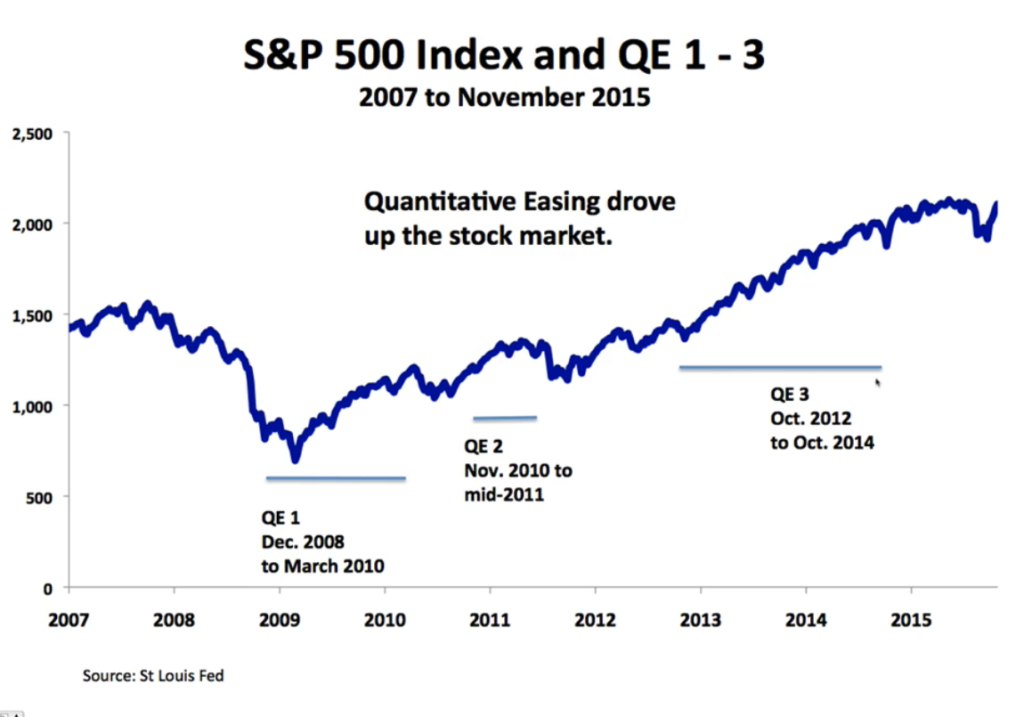

Quantitative Easing created $3.5 trillion from 2009 to 2014

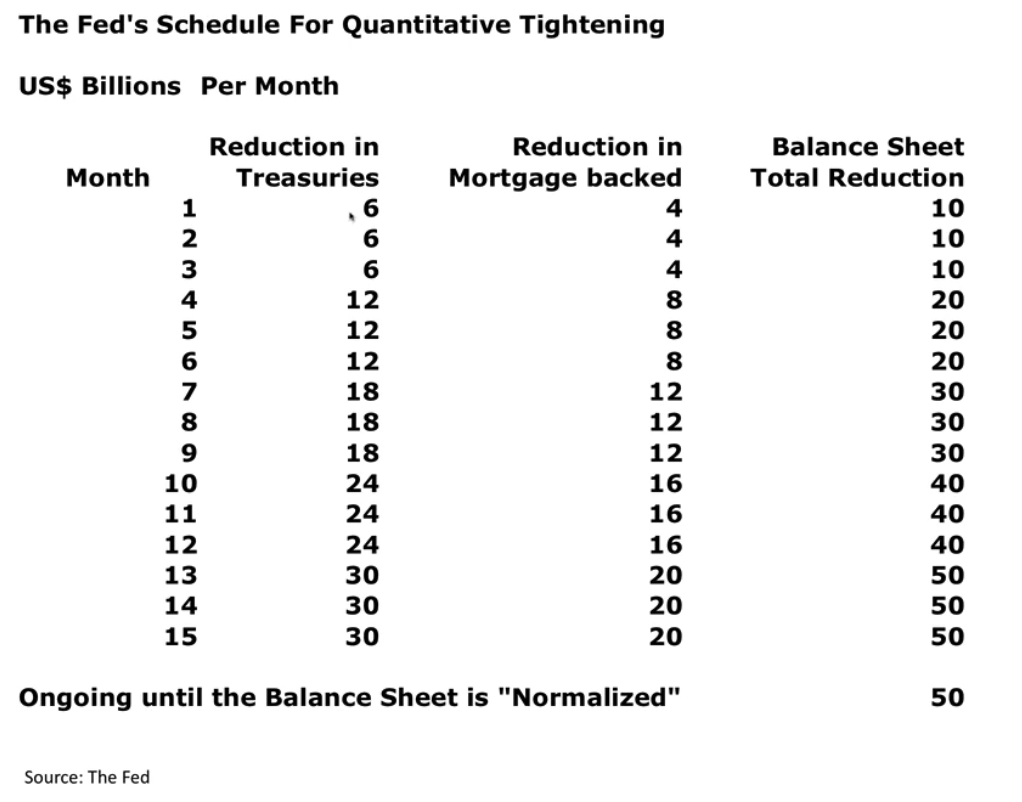

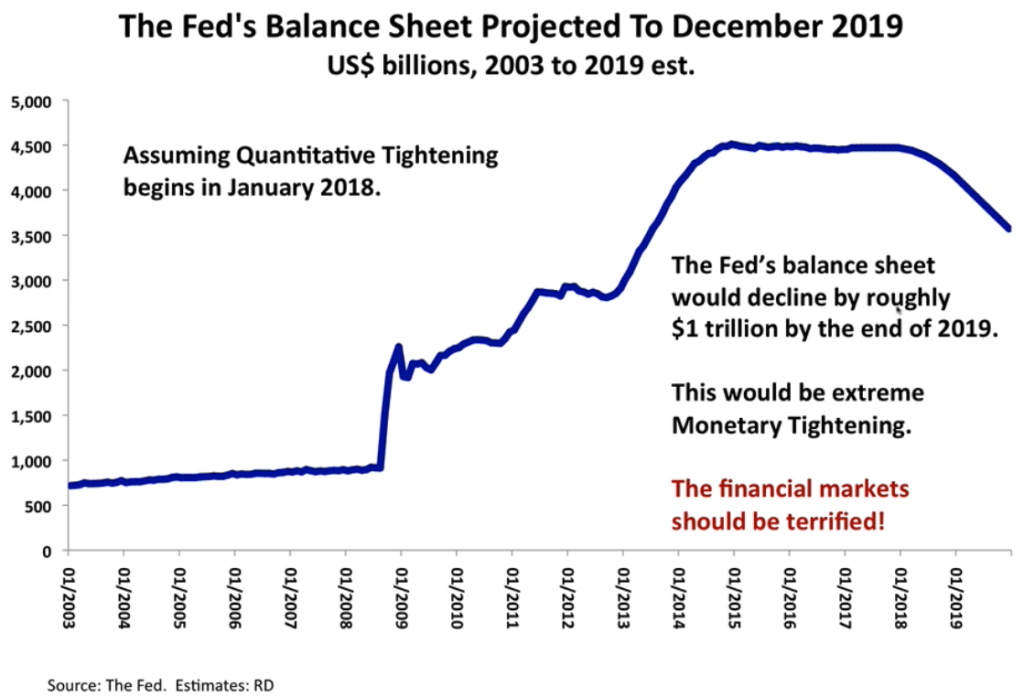

Now “Quantitative Tightening” is coming and will drain liquidity from markets

No launch date but says late 2018 but here is the Fed’s schedule

Do I think there will be a slight correction but the FED is trying to get back some “dry powder” to be able to stop a monumental slide? If there is a 10% plus correction the FED will go back to QE3-QE4.

In the end, don’t freak out just buy investments that are undervalued. If you are new well sorry you need a mentor or you need to push through lukewarm turnkey deals as fast as possible.

Andrew Savikas- Investor, advisor, writer, father. Founder at @yieldtalk. Ex @oreillymedia, @safari. Occasional consultant & speaker. Chronic reader.

1) Your background and your Real Estate investing track record? Andrew Savikas andrew@yieldtalk.com My own journey through crowdfunding, especially real estate

Importance of new crowdfunding choices in helping fuel entrepreneurism (and overall economic growth), especially serving traditionally underserved categories (eg non-males and non-tech companies outside of Silicon Valley, NYC, and Boston)

You should also ask me about the time I had to pick between the Google IPO and a new couch (I picked wrong!) criteria in your site, insights from looking at all though sites, and your recommendation for people to invest in rentals, crowd funding, or direct syndication.

