduced this Raptor, Toyota or Ford Raptor gas guzzler versus the Tesla model versus the in the middle hybrid.

Prius model of kind of different paths to doing this. Of course, all this is personal finance and what I really urge you guys to do is sign up for the club if you haven’t, and even if you are scared, book that call with me. I won’t rip your head off. I’m really nice when you get to know me. , we get on one-on-one and you.

Let’s go through this and let’s see which one of these paths really fits well for your family and or at least give you some what the options are. And let’s try and. Compressed time cycles for you because time is really the most important thing out there. But if I’m not gonna go into what the heck this analogy was, but what I’m gonna say is go back to the previous podcast that we did coaching call with Brian.

He was also a doctor. I go over this loosely, if not shoot us email, maybe we’ll do more. But certainly if you’re on the YouTube channel, put a comment below. We’ll answer, this is, this kind of, it’s real quality of life questions and personal finance questions, and this is ultimately what I really like because this changes lives.

Like going into a deal, doubling your money, whatever. That’s cool. Tax savings. Yeah. That’s amazing. When, a lot of the doctors will save 150, $200,000 in their first year by doing some of this stuff, and you. , of course. That’s, if you guys heard my kind of confession last week, sometimes when you have a lot of money, that may not mean too much, but you know when your net worth is under a million, a couple million dollars.

This is. Big life changing moments and maybe can be the difference between you having a second child or third chat, or even kids at all, or even, going down a different path in life, whatever you choose. But again, go check out that order podcast and if you have any questions let me know. Or if we ha you haven’t burned up your free intro call with me.

I urge you guys to do. Let’s get you guys going or at least get you a different viewpoint in so you don’t just screw around for the next 30, 40 years of your life, putting your money blindly into the stuff that they want you to do and enjoy the coaching call.

Hey folks, we have another hard work in a professional. Who’s going to be a volunteer to do a coaching call here. So Derek is a doctor. And if you guys like, like you guys are really liked this, I don’t know why people get like financial warism when they appear in on these things. But the truth is not many.

There’s not too many different profiles. And if you’ve gone to the YouTube channel and look for the coaching call playlist, or got an access to our members portal, which is free, you just got to sign up@simplepassivecashflow.com slash club. We actually align all the coaching calls based on networks.

So you can just find yourself and fit right in and find some of the past coaching calls people in the lower net worth than you. And some of the higher ones that you’ll get to at some point, but Dick in here, there. Thanks for doing this. Why don’t you quickly go over a little backstory to get the people that get to know you like.

Sure. Yeah. Thanks for having me. I’m excited to do this coaching call. As far as my background, so typical working or professional kind of investment background. I met my wife in medical school. We were both physicians and busy with training and residency and all that. So we just went down the typical route of basically doing retirement accounts and funneling all our money into stocks and bonds.

We thought were pretty smart cause we were doing mostly low fee index funds. So we weren’t picking individual stocks. We were doing a lot of just basically Vanguard mutual funds. And we’re doing that for basically 10 to 15 years. Cause we had two children along the way. And then just recently, actually earlier this year brother-in-law got me turned back onto real estate.

So went down a really deep dive into the podcast world and bigger pockets on your podcast. And really just started to look into this indication space and rental property space. And this year we actually purchased two rental properties. So one that’s for a longterm property where we actually have some in-laws staying in it.

So it’s not like a typical rental property, I would say. And then a second was a short-term rental property that we got in the mountain area in North Carolina. So we did all that this year. And then now I’m at the space where I really want to start more looking at passive, truly passive, so syndication type deals and maybe even starting to look into like infinite banking.

So basically just trying to get more sophisticated away from just mutual funds, stocks and bonds actually start. Getting some more investments into real estate. And then where are you guys at? Age-wise you guys got kids? So I am 40. Unfortunately the other complicating factor of my personal history is my spouse passed away suddenly like a few months ago, which complicated the issue.

So it’s just me now as a single father with two kids who are six and nine that has also led to this push very recently to really try to simplify my life and simplify my investment strategy. Obviously I want it to be high yield and useful, but I just really want simple. Sorry to hear that.

I know it’s something that all of us as we’re trying to get our stuff together, we never know what’s going to happen. It could be you, it could be them. I was kinda thinking the other day, if it was me. What’s the point. If I’ve gone, it’s all done the simulation ends, but that’s not a good way of looking at it, but yeah.

