Dear investor,

I had my head down in a couple of deals and especially during the HUI3 weekend (mastermind in Hawaii) which turned out to be amazing!!!

When I realized it the month of February was over and we were in the midst of the quickest 10% downward correction in the stock market ever. Supposedly due to the Coronavirus. I say supposedly because you can never really tell what is the reason for movements in stocks but this time it seems like it has really gotten people up in arms.

Video format of this Month’s investor letter:

- What is the Next Step in Asset Protection After LLCs

- Top Things Ignorant Investors Do

- Top Markets to Invest in 2020

- Stop Listening to Real Estate Gurus

- Mental Mistakes of Investors w Marco Santarelli

- How the Rich Use Land Conservation Easements for Tax Deductions

- What Interest Rate to Expect from Investing in Private Money Lending

- Don’t Invest in Short Term Rentals Until You Understand This

- Best Marketing Platform for Short Term Rentals

- How to Position Your Short-Term Rental

- How Much Money You Should Have to Do Private Money Lending

- How Politics and Rent Control Affect Where You Should Invest

- Big Changes to Your Retirement Account in 2020

- How the Secure Act Screwed over millions?

- Do I Need Asset Protection on my Retirement Accounts?

- Is it Safe to Transfer Money to Overseas Trusts?

- It took stocks only six days to fall into correction, the fastest drop in history – CNBC – “The S&P 500′s swift drop marked the quickest 10% decline from an all-time high in the index’s history. The speed of the decline over the past week even beats the Black Monday plunge in October 1987“

- Why the Coronavirus inverted the Yield Curve – Pensford – My initial thought was that the market is overreacting to the coronavirus news. “Classic flight-to-safety-knee-jerk-overreaction, rates will rebound if we can get a grip on containment.But the traders I spoke with were legitimately concerned about the long-lasting effect. Sure, the 35bps drop in the last few weeks was re-positioning to avoid getting steamrolled in the event the news got much worse.But longer term, the virus has the potential to pull the global economy into a recession.”

- Specialty Grocer Earth Fare to Close All Stores and Liquidate Inventory, Files for Chapter 11 Bankruptcy – REBusiness – “Most of Earth Fare’s locations are near a Whole Foods, Trader Joe’s, Sprouts and/or a Fresh Market,” says Beitz, whose firm operates an online platform called Planned Grocery. The app maps the real estate locations of all grocery stores in the planning, development and operating phases.

- Industrial Outlook for 2020-2021 Remains Strong – CPE – “Dallas is in growth mode due to many factors, such as strong population growth, a friendly business environment, low operating cost compared to other gateway markets and limited regional competitors,” local industrial broker Nathan Orbin, Cushman & Wakefield executive managing director. Net Lease

- Investors Still Value Dollar Stores – CPE – “Dollar General has announced 1,000 new stores in 2020, while Dollar Tree continues to focus on renovating hundreds of Family Dollar stores and growing in strategic markets.Currently, the average cap rate for dollar stores with 10 or more years of lease term remaining, that have been on the market 90 days or less is 6.16 percent. Logically, many of these current offerings are newly built stores, as they offer the majority of longer lease terms.”

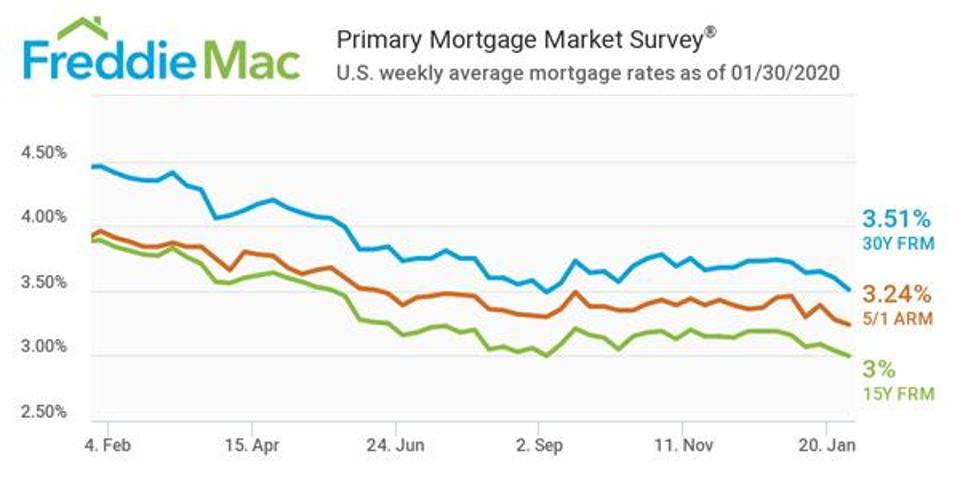

- Mortgage Rates Near 3-Year Low – Forbes – decrease was largely due to investor uncertainty surrounding the coronavirus, as well as trade-related and geopolitical concerns.

- Cleveland Multifamily Report – Winter 2020 – Boosted by the ongoing revival of the city core, the metro’s rental market wrapped up 2019 on a positive note. – CPE – “Most of the new development targets downtown Cleveland; the area ranks as the largest jobs hub in Ohio and is expected to see a population”

- Sherwin-Williams to Develop World Headquarters, R&D Center in Metro Cleveland for $600M – RE Business – The transition to the new facilities won’t occur until 2023 at the earliest, the company says. Sherwin-Williams previously launched a nationwide search for its new headquarters location before deciding to stay in Ohio, where it has been based since it was founded in 1866.