2) Something that you have recently or thought about “burning your cash” on for time savings or an improvement in quality of life. [Andrew] After leaving my last job (CEO of an ed-tech company for 5 years) right after my second child was born, deliberately moved to a lower-cost-of-living place and dialed down work commitments to have more time with my kids while they’re young. Definitely worth it! But I’ll never forget the night I was putting my son to sleep soon after my daughter was born and contemplating the return to a very demanding job that was only going to get more so, and imagining myself 5 years in the future wishing I could trade the money I’d made for more time with the kids while they were growing up.

3) Something that you changed your mind on? Our ego often gets in the way of greatness. [Andrew] Having kids definitely changed my perspective about the opportunity cost of my career trajectory. Has helped me see the benefits of a more balanced portfolio approach compared with driving 1000% down one path. Also, what it means to have a “balanced” or “diversified” portfolio. Was profoundly influenced by Nassim Taleb’s “Anti-fragile” and the concepts of convex and concave risk (and the notion of a “barbell” portfolio).

4) Anything we missed and contact info if you would like anyone to get a hold of you. URL? [Andrew] I’m a voracious reader, and as a side project I started posting lengthy reviews of books that have shaped my thinking about leadership, strategy, business, and more. I’m also super into meditation and mindfulness, and have written about 10 books that helped me apply mindfulness to my life in general, and doing better work in particular. And speaking of books, 13 years ago I wrote a book about Microsoft Word of all things.

OPM (Other People’s Money) concept does not apply to investing in business alone but to real estate as well. It is a strategy most financial savvy do to leverage, borrowing using other people’s money for capital to increase potential returns.

Why burden yourself when purchasing properties for investment if you can pool OPM (Other People’s Money) to start and strategize earlier?

Time is gold, and the clock is ticking!

Crowdfunding resembles the OPM concept. Wherein not only does one investor shell out money but a group of investors pools their money to purchase rental properties, multi-family units, or commercial property.

In a crowdfunding platform, they offer a minimum amount to start investing. It will use that money to manage a diversified portfolio of property projects all over the U.S. A scheduled payout will be established as the investor’s shares grow in value, still depending on the status of the property.

They were one of the biggest Crowdfunding sites however they went under because they can’t afford to secure additional capital to fund additional investor acquisition.

In other words, the marketing to get people to sign up is coming from outside sources (venture capital) and not from their business. This is typical of a tech startup.

How Real Estate Crowdfunding Works

Crowdfunding has websites that most of the time act as the connections between the company behind the website, the one looking for investment opportunities, and the investor.

A well-founded crowdfunding website (or company) must be a good negotiator of properties that they’re buying and can attract legit investors to profitably fund the opportunities they’re eyeing for. Moreover, they need to collectively pool money that can be used to invest in the company’s future.

Advantages and Disadvantages of Crowdfunding

Advantages Accessible to anyone No experience needed Exhibits positive returns as compared to a savings account

Disadvantages Capital can be at high risk Undisclosed penalties may be present Lack of control as an investor Poor liquidity

I’m doing some research on Crowdfunding sites (although I always prefer working directly with the operator as opposed to using these middlemen platforms). A lot of Hui Deal Pipeline Club members have been collaborating on this and been using Equity Multiple.

As a syndicator I don’t like using these sites to raise funds because: 1) I don’t have access to the investor contacts which totally kills the referral marketing for future deals and 2) we tried it on a previous deal where the Crowdfunding site committed to raising a small portion of our total raise and they fell on their face..

Not saying that the Crowdfunding sites will never be effective but at this time it is not a useful means for experienced syndicators who already have investors of their own..

Beware as an investor! Its like trying to find a mate on Tinder, this is a controversial subject I know. But for many, there is a reason they are on the “open market” and cannot attract “capital” on their own from their own personal network..

Fundrise & Realty Mogul have launched “eREITs” which tries to tackle investment vehicles other platforms are not capitalizing on.. It’s interesting to watch how they trademarked “eREITs”.. Definitely a sign where investing is going.. Again institutions controlling and taking a cut away from the little guy.. 🙁

BLACKHAT TACTIC 😉 Some deals are put out to private networks (like the Hui Deal Pipeline Club) and these crowdfunding sites simultaneously..

Many times the crowdfunding site offers a 7% preferred rate where the direct source offering gives a 8% preferred rate. Tricky ,tricky if you ask me!.

Now one could backward engineer this all and go around the crowdfunding site but still, like I always say, YOU DON’T KNOW THESE GUYS..

Syndicator’s are running around out there without any operator experience or portfolio of their own and doing deals with people just off referral.. A recipe for disaster if you ask me!

Here are comments from Hui Members:

“I’ve invested in 10 you have listed and am familiar with quite a few others. The best on your list are yieldstreet.com, groundfloor.us and streetshares.com. I have had 12-14 % returns with all three. Hedgable.com is also a good site for investing in the stock market.”

“Some of the companies have questionable backgrounds make sure you google ‘company name + SEC infraction.”

“Chicago company that was recently shut down for allegedly running a Ponzi scheme. They promised investors returns of 15% to 20% on Chicago real estate. This is a huge red flag in my opinion. Those returns are extremely tough to achieve in Chicago, even in “high yield” areas.” Read the related article here.

“The returns started around 15% using my criteria but have leveled off to about 8% since then and I expect it to remain as this level.”

“Lending Club – This is UNSECURED debt. This is also known as peer to peer lending.. Like a guy needs to borrow 3k for a table saw for his business or someone has a broken car.. Good user experience and the information on the dashboard provided is much more readable than Prosper.com.. One user says “my net annualized return is 12.37 % and Adjusted net annualized return is 5.6%.. Both information is easily readable on the dashboard and it gives an easy to read view of the payments of how much principal, interest, late fees.. Also gives a good view of the notes itself like issued, in grace, fully paid, late by 16-30 days. It has automatic re-invest and liquidate quickly.”

“PeerStreet – Works like Lending Club but is Secured by real estate.. They also give you quite a bit of information on borrower as well as the property details (LTV, Stressed LTV, Improved LTV, borrower’s FICO, etc.).”.

“Prosper – It does same as above Lending Club but not as good dashboard information interface.. It has automatic reinvest.”

Crowdfunding websites seem to show a lot of opportunities. Perhaps in a decade or more, it can be a viable solution or alternative to syndication.

https://youtu.be/1ErFrGnkcH4

“Yieldstreet – It’s for accredited investors only – So basically for people who are Rich already!”

“Some of the more established crowdfunding sites are starting to lower their returns because they have achieved a good sized crowd.. It’s still a wild wild west space with many platforms/website jockeying for position.. Many are offering high rates of return and under-collateralizing themselves in my opinion for market share.. Beware some have fraud in their past so make sure you do a little Google-stalking to dig up the dirt.. When I evaluate deals for the Hui Deal Pipeline Club, I realize there are so many deals out there that if someone has a questionable past, I just move on.. Too many good people doing good deals to not be choosy.. This is a newbie mistake I see a lot in private placement investors that they marry the first deal they get pitched at a local REI meeting.. It happened to my partner who lost $45K and myself who lost $40K.”

“Overall what I hear from you folks trying this method of investing is that the default rate is higher than what is expected and the middle man (crowdfunding site) is getting rich here.. But hey if you are not good at networking these are the table scraps you get.”

Note: There is a lot of consolidation in this new space. Think of the many competitors there was before there was the eBay or the Amazon. I get website alerts of the below sites going offline all the time.

https://alphaflow.com AlphaFlow helps investors build diversified real estate portfolios across the crowdfunding industry. Make informed decisions, faster.

https://agfunder.com AgFunder is the premier marketplace for the most promising Ag and AgTech startups seeking to raise investment capital from accredited investors.

https://1000angels.com Build your own venture portfolio, free of management fees or carried interest.

https://angel.co – OUT OF BUSINESS. Private single-deal VC funds led by top angels.

https://yieldstreet.com YieldStreet connects investors to originators with deep expertise in alternative lending.

https://circleup.com CircleUp lists companies for you to review across a spectrum of consumer product and retail categories. Browse or search our portfolio to find opportunities that interest you.

https://crowdfunder.com Venture Capital: Crowdsourced. Invest in many deals at the same terms as leading VCs

https://www.crowdstreet.com CrowdStreet provides superior technology solutions that enable all investors to directly connect, invest, and create wealth through real estate.

https://fundable.com Fundable is a powerful fundraising platform that enables Startups to quickly engage a large network of Backers to raise capital.

https://fundersclub.com Invest in the world’s most promising startups. Diversify your investment portfolio with insider access to highly vetted startups from Silicon Valley and beyond in just minutes.

https://hedgeable.com We are the only digital wealth manager to offer curated investing in venture capital.