That’s definitely gets you on the right path or at least tell you what I think. And great. But but right now you’re still working, right? Yep. I work full time W2. I know I’ve listened to a bunch of podcasts, yours included where there’s talk about like real estate status, professional, all of that.

I am not going to qualify for that. And that’s probably years out because the place I work at is actually pretty cool place. It’s a fun startup and I’m definitely, I think, going to continue it at least for the next few years. So I don’t really have any, that’s not in the immediate future to shut off my W2, if that makes sense.

So just a quick snapshot for people listening on the podcast. We also do this via screen share on the YouTube channel. So if you guys want to flip through some of the personal finance sheets as we go through, I’ll pop on over there later the net worth about two and a half. But what I wanted to dig in on, so assets first, right?

You S you mentioned a lot of it is just traditional stocks, bonds, mutual funds, et cetera. So at what I’m seeing is about 800 grand in that stock bonds mutual funds stuff. And then you’ve got a lot of equity in the rental and the primary residence that you guys live in that equity might be wrong. I might have filled out the sheet wrong.

So the equity is probably in the primary residence, I would say between three to 400, depending on what it’s going to sell for in the market. Okay. Know, you didn’t, you did it right. You did it right. You have the this is what it’s worth now that the Delta is, this is the mortgage on it. So I think you got it, right?

Yeah. So it’s three to 400 probably in my primary. And then the two rentals were just purchased within the last, six to eight months, the equity. And that’s definitely not quite as high, although the market is probably somewhere between 50 to 75,000 for each of those. Okay. So we will we’ll circle back around them.

Like we’re going to invest what money we’re going to use first in one particular order, which is always a very common question that comes up, but let’s figure out what your philosophy at this point. So what is your kind of your adjusted gross income? What do you guess it’s going to be this next year?

So right now, my wage is 265,000 per year. For that comes to after taxes. It used to be, my, with my spouse working as well as closer to half a million, but that’s obviously going to keep and then your expenses, right? Not cheap having a couple of kids, but luckily. The wonderful state of California, a little bit cheaper where you’re at, right? Yeah. North Carolina is not too bad. Although the area man is a little bit more expensive than the typical North Carolina, but it’s definitely, yeah. I lived in the bay area before, too. It’s not like San Francisco, other California areas. Yeah. Did you move over to the Carolinas for work or kind of her family?

So I was in the, I used to be in the military, so we were in California, then Colorado, which I actually really loved, but a lot of my wife’s family is from the Northeast area, so we just wanted to get closer to them, but didn’t want to go to an expensive New York or Massachusetts area. So that’s how we ended up in North Korea.

Okay. So what would you say you guys, monthly burn rate for expenses? You use it utilizing daycare or, yeah there’s afterschool, so our kids are in school, but we have to put them in after afterschool or after care. My wife has some car payments. Cause she got a new car. A couple of years ago.

We have our mortgage taxes, groceries, all that stuff. It’s probably around 10,000 give or take 10 to 12,000, depending on the months I used to track the budget a lot more closely. And then that kind of went away the last year or so, but that’s probably about it and that’s including like our, we would set aside money to go on nice vacations and stuff like that.

We lump that in. So probably 12,000 a month would be Yeah. And I think, this is 12,000 burn rate every month. And so you net about 10. So you’re spending at least a hundred grand a year. Maybe that’d be a couple of investments every year. As long as you for you guys, as long as you can stay above 50, 75,000, I think you’re good enough.

You can let off the gas a little bit, whereas some of the folks that are under 1000001.5 million they might want to tighten the belt a little bit. Going at a pretty decent clip here. It’s just a matter of being smart to work with putting the money. I think that’s my next big step is just being smart with deploying all the capital out for sure.

Yeah. I’m not a big personal finance guy anymore, saving the coupons, that type of nonsense. But you guys are doing pretty well. I’ve talked to some people in California where they make more than you yet. They’re barely able to save 30 to $50,000 and I’m like, dude, what’s going on.

It’s typically private school for kids is what flips that up or extremely big outs. But I think, your house is pretty big for North Carolina. You got the salary to support it and that’s actually something I’ve already been in the process of looking at, I put an offer in, on a townhouse that would be smaller to downsize.