- MBA Forecasts U.S. Economy to Slow in 2020 as Job Market Weakens – RE Business – His forecast calls for U.S. GDP growth of 1.2 percent in 2020, down from 2.2 percent in 2019, and for job growth to dip from a monthly average of 175,000 last year to 150,000 this year. The unemployment rate, which currently stands at 3.6 percent and is near a 50-year low, is expected to reach 3.9 percent by year’s end.

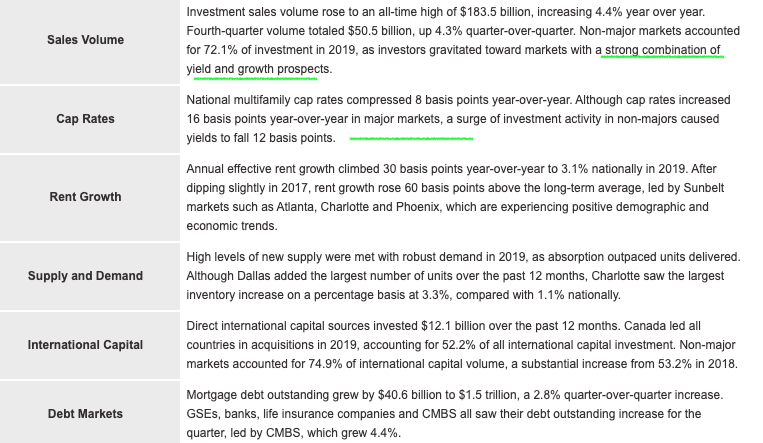

- Newmark Knight Frank MFH Capital Market Report 4Q19 –

- Arbor – Q4 2019 Small Multifamily Investment Trends Report

- Trump’s 2021 budget proposal – Cut $5.6 billion from Department of Education funding—that’s a 7.8% decrease with changes to the ways we take out and pay back loans for higher education expenses. Positives:Eliminating subsidized Stafford Loans, which don’t accrue interest while you’re enrolled, Eliminating the Supplemental Educational Opportunity Grant, which typically goes to independent students or those whose families make less than $30,000 per year, Cutting $630 million of funding to the Federal Work Study Program, Reducing income-driven loan repayment programs to one option. Instead of paying 10% of your income, you’d pay 12.5%. Payment plans would last 15 years instead of 20, with the remainder forgiven, but graduate students would have to make payments for 30 years under income-driven repayment, Eliminating the Public Service Loan Forgiveness program. Positives: Reinstating federal Pell Grant eligibility for short-term education programs and for some currently incarcerated students who are being released within five years, Increasing career and technical education funding by $900 million, Putting caps on graduate and parent loans with annual and lifetime limits. Parent PLUS loans for undergrads would be limited to $26,500. Graduate students would be capped at $50,000 annually and $100,000 total.

- The U.S. is experiencing its longest economic expansion on record, besting the period from 1991 to 2001. (CNBC

- The decade-long U.S. economic expansion has generated 20 million jobs. (New York Times

- 3.4% year-over-year wage growth is the strongest in more than a decade. (MarketWatch

- January 2020 had record job growth in the private sector: 291,000 new jobs, the largest monthly gain since March 2015. (Yahoo Finance