https://homeunion.com – OUT OF BUSINESS. Build a diversified residential real estate portfolio using HomeUnion’s end-to-end services of property selection, acquisition, management and sale to match your financial goals

https://ifunding.com -OUT OF BUSINESS. Revolutionizing Real Estate Investing. Individuals invest as little as $5,000 in institutional quality real estate.

https://lendingclub.com Build a diversified portfolio that can offers solid returns, low volatility, and monthly cash flow

https://lendingrobot.com Automated management of your existing Lending Club, Prosper, or Funding Circle accounts.

https://lendinghome.com Build your own diversified, institutional-quality real estate portfolio in minutes. LendingHome offers high returns and durations of just 12 months or less.

https://www.macrocrowd.com We work with investment specialists who have vetted billions of dollars in real estate developments. These industry giants provide us with exclusive investment opportunities for our platform’s investors.

https://microventures.com Get access to highly curated early and late stage investment opportunities

https://nextseed.com Invest in exclusive, pre-vetted deals that used to be available only to the wealthy and well-connected.

https://peerrealty.com PeerRealty is the premier real estate crowdfunding platform. Gain insider access to high quality opportunities with top developers.

https://www.peerstreet.com PeerStreet is a marketplace that provides unprecedented access to high quality real estate loan investments.

https://prosper.com Investors can earn solid returns by investing in personal loans listed on Prosper

https://seedups.com – OUT OF BUSINESS. Connecting Investors with Technology Startups

https://selequity.com Selequity connects accredited investors with the sponsors of commercial real estate (CRE) investment offerings. Our national network of accomplished real estate professionals assures you’ll have unique access to investment opportunities.

https://sharestates.com Invest in real estate with as little as $1,000. Faster access to capital for real estate developers.

https://upstart.com We go beyond FICO scores to finance people based on signals of their potential, including schools attended, area of study, academic performance, and work history.

https://wefunder.com Back founders solving the things you care about. Grok the risks, then join 93,004 investors who funded 155 startups with $35.5 million.

https://acquirerealestate.com –OUT OF BUSINESS. Acquire Real Estate identifies, underwrites and pre-funds high quality commercial real estate properties. We then offer the opportunity for accredited investors to invest alongside us.

https://www.wealthmigrate.com/ Wealth Migrate is the leading global real estate investment marketplace, giving investors direct access to exclusive real estate investment opportunities in premier markets around the world.

https://neighborly.com/ Invest in the places you live, work and play. Neighborly is modern public finance.

https://www.instalend.com Invest online in senior debt real estate opportunities and earn monthly distributions

https://www.realcrowd.com Build relationships with commercial real estate companies and invest directly in their investment opportunities.

https://www.venture.co Diversify how you invest with access to new private companies in exciting industries raising funding with offerings open to both accredited and every day investors.

https://streitwise.com A new way to invest in real estate designed to be rewarding and accessible for everyone, stREITwise cuts out the middlemen and passes the savings on to you, the investor.

https://www.iselectfund.com/ iSelect works with accredited investors to assemble a diversified portfolio of the Midwest’s most promising emerging growth companies through their own financial advisors.

https://www.realtyevest.com RealtyeVest is an online marketplace that connects investors and sponsors (real estate owner-operators) to crowdfund exclusive real estate investments.

https://www.arborcrowd.com ArborCrowd is an online commercial real estate company. By allowing people to co-invest with successful real estate deal-makers, ArborCrowd enables millions of investors to maximize their financial returns.

https://crudefunders.com Using Crudefunder’s innovative online investment marketplace, we provide sophisticated and beginner investors with the opportunity to invest in Oil & Gas Projects.

https://www.cityvest.com CityVest is an online marketplace where accredited investors can pool their capital to buy shares in institutional real estate investments.

https://www.rabbleworks.com Rabble is an impact investing platform that connects people with projects that strengthen communities.

https://firstrealfund.com First RealFund’s Mission is to identify, offer, co-invest, & manage superior commercial real estate investments with capable owners and quality assets.

https://www.honeycombcredit.com/ Honeycomb allows local businesses to borrow loans of up to $50,000 directly from their own loyal customers for business expansion projects.

https://fig.co A publisher where you can get a share of revenue from game sales – we bring together developers and communities from all over the world to publish great games.

https://www.buytheblock.com Buy The Block online investing in real estate with your peers. Pool funds, share knowledge, vote on a property to invest, efficiently manage accounts online.

OPM (Other People’s Money) concept does not apply to investing in business alone but to real estate as well. It is a strategy most financial savvy do to leverage, borrowing using other people’s money for capital to increase potential returns.

Text “simple” to 314-665-1767 to download the Hui Google Drive files and the 2018 Rental Property Analyzer

Please help the show by leaving a review: http://getpodcast.reviews/id/1118795347

Join the Hui Deal Pipeline Club! SimplePassiveCashflow.com/club

Pardon the grammar – I’m an Engeneer, Enginere, Engenere… I’m good with math! Here are the Show Notes:

Currently have 5 rentals and 80k of income and trying to paying off rentals because near retirement

Also flips properties where the goal is 20k profit

He outsources much of the work

Got rentals in 2011 and regret not doing it earlier

Got hammered in 2008

Got out of the market in 2000

Interest rates are very low which is different that past times which means a good time to lock in loans, stocks are pretty high

Real estate is not for everyone and might have a wrong skill set

If you don’t want to do the work be a hard money flipper but only make 10% (you need to have the money)

Don’t lend to someone doing their first flip

Need to hire a virtual assistant – 5 properties can manage by self

Let go of politics

Marriage advice

Begin with the end in mind – He already knows his legacy and just lives it

Teaching kids financial principals – mindsets and habits

To teach a 12-year-old – give them money

To teach a 30-year-old – they need to want to fix the money problem

Letting go to be happy

richersoul.com

Text “simple” to 314-665-1767 to download the Hui Google Drive files and the 2018 Rental Property Analyzer

Please help the show by leaving a review: http://getpodcast.reviews/id/1118795347

Join the Hui Deal Pipeline Club! SimplePassiveCashflow.com/club

Pardon the grammar – I’m an Engeneer, Enginere, Engenere… I’m good with math! Here are the Show Notes:

Mark Allen is a broker

Started in 2009 and went to Westpoint Academy

Got a $35k loan to get started in FL

Started with subject to or assuming the loan method of acquisition

2015-2016 sold initial properties and started flipping properties while working the day job

lead to MFH

Saved the money from flips and day job to go into MFH

You can find Mark at SVN and check out his podcast

ROI on time is more for Commercial than residential

Provide value by driving properties, pictures, transaction beat

Yadi matrix, co-star offer owner data

Face to face is better than email or phone

Bring 80-year-old sellers flowers

once or every two months a touch point with some value

As an investor go right to the broker and all of them

CCIM is a higher level designation (but that’s your job as an investor to know what a deal is)

Loopnet/correct C is a good way to find active brokers who are perhaps hungry

SVN, Marcus, Colliers, JLL, CBRE are popular brokers

Call brokers and introduce yourself

Share pitch deck with broker and share team so you show that you are credible

With our technology today and the availability of financial information right at your fingertips, many people consider doing D-I-Y financial planning on their own.

We can’t blame them!

Some do not trust financial planners these days and they do not think that they’re not following the fiduciary rule at all. Perhaps, they have this one acquaintance who suddenly, out of nowhere, will message you and invite you for coffee. Only to find out that they want to discuss wealth management and financial analysis!

Is it still worth your time and resources to trust a financial planner?

https://youtu.be/KSar5qUV1d0

What’s a Financial Planner and What is Their Purpose

A Financial Planner assists you on your financial goals and purpose. They may involve in your budgeting, saving, tax strategies, wealth building and financial legacy creation.

They figure out your financial situation, digging in from your past financial problems towards creating doable financial goals that will bring freedom. In which, they must respond to the BEST interest of their client.

They figure out your financial situation, digging in from your past financial problems towards creating doable financial goals that will bring freedom. In which, they must respond to the BEST interest of their client.

Financial Planners and My Experience

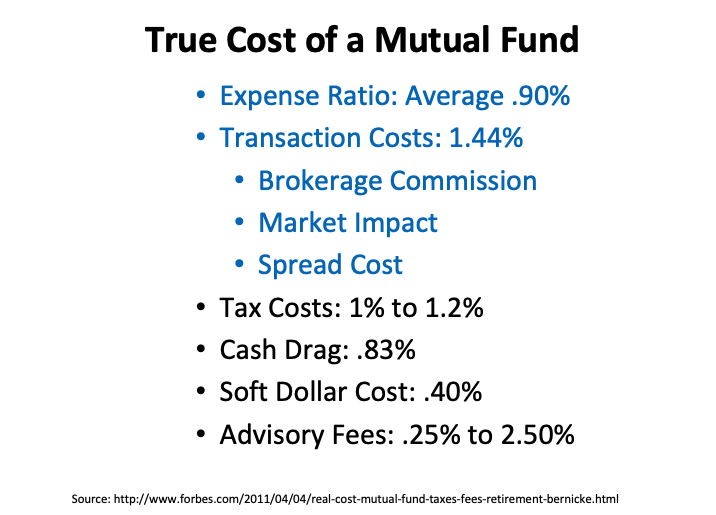

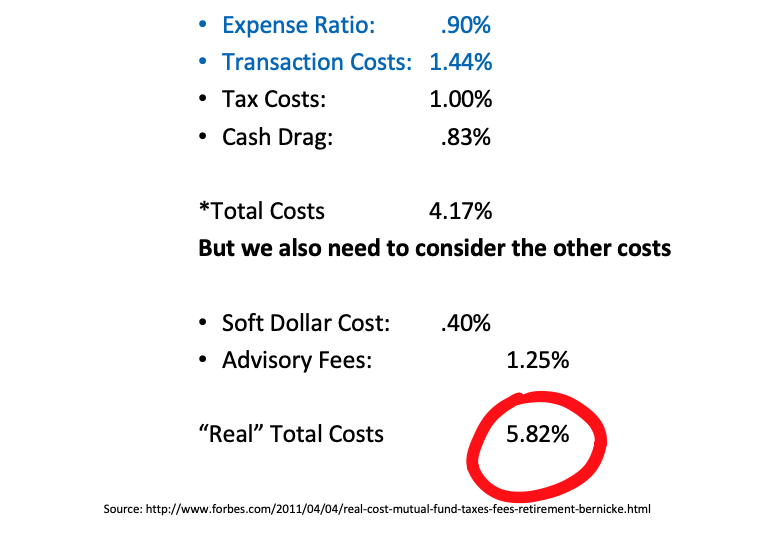

Today, we call this ACH direct deposits but the importance of this cashflow has not changed. Yet, in the 1960-1980s, Americans were brainwashed to invest in non-income based investments that had heavy hidden fees with the creation of mutual funds.

This topic really fires me up!

Here is a little humorous video to lighten the mood. Warning… the video is 20 minutes so better put the sign on your desk saying you are “away at the toilet” or “away at lunch.”

I’m not a fan of Suze Orman/Dave Ramsey show because of their scarcity/frugal money saving ideas. But for some people who can’t seem to save two pennies to save their life, I guess it is better than nothing.🤷🏻

Obsessed on planning for your retirement?

https://youtu.be/gvZSpET11ZY

NOTE: Check out Suze Orman WTF face at 4:41 when the caller says their financial planner recommended buying an annuity (shocking 5% commission for the financial planner) .

At 4:00 financial advisors make commissions and often put you in investments that are good for their pockets.

Obama tried to do a good thing and pass a law where all financial professionals (like brokers and insurance agents) had to adhere to the “fiduciary” standards—meaning they’d have to work in your best interest if they were advising you on your retirement investments. Unfortunately, this died recently and there is no more fiduciary rule.

Let’s make it clear, financial planners are NOT financial experts.

Have you noticed that many ‘experts’ are simply fee-based salespeople?

Most financial planners, advisors, wealth managers, professional managers, brokers, etc. are paid fees regardless of whether you make money. Even those who cater to the ultra-wealthy or manage family offices receive asset management fees based on total funds under management.

Look you don’t have to invest in real assets and get the amazing returns and tax benefits but whatever you do don’t invest with a financial planner!

Why?

Putting your money in an S&P 500 index fund and forgetting about it will almost guarantee you higher returns than relying on a finance professional. The S&P 500 beats financial professionals, including advisors and mutual funds, 92.2% of the time. You’re better off investing on your own and investing in an S&P 500 Index Fund!

I do not recommend any financial planner because I don’t take financial advice who is still working for a paycheck and not out of the rat race (lives in their parent’s basement) but if you must go with one of my friends or a flat-fee one – http://www.fpany.org/

I have heard of these guys/gals do their sales pitch and use fear-based words like “diversity”, “security” and “risk”where the 25-year-old kid is trying to sell random investments to me. And don’t get me started when I tried to tell them about the being your own bank concept. #FacePalm They just tried to sell a higher return (6% whoop-ti-doo) with no liquidity. Totally not what I was going for. Not saying these guys are bad people, they just don’t know any products of the Wall Street institutions.

Note: When I call out financial planners I am also calling out brokers and insurance salespeople. I repeat, never listen to a broker! If they make enough phone calls, eventually they get someone to purchase a stock and make their commission.

Don’t be another Tool who invests in mainstream retail investments. You are getting robbed with you knowing!

Share this with your co-workers & friends/family that still believe in the Easter Bunny (happy pre-Easter!) and have a false sense of security in what this financial planner says.

Who took all your money?!? We are living in the best time to be alive with all this information at our fingertips.

Why do people still choose to follow the advice from financial planners working for a commission or so-called low-cost index funds that have about a million middlemen taking the majority of your returns? Who knows, probably why 10% of people in this test are still using the “pull out method” as their form of birth control?

This is a little off topic but make sure you are still awake there because financial education is very important.

Check out this podcast with a CFP telling us of the insider secrets in the industry.

Speaking of less known tricks! Last year, I learned this cool financial hack utilized by the smart money. By being your own bank and using the “Infinite Banking Concept” you can create a dividend-paying whole life insurance. It is called Life Insurance but its just a tax code loophole to make a tax free yield in an account that is sheltered from lawsuits and creditors. I can assure you this is another thing your financial advisor or life insurance sales guys just don’t get. Likely because they are still working for a paycheck and it actually decreases their commissions.

“Fiduciary”- AKA Fid- “dushe” -iary – Means nothing more than someone is intentionally not going to screw you. Or sell you investments that put more money in their pocket.

For you, high net-worth professions still dabbling in paper assets you won’t want to miss this other trick that I will reveal on there too.

Financial advisers and portfolio managers get paid no matter what.

They make money by taking a percentage of your portfolio called an asset management fee. They have skin in the game.

Here’s how it works when things are good and the tide is floating all boats:

Your manager creates your portfolio but doesn’t really out preform the index funds

You have a gain and your manager takes 1% of that sum.

But in a bear market this is how it works:

Your manager cannot save you from a market downturn because they don’t put you in hard assets (cause they can’t get paid off of it)

You lose 20% of your nest eff and yet your manager takes 1% of the sum.

They still invite your to the customer appreciation party 😉

In bad times these managers rarely take any blame. Conventional conversation says nobody could see a downturn and we were dollar-cost averaging anyway.

If the market is good, they can take full credit for their supposed management skills.

They try to make things confusing with their complex trading systems which no one can explain in order to glorify their position and allow you to just let them drive.

No one really gets rich with Wall Street investing other than the insiders. Not retail, mainstream investors. As real estate investors, we do not buy retail (turnkey is sort of retail) but syndications and private placements are not retail.

https://youtu.be/Y1PZCSZbBDI

I only invest in things that make sense. Where the income has to exceed the expenses. And where there is a forced appreciation (not market appreciation) where you have control over your destiny.

In the end, you want to buy direct as possible. Buying REITS is the same thing as buying mutual funds with a bunch of middlemen. Crowdfunding sites remove a few layers but as a syndication working with a Crowdfunding site is very expensive way of acquiring capital. Sometimes I wonder who are the people using this high cost of private equity… Perhaps they are “desperate syndicators?”

Do you believe in the Easter Bunny?

Annuities are products of insurance companies peddled by their agents. And built upon a pyramid scheme with an older guy (which white hair) employing a bunch of young guys to find warms leads to a fancy office.

Annuities pay extremely high commissions, often 7% or higher. On a sale of a $200,000 annuity, an insurance salesperson can earn $14,000.

When you have to pay Peyton Manning and Brad Paisley to advertise your product.. I’m out.

The drawbacks of an annuity (especially the opportunity costs of buying your first turnkey rental) are often ignored by ignorant salespeople. An annuity is one of the worst investments you can make!

Insurance salespeople use scare tactics to sell annuities using terms like: 1) capital preservation, 2) diversification, 3) risk.

They claim, with an annuity, you’ll never run out of money. The one so-called advantage every insurance salesperson will tout is the guaranteed monthly income the holder will receive once he reaches retirement age. No matter the state of the economy, the salesperson touts, “you will always get paid, and your principal will not lose value.”

Protected principal and a fixed income sound nice but here is the truth…

Before we get into the drawbacks of annuities, it’s important to discuss the principle differences between the two main types of annuities, fixed and variable annuities.