- The U.S. hit the lowest unemployment rate in 50 years in 2019. (Whitehouse.gov

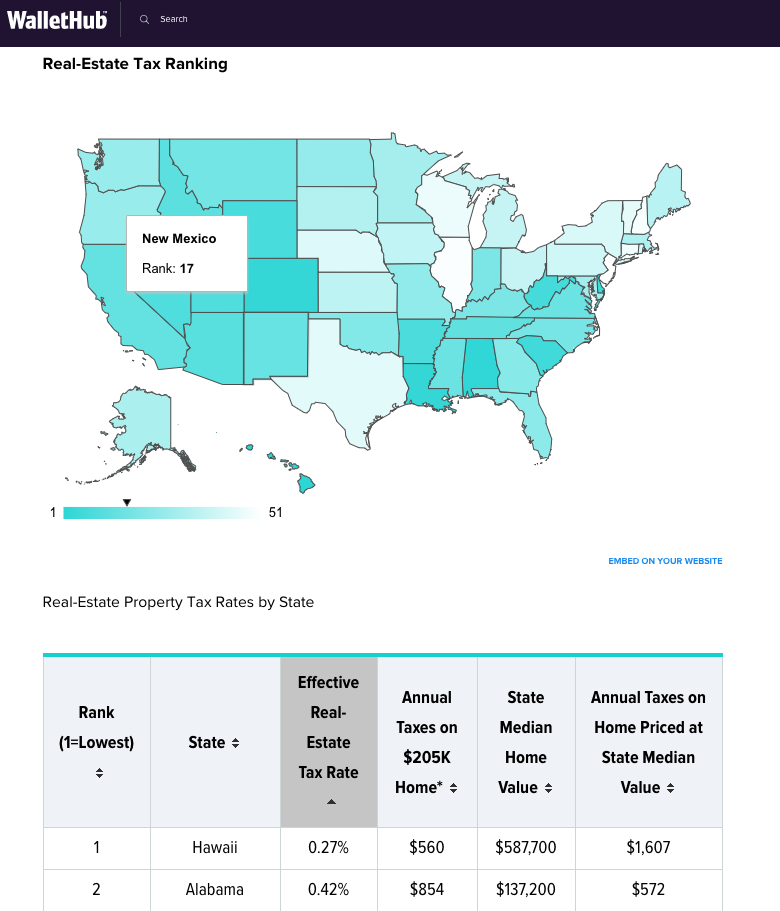

- 2020’s Property Taxes by State – WalletHub –

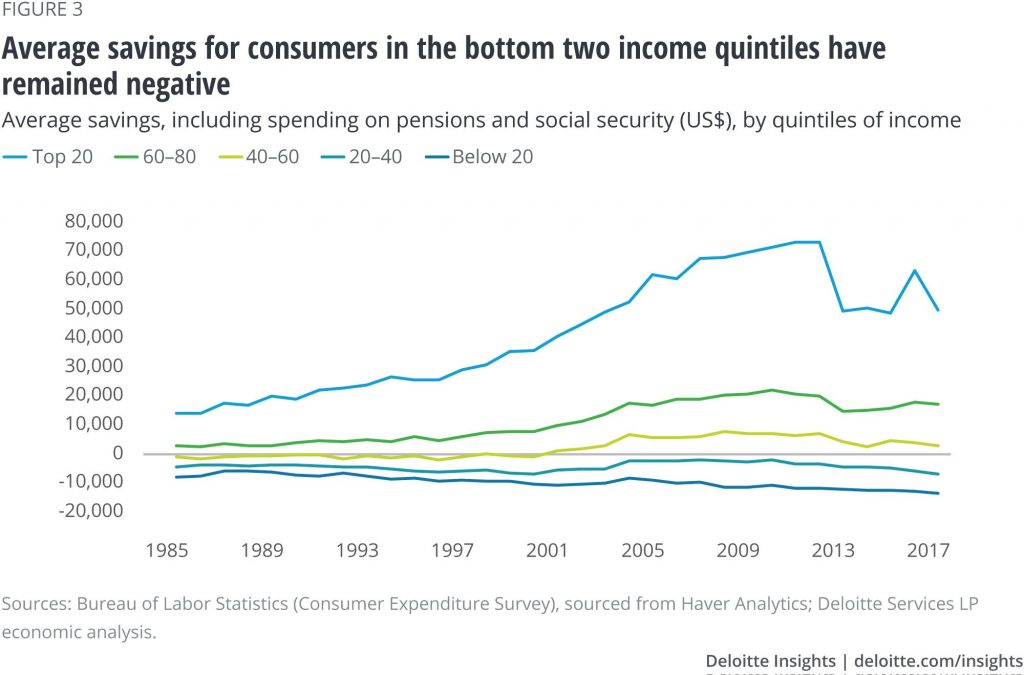

- Personal savings: A look at how Americans are saving – Deloitte – While the personal savings rate has been trending upward, average savings—calculated using the Consumer Expenditure Survey—has been on a broad declining trend since 2010–2012 for consumers across income levels and for key working-age groups.

Starting with a coach to keep me accountable and compress “lying to myself time”

A little work trying to work with someone at Donorschoose.com

Working with coach to find a bigger way to find an impact?

Don’t have any bigger plans for 2020? Any ideas?

Do HUI3 every year. Maybe MLK weekend 2021.

After leaving the day job I am realizing that there is (was always) just me as the barrier. We all get the same amount of hours a say to create something more meaningful. Its unfortunate at most people have to spend at least 40 hours a week feeding the time clock.

No exceptions

Passive Investor Accelerator & Mastermind

-Mostly Accredited high paid professionals to connect with personally and build your own network (currently 45 members)

-27 modules of content in a closed membership site

-Bi-weekly Zoom Video calls (25+ on-demand recordings a year plus all library of past calls)

-Now with a membership coordinator check-in’s to help facilitate what you are doing and connect you with the right people in the group (if you are shy)

Learn more and apply – SimplePassiveCashflow.com/Journey

If can do me a favor… If you get a chance people review leave a review for the podcast on iTunes (https://podcasts.apple.com/us/podcast/simple-passive-cashflow/id1118795347) and email simplepassivecashflow.com to a friend.

Transcript:

0:00

Hello everybody is March 2020 and this is the monthly market update that I try and do every month for you guys a compiled ation of different news articles that I’ve come across this past month you guys can get all the show notes to this at simple passive cash flow calm slash green 11 podcast listeners can get access to the recording on the YouTube channel or go to simple passive cash flow comm slash investor letter if you’re checking this out later and you want to get all the past monthly updates there you haven’t heard of me before My name is Lane Kawaoka x engineer I have the simple passive cash flow podcasts on YouTube Spotify, iTunes I Heart Radio. This is a story about a dude named Lane he moved to the mainland and bought one place to stay and then one day he went try to rent them out. And then he became one really but still may.