Fixed annuities are very much like a bank CD. You deposit a sum of money, and the insurer agrees to pay a certain interest rate over a specified period. Supposedly, you’re protected from downside risk in that your principal is contractually guaranteed.

Variable annuities, on the other hand, are more like mutual funds and can go up and down with the market. However, there are some significant differences between annuities and mutual funds that make choosing mutual funds over a variable annuity a no-brainer.

Stock Market Scenario (2022)

With the differences between fixed and variable out of the way, here are the primary reasons why you should avoid annuities:

1. Limited Upside

With fixed annuities, in exchange for the security of a monthly income, you give up most of the upside on your investment. Fixed annuities protect principal but also limit the upside. Some fixed annuities allow the holder to participate in the upside of their investment; however, they usually cap it at around 4% per year.

So even though it’s true if the market falls 20%, the investor won’t lose any money with a fixed annuity, on the flip side, if the market gains 20%, in most cases you will not participate in the upside. If you do, you’ll be limited to 4%.

With fixed annuities, even with the highest paying offerings, the most you will top out at is 4% per year. Factoring in inflation, that 4% on your principal in today’s dollars, may not be worth much when you retire in 20 years.

2. Fees & Expenses

Some compare variable annuities to mutual funds, but there’s one big problem with that comparison. Even though you can enjoy more upside than with fixed annuities, variable annuities are saddled with additional management fees not associated with mutual funds.

These high fees, usually known as insurance costs or M&E (mortality and expense) charges, result in higher annual operating expenses than mutual funds.

https://youtu.be/8v-DiV2b6wI

Average annual expenses are up to three times higher than a typical mutual fund’s expenses, sharply reducing your future investment returns.

Example how impactful fees are:$1,000 for 40 years @ 8% = 24,523.81 => 0% fees = you keep it all$1,000 for 40 years @ 7% = 16,440.17 => 1% fees = you keep 66% of your return$1,000 for 40 years @ 6% = 11,020.97 => 2% fees = you keep 45% of your return1% in fees on an 8% return costs you 33% in compounded losses over 40 years.

3. Taxes and Penalties

Annuity distributions are taxed at ordinary rates. The monthly distribution on a fixed annuity is taxed just like interest on a CD. That fixed annuities are taxed like CDs is not unexpected. That variable annuities, invested like mutual funds, are taxed at ordinary rates when money is withdrawn should make every potential buyer of annuities run for the hills.

So on top of the already high management fees, you’ll more than likely pay more in taxes when withdrawing your money at ordinary rates instead of the capital gains rate you’d pay from withdrawals on your mutual funds. On top of the obvious tax disadvantages of investing in annuities, the various penalties associated with annuities should also deflate any enthusiasm for these products.

Annuities are contracts that require you to hold them for a minimum amount of years (i.e., surrender period) before the guaranteed payments kick in. If you withdraw your money within this surrender period, you’ll incur early withdrawal penalties. Surrender periods vary from two years to 10 or more, and the corresponding charges typically decline with time.

For example, a deferred annuity with a 10-year surrender period would charge 10 percent on money withdrawn the first year, 9 percent the second year, 8 percent the third year and so on. On top of the early withdrawal penalty, if you make a withdrawal before age 59½, you’ll be subject to a 10 percent federal tax penalty. With these types of penalties, annuities are designed to keep you in for life.

4. Their Guarantee is not Exactly a Guarantee

Unlike bank deposits that are guaranteed by FDIC for up to $250,000, annuities are not federally insured. The insurance companies themselves make the guarantees, and those guarantees are only as secure as the insurance company making them. If the insurance company goes belly up, you’ll be out of luck.

5. About That Guaranteed Income

It doesn’t sound so great when you really dig into the math. For example, if you bought an annuity at age 35 that doesn’t start paying until age 65, you’re tying up your money for 30 years. For what? The chance to make a maximum of 4% a year on a fixed annuity, taxed at ordinary rates? Variable annuities aren’t much better as outrageous fees absorb any potential upside. To illustrate how bad annuities are as an investment, especially for retirement, consider the performance of the S&P 500 over the past 30 years, which had an average annual return of 6.73%. You’d be far better off putting your money in an index fund for 30 years and letting that money compound so by retirement age, your return will far exceed the 4% return on a fixed annuity, and you will enjoy the advantage of your withdrawals being taxed at the capital gains rate instead of at ordinary rates with annuities.

Like a subpar cell phone pushed by an overzealous salesperson, annuities are subpar financial products pushed by overzealous insurance agents who stand to make a killing on commissions if they sell you one.

They prey on the fear that you’ll run out of money in retirement if you don’t go with something that pays you a guaranteed fixed income. You may want to think twice before considering annuities as an investment. I can’t think of one person annuities would benefit and the only ones profiting from them are the insurance companies and their agents selling them. Don’t fall for their incentivized sales pitch!

The hardest part of breaking up is just transferring over the money when your salty-FP does not help you and stops being your pal.

https://youtu.be/HJ89lMXLJGA

An excerpt from “Tax-Free Wealth” by Tom Wheelwright

THE MUTUAL FUND TAX TRAP

Mutual funds are the most common form of stock market investing. The problem is that mutual funds contain a tax trap that many people don’t know about. Think of a mutual fund as a pass-through entity like a partnership. The income earned in a mutual fund is not taxed to the mutual fund. Instead, it’s taxed to the investors. That might be okay if everyone entered a mutual fund at the same time. Everyone would simply report their share of gains and losses on the stocks sold in the mutual fund, and then they would see the value of their investment grow or decrease by those same gains and losses.

That, however, is not how it works. If you invest in mutual funds, you will likely buy into a fund that has been around for many years. Over the years, investors have come and gone while the fund has purchased many different stocks over those same years. The challenge comes when the fund goes to sell a particular stock. Let’s say you decided to invest in Mutual Fund A at the beginning of the year. The fund bought Stock B for $10 per share fifteen years ago. When you joined the fund at the beginning of the year, Stock B had a market value of $50 per share. The day after you join the fund, the fund managers decided to sell the stock. So there is a gain to the fund of $40 per share on the sale of Stock B.

Who pays the tax on the $40 gain? You do, even though you just joined the fund the day before. All investors who owned shares of Mutual Fund A on the day the mutual fund sold the stock share the gain. Doesn’t seem fair, does it? It gets worse.

Suppose you paid $100 per share for Mutual Fund A when you bought it in January. At the end of the year, the stock takes a dip in value and now your shares of Mutual Fund A are only worth $80 per share. You still have to pay tax on your share of the $40 gain from the sale of Stock B inside the mutual fund.

RULE #17: Mutual funds are one of the few places where you can lose money and still owe tax on your investment.

Our mastermind did a book club on this book and here are therecordings.

“Wall Street is the only place that people ride to in a Rolls-Royce to get advice from those who take the subway” -Warren Buffet s

This is a confession that I have trouble hanging out with regular people because I struggle to biting my tongue whenever I hear money myths.

Part of the problem is that people and their parents (role models) have lived this way for so long that I am fighting uphill. Combine this with confirmation bias and fragile over compensating egos who don’t have a clue what they are doing financially it’s just better to shut up and smile silently.

Many of the misconceptions out there are born from millions and millions of marketing dollars to feed the Financial Complex and commissions for misled sales-folks just trying to pay for food, shelter, and clothing.

Here are some of these myths that I want to call out in this safe SPC environment:

A 529 college saving is for the investing clueless. A 529 plan is a type of savings account designed to help pay for college-related expenses. There are two types of 529 plans: college savings plans and prepaid tuition plans where college savings plans are more typical because prepaid tuition plans come with big premiums and are not guaranteed by the state Like a 401K or other retirement accounts, it grows tax-free. By investing any after-tax contributions in stocks, bonds, or a mix of other investment options you choose you can shelter it from taxes until you can take it out if used for qualified educational expenses (undergraduate or graduate studies, including tuition, books, computers, and even room and board and now private elementary, middle, and high school tuition). Prepaid tuition plans allow you to pre-purchase all or part of tuition costs for an in-state, public college. You can also transfer your investment to a private college 529 plan that is sponsored by over 250 private and out-of-state colleges. You are essentially locking yourself into current tuition rates but the sophisticated SPC Nation knows that you are losing out on the immense opportunity costs if you invested that money instead in income producing turnkey rentals or syndications. And that brings us to the bigger issue… investing within a 529 is will get you some tax incentives but you are still investing in garbage (stocks, bonds, REITs, money market accounts, mutual funds) with the most risk and lowest returns. Other notes: be careful not to put into the child’s name because that would not be smart because they will likely like to screw off in Japan or something (unqualified and will face a 10 percent penalty tax). Also, the maximum lump sum contribution allowed before a gift tax is applied is $15,000 per year ($30K per couple if your child is so lucky to have two parents) #gratitude. If you are trying to game your FAFSA to get student loans in most cases if a dependent child or their parent owns the plan, financial aid eligibility will only be reduced by five to six percent. If the child owns the account and files as an independent, it can reduce aid by 20 percent (we told you not to do this above). You can get really tricky if a non-parental relative owns the fund, there will be no effect on financial aid — unless they withdraw the money. In this case, FAFSA sees the funds as income, and this can reduce financial aid eligibility by up to 50 percent. To avoid reducing your child’s eligibility, be sure to withdraw the money after any financial aid has been awarded. But remember you are still investing in garbage (stocks, bonds, REITs, money market accounts, mutual funds) with the most risk and lowest returns. Invest in hard tangible assets where the risk is less and returns are stronger!