0:59

So first headline here. And I think a lot of us have been on this roller coaster ride the past. That’s the past week I took this article a few days ago, it took stocks only six days to fall into correction, the fastest drop in history, though this was back on February 27. And it was the quickest 10% decline all time. And I believe it’s gone up a couple times and down once I mean, today, it went up 1000 points, just craziness. If you ask me, it’s all fake money, I don’t have any stocks. My stuff is all in things that I feel like I can control and cash flow, whether the stock goes up 5% or down percent, or 6% or 2%. The value is what it cash flows every month, but it’s been pretty cool watching this, the Fed dropped the rate by half a percent point you could probably say that’s partially due to the corona virus that’s out. I don’t really buy into the whole media thing. It’s not as debilitating as the flu is I believe that mortality rates on it’s like 2%, but I’m not a medical person, nor do I know what’s really happening out there, but as they know anything, the media typically throws it out of proportion. A little bit of hindsight on coronavirus. I have a couple charts in here showing what the SARS did a while ago. That was way back when in 2003. So pence furred said that the coronavirus inverted the yield curve and again my initial thought was that the market was overreacting to the corona virus news classic fight to safety knee jerk reaction quote here the traders I spoke to were legitimately concerned about the long lasting effect. Sure the 35 bps drop in the last few weeks was repositioning to avoid getting steamrolled in the event that news got much worse. And of course, this was only about a week or two weeks ago, but in the long term, the virus has the potential to pull the global economy into recession, just like any other black swan event that we’ve been talking about for the past few years China trade war Iran you name it the euro. So there’s a couple of charts here showing the decline of when SARS came into the picture with these charts are showing is that the SARS actually made an uptick after that it was short lived charts of SARS impact on the stock market was material but short lift so if history will repeat itself perhaps we’re going to look for a little bit of a bull market on the heels of this coronavirus endemic supposedly moving on specialty grocer Earth fair to close all stores and liquidate inventory files for chapter 11 bankruptcy. This is a health food store out on the east side of the country. This one’s showing one in North Carolina the most of their locations are near Whole Foods Trader Joe’s sprouts are fresh marks. So they’re kind of just getting gobbled up by their competition, but it’s showing how a lot of these other competition is pretty fierce out there even with something that’s traditionally been thought of as an emerging market which is healthy supermarkets. CPE says industry outlook for 2020 to 2021 remains strong Dallas is in growth mode due to many factors such as a strong population growth, a friendly business environment, low operating costs compared to other gateway markets and limited regional competitors. And I think if you’ve been listening and hearing to the market, you know, this is sort of Captain Obvious news. Dallas is obviously one of the frontrunners in terms of growth, but you dig a little bit deeper and if you’re actually trying to find deals there, it’s probably banging your head against the wall or pulling your hair out whatever you do to cope with things you know, everybody knows about it, right? So as an investor, you want to go where the action is at yet you want to stay away from where all the frenzy is, too. So the interest rates have been coming down. As we all know, Forbes is saying the mortgage rates near three year low decrease was largely due to investor uncertainty surrounding the coronavirus as well as trade related and geopolitical concerns. As I said earlier, the Fed dropped The interest rate half a percent, which is pretty big movement, normally they’d like to move it in terms of quarter points. And I think when everybody hears the bad news, they automatically think that they should probably look at refinancing their mortgage. But that’s not always necessarily true. The feds rate it sort of is correlated with the Treasury, but it’s not always but this time when they did drop it half a point, it did drop a treasury, so that impacts the mortgage rates and I locked in a big deal today with him closing so I think we got kind of lucky there. We got like a 3.5% on a commercial loan to pretty awesome, but I think people get a little bit too excited. I mean, 3.5% 3.754% I mean, who really cares? I mean, it’s it really doesn’t make too much of a difference when you run the numbers and you run out of deal five, six years, but it sure helps. Nice. We get lucky.

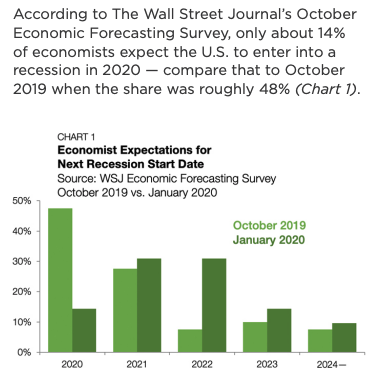

5:53

We work with hard working professionals looking to opt out of investments for the clueless I mean mainstream investors We work with people we have a direct relationship while enjoying higher returns and a quicker path to financial freedom. I personally move my endorsement from turnkey rentals to syndications as my network has grown however, the downside of many of these deals is that you need at least $50,000 to invest and the frequency of deals that meet my criteria is sporadic.

6:21

Check out my article about passive

6:22

cash flow calm slash fund and learn how I always have cash on hand by using the American Home preservation fund as part of this one two punch to be ready for a great deal while still making a double digit return. I had been investing in HP since 2016. HP is a crowdfunding solution to the mortgage crisis in America. We’re collectively the fund and investors like you pulled their money together and get great bulk discounts and distressed mortgages. It’s a business model that I think gets stronger should a bump in the economy comm because this is where there will be even more distressed inventory for HP to purchase. The American Home preservation fund aims to keep people in their homes. So you can make a 10% return while making a positive social impact invested as low as $100 by going to HP servicing.com slash investors. And if you want the free burn zone book and learn about George Newberry story, please send me an email at Lane at simple passive, casual calm.