Non- solicited Advice. Ever hear retirement advice from a fellow co-worker? Well if they have been there investing their money in risky stock/mutual funds or better worse the company sponsored 401K or pension plan. Why the heck would you take their advice? One of the most common pieces of advice is that they tell you if you delay your retirement to age 65, you get more money! Of course, you will because the Government has done the math and they figure many of those sorry souls will die decreasing their entitlements they have to pay out.

The tax code is written in such a way where only the first few pages of the tax code explain the tax rates. The remaining thousands and thousands of pages explains how the government will incentivize you for government stimulus activities where you can get tax breaks for them. If the government takes these tax breaks it would remove the incentive for the so-called rich (leaders in creating) business and jobs, provide housing, oil, gas, food or whatever government stimulus is needed. Learn more from our Book Club study of Tax-Free Wealth. Avoid Ordinary Income – The wealthy avoid ordinary income because you can pay up to 39.5%.

Borrowing as a Strategy for Asset Protection. Having a paid off house is the worse thing for asset protection. Everyone knows what you owe (or lack thereof) and you are a sitting duck for litigation in a country that leads the world in silly lawsuits. Encumbering your assets (hopefully good ones that produce income) in debt makes you less of a target to a predatory lawyer. PS… debt increases your return on investment as well as locks in your value because as inflation continues to rise you are paying back the balance on the pre-dated amount.

REITS are like mutual funds. There are so many middlemen taking your money with hidden fees. It is like investing in real estate just as much as drinking high-fructose corn syrup “real” soda.

-Lane Kawaoka

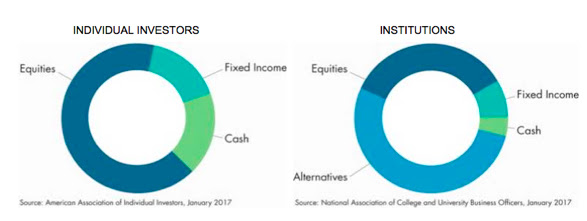

According to the 2017 American Association of Individual Investors Asset Allocation Survey, the average individual investment portfolio consisted of about 66% equity, 16% fixed income, and 18% cash.

Large institutional investors or “Smart Money” asset allocation models contrast that of the average retail investor.

According to a January 2017 report from the National Association of College and University Business Officers (NACUBO), university endowments report average asset allocations of 35% equity, 8% fixed income, 4% cash and 53% alternatives.

With 401(k)s and IRAs heavily invested in mutual funds and with investment advisors heavily skewed towards equities to drive up fees, it’s easy to see why individual investors prefer the convenience of Wall Street.

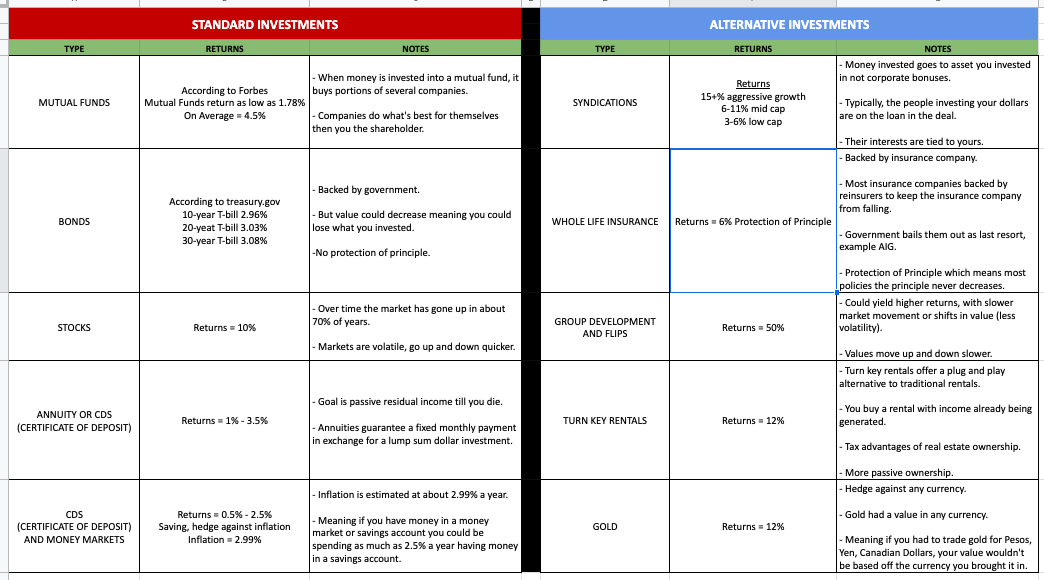

Why does the smart money allocate a majority of their assets to alternative investments? The simple answer is the returns are better.

Alternative investments are shielded from the volatility of Wall Street.

The JOBS ACT opened up the playing field is allowing more people into syndications.

First option: Cash it out and just walk away with the cash that’s in it is the obvious choice that I would recommend in most cases especially when you can put it into a turnkey rental or syndication. In that case, you obviously no longer have a life insurance policy so the death benefit goes away.. Because of the way it was designed, it hasn’t built enough cash value yet for there to be any tax consequence so she doesn’t have to worry about that..

Second option: You could borrow against this policy and use the money that way.. Basically, she could do banking inside what she currently has, the downside is that it’s not a great cash building policy so there’s more cost in it than what you’d like to see and then the loan rate may not be real favorable..

Third option: Open a new policy (one that is designed for cash build up) and do a 1035 exchange into it where you could use the policy for banking.. The nice thing here is that you would have a little cash right up front to boost the new policy.. The downside is just going through the process of getting a new policy..

So basically, if you need/want the insurance death benefit and/or would like to use the banking strategy, the best bet would probably be to get a new policy that designed for that purpose and dramatically reduced cost.. If you don’t really care about using the banking strategy then you can just cash out and walk away with no issue..

Why We Avoid Investing in Wall Street

Wall Street investments:

Is a roller coaster. Your investments are at the whim of the market. And things move so quickly.

You have little input or control. With real estate you can use insider knowledge.

Investments are retail meaning there are many layers of salesmen. Everything is based off sales commissions. The key is to get closer to the source to cut out all the layers of middlemen.

“We know what is going to happen if you keep investing in the same old stocks/mutual funds/bonds… you will keep working at your job with a lackluster retirement in 40-50 years. Invest in real estate for cashflow is a proven way that I created my pension today and allowed me to retire before I hit the age of 34. Do the math… the numbers don’t lie… people do” -Lane Kawaoka

Thank you for supporting SimplePassiveCashflow. I made this website because I was lonely and wanted to build a tribe. Join me below:

Text “simple” to 314-665-1767 to get access to the Hui Google Drive files and the 2018 Rental Property Analyzer

Please help the show by leaving a review: http://getpodcast.reviews/id/1118795347

Join the Hui Deal Pipeline Club! SimplePassiveCashflow.com/club

Pardon the grammar – I’m an Engeneer, Enginere, Engenere… I’m good with math! Here are the Show Notes:

Gets a piece of the action by leveraging your time, knowledge, and connections.

Download a free chapter in the Hui Files

Get a heloc, keep your income in the heloc and pay down your home mortgage

People depend on traditional sources

Don’t quit your job until you have the next thing going

Dolphin culture – help people without any return

Jordan Goodman has spent the past 40 years focused on one mission: to help Americans do better with their money. In a career spanning newspapers, magazines, books, radio, television, live events, teleseminars, and the Internet (www.moneyanswers.com), he has helped millions of people to solve their financial problems and realize their financial dreams.

An honors graduate of Amherst College, Jordan had just received his masters degree from the Columbia University School of Journalism in 1977 when he launched an award-winning, consumer-oriented newspaper insert, INFO, which reached 4 million readers every week. That early foray into consumer journalism soon led to an 18-year stint at MONEY, the foremost personal-finance magazine in the U.S., where Jordan reported and wrote on every aspect of personal finance. During his tenure at MONEY, he also became a regular presence on radio and television programs around the country. When Jane Pauley and Bryant Gumbel of the “Today Show” wanted to refute some of the more dubious strategies of financial guru Charles Givens in 1986, it was Jordan they asked to face down Givens. When Ted Koppel needed a financial expert to explain to “Nightline” viewers the implications of the stock-market crash of October 19, 1987, it was Jordan to whom he turned.