7:23

Well, that’s a like a report from CPE talking about cleaving here cleaving multifamily report boosted the ongoing revival of the city core. So this is an example of like, you have to look at it from a submarket viewpoint, I think a lot of people will look at places like Birmingham or Cleveland. And you know, one of the first things you should look at is the population growth or where’s the population going? And that’s one way of doing it, but you really got to look at it a little bit deeper, and you got to look at on a sub market. So in Cleveland, what’s happening is that the downtown area is getting most of the new development whereas the suburbs are kind I’m struggling a little bit. So CPE says here most of the new development targets downtown Cleveland, the area ranks as the largest job hubs in Ohio and is expected to see a population growth. And I followed that up with another Sherwin Williams to develop world headquarters in Cleveland. The transition to the new facilities won’t occur until 2023 at the earliest, and they previously launched a nationwide search for their new headquarters before deciding to stay right at home in Ohio, where it’s been based since 1866 news from Las Vegas we have several articles about some of the older hotels when I mean older Oh, what was it like Carnival one, the ones that are maybe a decade or two old but they’re finally going to make a what I would call Class A hotel. And the reason why I look at this stuff is you know, just I’m not interested in hotel investing, but it’s interesting to see another asset class how they cycle through assets and how and when I say it gets older, some other things Group buys it maybe it does a little bit value add and then they take it down and then these new properties come up so dream Hotel Group is opening a 450 room luxury hotel on the Las Vegas Strip This is dubbed dream Las Vegas the project is looking to open in 2023 course are gonna have a rooftop pool deck bar lounge, two restaurants, two additional bars, gaming floor, everything that you would probably want in a level hotel. You guys are probably asking where is it? It’s going to be located across the street from the Mandalay Bay Resort and will be one of the first hotels seen from the iconic Las Vegas site property will be situated two blocks away from the new Allegiant stadium the future home of the Las Vegas Raiders, maybe Tom Brady will go there. Who knows. So already business reports that NBA forecast the US economy to slow in 2020 as job market weakens, and I always just put these articles in here, you know, these are all commentary, and you’re just making wild guesses in the sky. And I like to try and put both good articles and bad articles. But they have a point sometimes. And sometimes these predictions never happen. But again, the media is trying to sell news articles. So for those of you guys who are looking on the screen, we are showing the trend from 2018 1920 and prediction 2021 2022 of GDP growth, which is dipping this year in 2020, which should come right back up in 2021 and 2022. Inflation is holding pretty steady at 1.8 to 2.2 2.4%. Across the five years unemployment again pretty steady at just under 4% Feds funds rate it’s expected to dip down this year but come back up to where it was in 2018. And the 10 year Treasury and the 30 year mortgage rates are sort of fix. They kind of follow the Fed funds rate they’re calling the 30 year mortgage to be 3.7% this year. And go up to 3.8% next year and then up to 4.1% 2022. And this is pretty consistent with what I’m thinking I think 2020 will be a little bit of a weakness or take a breath year pretty sure Trump is going to win whether you like it or not, I don’t care personally, and then we might be in for another few years of a nice Bull Run after this is kind of my prediction took this excerpt from the Newmark Knight Frank multi family housing capital report from their 2019 fourth quarter report. Usually these things are just a bunch of words and blah, blah, blah, blah. So I’ll go over the highlights here are the sales volume, they reported that investors gravitated towards markets with a strong combination of yield and growth prospects. Yes, not too insightful. There’s kind of like obvious right in terms of cap rates, national multifamily cap rates compressed eight basis points year over year, which is nothing although cap rates increased six basis points year over year in major markets a surge of investment activity in non major markets cause yields to fall 12 basis points the rest I’m not going to read because it’s not doesn’t seem like too much of a news you guys can check this out on the YouTube channel if you guys are so inclined to read into it Arbor who is a direct lender and we use arberg for our deals, you can go through any broker, but those brokers typically don’t add any value and it just makes more sense to go straight to the source which is our bro who deals the Fannie Mae and Freddie Mac large commercial paper. So in their 2019 fourth quarter small multifamily investment trends report which are smaller multifamily apartments, I probably say and like the 20 to 100 unit ban. They’re saying that according to The Wall Street Journal’s October economic forecasting survey, only about 14% of economists expect the US to enter into recession in 2020. Compare that to when they tested in October 2019 when the share was roughly 48% sense. So what they’re saying here is the economists are sort of backpedaling, and the 48% of them call the 2019 recession. And when it didn’t happen, no, only 14% of them are calling it for 2020. And they put this on a graph what the survey was in 2019 and 2020, which, again, is horrible data, right? It’s just a survey Who the heck knows, right? But it gets these people are a little bit more insightful, I guess. But it’s still just opinion. But I think what you’re just seeing is everybody wants to look like the smartest guy and cause a recession. But when it doesn’t happen in the year just backs up to the next year. Now it’s in the next year. Oh, it’s in the next year. So I think that’s what you’re seeing in this article. Again, not too much news. But sometimes I’ll put some of these bad news articles in here just to pointed out again from arbour in that same report, they are graphing the spread between small multifamily cap rates and the 10 year Treasury yields through fourth quarter 2019. And this is why we do it folks. This is why we invest and use leverage because as investors, you’re making the difference between the spread between the cap rate and the your interest rate, which is basically the 10 year Treasury. So if you look back from 2009 to now it’s there’s always been about 300 to 500 points spread, it’s gone up a little bit, it’s gone down, but it stays pretty consistent. And I think this is one of those absolute truths in the world where this is the way the world works. And this is why I’m not too concerned where interest rates go, because if interest rates go up likely so well, the cap rates again, as an investor, I make my money off of a spread, which is typically a consistent 500 to 300 points spread, and then I apply leverage on that, too. If you’re thinking four to one, you multiply this by four. So I’m sure all of you have been keeping up with the proposed budgets from Mr. Trump, but if not, I took a little excerpt on the proposed budget which you can get online at OMB I don’t know why you would would unless you don’t have a day job and you don’t have anything better to do. But he is proposing a 5.6 billion cut from the department of education funding. What does that mean? That’s a 7.8% decrease. So I’ll go over the negatives and some of the positives here the negatives are eliminating subsidized Stafford loans. And those are the ones that don’t accrue interest while you’re enrolled. They’re going to eliminate this supplemental Education Opportunity Grant, which typically goes to independent students or families who make less than 30 grand a year, they’re cutting the 630 million of funding to the federal work study program, reducing income driven loan repayment programs to one option instead of paying 10% of your income you’d pay 12.5% payment plans would last 15 years instead of 20 with the remainder forgiven, but grad students would have to make payments for 30 years under income driven repayment and they’re eliminating the public service loan forgiveness program. Some of the positives are there reinstating the Federal Pell Grant eligibility for short term education programs. And for some currently incarcerated students who are being released within five years increasing career and technical education funding by 900 million in putting caps and graduate and parent loans with annual and lifetime limits Parent PLUS loans for undergrads will be limited to 26,500. graduate students would be capped at $50,000 annually and $100,000 total who knows how this legit plan will go and be changed. But that is the way that Trump’s kind of got his education budget lined up, should he get reelected wallet hub. These guys are really good at making these cool color graphs comparing state to state but this is actually very misleading. So what they did here is they took the 2020s properties taxes by state and I guess it’s kind of good because they have it a sort of an interactive table where you can click on the effective tax. Real estate tax rate here and number one lowest is Hawaii at 0.27%. Number two is Alabama at point four 2% effective tax rate on the real estate you know, you gotta use your brain here because obviously Hawaii’s average medium price is probably about three or four times that of Alabama. So you have to really look at what is the annual taxes on a median home that next column over the annual taxes on a $200,000 home. To me that column is meaningless because that’s a mansion in Alabama. And you frankly can’t find a 300 square foot house in Hawaii for that much state median home value, as you can see there $130,000 in Alabama to $587,000 in Hawaii, but for those of you in Hawaii, that’s the price of Paradise live where you want invest where the numbers make sense. I actually like the fourth column here annual taxes on home price at state medium value. I think that’s where you’re starting to see where the true month numbers are being shown because a lot of times like our Facebook group for example, someone will chime in and say well you know, Alabama has low taxes right and here the effective tax rate is the number two lowest in the country but you got to go on the based on the value so like another one is a famous one is like Chicago, Chicago has really high taxes and sort of high values so that can really skew your numbers. Again, I would just recommend if you’re looking at rental properties, just put into the analyzer and see how the numbers turn out and compare that number at the bottom of the spreadsheet which is anticipated cash flow on your Performa we kind of had a lot of bad news. I wanted to put in the side with some good news. And these are all five headlines of Hey, look on the brighter side guys, it’s not all doom and gloom. First one here by CNBC. The US is experiencing the longest economic expansion on record best seen the period from 1991 to 2001. Some guys probably like Whoa, what’s gonna end soon? Well, you should enjoy the good times right now. New York Times says the decade long us expansion has generated At 20 million jobs market watch says 3.4%. year over year, wage growth is the strongest in more than a decade. Yahoo Finance says January 2020 had a record job growth in the private sector largest monthly gains since March 2015. And the Whitehouse. gov was always trying to toot their horn does the US hit the lowest unemployment rate in 50 years in 2009. Of course, there’s a lot of questions whether how do you take the unemployment rate? Is it legit, but right now things are pretty good. I mean, people are working and I haven’t really seen any indicators saying that larger companies are laying people off decreasing their orders. And in my mastermind, I’m in somebody predicted the 2008 meltdown in there and that person was like a big time builder. And they were saying that they knew it was coming down when the foot traffic that we’re checking out those new bills just weren’t there. The demand just dried up and that was when they knew was the end and that’s why it’s been 25 thousand dollars to go to groups like that because they are closer to the action. And hopefully I can react better than the average bear out there by having that information. And I don’t want to just sit on the sidelines. I know I say this so many times, but it’s because I talked to so many new investors, you know, they’ll book every intro call with me, we’ll chat and a lot of investors will have this mindset of like, well, it’s the top of the market, I’m just gonna hold back. And I think that’s a huge mistake, especially if your net worth is under half a million dollars, you need to go out there and swing the bat and go into equity deals and grow your network. You might be hearing guys that are four or 510 million dollars and above sitting on their high horse saying they’re not doing anything right now. Well, guess what, they can do nothing. They can live off one 2% off that large portfolio and not do anything and I ultimately think is just newer investors just kind of shooting themselves in the foot. So Deloitte did a report on the personal savings rate of Americans. And they said while the personal savings rate has been trending upward average savings calculated using the consumer actions expenditure survey has been on a broad decline since 2010 2012. for consumers across income levels and for key working age groups. So we got a little graph here showing how different groups are saving their money, which ultimately, I think that’s the most important statistic to keep, you know, whenever I have a console with an investor, yeah, like to know how much you make and how much you spend, but I ultimately want to know how much you net