While at MONEY, Jordan also began to write the first of his 14 highly acclaimed books on personal finance. The Barron’s Dictionary of Finance and Investment Terms (1984), which Jordan co-authored with John Downes, has been translated into Spanish, German, Russian, Japanese, and Chinese, and has sold over 3 million copies worldwide. Now in its ninth edition, it is considered a classic in its field and a staple on the syllabi of college personal-finance and business courses, MBA classes, and securities training seminars.

In the 33 years since the dictionary was first released, Jordan has also written:

• Barron’s Finance and Investment Handbook (1986, co-authored with Downes) that provides a comprehensive analysis of every form of investment, plus a multitude of important investment resources. (The ninth edition came out in 2014.)

• Everyone’s Money Book (Dearborn, 1993, 1998 and 2001) a 970-page comprehensive financial reference that included over 6,000 resources and sold over 250,000 copies.

• The Everyone’s Money Book Series (Dearborn, 2003)

(including six separate volumes on Credit; Stocks, Bonds, and Mutual Funds; Real

Estate; College Financing; Retirement Planning; and Financial Planning)

• Reading Between the Lies: How to Avoid Becoming a Victim of Wall Street’s Next Scandal (Dearborn, 2004) aimed to educate consumers shaken by Enron-era debacles.

• Master Your Money Type (Warner Business Books, 2006) about the different psychological styles with which people relate to their finances, and how to minimize their weaknesses and maximize their strengths to build financial well-being.

• Fast Profits in Hard Times (Grand Central Publishing, 2008) that anticipated the current financial downturn and provides readers with investment strategies that allow them to make money even in a down market.

• Master Your Debt (John Wiley, 2010) which explains the many changes in the world of debt and offers specific resources to help readers pay off their mortgages in 5-7 years instead of 30 years, get control of their credit card debt, student loans and all other kinds of debt.

• The Ultimate Guide to Student Loans (CreateSpace, 2014) which explains how to save and invest before a child goes to college, how to get the best student loans when they get to college, and how to pay them off as quickly as possible after graduation.

It’s been 20 years since Jordan, in such demand as a keynote speaker, author, and guest expert on radio and television, left MONEY to focus on independent projects. He is the host of the weekly national Money Answers Radio Show which appears on the online VoiceAmerica Business Radio Network at www.voiceamerica.com. Once or more each week, he appears as a commentator on major TV news networks such as CNN, CBS, ABC, Fox News Network and Fox Business Network. During frequent trips around the country, he is a guest on local and regional radio and TV stations as well as a keynote speaker for such diverse audiences as the military, corporate employees, college students, and trade association members. He also participates in non-profit personal-finance-literacy programs such as those sponsored by the Jump$tart Coalition. And virtually every day, often several times a day, from a microphone on the desk in his home office, he speaks to millions of listeners through his regular guest appearances on countless radio shows. These include such prominent programs as “Sunday Morning Magazine” on KMOX that reaches numerous Midwestern states; KOA’s Money Monday hour with Mandy Connell in Denver, WCCO in Minneapolis with Jordana Green, WGN in Chicago with Steve Cochran.

Along the way, Jordan also has reached vast national audiences as a weekly commentator on CNN’s “Business Day” for 3 years; on Public Radio International’s “Marketplace Morning Report” weekly for 6 years; on the Mutual Broadcasting System’s “America in the Morning” daily for 8 years; and as a guest expert on NBC-TV’s “News at Sunrise” weekly for 9 years.

The son of a father who was a political-science professor for 32 years at the Ivy League’s Brown University, and a mother who was a dedicated community-service leader in Providence, Rhode Island, Jordan early on melded his father’s focus on world events with his mother’s emphasis on serving others. His parents’ formative influences, combined with his firsthand experience of a traumatic family financial crisis when he was a teenager, in large measure explain both the career path he has pursued with such passion and the reasons why he is today widely known as “America’s Money Answers Man.”

In all he does — in his books, his media appearances, his live speeches, his teleseminars, and even in the hundreds of email replies he crafts each month in response to listeners who write to ask for his advice, Jordan:

• teaches the underlying principles of responsible personal finance.

• makes clear the impact of current events on the consumer’s wallet.

• provides outstanding resources that can help the consumer to take the next smart step.

Text “simple” to 314-665-1767 to get access to the Hui Google Drive files and the 2018 Rental Property Analyzer

Please help the show by leaving a review: http://getpodcast.reviews/id/1118795347

Join the Hui Deal Pipeline Club! SimplePassiveCashflow.com/club

Pardon the grammar – I’m an Engeneer, Enginere, Engenere… I’m good with math! Here are the Show Notes:

Doing one house gets you started to gain momentum

Han solo moment was went when into MFH

At first wife was nervous in the beginning but with success came on board

Moved to MFH when had 5 units and 2k in cashflow

SFH is the way to go to learn to rent and pick out a property manager but its a personal question

Worse moment was seeing 2008

A pain point that forces people to make a change

Working up to expenses plus 20k

Do a little bit each day

Set goes every year – 40-50 goals – review once a week

Personal Background

Grew up in Oxford, Michigan

Graduated from General Motors Institute/Kettering University in Flint, Michigan in 2000 with a Bachelor’s in Mechanical Engineering

Married to wife, Lindsay and have 3 kids together

Started engineering career in 2000 and progressively moved up in position and responsibility to an engineering manager

Currently a program manager for automotive supplier Brembo

Real Estate Projects

Purchased primary residence in White Lake in 2008 as a foreclosure and rented out old primary residence in Madison Heights – “accidental landlord”

First intentional rental was a 3 bed 2 bath house in Waterford in 2011, added 3 more in Waterford from 2012-2014

Bought 12 apartment units in Monroe, Michigan in 2015

Bought 12 more apartment units in Monroe, Michigan in May 2016

In due diligence on a 63 unit apartment building in Lansing, Michigan

Goal is to retire my day job 2 years from now. From there, options I am looking into are real estate syndication and home inspecting

Success Habits

Keep a quarterly finance sheet to keep track of Net Worth, Assets, Liabilities, Income, & Expenses

List out yearly goals for family, finance, health, learning and track each week

Make sure to do things daily to get closer to goals

Dave Ramsey

Lifestyles Unlimited

REIs for networking

Checklists

Books

Millionaire Real Estate Investor – Gary Keller

Rich Dad Poor Dad – Robert Kiyosaki

The Complete Guide to Buying and Selling Apartments – Steve Berges

48 Days to the Work You Love – Dan Miller

What Color is Your Parachute – Richard Bolles

The Slightest Edge – Jeff Olson

Compound Effect – Darren Hardy

Quotes

“Leverage is key to wealth” – In regards to money, time, knowledge

“Money is on the other side of fear”

“Most people overestimate what can be done in the short term and underestimate what can be done in the long term”

“If you give a house a cookie…”

“What gets measured gets done”

“Spectacular achievement is always preceded by spectacular preparation”

“Those who say it can’t be done should get out of the way of those doing it”

“Go as far as you can see, once you get there, you will see farther”

“Play the game of money to win, don’t play not to lose”

“Don’t quit when you are tired, quit when you are done”

“Make sure your ladder to success is on the correct wall”

Contact Info

Email: bradtacia@gmail.com

Facebook & Linked In – Brad Tacia

Facebook Page – Apartment Investors of Michigan

George Ross (Trump’s legal advisor pre-presidency)

People don’t realize how long it took me to be financially free after buying my first rental in 2009. Granted I bought way too many single family homes and should have bought bigger deals sooner I now know how to accelerate the process.

But before I even had $20,000 saved up for my first down payment I was cheap… well I still am.

Looking back on the crazy stuff I did to save money, I now realize that I was trading time for money.

I still believe that saving money and being responsive is a good behavior to have. To spend your money wisely on value and not get caught up on the Hedonic Treadmill where we keep trying to keep up with the Joneses.

I started to a hobby to make Mead or fermented honey wine. It’s pretty healthy because of the good bacteria cultures.

I started it because I needed to diversify from my Kombucha hobby because moving to Hawaii I was worried that there was going to be a fruit fly infestation that would wipe me out.

Got to be diversified with multiple streams of income!

It’s been a busy month after wrapping up the closing on these two latest deals. If you are interested in the deal flow, make sure you are a part of our Hui Deal Pipeline Club.