at the end of the year again, most investors in our group, they’re able to save maybe about $30,000 a year and other ones that are a little better making able to see $50,000 a year that means they might be able to buy two rental properties a year not saying they would, right, but you’ll probably go crazy after you get five or 10 of those turnkey rentals, but they’re exponentially growing their portfolio. So this graph is kind of showing. One thing I pick up on is from 2008. You know, everybody got shell shocked and the recession brought people back to frugal ness. And I think there was a hashtag trend out there where he was cool to be frugal. Right, I read another book and they coined this term called the Great forgetting. And they say, people will normally forget how things were in like eight to 12 years. And I think that’s what’s going on here. Maybe people got really frugal 2008 to 2009 1011 12. But you’re seeing that the clients start to happen in 2013, especially in the top 20% of folks. And the other takeaway I have from this graph is it’s just a little bad that the top 20% have so much disposable income, and that’s why they you know, they go into the all these deals, and that’s great, right, but the people who are in the 8060 to 80 percentile 40 to 60 percentile 20 to 40%. percentile, like they just are not able to create any net at the end of the year. In fact that people that are below 40%, they are negative, they’re they’re like going into debt every single year. So some new podcasts that I have created this past month are up here we did some discussions with asset protection. If you guys think lol C’s are the end all be all well that’s just where it starts and then people that are 1,000,002 million dollar net worth and above should probably be looking into irrevocable trusts and potentially even international trusts. We had Marco Santorelli of nerado who talked about Top Things ignorant investors do and again one of those gonna shoot themselves in the foot not doing anything so in the top markets to invest in 2020 in all these are short YouTube clips that have created in the YouTube channel so if you guys want to go there and share it with friends, I’d appreciate it part of the Richie’s land conservation easements what interest rate to expect from private money lending don’t invest in short term rentals until you understand this, where’s the best marketing platform for short term rentals. Another big one is how is the politics and rent control affect where you should invest? I just stick to the red states simple passive cash flow right big changes to your retirement accounts. And if you didn’t hear what they did with the secure act better, go and check out that article on how the secure x screwed millions out of people’s retirements and do I need asset protection on my retirement accounts was answered in that short form but do you guys have any more questions go to simple passive cash flow calm slash question and type it in there if you leave your email we’ll try and get an answer back to you for a little bit of what I’ve been up to. And again, these all come from the Tony Robbins six needs versus growth so I started to employ a coach to keep me accountable and compress time for me and basically eliminate the time that I lie to myself continually I’ve been doing this for about a month and already it’s just been totally worth its money. I think consider a accountability partner for your selfish you can’t afford it. But yeah, I mean, at the price I pay for this thing pays for itself like four or five times over there, like the emotions that you have the thoughts you having is a sign it’s your job to turn that sign into action. And most times in the past I would just like ignore it right. But as I tell somebody coach who has skin in the game in me being successful, they kind of tease that out and they don’t let me just be okay with contribution. So I actually had a call, I’m trying to work out something where we can contribute to some kind of a charity. I think if the URL is like simple passive cash flow, calm slash charity, you can see the couple projects we’ve done in the past. But my problem is, like, I don’t have the time to find good causes to give to and I don’t want it to just go into oblivion, like a Red Cross thing. I’m not saying it’s a bad cause, but I’d rather be a little bit more. I mean, I’m totally acting like a spoiled rich person, but I want to have control over it. I want to designate where it goes. And one cool site that I found was donors choose so I had a consult with them today figuring out what we can do as a group to pull our money together and something where I can go in there maybe an hour a month and select individual projects. And what’s cool in there is like my wife’s a teacher. So we did this with her class. Last year, and quite frankly, she can’t spend all the money. I mean, there’s just there’s a lot of need on this other site, other teachers but it’s really cool because the teachers they give you feedback, the kids write you letters and they give you like a monthly report on what’s happening so you really feel like you’re making a difference but I want to go in there and pen select projects that are aligned with financial literacy education. Somebody wants to buy a seesaw or some kind of I think it was like a canoe or something. I’m like yeah, we’re not gonna do that and that’s where I’m going to get involved try and pick some of those projects but if you guys have something else or somebody else in our who wants to take the lead on being the point person for selecting these type of charities, let me know number three here significance again, I working with that coach and something that I’m realizing working with them is I need to try and find a way to make a bigger impact whether it’s for ego or what I feel that I need to help spread the word of financial freedom and investing the right way too many people are just misled By the wrong things like paying off debt, I mean, if you pay off debt, you’ll never buy assets that grow your net worth. That’s exactly what they want you to do if there wasn’t dead people would never own their houses not saying that buying a house to live in is a good idea. Number four, how did I create uncertainty in my life? Because sometimes you need to get out of your comfort zone. I don’t have any bigger plans for this year. So if you guys come up with ideas that will stuff for our group to do I don’t know I’m maybe I’m just a little tired. Since we had the QE three in Hawaii a few weeks ago. How did I create some certainty? The QE three was really cool. And I’ll put some pictures on it here. That was us. And that was how I fulfilled that last love and connection because people is what makes all the difference. But people came over for probably about four days, five days actually, if you count the first night, and it was a lot of fun. And it’s something I think that I’m just speaking for myself. Something I’ll probably remember forever. It’s not often you get a group