I recently met George Ross who came to speak to my Syndication Mastermind for a private dinner. If you have need the movie “The Founder” you know the lawyer had a very big impact to Ray Kroch. George was the legal counsel to Donald Trump during his rise and “retired” once he hard Trump was running for presidency. George He held court to the remaining 15 of us for 3 hours after dinner until midnight telling stories for the past. Very insightful to know that this man shaped the Trumps business sense.

He is known as a master negotiator and he gave us the following relationship advice:

“In marriage, I tell my wife that I make all the Major decisions and she can have the Minor decisions… In all my years of marriage, we have not had one Major decision come up.”

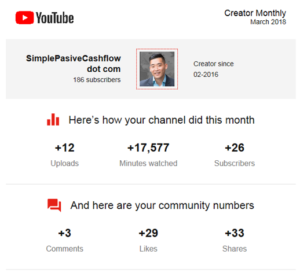

The recently launched YouTube Channel just clocked in at 17,577 minutes or 293 hours or 36 working days. So there much be one person watching my content around the clock which on the clock.

I need a little bit of a break and took the time to reflect back on how far I have come from 2009 and buying that first rental property. By the way remember to incorporate “play” into your day.

The first twenty tips came from myself but after sharing the list and finding the other ex-cheapskates out there we have been slowly syndicating more and more bad ideas. Note: they are not in any particular order.

Our parents will be so proud of us!

If you want to add more, please email me and I will keep growing the list. And if you like I can add you initials at the end to cement your legacy.

If you call me collect, I will not pick up!

UPDATE 19.06.17 – In some respects I still wear the cheapo badge like a old war medal. The truth is that cheap/easy/free people rarely get anywhere. It took me 7 years to get to 11 units on my own. I was not until 2016 where I started to invest serious money into mentorship, traveling, and connecting with people. Little do cheap/easy/free people know is that others see right through them and it surfaces as textbook scarcity mindset which repels the right people.

Money saving ideas for the shameless… (the before)

Stack Mr. Rebates shopping portal and Groupon discount codes with gift cards purchased from eBay or Safeway with more gift cards and Mr Rebates shopping portal. To sign up go here: http://www.mrrebates.com?refid=413597

Take a shower at work to save on utilities, water, and electricity – as a side benefit you go to the gym more often (do your 3S’s there, shit, shower, shave)

If you work in a startup company that caters food, it’s a no brainer— eat at work and bring food home. Maybe you can even befriend someone that works there and join them for lunch from time to time. For extra credit consider a life of “intermittent fasting” and totally binge at these free meals.

Wash your car in the rain. No mineral deposits left while it dries. Video of me demonstrating this: https://youtu.be/kZkYnkXOI7Q

Costco leasing to own program

Buy an Anker powerbank and charge it at work. Sadly I never got around to use them during what little time I had at home 🙁

I would sign up for Microsoft play-tests so I could get a free software to then sell on eBay for money. The sad thing is that I am not even a gamer and it was completely obvious to the playtest team.

Always take a pee before leaving for the day.

Try to poop at the same time every day while at work… get paid to poop. Time is money and flushes cost 10 cents.

There are soft drinks available at restaurants?

Why are you eating at a sit down restaurant, you have to pay tip?

If you must, order food to go and eat on the premises. Best of both worlds!

Wear clothes with the tag on it and return it.

Buy a snorkel from Costco to go to Hanama bay while visiting Hawaii to return it. Another Hui member cautions that on many electronics there is a 90-day return policy. Lady who returned a dead Christmas tree on Jan 4th.

I rode my dangerous 50cc moped in the Seattle rain so I would not have to pay $4 per galleon in 2010.

Use an app like GasBuddy to find the cheapest gasoline station, better yet, double stack your Costco credit card (4% cash back on gasoline) and buy Costco gas.

This one is a bit morbid, but an important one. Set up a revocable living trust with your lawyer to avoid probate expenses following the death of your family members\

Susie Orman’s advice – make coffee at home and save yourself the $5 Starbucks Vente frappucino

FAST (intermittently, not forever)! Skip breakfast daily (work yourself up gradually) and when you’re ready to get to the big leagues, attempt to fast for an entire day (no breakfast, lunch or dinner)

Maximize and optimize what you’ve got BankPurely has a 1.30% APY since April (not sure if promo rate?) but most banks have 1.0+% (which is 10x the 0.1% APY rate given by most conventional brick and mortar banks like BofA, Chase, WellsFargo)

Use Honey or Ebates or other discount portals for Amazon/eBay or other internet purchases to save a few %

Certain credit cards provide 5x bonuses (Chase Freedom has rotating categories) and Chase Business cards are good for auto-pay things like internet with extra bonus categories

2) go back to tahoevine’s deal manager page to put in the order #

3) once the stuff arrives, wait 7 days to write a review on it (it has to be a positive review and you get better ratings if you include photo and/or video)

4) copy the link of your review into tahoevine’s deal manager

5) get the full refund a day later via paypal.

A bought a bunch of random stuff (mostly dog stuff lol) just to test it out but so far it’s been working like clockwork:

Save the money by not sending them to private school (for the supposed network) instead just buy them a crappy car un college and have them give the rich kids to and from the parties. Its like grain finishing grass fed cows.

Growing up in Hawaii where a gallon of milk is $8, I was taught to save money in strange ways. (I don’t drink milk)

Some of those were pretty bad which develop into unhealthy money mindsets and can translate to negative social profiles.

Some downright unethical but hey if you are a cheapskate, own it!

I don’t condone any of these tactics but look, it is no coincidence why you folks continuously have so much money to invest and pay your bills on time unlike 4 out 5 of my Birmingham rentals every month.

Trading money for time… (the Recovery) – updated 11/8/18…

Using disposable chopsticks, plates, bowls, clubs, and forks to minimize time to wash dishes and put away. Also need less space for more of this “stuff”. I think we do not realize how much not only time we waste on this but water and electricity go into this.

Use Uber as much as I can to minimize stress, the chance of an accident, 50 cents a mile per the IRS in wear and tear to your vehicle but most importantly you can bring your laptop and get some work done.

Leasing a car – such a great decision. Its fun, the numbers make sense if you are able to grow your money at more than 14% a year, and don’t have to deal with any maintenance issues.

Eat out. It just tastes better too. And no cleanup, prep, grocery shopping, etc.

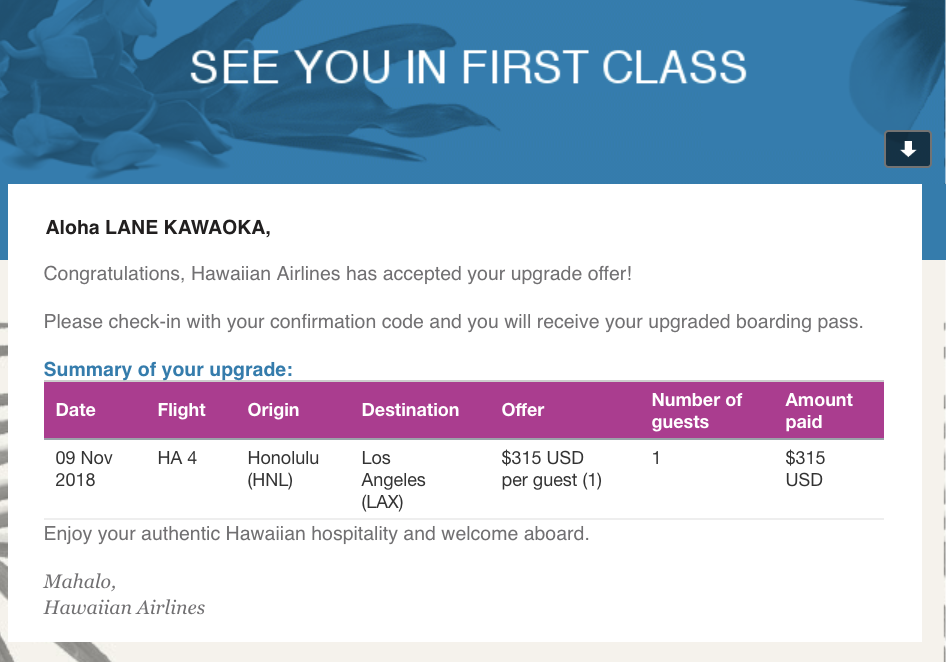

I used to be notoriously known for taking a red-eye flight from Hawaii (save on hotel) to the mainland and start the next property trip or conference the next day. Late in 2018, I decided to really upgrade to first class (pay $300 of my own money as opposed to using some kind of credit card travel hack or using my frequent flier status when I was once a corporate slave).It felt good but I believe more for paying for value and will only do it when I need it

It felt good but I believe more for paying for value and will only do it when I need it

It felt good but I believe more for paying for value and will only do it when I need it