of 30 to 55 year olds in a room are out hiking out on the beach for a sunrise. out to a luau out playing some pickleball and escape rooms where you can do something fun with first total strangers but really start to bond over some of the like mindedness of the financial freedom aspect. And you know, what do you do to build a legacy? So that was something that I want to do it more in the future. And I am thinking this slight mastermind thing might be a annual event ran more like a family reunion than a dozen other real estate events. So maybe Martin Luther King weekend might be a good time to do it. This time was a little weird with Valentine’s Day involved on the first day, I had to go to 90 degrees. So that kind of took a lot of energy. Yeah, maybe mark your calendar might be a little premature of Martin Luther King 2021. Let me see you guys in Hawaii, some of the resistance and barriers after leaving my day job. I’m realizing that it’s just me is the barrier and it always was and people always say well, you must have a lot of this extra time to do what you want. And I honestly say that I probably get almost the same amount done. The day as I did when I was working a full day job I might get like 10 20% more done without the day job but I think it’s there’s a lot less stress a lot better quality of life and it just brings perspective that people especially for the people who don’t like their day jobs most people have to spend at least 40 hours a week beating the time clock in for what right yeah, you make some good friends at work but if you didn’t have to go to the job would you still hang out with those people? Maybe Maybe not. So if there’s any way I can help anybody get out of financial freedom you know, that’s what I’m trying to wrap my head around how do I kind of help the most people get out of this a quick technology tip wrote a quick article on how do you create an instant note without opening up the lock feature on your iPhone every single time I just get so many ideas and I’m sure a lot of you guys get so many ideas and just trying to capture it is one of the most important things especially if you’ve read the whole GTD getting things done methods I finished up this willpower doesn’t work which actually thought was wasn’t a bad book. I thought like it was just had a lot of different strategies. there and I think you’ve just listened to it not at two x speed or three x speed, you just listen at one x speed that might incite some habit changes or new processes you can put into your daily life. So I just wrapped that up and I’m starting to read the go giver. Now, I think the premise is helping others get to where they want to be, and the rest should fall into place. And I’m starting the book club. So what we’re going to do here is every other month I’ll be the last Saturday of the month, every other month, we are going to do a webinar or a meeting and whoever wants to join on you know, you don’t have to be in the passive investor accelerator mastermind and just jump on and hopefully you read the book, but the goal here is to read five or six books a year and you guys can join there at simple passive cash flow calm slash lien hat and click the button register with zoom and you can join us on all the BI monthly calls we have on the books so if you guys go there, sign up and or you go you got two months, I think the next one, I’ll have it is April 25, which is Saturday where we’ll be going over the good giver. So you guys got two months to read it though, but it gets started now. And if you haven’t checked out the passive investor excetera mastermind, we are pretty much done with the first year of it in existence, some investors are phasing out of it. And that was my goal, right? Get them in, get you guys up to a point where you guys can analyze deals and be able to create your network and build some friendships. And if you guys want to get out, right, it’s not one of those things that you need to be in forever. Maybe you need to take a break. Maybe you can come back later. But yeah, we got some openings there. So if you guys want to check that out, go to simple passive cash flow, comm slash journey. So somebody asks, How do you find or choose your coach? So I just went through the Tony Robbins, folks, I can connect you with my guy, but yeah, I mean, supposedly you do the disc exam and this personality test and they fit you with somebody. I don’t know if that’s really how it is, but I Like as a speaking as an entrepreneur, everybody’s an entrepreneur these days, right? You don’t know who’s legit, who’s just faking it. So I just want to go to some brand that was sort of okay. And I’m sure Tony Robbins brand and or directory of coaches is sort of, okay, maybe even pretty good. Who knows, but I just didn’t have the bandwidth to go find a coach. And some people recommended one rule. If you want to really go and roll up your sleeves and go find your own coach, a recommendation that was given to me is you always go off for a referral. It’s just like, Oh, right, like that’s what we do with property managers, brokers, everybody, right, syndicators, it’s always offer all and then they said, well try it out. You can do a few sessions with somebody another session with somebody else and just try it out. See how it works, because that coach may not jive with you, or you may really resonate with them. And another question I had was, well, does this person need to run a podcast and be in real estate and do this stuff I do. And the conclusion that I came up with that you may or may not agree with is that No, they don’t. need to know anything about what you do, they don’t even need to know what a rental property is, or they don’t. Their role is to apply a framework of getting results with you and keeping you accountable and calling you out on your BS. And if they can do that, they probably do 80 to 90% of what you’re looking to do. So a thing that’s just my opinion is they don’t really be doing what you’re doing. I think if you’re looking for that type of person, you’re looking more for a specific business coach. Thank you for listening, and we’ll see you guys next month and be sure to tell your friends about the podcasts and have a good evening everybody like

33:41

this website offers very general information concerning real estate for investment purposes every investor situation is unique. Always seek the services of licensed third party appraisers inspectors to verify the value and condition of any property you intend to purchase. Use the services of professional title and escrow companies and licensed tax investment and or legal advisor before relying on any information contained here and information is not guaranteed as an every investment there is risk. The content found here is just my opinion and things change and I reserve the right to change my mind. Above all else, do your own analysis and think for yourself because in the end, you’re the only person who is going to look out for your best interests.

Transcribed by https://otter.ai